Key Insights

- Outstanding Loans and Deposits fell 42% and 32%, respectively.

- Liquidation metrics increased 290%, exceeding $134 million in Q1.

- COMP incentives have dropped 50% in the quarter and are set to diminish to zero by Q2.

- Quarterly borrow and deposit rates averaged 3.8% and 1.5%, respectively

- DAI quarterly deposits declined over 90% in the Q1

Introduction to Compound

Launched in September 2018, Compound is a leading interest rate protocol built on Ethereum that enables users to permissionlessly borrow and lend assets from a pool of collateral. It sets interest rates for those assets algorithmically using an interest rate model based on the proportion of assets lent out, which it calls the utilization ratio. Compound launched its V2 protocol in May 2019, which introduced additional assets, individual risk models, and smart contract gateways for each asset, among other features. In April 2020, Compound replaced the administrator of the protocol with community governance, empowering COMP token holders to take control of the protocol. In June 2020, Compound began distributing COMP to users via a pioneering liquidity mining program reserving 42% of the total COMP supply to be distributed to users over the next four years.

Compound KPIs across the board were largely down due to market volatility, decreasing overall loan appetite and applying supply pressure. Outstanding loans and deposits fell 42% and 32%, respectively, while liquidations skyrocketed 295% in Q1. Governance facilitated a few key changes to the protocol, including collateral factor adjustments, updating the price oracle, reducing COMP proposal thresholds, and reducing COMP rewards by 50%.

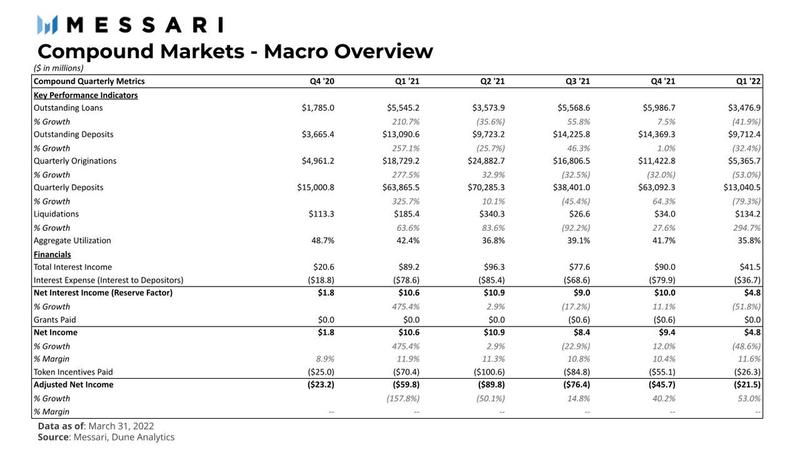

Compound Markets – Macro Overview

As Q1 2022 wrapped up, many key performance indicators for Compound experienced substantial declines. The quarter ended with a 42% decline in outstanding loans, a 32% decline in outstanding deposits, a 53% decline in originations, which was already down 32% in the prior quarter, and an astounding 79% decline in deposits. Quarterly deposits hit an all-time-low in the trailing twelve months (TTM). Q1’s only growth area was in liquidations with a monstrous 295% increase, totaling $134 million, largely driven by market volatility towards the end of January.

Unsurprisingly, the slashing of KPIs across the board had a material impact on protocol financials. Net income, which was up 12% in the prior quarter, fell by 48%, totaling $4.9 million in the quarter.

Last quarter was catalyzed by the total crypto market cap experiencing all-time-highs of $2.97 trillion. After an overheated end of 2021, the market cooled off and shaved over 40% in value, ending January with approximately $1.68 trillion in total market cap.

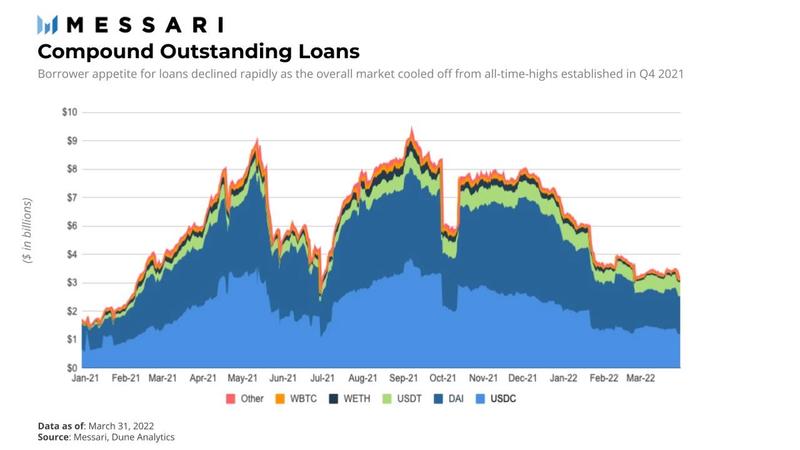

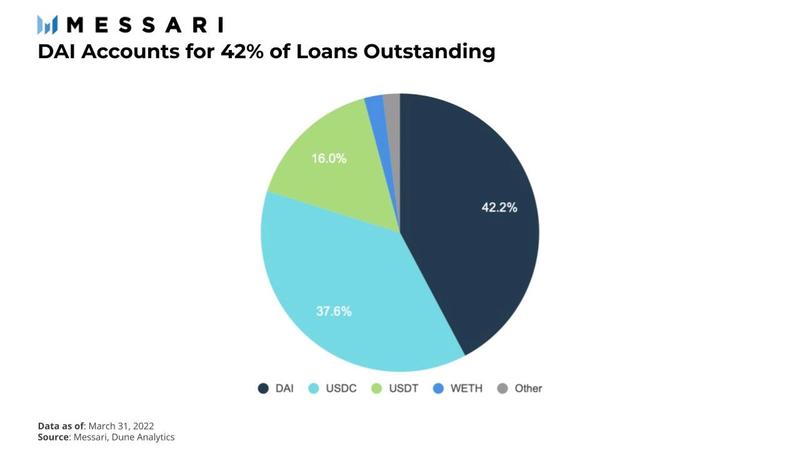

Outstanding loans were down 42% in the quarter, dropping to levels seen back in Q1 2021, when the total crypto market cap also had a cooling period. Loans in stablecoins denominated in USDC and DAI continued to outpace loans denominated in other assets. DAI maintained its market share of overall loans outstanding on Compound as Q1 2022 ended.

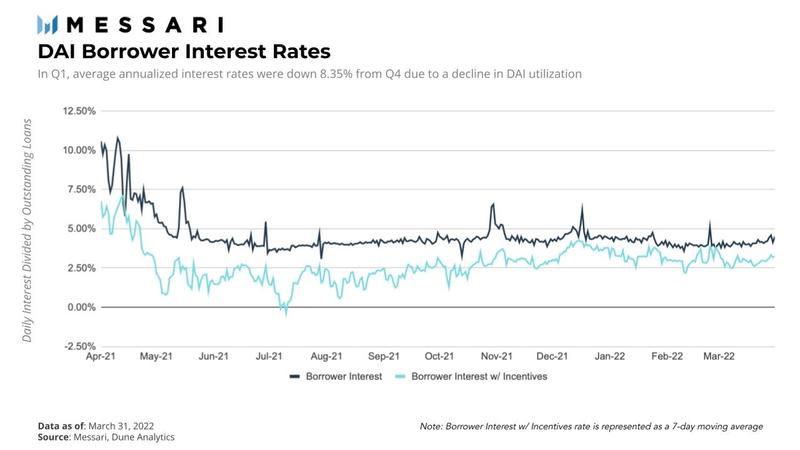

Borrower interest rates were relatively stable compared to the prior quarter. The average annualized interest rate was 3.85%, down from 5.02% in Q4. Rates decreased as users’ demand for leverage decreased as the market cooled off in Q1. Additionally, the COMP distribution bug in Q4, resulted in assets leaving the protocol, which impacted supply and drove rates higher. Borrower interest rates maxed out at 4.48% as the market hit YTD lows.

Outstanding deposits were down 32% in Q1 with the steepest decline transitioning into February. Similar to outstanding loan volumes, deposits approached TTM lows seen in Q2 2021. Deposit volumes rose in March with depositors continuing to prefer WETH.

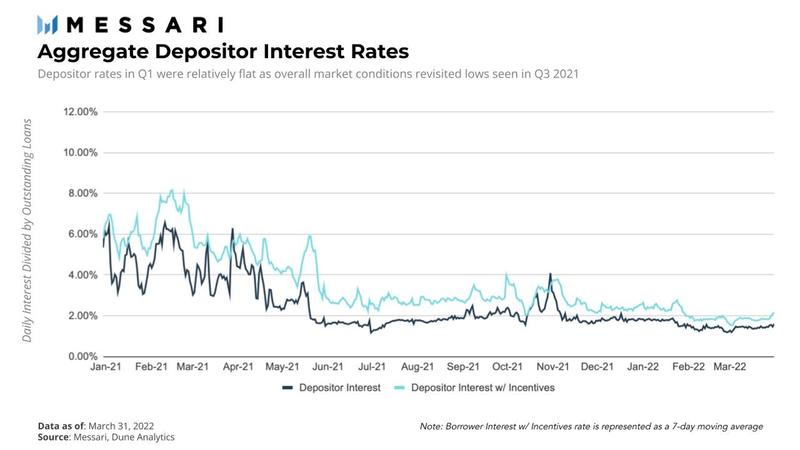

Depositor interest rates were down but stable over the quarter. This can be attributed to deposits consistently matching borrower demand. The average quarterly depositor interest rate was 1.51%, down from 2.04% in Q4. Annualized interest rates hit a low of 1.19% in Q1 and peaked at 1.87%. Interest rates saw their steepest decline at the end of January due to market volatility.

Compound’s aggregate utilization ratio remained relatively flat at the onset of 2022 but gradually weakened as the crypto market experienced turbulence rolling into February. Outstanding deposits declined at a slower rate of 32% relative to 42% for outstanding loans, which contributed to the utilization ratio revisiting its lows back in Q3 and Q4 2021.

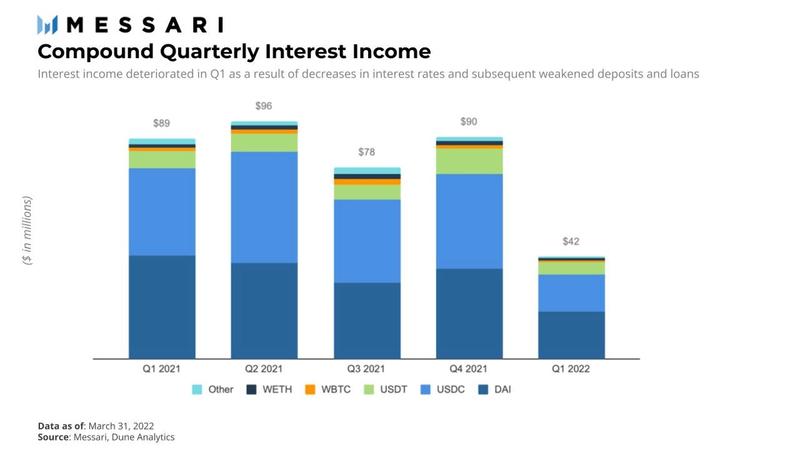

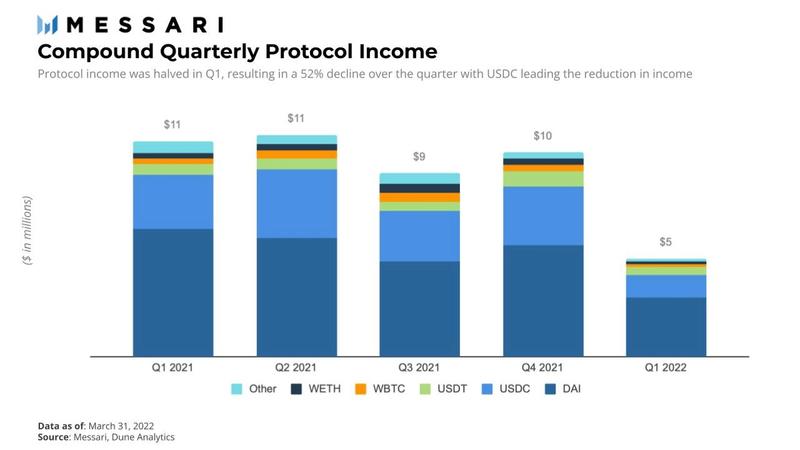

Interest income for the quarter deteriorated by 54% compared to Q4 2021. Coincidentally, interest and protocol income virtually experienced the same percentage changes in Q1. USDC dropped the furthest, falling 62%, followed by USDT and WBTC declining 50.8% and 50.7%, respectively. Quarterly interest income was impacted because market volatility decreased loan appetite.

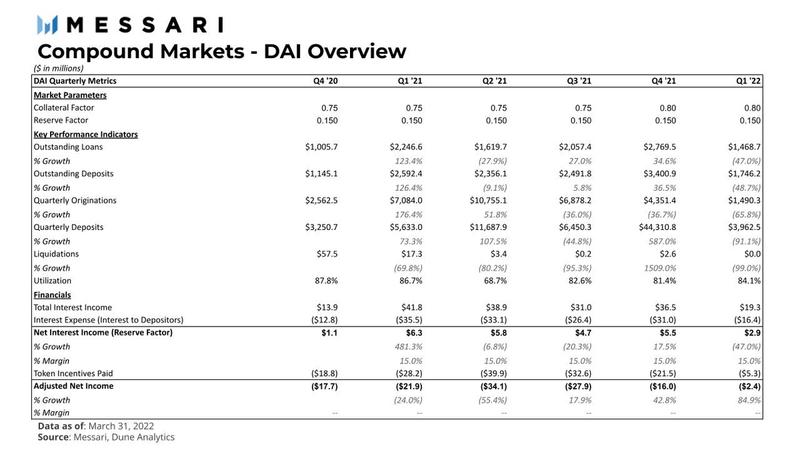

Protocol income was halved, dropping from $10 million in Q4 2021 to slightly under $5 million in Q1. DAI, which is responsible for over 60% of protocol income in Q1, was down 47% quarter-over-quarter.

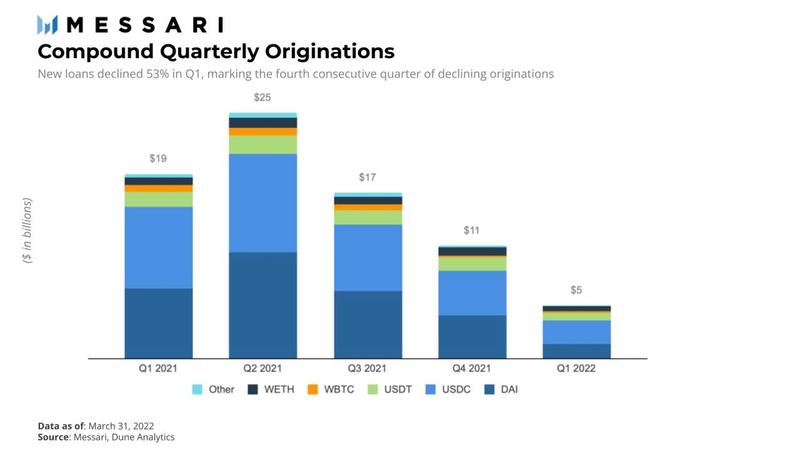

The narrative continues across originations (new loans) for Q1. Total originations were down 53% in the quarter, led by DAI with a $2.9 billion drop (66%), over the quarter. USDC and USDT held strong but still had large declines of 48% and 47%, respectively. USDC continued to show dominance in origination volume from the prior quarter. WBTC was the only asset that grew in originations over the quarter, resulting in a 17% increase or $1.7 million.

New quarterly deposit volume took a nosedive in Q1, falling from $63 billion to $13 billion, or 79%. DAI quarterly deposits plunged by over 90%, from $44 billion to $4 billion in Q1. Compared to DAI, WBTC fell a modest 18% in deposit volume in the quarter. On-chain data suggests a user was using flash loans to arbitrage between AAVE and Compound in December 2021, driving quarterly deposits up 587%. Subsequently, another market-maker pulled DAI off the protocol in Q1, contributing to the spike in deposit volume quarter-over-quarter.

DAI, WETH, and USDC are now in contention for overall quarterly deposits on Compound, with $4 million, $3.6 million, and $3.5 million in deposits, respectively. USDC was able to close the gap on WETH deposit volume in Q1, relative to the prior quarter.

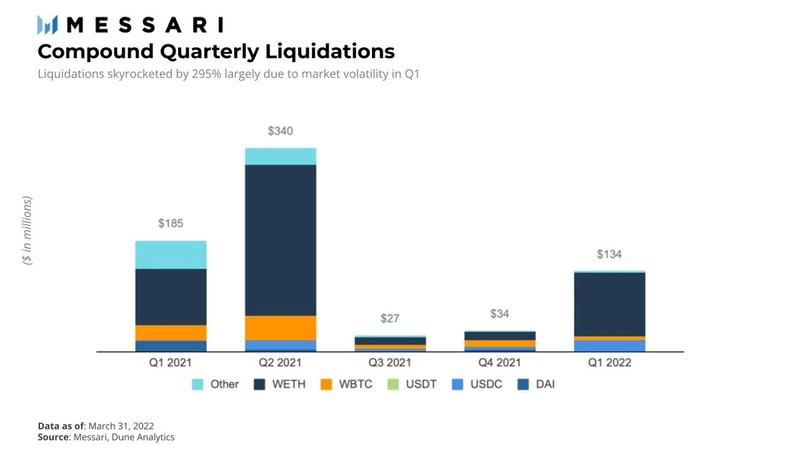

Liquidations on Compound peaked towards the end of January, growing 295% quarter-over-quarter. This activity was largely due to liquidations across the WETH and USDC markets resulting in increases of 270% and 665%, respectively. WETH liquidations grew from $14 million in Q4 to $106 million in Q1, largely due to ETH volatility experienced in late January. USDC markets experienced a $13 million increase in liquidations over the quarter while DAI liquidation volume was virtually non-existent in Q1 relative to the prior quarter of $3 million.

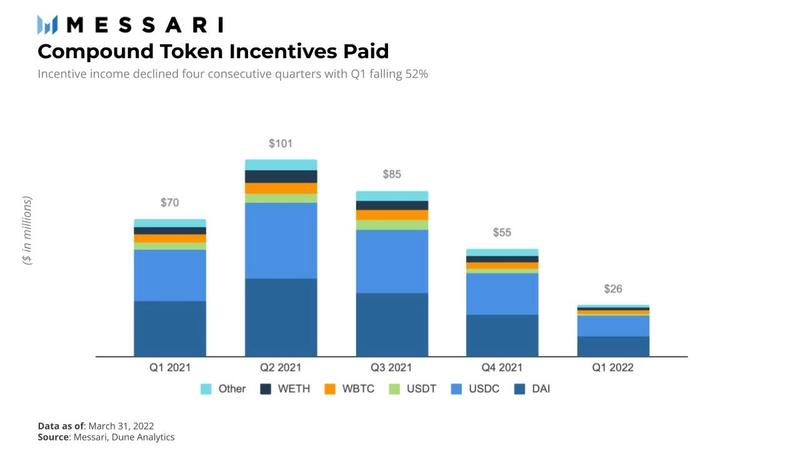

COMP token incentives fell drastically by 52% in Q1. These incentives are a key driver of depositor and borrower activity. Governance passed a proposal at the end of Q1 that would reduce COMP incentives by 50% with plans to eliminate incentive rewards. Given these plans, there should be a rapid decline in COMP token incentives in Q2.

Compound’s Five Largest Markets – Micro Overview

Compound markets experienced various modifications in the quarter through governance. Gauntlet facilitated collateral factor adjustments across eight markets, GFX Labs introduced an updated price oracle, and a new algorithmic stablecoin market, FEI, was added to the protocol. Continuing last quarter’s trend, borrowers continued to favor loans in stable assets over others.

Although key performance indicators across the board were down in Q1, DAI continued to be the prevailing market on Compound, leading in metrics like loans outstanding, deposit volume, interest income, and protocol revenue. DAI loans outstanding decreased 47%, from $3.4 billion to $1.5 billion, while DAI’s outstanding deposits decreased at a slightly higher rate of 49%, from $3.4 billion to $1.75 billion. Expectedly, quarterly originations were down 66%, from $4.4 billion to $1.5 billion. Liquidations in DAI were virtually non-existent in the quarter.

Average annualized interest rates were down from 4.5% in Q4, to 4.12% in Q1. Borrower interest rates hit a low of 3.58% and peaked at 5.10% in the quarter. The utilization ratio increased by 3.24% in Q1, resulting in borrower interest rate volatility. DAI continued to outpace loans outstanding, comprising over 42% of all loans outstanding ending the quarter.

USDC continues to be the second-largest loan market in Compound with $1.3 billion in outstanding loans, down 41%, or $2.2 billion from the prior quarter. Outstanding deposits declined at a slower rate of 37%, resulting in a utilization ratio decline of 6.2%. USDC borrower rates experienced far less volatility compared to the prior quarter with an average annualized interest rate of 3.56% in Q1. Interest rates peaked at 5.09% while bottoming at 2.62% in the quarter.

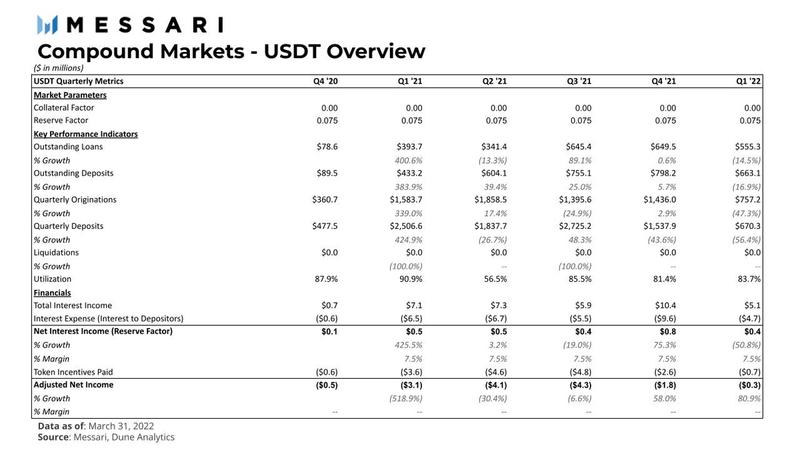

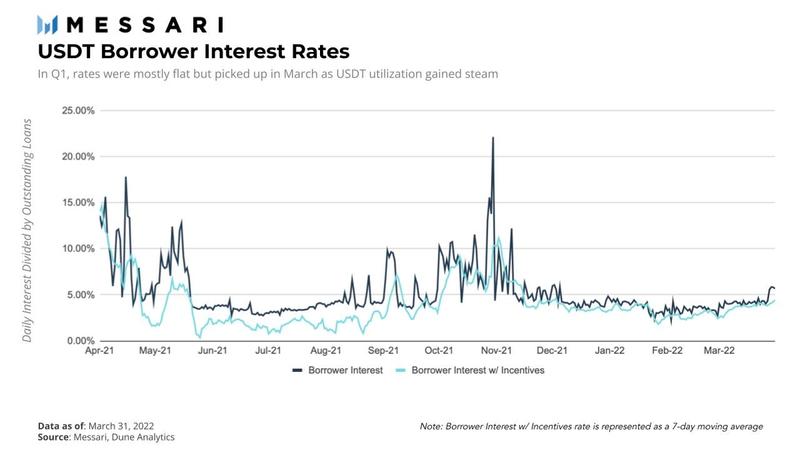

Outstanding loans and deposits in USDT fell modestly compared to DAI and USDC. Loans denominated in USDT declined 14.5%, from $649 million in Q4 to $555 million in Q1. Subsequently, deposits fell 17% from $798 million in Q4 to $663 million. Utilization rates increased 2.9% over the quarter, with USDT borrower rates averaging 3.85%. After hitting a floor of 2.25%, interest rates began to increase, reaching 5.85% towards the end of the quarter.

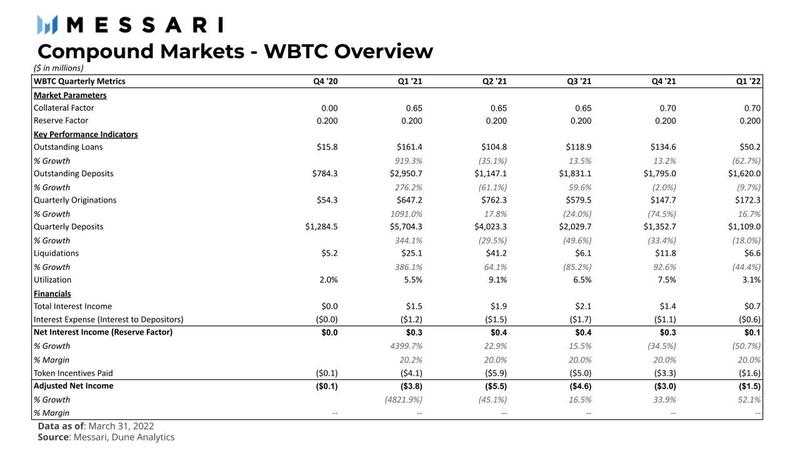

WBTC is the only asset within the top five in the protocol to experience a single-digit decline of 9.7% in outstanding deposits, falling from $1.8 billion in Q4 to $1.6 billion in Q1. In contrast, outstanding loans (USD) declined 62.7% from $134 million in Q4 to $50 million as the quarter ended.

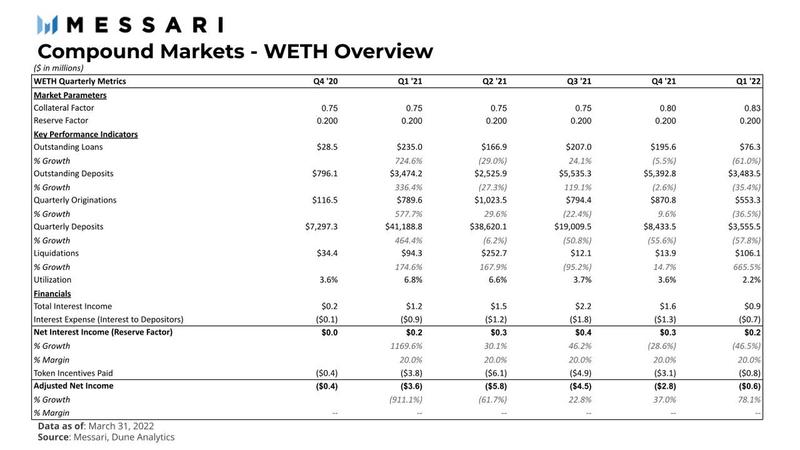

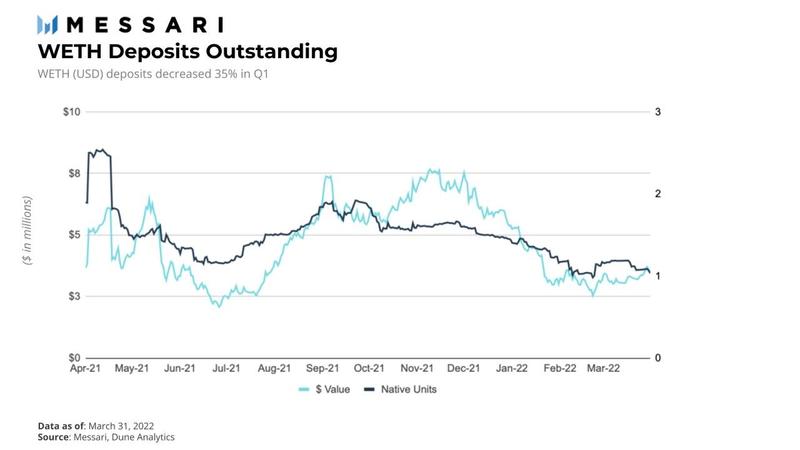

WETH continues to be Compound’s largest market by deposits outstanding. Because KPI metrics were largely down in both outstanding loans and outstanding deposits during a very turbulent Q1, WETH liquidation metrics would logically benefit. WETH markets experienced a gut-wrenching 665% increase in liquidations, up from $14 million in Q4 to $106 million in Q1. This activity was mostly captured at the end of January and cooled off as the quarter wrapped up. Outstanding loans (USD) declined substantially by 61%, while outstanding deposits (USD) declined by 35%.

WETH represents 36% of outstanding deposits and continues to outpace deposits denominated in other assets quarter-over-quarter.

Governance & Key Events:

Key Events

MakerDAO Deposit Module

GFX Labs and the Compound community proposed to MakerDAO to prioritize launching a Compound DAI Direct Deposit Module (D3M), which is a Maker Protocol implementation that enables Maker to directly inject DAI into the Compound DAI borrowing market. MakerDAO voting passed a poll in January.

Compound Comprehensive Protocol Audit

The Compound community recently voted to approve a long-term security partnership with OpenZeppelin, conducting audits over select Compound governance proposals along with advisory services and monitor solutions. Throughout the quarter, they’ve identified several vulnerabilities which were laid out to the community with recommendations for future proposal upgrades.

COMP Rewards Dissolution

A proposal was passed and executed at the end of March to reduce COMP rewards by 50% immediately and then winding down rewards to zero within a month.

Governance Decisions

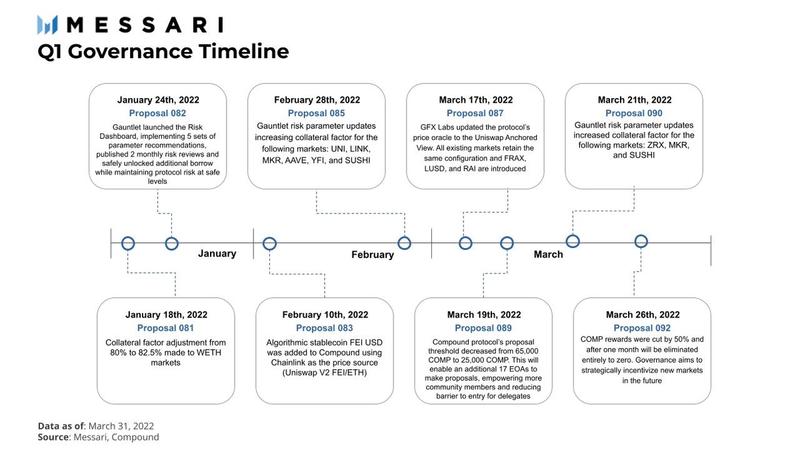

Proposal 081 – Risk Parameter Updates for ETH (Exec. 01/18/22)

Proposal 081 made parameter adjustments to the ETH market, changing the collateral factor from 80% to 82.5%.

Proposal 082 – Dynamic Risk Parameters – Quarterly Update (Exec. 01/24/22)

This proposal reviews Gauntlet’s partnership with Compound and updates its streaming grant for Q1 2022. Gauntlet proposes a quarterly fee of 8,168 COMP for the quarter.

In addition, as was requested by the Compound community, Gauntlet will replace its existing COMP stream with a Sablier stream. This governance proposal sets the Contributor Comp Speed to Gauntlet to zero and sets up a Sablier stream to Gauntlet instead.

Gauntlet has launched the Risk Dashboard, implemented five sets of parameter recommendations, published two monthly risk reviews, and safely unlocked additional borrow for Compound while maintaining protocol risk at safe levels.

Proposal 083 – Add Markets: FEI (Exec. 02/10/22)

FEI USD was added as an algorithmic stablecoin on Compound with the following risk parameters: collateral factor 0%, reserve factor 25%, borrow limit — none, COMP rewards — none, and price source — Chainlink (Uniswap V2 FEI/ETH).

Proposal 085 – Risk Parameter Updates for UNI, LINK, MKR, AAVE, YFI, and SUSHI (Exec. 02/28/22)

Proposal 085 made parameter adjustments to six Compound assets as follows: cAAVE collateral factor from 60% to 65%, cLINK collateral factor from 70% to 75%, cMKR collateral factor from 55% to 60%, cSUSHI collateral factor from 55% to 60%, and cYFI collateral factor from 60% to 65%.

Proposal 087 – Oracle Update (Exec. 03/17/22)

This proposal by GFX Labs aimed to update the protocol’s price oracle to the Uniswap Anchored View. Chainlink currently pays double the gas costs to maintain prices on the current oracle and the pending oracle. All existing markets retain the same configuration, and FRAX, LUSD, and RAI are introduced.

*The introduction of FRAX, LUSD, and RAI to the oracle was on a best-efforts basis and exists for governance’s consideration in future asset-specific governance votes. Their addition is not an endorsement or opposition to their addition to the protocol.

Proposal 089 – Lower Proposal Threshold to 25,000 COMP (Exec. 03/19/22)

This proposal aims to lower the Compound protocol’s proposal threshold from 65,000 COMP to 25,000 COMP.

The proposal additionally sets the minimum settable proposal threshold in GovernorBravoDelegate to 1,000 (this allows for lowering the proposal threshold in the future). The new change will allow anyone with a minimum of 25,000 COMP to make formal governance proposals on-chain for votes. The proposal grants 5 COMP to Ratan to reimburse gas fees for deploying the new GovernorBravoDelegate contract.

This proposal follows Proposal 88 by GFX Labs which was canceled and aimed at lowering the proposal threshold to 10,000 COMP.

Based on community feedback, there was an agreement to reduce the proposal threshold from 65,000 to 25,000 COMP. This new threshold enables an additional 17 EOAs to make proposals, empowering more community members to participate in governance and programmatically reducing the barrier to entry for delegates.

Proposal 090 – Risk Parameter Updates for ZRX, MKR, and SUSHI (Exec. 03/21/22)

Proposal 090 made parameter adjustments to three Compound assets as follows: cMKR collateral factor from 60% to 65%, cSUSHI collateral factor from 60% to 65%, and cZRX collateral factor from 60% to 65%.

Proposal 092 COMP Rewards Adjustments – Kickstart Rewards: Step One (Exec. 03/26/22)

This proposal aims to build on previous discussions in COMP Reward Adjustments by ending the current COMP rewards program and starting a new COMP rewards program with the primary purpose of kickstarting new markets. This proposal will immediately cut existing COMP rewards by 50% and after one month will cut COMP rewards to zero. The proposal will introduce a program to identify interest rate models across all markets. Once the interest rate model is optimized, the team will establish an effective rewards program to kickstart new markets.

The initial objective of the COMP rewards program was to reward protocol users with tokens. While this was an effective way to onboard and reward early adopters, the practice of COMP farming for profit is not sustainable.

Most COMP rewards have been distributed to mercenary capital, which they immediately sell off. This causes a great disservice to the existing users and tokenholders, ultimately diluting their share of the protocol. These incentives need to be used strategically to grow the protocol to the benefit of Compound, users, and tokenholders.

Proposal 092 is the first step toward launching the new rewards program. Existing rewards are being cut by 50%.

Governance Discussions

GFX Lab’s proposal includes a laundry list of protocol improvements — here are a few key:

- Deploy Compound V2 to L2s and side chains reducing gas fees and increasing accessibility

- Transition off legacy cTokens across markets, improving protocol revenue and corresponding interest rate models and bringing upside for the protocol

- Allocate resources to research, test, and upgrade existing interest rate curves, liquidation mechanisms, and developer code base

Certora’s Verification proposal aims to significantly and continuously improve the security of the Compound platform by offering a formal verification and path coverage tooling service to contributors and dApp developers within Compound.

Grant Program Overview

The community learned from the wildly successful Compound Grant Program (CGP) 1.0, which funded over $1 million in over 30 grants. The second iteration, CGP 2.0, is currently being designed with the vision to build the best community-led organization possible. The protocol plans to staff a full-time team to develop clear communication processes that enable more transparency across the community. However, the CGP has remained paused in Q1, due to a lack of focused resources to develop plans to launch CGP 2.0.

Road Map

Multi-chain Strategy

In an effort to adapt to the rapidly changing blockchain landscape and learn from the challenges experienced during the development of Gateway, the Compound community has chosen to first establish a presence on EVM-compatible chains as fragmented multi-chain markets with shared liquidity pools.

Compound Treasury

Scaling Compound Treasury will continue to be a focus in 2022. The Treasury is a centrally managed product built on top of the protocol. It is designed for non-crypto-native businesses and financial institutions, operating as an institutional on-ramp to Compound markets.

Compound III

Compound III is an EVM compatible protocol that enables supplying of crypto assets as collateral in order to borrow the base asset. The initial deployment of Compound III is on Ethereum and the base asset is USDC. The supply and borrow interest rates are bound by separate curves that have a utilization “kink” affecting the rate calculation. Accounts can only earn interest by supplying the base asset.

The evolution of Compound relies heavily on community contributions through governance. Even if many members agree on what protocol improvements should take place, efforts can be stalled due to the allocation of resources and compensation structures of contributors.

Closing Thoughts

Compound’s overall activity was largely influenced by the volatility of the broader market in the quarter. Retreating from Q4 market all-time-highs, users’ appetite for loans and deposits declined sharply in Q1. This sentiment appears to be the primary driver in the decline of both borrower and deposit interest rates as well as protocol income, consequently resulting in triple-digit percentage increases in liquidations from the prior quarter.

With COMP rewards being slashed by 50% at the end of Q1 and plans to be ultimately brought to zero in the following month (Proposal 092), Compound markets should start to stabilize, shaking out mercenary capital who are the primary beneficiaries of incentive rewards. These protocol participants immediately sell off rewards, which can negatively impact COMP price and tokenholders. As a response, Compound is aiming to optimize markets across the board and introduce effective incentives to kickstart new markets. These actions should result in a net positive for COMP tokenholders, fostering a healthier and more sustainable protocol.

The recent onboarding of OpenZeppelin’s security partnership and Gauntlet’s risk dashboards are great examples of collaboration through governance. For Compound to remain competitive with the likes of AAVE and MakerDAO, critical protocol improvements in the near term are paramount. As COMP incentives diminish in the coming month, community members will need to continue driving strategic initiatives through governance to attract new users, increase market efficiencies, and ultimately improve the protocol’s dominant position in the market.

This report was commissioned by Compound, a member of Protocol Services. All content was produced independently by the author(s) and does not necessarily reflect the opinions of Messari, Inc. or the organization that requested the report. Paid membership in Protocol Services does not influence editorial decision or content. Author(s) may hold cryptocurrencies named in this report.

Crypto projects can commission independent research through Protocol Services. For more details or to join the program, contact ps@messari.io.

This report is meant for informational purposes only. It is not meant to serve as investment advice. You should conduct your own research, and consult an independent financial, tax, or legal advisor before making any investment decisions. Past performance of any asset is not indicative of future results. Please see our terms of use for more information.