Comments from the Swiss National Bank chairman signal that he does not understand the bitcoin market or is strategically downplaying it.

Today, a report emerged indicating that Chairman of the Swiss National Bank (SNB) Thomas Jordan commented on the liquidity of the “cryptocurrency” market.

“Cryptocurrencies are not liquid enough for the bank to have as one of its investment assets,” Jordan said.

While the chairman did not mention bitcoin by name specifically, bitcoin is by far the most liquid asset in the cryptocurrency market, and is the only logical choice for the central bank to add to its balance sheet among all “cryptocurrencies,” so it stands to reason that he is dismissing bitcoin’s liquidity.

In its 2020 annual report, however, the bank reported an asset allocation of 91% foreign currency investments, 5% gold, 1% Swiss bonds and 3% miscellaneous assets, totaling 999,027,900,000 CHF (or $1,094,506,994,458).

Digging into the report, and SNB’s strategy in general, it becomes clear that Jordan does not understand bitcoin, its liquidity or its position in relation to the investment assets that he does consider to be “liquid enough.”

“The most important element for managing absolute risk is broad diversification of investments. Risk is managed and mitigated by means of a system of reference portfolios (benchmarks), guidelines and limits. All relevant financial risks associated with investments are identified, assessed and monitored continuously. Risk measurement is based on standard risk indicators and procedures. In addition to these procedures, sensitivity analyses and stress tests are carried out on a regular basis. The SNB’s generally long-term investment horizon is taken into account in all of these risk analyses…

The currency reserves are mainly composed of gold, bonds and shares. The diversification effects achieved by adding shares to a portfolio, as well as equities’ high liquidity, make them an attractive asset class for the SNB. Furthermore, given that expected return is higher on shares than on bonds, this asset class helps to preserve the real value of the currency reserves.” -SNB’s 2020 annual report.

With the Swiss franc strengthening over the past two decades, SNB has engaged in the practice of printing francs to buy dollars (and other foreign currencies), and to buy dollar-denominated assets, including a large number of U.S. equities.

To claim that “cryptocurrencies” (read: “bitcoin”) are not liquid enough to invest in is laughable. In what CEO Elon Musk called a recent test bitcoin’s liquidity, Tesla netted a $272 million profit on its recent investment.

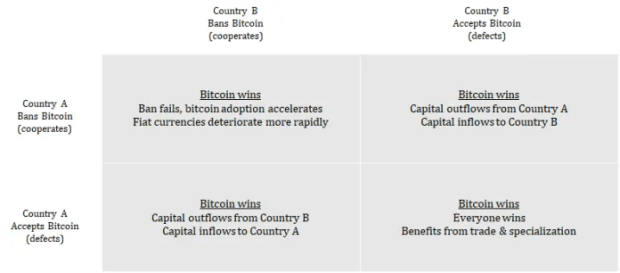

It is clear that Jordan is attempting to downplay what is really occurring: Central banks are being displaced and disrupted by superior technology in real time, and the game theory suggests that they should further accelerate their own demise by accumulating the world’s first and only absolutely scarce monetary asset.

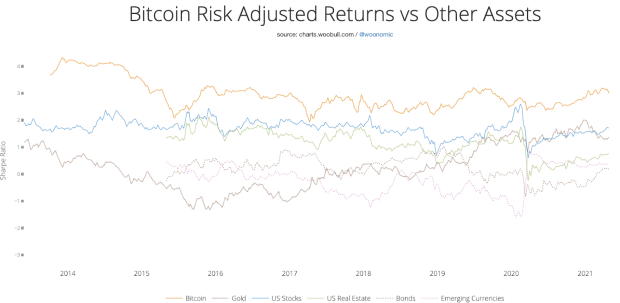

If the SNB was truly interested in mitigating risk through diversification, as well as investing with a “long-term time horizon,” it would start accumulating bitcoin, and most likely not disclose the action. The numbers don’t lie, bitcoin as an asset is actually the least “risky” in terms of risk-adjusted returns.

The game theoretic adoption of bitcoin at a nation state and central bank level has yet to begin. No one is better than their incentives, and the incentive of being an early adopter of bitcoin at a central bank and sovereign level is too strong. Expect central bank accumulation of bitcoin, even while they denounce it.

For bitcoin HODLers and stackers everywhere, let’s hope Jordan is truly oblivious, and does not yet realize that he doesn’t have a choice whether or not to buy bitcoin, but rather can only choose at what price to buy it.

{kind=link}