Key Takeaways

- The Oasis Network is designed to be a privacy-focused, scalable, Proof-of-Stake (PoS) Layer-1 smart contract platform that is Ethereum Virtual Machine (EVM) compatible.

- The network’s value proposition is its multi-layer modular architecture that enables the scalability and flexibility to deploy low-cost privacy-focused smart contracts.

- Given the size of the Layer-1 smart contract economy, there is a significant opportunity for the network to accrue value.

- The launch of the Emerald ParaTime and the resulting launch of DeFi applications sparked noticeable network activity at the beginning of 2022.

- Launching the Cipher ParaTime in Q2 2022 is anticipated to bring confidential smart contracts into existence and drive new use cases within DeFi.

- The Parcel ParaTime is a set of privacy-first, data governance APIs designed to give users better control of their data and enable developers to deploy an isolated compute environment for privacy-preserving analysis.

- A growth strategy consisting of an ecosystem fund, grants programs, developer accelerators, and community initiatives is in place to support ecosystem growth.

The Layer-1 smart contract platform race for market share and adoption turned into an all-out sprint as use cases expanded and alternatives to the Ethereum network experienced exponential growth through the end of 2021. Networks like Terra, BNB Chain, Fantom, and Avalanche witnessed unprecedented growth in average daily network transactions, active daily addresses, market capitalization, and total value locked (TVL). Much of the growth can be attributed to the competitive forces shaping traditional industry strategies that resemble Michael Porter’s Competitive Strategies. Congestion on the Ethereum network, the slow rollout of Layer-2 scaling solutions, the ability to bridge assets cross-chain, and the ability to execute smart contracts on more efficient networks allowed new alternatives to gain a competitive position as differentiated solutions and cost leaders.

While Layer-1 platforms exhibit many fundamental differences, almost all of them aim to solve the blockchain trilemma by attaining adequate decentralization, scalability, and security while hosting smart contracts. While their smart contracts inherit blockchain’s data availability and security, they also inherit its lack of confidentiality. Layer-1s do not currently support privacy on their public networks as all records are logged on the blockchain, allowing anyone to read their contents. This presents privacy concerns, due to the possibility of linking ledger addresses to real identities. As adoption grows, users may start to prefer privacy surrounding their activity or sensitive data. This lack of confidentiality, in a sense, could potentially be considered a fourth problem for Layer-1 platforms to solve, and perhaps a “quadrilemma” is on the verge of sparking the next leg of the race towards adoption.

As adoption continues, new platforms with privacy solutions may start to experience the exponential growth realized in the recent past. One such platform, the Oasis Network, is a Layer-1 that aims to solve the trilemma and do so with the flexibility to host privacy-enabled smart contracts. With its unique architecture and deployment of confidential computing technology, the Oasis Network is planting the seeds for growing an open, data-responsible economy with privacy.

Background

The Oasis team was formed in 2018 and consists of contributors from around the globe with diverse backgrounds ranging from start-ups to traditional finance and tech companies. The team also has strong roots in academia. Dawn Song, a professor at the University of California, Berkeley, known for her research in computer security and artificial intelligence, is the Founder of Oasis Labs. Oasis Labs is an active member of the Oasis Ecosystem, and one of the early contributors to the Oasis technology. The team raised funds from well-known venture capital firms and investors such as Andreessen Horowitz (a16z), Polychain Capital, Pantera, and Binance Labs, among others, to support the network’s initial development. After the private testnet launch in 2018, the public testnet underwent various iterations alongside bug bounties, audits, and network upgrades before the public mainnet launch in 2020. Fast forward to today, and it has since gone through additional technical developments and an ecosystem expansion that includes a $200 million ecosystem fund while becoming the second-most commonly held asset by crypto funds as of Q4 2021.

Source: Oasis

At the onset, the Oasis Network was designed to be a privacy-focused, scalable, Ethereum Virtual Machine (EVM) compatible Proof-of-Stake (PoS) smart contract platform. Its privacy and scalability features are designed to advance DeFi and Web3 by creating a new type of digital asset called Tokenized Data. Unlike existing tokenized data solutions at the application layer, the Oasis Tokenized Data solution is at the network layer, allowing applications to build on top of and harness the benefits of its confidential compute technology. Collectively, the design is intended to allow users to take control of and monetize the private data they generate, thereby incentivizing what Oasis calls a data-responsible economy.

Network Architecture

Overview

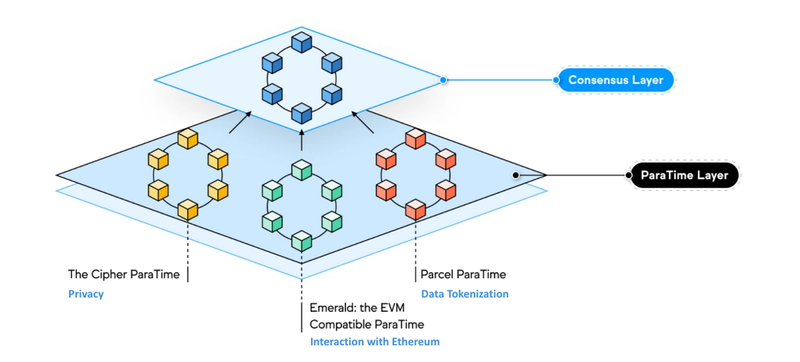

The Oasis Network utilizes a modular architecture that separates consensus and smart contract execution into the Consensus Layer and the ParaTime Layer, respectively. Both layers are integrated to provide the same functionality of a single network. However, separating these layers allows ParaTimes to process transactions of different complexity in parallel with shared consensus. With this flexibility, workloads and upgrades processed on one ParaTime will work symphonically with consensus to independently ensure network security and finality without impacting other ParaTimes.

Source: Oasis

Consensus Layer

The Consensus Layer accepts updated state hashes from ParaTimes and writes them into the next block of the Oasis blockchain, while ParaTimes operate as separate networks that can be configured and customized to run specific applications. The network’s two-layer modular solution addresses both security and scalability. While the flexibility to develop ParaTimes in isolation supports scalability, it also enables specific execution solutions such as confidential computation technology to address smart contract privacy concerns.

Source: Oasis

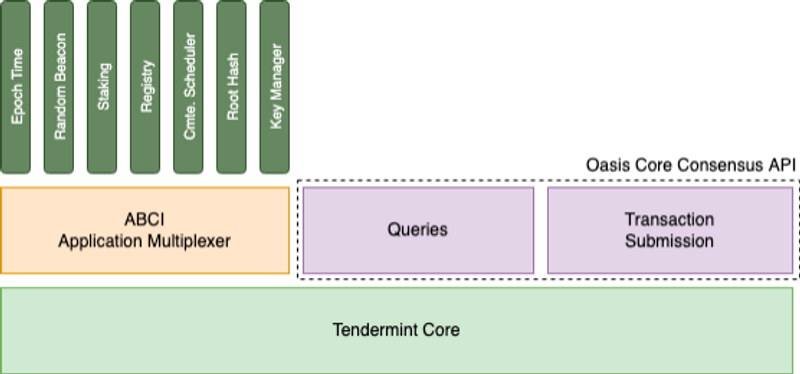

The Consensus Layer is the foundation of the Oasis Network and, in and of itself, is designed around the principles of modularity, which allows for agnostic consensus such that it can be interchangeable with any consensus logic in the future. Currently, the base layer consists of a modified version of Tendermint Core, a Byzantine-Fault Tolerant (BFT) consensus engine. It uses a PoS mechanism and a decentralized set of validator nodes and node operators. The validator nodes are randomly selected to form a committee that accepts state hashes from ParaTimes, maintains the public ledger, and ultimately secures the network. The committee’s size dictates the security of the Oasis blockchain and is currently set to 110 validator nodes. Further, unlike most consensus layers, node operators run distinctive types of nodes that are tasked with providing a minimal set of services (e.g., staking and registry) specifically for ParaTime functionality.

The Consensus Layer Beyond Tendermint Core

As the Consensus Layer diagram above illustrates, the multiple layers of consensus begin at the top, with the nodes tasked with providing a minimal set of services. These services range from maintaining epoch-based time-keeping services to coordinating key manager runtimes and storing and publishing policy documents and status updates required for key manager replication. This multi-node architecture aims to reduce complexity and, ultimately, the risk of computational errors at the execution layer.

Further, Tendermint Core consumes consensus logic via the Application Blockchain Interface (ABCI), the interface between Tendermint and a single application. Since the Oasis Network has multiple services that need to be provided by the Consensus Layer, it uses an ABCI application multiplexer which performs some common functions and dispatches transactions to the appropriate service-specific nodes. This is how core consensus is able to interact with each of the service nodes.

Core Layer Staking and Consensus Voting Power

The current voting power mechanism is stake-weighted, which means the consensus voting power is proportional to its stake. In this model, the network will require signatures by validators representing greater than two-thirds of the total stake of the committee to sign a block. Note that in Tendermint, a validator’s opportunities to propose a block in the randomly generated block proposer order are also proportional to its voting power.

Validators must stake a minimum of 100 tokens to contribute to the network’s security. Each registered entity can have at most one node elected to the consensus committee at a time. The chance of being selected for the committee will be proportional to a validator’s stake weight (self-stake amount plus delegated stake).

The network currently targets an inflation rate between 2% and 12%, with validator reward amounts dependent on the length of time staked. To be eligible for staking rewards in a given epoch, a node needs to sign at least 75% of blocks in that epoch.

The network will only slash for double-signing. Double-signing penalties will result in the loss of the minimum stake amount and a frozen node. Freezing the node is a precaution to prevent the node from being over-penalized. The network will not slash for liveness or uptime. Oasis requires a 14-day unbonding period if validators or delegators move their staked funds. During this time, staked tokens are still at risk of getting slashed for double-signing and do not accrue rewards.

ParaTime Layer

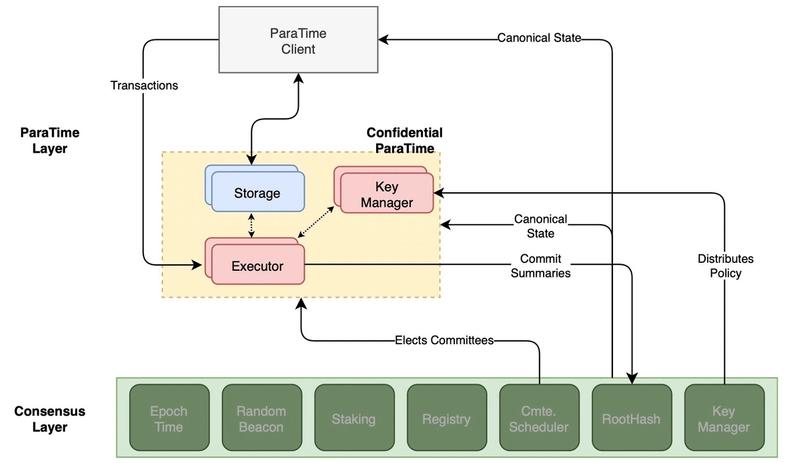

The ParaTime Layer is the smart contract execution layer that consists of multiple, parallel ParaTimes, each representing a computing environment with a shared state. Operating a ParaTime requires the participation of node operators, who contribute nodes to an open or closed compute committee in exchange for rewards. Oasis uses discrepancy detection to verify ParaTime execution. This verifiable computing technique permits the use of smaller committees and requires a smaller replication factor for the same level of security, which, according to Oasis, is more efficient than sharding or parachain models. The two key features include (1) random selection of compute nodes from a population to form a compute committee and (2) only accepting the results if all committee members agree. If there is a discrepancy, a separate protocol called “discrepancy resolution” is enabled, serving as another security parameter. In a sense, smart contract execution functions similarly to the Consensus Layer and its use of node operators and a compute committee. ParaTimes can be operated by anyone and can have their own reward system, participation requirements, and structure; meanwhile, node operators can participate in any number of ParaTimes.

Source: Oasis

As described previously, the separation from consensus allows the network to address scalability through its modular design. The separation also allows ParaTimes to be different from each other. One difference is the ability to run confidential ParaTimes or non-confidential ParaTimes, with the latter being similar to Ethereum and other alternative Layer-1 networks. Furthermore, ParaTimes can evolve independently while maintaining consensus even as security, scalability, or privacy technologies advance. In other words, the network can maintain a public ledger while having an ecosystem of separate ParaTimes that can evolve with technological advancements, allowing it to adapt and serve future use cases. Beyond confidentiality, Paratimes have the flexibility to configure parameters such as the size of the committee’s performing execution, which relates to the level of security a user needs to satisfy particular business requirements. Further, ParaTimes can run different VMs such as EVM or Rust-based smart contracts and can be designed to be permissioned or permissionless systems. Ultimately, ParaTime customization and flexibility allow developers to strike the desired balance between security, performance, and privacy.

Confidential ParaTimes

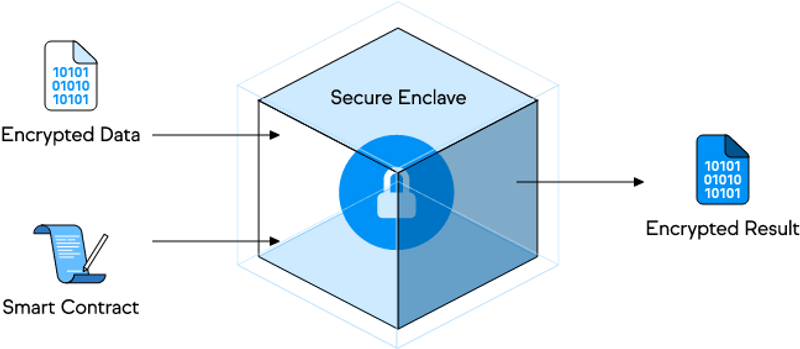

Privacy-enabled smart contract execution is one of the core value propositions that Oasis is known for. Cipher, an upcoming ParaTime, will support confidential smart contracts. In a confidential ParaTime, nodes are required to use a secure computing technology called a Trusted Execution Environment (TEE). TEEs are analogous to a black box for smart contract execution. With the use of key management (illustrated in the ParaTime Layer diagram above), encrypted data goes into the black box (i.e., Secure Enclave) along with the smart contract, where the data is decrypted, processed by the smart contract, and then encrypted before it is sent out of the black box. This process ensures that data remains confidential and is not disclosed to the node operator or application developer. Other secure compute technology, such as Zero-Knowledge Proofs (ZKPs), can also be used to execute private smart contracts. The interchangeability of secure compute technology is an additional example of modularity and value proposition at the ParaTime Layer.

Source: Oasis

The ROSE Token

The ROSE token is the Oasis Network’s native token used for transaction fees, staking, and delegation on the Consensus Layer and for smart contract operations that require fees on the ParaTime Layer. The token is also anticipated to be used for network governance, which is currently being modeled to be a hybrid off- and on-chain mechanism whereby changes to the network will be determined democratically by node operators. Voting power is anticipated to be based proportionally on self and delegated stake.

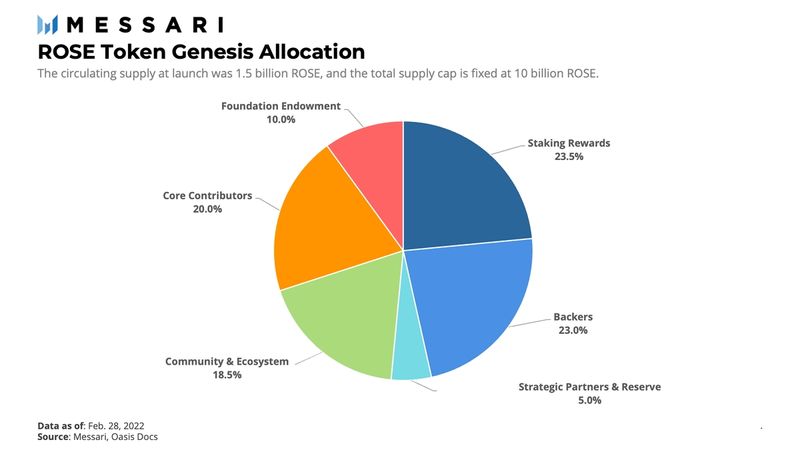

Suppose the network’s value proposition of privacy allows for continued traction. In that case, the token will likely accrue value from increased protocol revenue, the expansion of network infrastructure and node operator stake, and demand for governance stake. The token itself has a fixed supply of 10 billion ROSE. Not all tokens were released publicly on mainnet launch. Due to release schedules and locks, only a fraction (1.5 billion ROSE) of the total existing token supply was introduced into circulation at mainnet launch.

As a percentage of the total existing token supply, the quantity of ROSE tokens reserved for various network functions follows the allocation below.

Backers: Between 2018 and 2020 Oasis raised over $45 million from well-known investment funds that acquired 23% of the total supply cap at network launch.

Source: Oasis

Core Contributors: As compensation to core contributors for contributing to the development of the Oasis Network, 20% of the total supply cap was allocated at network launch.

Foundation Endowment: With the initial 10% allocation of the total supply cap, the endowment to the Oasis Foundation is tasked with developing and maintaining the Oasis Network. A portion of the Foundation tokens not introduced to the circulating supply at launch are staked on the network. Foundation staking rewards go back into the network via validator delegations, network feature development, and ecosystem grants.

Community and Ecosystem: Funding programs and services that engage the Oasis Network community, including developer grants and other community incentives by the Oasis Foundation, initially held 18.5% of the total supply cap.

Strategic Partners and Reserve: Funding programs and services provided by key strategic partners in the Oasis Network initially held 5% of the total supply cap.

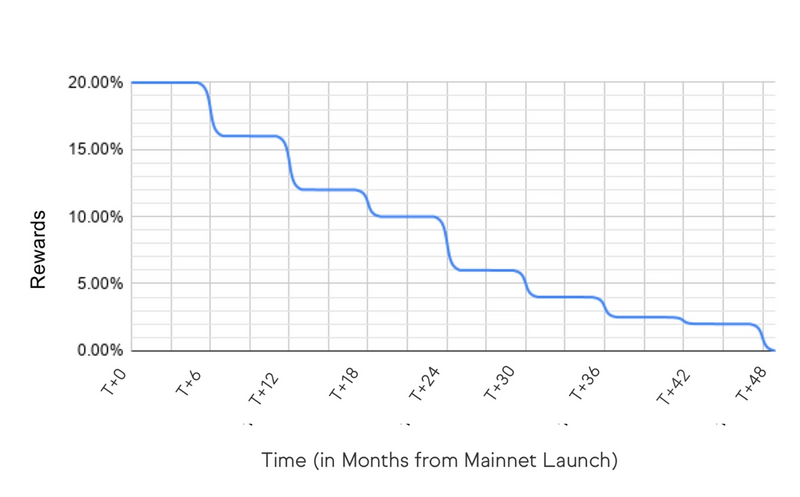

Staking Rewards: On-chain rewards are set to be paid out to stakers and delegators for contributing to the security of the Oasis Network. Approximately 2.35 billion ROSE (23.5% of the supply cap) will be paid out as staking rewards to stakers and delegators over four years. Rewards will be disbursed by on-chain mining mechanisms, calculated based on how many blocks are produced, how many nodes are participating in staking, and how many tokens are staked.

Source: Oasis

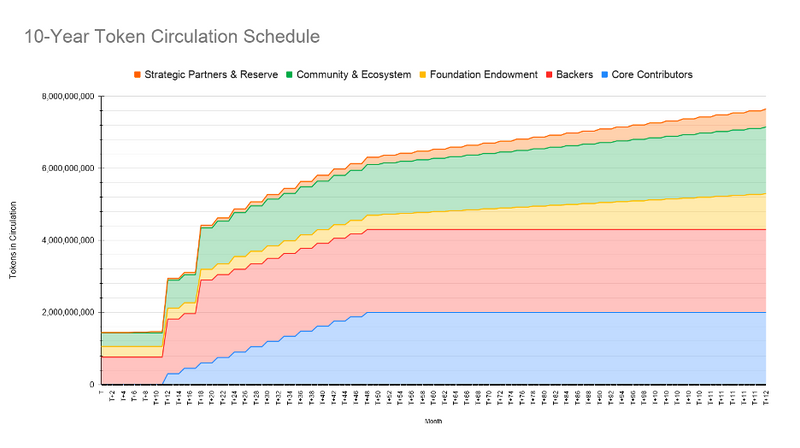

The tokens not allocated for staking will be disbursed according to the following 10-year release schedule:

Source: Oasis

The token supply curve above begins at launch, which occurred in 2020. A rapid increase of unlocked tokens began after 12 months and began to level off recently in the 15th month. In 2024, the token supply release will experience a further leveling until hitting its plateau in the 10th year.

Current State and Glimpse into the Oasis Network Ecosystem

Current State

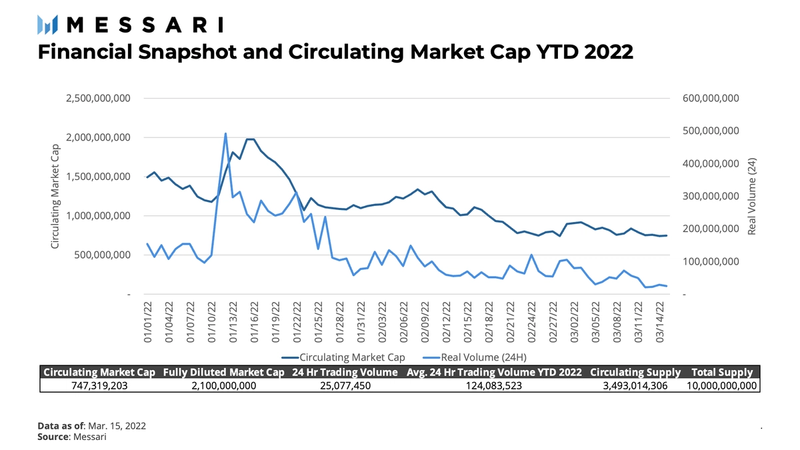

Like many digital assets, the ROSE token has declined in valuation by ~50% year to date (YTD), along with a decline in trading volume across exchanges. The top three trading pairs by volume are trading on Binance (USDT, BUSD, BTC) currently making up ~45% of all ROSE trading volume.

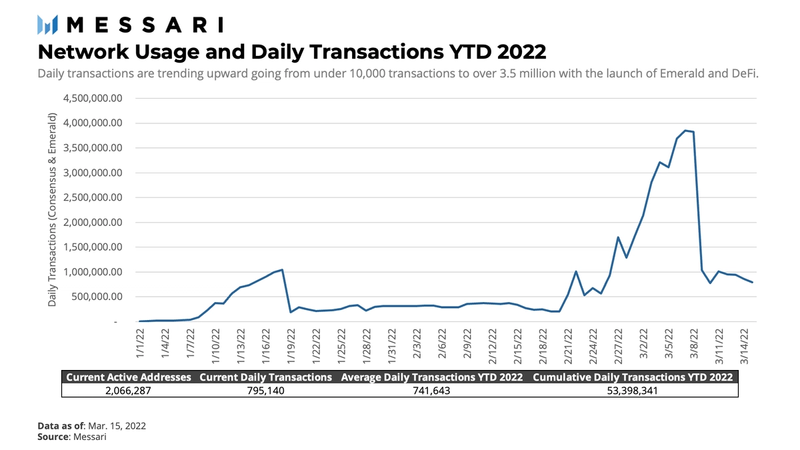

While trading volume has declined, liquidity of the ROSE token is still relatively healthy, with daily trading volume ranging between $100 million to $500 million, equating to ~$125 million in trading volume on average YTD. Though valuation and trading volume metrics have experienced a downward trend, network usage has experienced a noticeable upward trend.

At the beginning of 2022, the Consensus Layer of the network was averaging below 10,000 transactions per day. By the middle of January, transactions grew to greater than 140,000, representing an approximate 2,600% increase. Current daily transactions of 110,000 are outpacing the YTD average of 100,000, which also indicates an upward trend. As of March 15, 2022, consensus consists of 153,000 active addresses and has processed 7 million transactions in the aggregate. Further, Emerald launched this year and has generated as many as 3.8 million transactions in a single day and is averaging about 650,000 transactions per day.

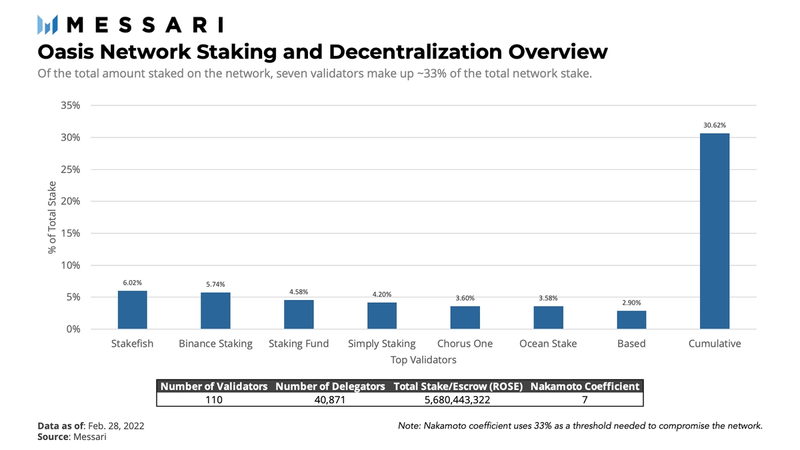

Beyond market data and network usage, the network infrastructure has grown from 100 active validators to 110 and has witnessed evolving decentralization metrics.

Currently, seven validators contribute to just under ~33% of the network’s total stake. The methodology behind the Nakamoto Coefficient assumes 33% is the threshold of total stake needed to compromise a network. The higher the coefficient, the more secure a network is deemed to be as it would require a greater number of validators to collude against the network. Given this methodology, the Nakamoto Coefficient of Oasis is similar to other Layer-1 networks, even though most others launched before Oasis, allowing for more time to decentralize their networks. Only time and adoption will determine the extent Oasis Network grows validator sets and a more diversified distribution of stake.

Ecosystem Overview

There may be a reason why the Oasis Network’s token symbol is ROSE.

Source: Oasis

An oasis is a fertile place in an arid environment. The water it provides turns into a thriving ecosystem of plants and animals. In the same way, the Oasis Network provides the resources for applications to build DeFi services and new use cases. Evaluating Oasis Network’s current state is a starting point for assessing the ecosystem. Given recent developments and anticipated value propositions to come, following along to see whether it succeeds at thriving will be top of mind as we look ahead into 2022.

A key driver of recent growth was the result of launching the Emerald ParaTime. Emerald is the EVM-compatible system essential for Solidity-based smart contract execution. Having EVM compatibility and Solidity support means that any token developed for Ethereum can be migrated through existing bridge infrastructures like Wormhole, cBridge, and Multichain, which also went live earlier this year. Emerald also allows the ERC-20 token standard to run natively on the Oasis Network. Ultimately, the launch of Emerald brought a flurry of DeFi activity to the network, which is reflected in the increase of daily transactions at the beginning of 2022.

DeFi on the Oasis Network

Source: Oasis

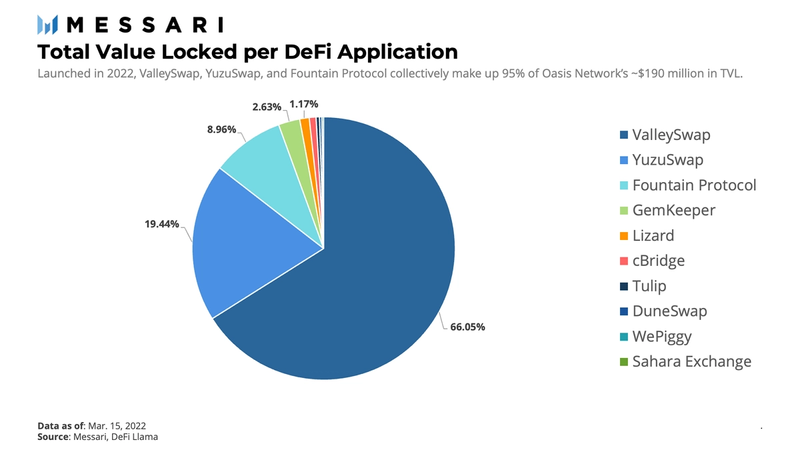

Along with Emerald, the network launched DeFi infrastructure including the Oasis Wallet for the ROSE token, and it also integrated with bridges like Multichain. This sparked the network’s first DeFi application, YuzuSwap (YUZU). YuzuSwap is the network’s first community-developed decentralized exchange (DEX) that offers users low-cost trading services. The DEX allocates 20% of all transaction fees to the YUZU DAO where holders of the YUZU token can use those funds to incentivize further protocol growth. Within a month of launch, YuzuSwap exceeded $100 million in TVL and $1 billion in trading volume.

Another major contributor to recent growth is ValleySwap (VS), a DEX that launched as recently as February 24, 2022. The launch of ValleySwap clearly generated a renewed uptrend in network activity at the end of February as daily transactions spiked at that time. As of March 15, YuzuSwap and ValleySwap are producing ~$1–3 million in daily trading volume and have accrued $37 million and $125 million in TVL, respectively.

The third-largest DeFi application on Oasis is Fountain Protocol (FTP), the network’s first lending protocol. It launched with 200,000 FTP in incentives and generated over $7 million in TVL in its first day. Using Fountain, users can experience one-stop management of DeFi assets with high capital efficiency and take advantage of the low-cost Oasis Network. As of March 15th, Fountain Protocol is the third-largest DeFi application on the Oasis Network after growing to $17 million in TVL.

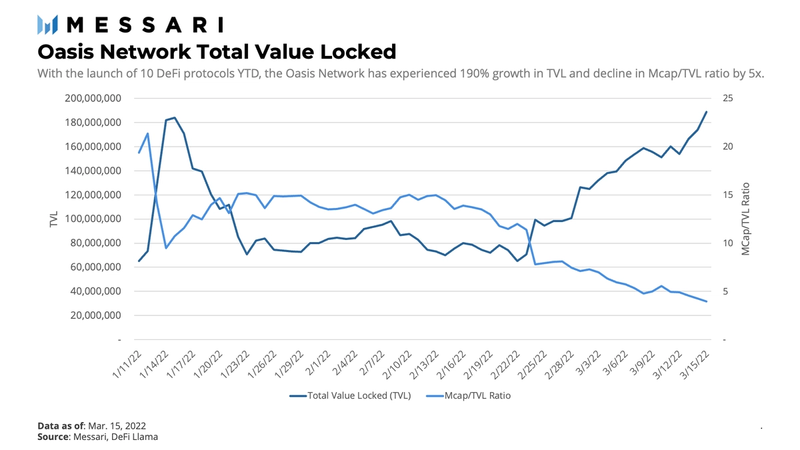

With the launch of these DeFi protocols, the Oasis Network not only saw an increase in daily transactions but rapid growth in TVL.

Intuitively, the market cap to TVL ratio declined as the market cap declined by 50%, and TVL increased by 190%. This fundamental ratio represents how a network is valued relative to value locked. If the ratio is a large number, the network value is viewed as being overvalued. In other words, a network with an MCap/TVL below 1 represents a network value that is less than the capital locked in the entire network. Given that the network was carrying a nearly $1 billion market valuation before the launch of DeFi, it makes sense to see such a drastic decline in the ratio after the resulting growth of TVL.

The Ecosystem Beyond Emerald

Oasis Network is launching two additional ParaTimes that go beyond Emerald. The Parcel ParaTime and the Cipher ParaTime. Parcel is the system that stores, governs, and computes confidential data. By integrating Parcel SDK into their applications, developers can incorporate privacy-preserving data storage, governance, and computation. This ultimately serves as the Tokenized Data engine, which can convert any data file into an NFT.

With Parcel, the Oasis Network intends to foster a responsible data society using Tokenized Data. Data providers on the Oasis Network will be able to put their Tokenized Data to use by earning rewards from applications that analyze or control how their sensitive information is used on different services. This concept differs from the data ownership we are familiar with today in that data is not monetized or controlled by those who generate it.

Source: Oasis

Currently, Parcel is a permissioned ParaTime for use by enterprise partners such as Binance, Genetica, and BMW. Binance is one such partner that has engaged with Oasis to combat bad actors across various exchanges. With theft and attacks as prevalent events in crypto, exchanges need a platform to identify and ban bad actors. Oasis and Binance created the CryptoSafe Platform to enable exchanges to share threat intelligence data. Using the network’s confidential compute feature, exchange data can be kept confidential even when compared across exchanges. While Parcel is currently a permissioned network, it is anticipated that it will become permissionless by the end of 2022, bringing Tokenized Data into public reality.

Further, the third piece of the puzzle is the Cipher ParaTime. Cipher is the confidential smart contract system set to launch at the end of Q2 2022. Cipher is a core value proposition of Oasis that will support WebAssembly smart contracts that make confidential compute possible.

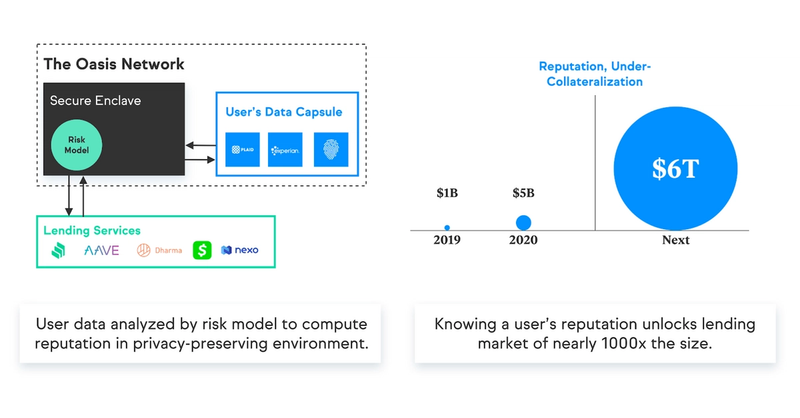

When the additional ParaTimes launch, they have the potential to open the network to an ecosystem aimed at privacy-first DeFi, including privacy-preserving decentralized exchanges. To that end, they are designed to make it easier for DEXs to prevent front-running transactions, for NFT users to protect their assets privately, and for them to hypothetically unlock more value from traditional credit and lending markets seeking confidentiality. An example of how DeFi applications can unlock the value of Parcel and Cipher is depicted below.

Source: Oasis

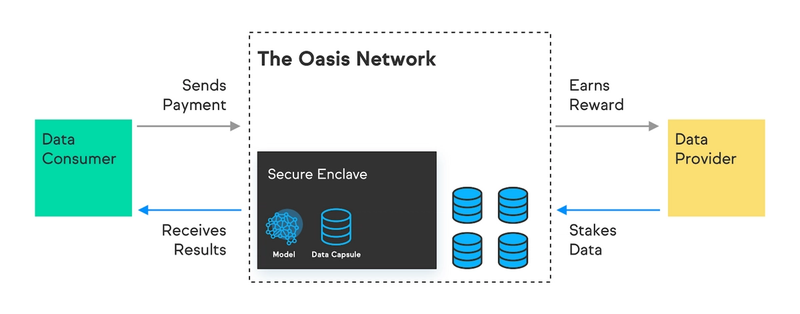

In this example, users will be able to utilize Cipher and a Trusted Execution Environment (TEE) to protect their private data while monetizing and disclosing private data to various DeFi services through the power of Parcel. For example, a user’s risk profile and reputation could be used such that lending services can manage risk and gauge appropriate collateralization requirements. With this knowledge, lending services like Aave could offer under-collateralized lending based on credit-worthy reputations. It will be interesting to track their adoption and usage as the market opportunity for these ParaTimes is substantial. Additional use of these ParaTimes may also generate or supersede the network activity as their Emerald counterpart did in early January.

Competitive Landscape

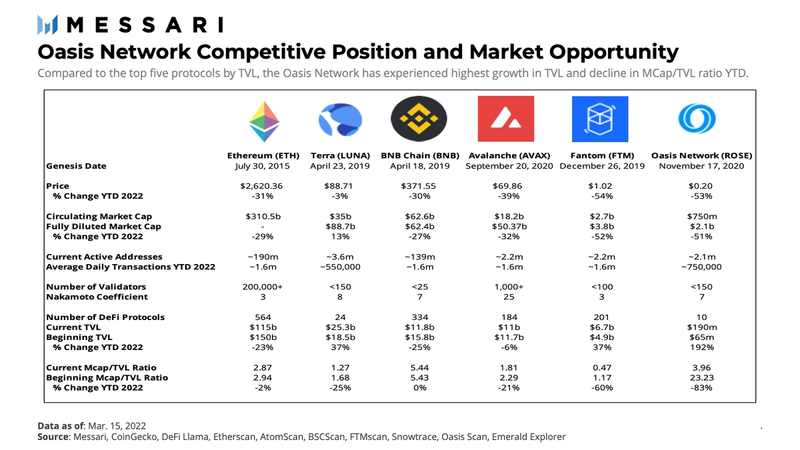

Compared to the top five protocols by TVL, Oasis metrics may not be as large but represent the market opportunity the network has when compared to other Layer-1 platforms. There are a few other key items to point out. First, Oasis launched its Consensus Layer later than most of the top L1s in existence today. It also didn’t launch its EVM ParaTime until January of this year. Lastly, none of them have confidential compute technology at the center of their ecosystems. Nonetheless, when we evaluate each network over the same period, Oasis experienced greater growth in TVL than each of the top chains. As of March 15, 2022, Ethereum experienced a 23% decline in TVL while Oasis experienced a 192% increase. Although this very well could be the result of the high growth that is usually experienced by any early-stage endeavor, the traction may suggest there is a driver for using and building on the Oasis Network technology.

The key to Oasis closing the gap on its multibillion dollar counterparts may rely on the privacy value proposition on the way. If adoption becomes apparent and the gap closes by even a small percentage, Oasis is poised to capture market position as a privacy-enabled, smart contract platform.

The Road Ahead, Potential Challenges, and Growth Strategy

Like many networks in this highly competitive space, positioning in the market may come with some challenges. The growth of the network infrastructure for additional ParaTimes needs to continue for a successful launch. As with the launch of any network, some potential risks and setbacks could occur due to a lack of infrastructure and decentralization. Given the recently generated network activity from the launch of DeFi, Oasis needs to find strategies to successfully launch additional ParaTimes, maintain growth, and pursue opportunities to close the gap with more mature networks. With that in mind, Oasis does appear to have a strategy to mitigate these challenges. In addition to the anticipated launch of Cipher and Parcel, the Oasis Foundation has engaged with a group of backers that include Binance Labs, Pantera, Dragonfly Capital, and others to pool together more than $200 million in funding for developers and projects looking to build on the Oasis Network. Moving forward, it will be imperative to evaluate the continued growth of Emerald and the launch of Cipher and Parcel in tandem with the capital efficiency of the ecosystem fund.

In addition to the ecosystem fund, the Oasis Foundation has been working with development teams through Grant and DevAccelerator programs to build applications and integrations on top of the Oasis Network. As a result of these programs, there are over a dozen recipients actively building.

Finally, the Oasis Network has implemented a strategy to build community by way of an Ambassador Program and University Program. Oasis seeks to build a global body of ambassadors to run meetups, answer developer questions, and stress test the Oasis Network. The University Program stretches across five continents, with over 25 university departments and blockchain clubs participating. University Program members run nodes and build apps that include Blockchain at Berkeley, Tsinghua University’s Student Association of Digital Finance, and Cambridge University’s Blockchain Society.

Collectively, Oasis has organized an ecosystem fund, grant, accelerator program, and community programs to mitigate network risk by expanding network infrastructure and driving network activity for the foreseeable future.

Closing Summary

The Layer-1 smart contract platform race for adoption and market share is likely far from over as Ethereum continues its architectural redesign and incorporates scaling solutions. New use cases continue to demand alternative solutions, and one of those solutions may very well address the desire for confidential computation technology on a purpose-built, modular execution layer. With its unique architecture and deployment of confidential computing technology, the Oasis Network seeks to meet such a demand. Oasis stands well-positioned to close the gap in the Layer-1 race as the network moves forward with expanding applications on Emerald and launching Cipher and Parcel.

Though technical challenges may present themselves along the way, Oasis is positioned with a growth strategy that includes an ecosystem fund, incentive programs, and community initiatives organized to mitigate such challenges and drive growth. Although many Layer-1s experienced exponential growth in 2021, Oasis was not quite in the race as major developments and launches had yet to occur. To that end, this year is a pivotal year for the Oasis Network, as the network unleashes its value proposition to the decentralized world.

This report was commissioned by Oasis, a member of Protocol Services. All content was produced independently by the author(s) and does not necessarily reflect the opinions of Messari, Inc. or the organization that requested the report. Paid membership in the Hub does not influence editorial decision or content. Author(s) may hold cryptocurrencies named in this report and each author is subject to Messari’s Code of Conduct and Insider Trading Policy. Additionally, employees are required to disclose their holdings, which is updated monthly and published here. Crypto projects can commission independent research through Messari Protocol Services. For more details or to join the program, contact hub@messari.io. This report is meant for informational purposes only. It is not meant to serve as investment advice. You should conduct your own research, and consult an independent financial, tax, or legal advisor before making any investment decisions. Past performance of any asset is not indicative of future results. Please see our terms of use for more information.