Key Insights:

- The PCV remains well-funded and opens many opportunities for allocation or utilization with new products.

- New tools like Turbo are being built to take advantage of the Fei Protocol’s ability to mint stablecoins and manage a peg with Rari Capital’s lending platform

- The FEI stablecoin showed poor adoption and performance relative to peers, but it maintained peg stability despite a volatile market.

- The total addressable market for providing liquidity solutions to DAOs is in the billions of dollars and will scale with the market as a whole.

Project Overview

Initially launched in April 2021, Fei Protocol is a decentralized ERC-20 stablecoin project. The team innovated Protocol Controlled Value, using protocol-owned equity to backstop the algorithmic incentives it had created to manage a stablecoin peg. Because PCV is not debt or seigniorage, there is no risk of a liquidation event or death spiral. The risk lies in the fidelity and volatility of the PCV’s assets, relative to the outstanding liabilities in minted stablecoins. The Fei Protocol PCV consists of decentralized assets and is currently deployed to provide liquidity and earn yield. The “collateral ratio,” which measures circulating FEI supply to PCV, is a key metric in determining the credibility of the peg. Fei V2 was announced in October 2021, removing the direct incentives mechanism in favor of 1:1 redeemability of FEI for decentralized assets ETH, DAI, and LUSD. The DAO manages the reserve pools that back these mint/redeem mechanisms, currently with a 50 bps spread. As part of V2, the DAO aligned TRIBE (the project governance token) with the stablecoin as seigniorage. TRIBE now benefits from the PCV’s earnings in the form of buybacks, while also playing backstop (seigniorage) if the PCV can’t backstop the existing stablecoin supply. In January 2022, Fei Protocol merged with Rari Capital to form Tribe DAO.

Quarterly Discussion

- The State of Fei

- Fei-Rari Merger

- FEI stablecoin performance and adoption

- PCV Management

- Tribe Token

- LaaS

- Roadmap

- Turbo

- xTribe

- Other Key Announcements

- Concluding Thoughts and Questions

The State of Fei

Fei is a protocol in transition — both in its utilization and structure, with the creation of Tribe DAO and merger between Fei Protocol and Rari Capital. FEI is a fully functioning stablecoin that is in its own category. Unlike most stablecoins, FEI is certainly not centralized. FEI is not a purely algorithmic stablecoin. Neither is FEI a collateralized stablecoin, as there is no debt or collateral involved. Instead, FEI can be thought of as a reserve-backed stablecoin.

The team innovated Protocol Controlled Value, which is different from collateral because it is owned and controlled by the DAO. The original design attempted to pair this PCV with an algorithmic design, using direct incentives to manage the peg with the PCV as a backstop. Despite being an innovative design and highly touted project, it did not function as desired. Fortunately, Fei was able to pivot and use 1:1 minting and redeemability of PCV for FEI within a band to maintain the peg, the design it currently uses.

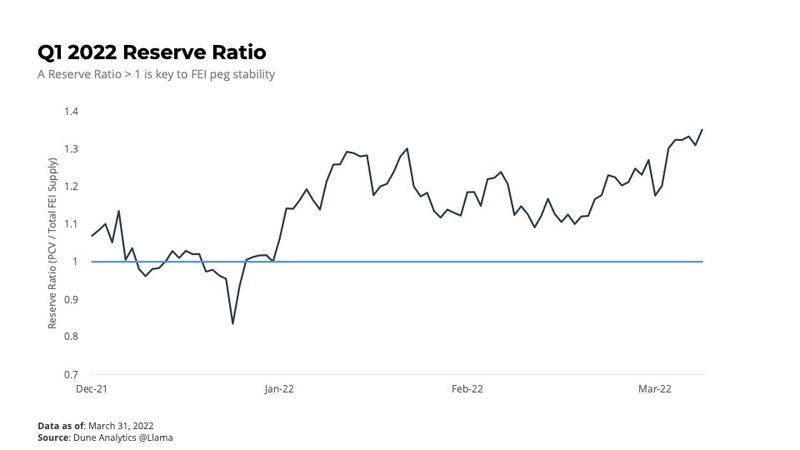

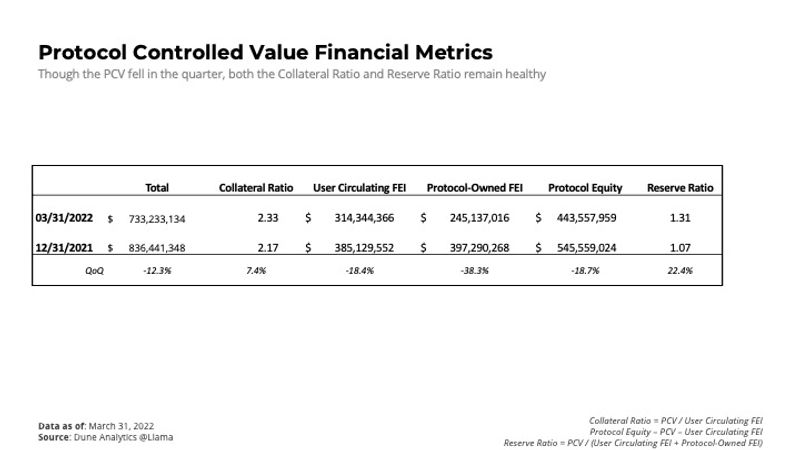

Using the reserve-backed stablecoin model we can explain the balancing forces for the stablecoin peg. The reserve ratio is the ratio of total PCV relative to total FEI supplied, which includes the circulating supply and the protocol-owned supply. Intuitively, this model holds because the equity value owned by the protocol must be greater than or equal to the value that the protocol has added to the market via FEI. Empirically, it is unclear if this model will hold given the limited data, and likely needs to include an interest rate assumption for completion. In Q1, the reserve ratio dropped below 1 in January. It did correspond with downward pressure on the peg and redemptions of FEI for PCV, though the difficult market environment makes the actual causes unclear.

The reserve-backed stablecoin framework is also useful for framing Tribe DAO’s future plans. The collateral ratio (PCV relative to circulating FEI) reports how much “dry powder” the protocol has to mint and deploy FEI stablecoins productively. This is the liquidity engine that Fei Protocol created: the DAO can both earn yield on PCV assets while minting FEI against them to create and utilize protocol-owned FEI. The marriage with Rari Capital (and the New Year resolution tweet) clarifies the intentions for protocol-owned FEI: to use the lending platform and liquidity engine to become a liquidity provider for DAOs by offering cheap stablecoin liquidity to Rari lending pools. This is an extremely powerful proposition given the state of the PCV and size/growth potential of the market.

DAO treasuries are currently measured at over $9 billion. As the crypto market matures and grows so should treasuries, giving Tribe DAO the opportunity to grow into an expanding market. With the launch of Turbo in the second quarter and other future products leaked, all pitched as solutions for DAO liquidity and treasury management, the team showing no shortage of products to utilize existing PCV to be deployed as productive protocol-owned FEI, which should increase value for the DAO.

A fundamental question going forward will be how will the DAO grow the PCV. As discussed above, Tribe DAO plans to use existing PCV to provide DAOs with liquidity. However, there is no roadmap yet for increasing demand to minting new user-owned FEI in exchange for reserve assets. The latter would require increased FEI demand and adoption. The upside, of course, is deeper, more liquid markets and greater adoption for a decentralized stablecoin. It would also mean a larger PCV. The downside is the impact on the collateral and reserve ratios. The products so far announced utilize the PCV by supplying FEI to the market with novel products that should drive returns on PCV, but they do not necessarily create incentives for FEI demand.

The teams at both Fei Labs and Rari Capital have proven to be proficient and indefatigable in their product innovation, design, and launch (i.e., the devs ship) both individually and now combined under Tribe DAO. Although the current direction of the project is becoming clear, there are still some questions and opportunities in the long term. Currently, the project is well-funded with a strong balance sheet position and new products coming to market.

The DAO Merger

On November 16, 2021, Joey Santoro (co-founder of Fei) and Jai Bhavnani (co-founder of Rari) proposed a merger of the two protocols. The final snapshot vote to tie the two was completed in January this year, forming the Tribe DAO. As of March 31, 2022, over 5.7 million RGT (Rari Governance Token), around 47% of the supply, has been exchanged for roughly 152 million TRIBE at an exchange ratio of 1:26.7. RGT holders have until August 1, 2022 at midnight GMT to exchange their tokens at the fixed rate, after which it will essentially become a meme token with no governance rights. The vote also confirmed Fei would be assuming Rari’s outstanding liabilities from a hack in 2021. Fei has paid out over $9.6 million to victims of the hack that totaled slightly over $11.6 million. Although snapshot votes passed with few voting dissent (0 RGT against, 3.9k TRIBE against), the team created a ragequit mechanism for TRIBE holders who disagreed with the decision. About 10% of these holders chose to transfer for a fixed amount of FEI (roughly 1.088/TRIBE).

The merger was motivated by the synergy team’s saw between the two protocols and fairly equal market caps. Fei has a treasure chest of liquidity via PCV, and Rari has Fuse, a platform to create customizable lending pools. FEI was already the largest asset by total value locked in Fuse pools. If their incentives were aligned under one DAO, the team would be able to take the rails of the two projects to build significantly more powerful products. The existing products, FEI stablecoin and Rari Fuse Pools and Vaults, will continue to operate independently while being governed by Tribe DAO. The focus of their new product launches is to find use cases to marry lending markets with a liquidity engine.

FEI Stablecoin Performance

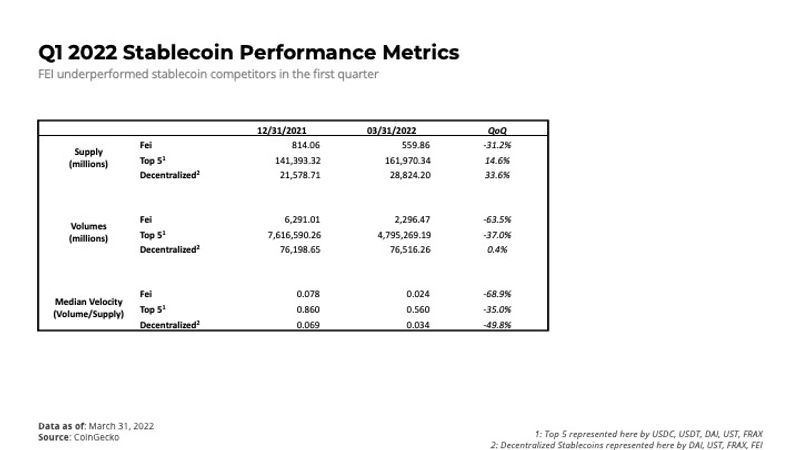

The protocol’s primary product lagged behind peers in the first quarter in terms of supply growth, volumes, and velocity (the ratio of volume to supply). The V2 implementation and governance updates thereafter helped the stablecoin maintain its peg within the desired band, piggybacking off the DAI peg with a 1:1 redeemability for DAI via the peg stability mechanism. However, in terms of volatility around the peg, FEI’s peg remains wider than the top five stablecoins.

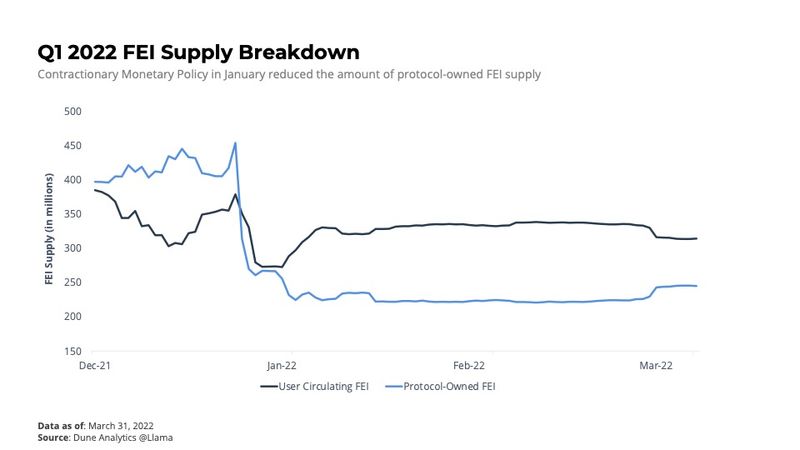

The supply numbers for FEI include both circulating FEI and protocol-owned FEI. As market volatility increased in December and January, so did DAI and FEI peg stability. This led to increased redemption of FEI for DAI, primarily from arbs. Simultaneously, PCV declined as ETH fell, putting pressure on the reserve ratio. Fei Protocol enacted contractionary monetary policies on January 23 and January 25 by reducing protocol-owned FEI from the market. For the quarter, circulating FEI supply fell 18%, and protocol-owned FEI dropped by 38%. As of March 31, 59% of FEI supply is on DEXs, led by Uniswap and Curve. Under 12% of supply is on lending platforms, with Rari and Aave the largest holders.

PCV Management

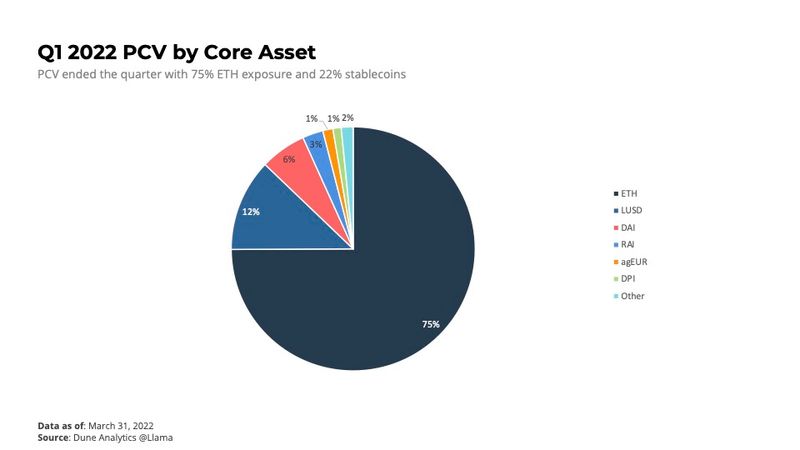

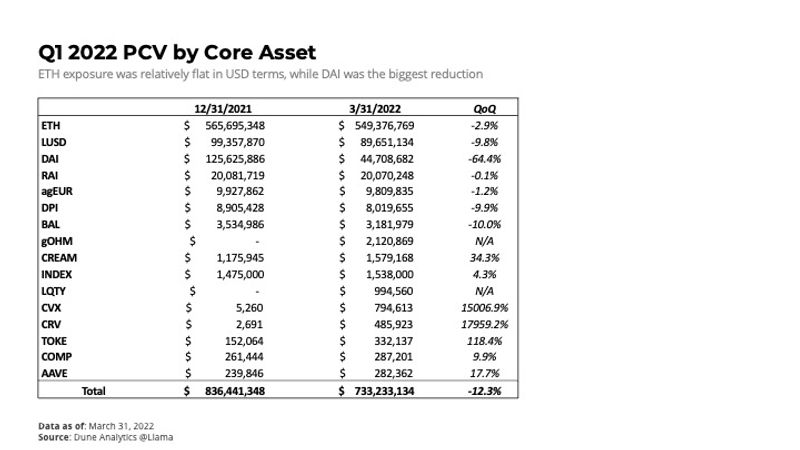

Fei’s PCV is predominantly ETH as measured by core assets (including stETH and other ETH lending deposits). It’s entering the quarter at about two-thirds concentration in the asset. Almost the entire remainder is in decentralized stablecoins LUSD, DAI, and RAI, with about a 2% balance spread across native lending and exchange tokens like BAL, COMP, AAVE, TOKE, CREAM, etc., and a 1% position in DPI. As the selloff in markets progressed through December and January, Fei saw a substantial amount of FEI redeemed in exchange for DAI, depleting balances from $125.6 million to $44.7 million by the end of the quarter. The team made monetary changes by reducing the supply of FEI to relieve pressure on the peg. Redemptions have since halted, leaving Fei Protocol with a 75% concentration in ETH as a core asset at the close of the first quarter.

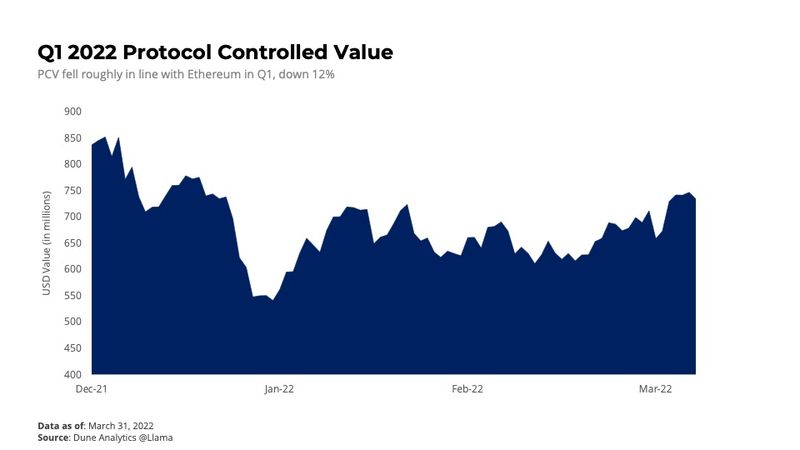

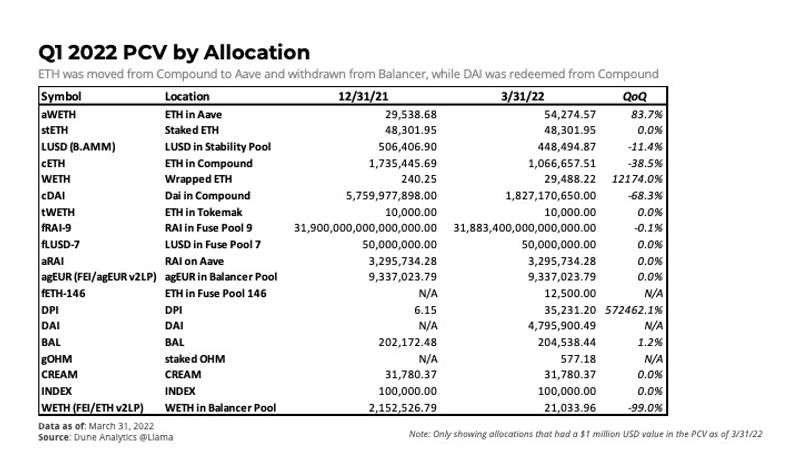

The PCV shrunk in value by 12.3% in Q1. The primary factors were the circulating FEI redemptions for DAI as well as an 11% fall in ETH price, which was largely offset with a 9% increase in ETH held. The second largest increase in PCV was the introduction of gOHM to the PCV after entering into a partnership with OlympusDAO, building a $2.1 million position. The Tribe DAO controls the allocation of the PCV and was active in the quarter. The biggest changes were repurposing ETH from Compound and a second Balancer pair to Aave. Stablecoins were also released from Compound and the Liquity Stability Pool, a yield-generating pool of assets that liquidate LUSD loans, as the protocol replenished the stablecoin balance after the January Dai drain.

Tracking the PCV’s yield generation will reveal the efficacy of the DAO to manage the assets in the PCV. Unfortunately, it is difficult to track revenues produced by allocations currently. As the steward of the PCV, the DAO is incentivized to optimally allocate both PCV assets and protocol-owned FEI. This risk/reward balance should directly impact the value of the TRIBE token.

TRIBE token

With the launch of Fei V2, TRIBE became more than just a governance token. It assumed the buyer-of-last-resort role to backstop FEI as well as benefit from buybacks from earnings on PCV. Most importantly, however, TRIBE is the governance token for Tribe DAO, managing FEI, Rari Capital, and the PCV. There is an initial maximum supply of 1 billion TRIBE, with 453 million circulating at the end of the first quarter. Because the DAO has discretion to allocate rewards to incentivize liquidity, the token’s inflation rate will be dynamic going forward. That said, the core team and investors are subject to a 4-year linear vesting and 5-year back-weighted vesting, respectively. The DAO uses the treasury TRIBE holdings as extra rewards to incentivize users to engage with different Fuse Pools as well as other liquidity investments with their PCV or protocol-owned FEI. To increase the alignment of governance and yield for TRIBE holders, the DAO is planning to release xTribe in Q2.

Liquidity-as-a-Service (LaaS)

In November 2021, Fei Protocol and Ondo Finance launched Liquidity-as-a-Service (LaaS). LaaS is a debt offering that DAO treasuries can use to increase their project’s liquidity. Historically, liquidity mining is at the cost of equity capital for a treasury, as they need to bootstrap two sides of a liquidity pool as well as incentivize others to do so with token rewards, i.e., equity from the treasury. With LaaS, the DAO only needs to fund one side of the liquidity pool, and FEI will loan them a stablecoin for the other side. The cost of the debt is a fixed percentage paid to Fei Protocol (5% in the first iteration) plus the impermanent loss of the pair, less trading fees earned. At the end of the loan, the DAO pays back Fei Protocol the full senior principal position plus interest, keeping the liquidity fees.

This offering still has its risks. For Fei, if the DAO token they are loaning against goes down more than 50%, the DAO will have to liquidate other treasury assets to pay back the loan in full. Because this is a debt offering, not equity, Fei might need to secure collateral to the junior assets it is loaning against in the event the borrower’s treasury doesn’t have enough assets to repay.

The first experiment resulted in both profit and risk, as seen by the bear market ensuing shortly after launch.

Results from the first experiment were profitable but also demonstrative of the nuanced risks, revealed by the bear market that ensued shortly after launch. First of all, there was a lot of appetite from DAOs, proving there is demand for this liquidity product. Fei also learned a lesson on how to approach liquidity and debt offerings. Some holes in the first iteration were no liquidation rules nor collateral controls, leaving Fei in the unintentional position of directional trader. In the coming launch of Turbo and other products, the DAO will benefit from this first Liquidity-as-a-Service innovation and will be able to create new guardrails and frameworks for deploying FEI. There are also more opportunities to launch new LaaS markets in a more structured form.

Roadmap

Turbo

Launched on April 20, Turbo is the first release from the newly formed Tribe DAO of Rari Capital and Fei Protocol. An interest-free stablecoin-lending facility to DAOs, Turbo takes whitelisted DAO treasury assets (native tokens) as collateral in exchange for a zero-interest loan on FEI, as long as the FEI is allocated to a yield-generating strategy. The appeal to DAOs is a liquidity boost to their lending pools.

For example, if ABC DAO was whitelisted (certain liquidity and historical volatility metrics need to be met) by Tribe DAO for Turbo, then ABC could borrow FEI for zero interest against an equal value of ABC collateral as long as it will add the FEI to a yield generating strategy like a Fuse pool. Adding a stablecoin to a Fuse Pool increases liquidity in the pool in two ways: first, by increasing total size, meaning more can be loaned at a lower utilization rate, and second, by adding an asset that can be borrowed using the treasury asset allocated as collateral. For ABC DAO, ABC tokenholders would be able to lend their assets to the pool and borrow FEI against that collateral. The DAO receives interest and fees on those assets — a productive use for previously stagnant treasury assets – and Tribe DAO also takes a cut of those fees, adding to its PCV.

For Tribe DAO, Turbo is a way to monetize its PCV. As discussed earlier, Tribe DAO should seek to manage FEI monetary policy and keep total FEI supplied below the PCV. However, while the reserve ratio mentioned above remains above 1, Tribe DAO can use its ability to mint FEI as a productive use of capital to generate fees, essentially borrowing against its PCV to mint and loan out FEI. This dynamic demonstrates how the liquidity engine of Fei Protocol (i.e., the ability to maintain a stablecoin and attract assets for PCV) paired with the lending platform of Fuse can create productive capital.

xTribe

The Tribe token continues to evolve along with the Tribe DAO. At inception, TRIBE was the governance token for the Fei Protocol managing the FEI peg and PCV allocations. After the transition to V2, TRIBE became a seigniorage token as well, benefiting from yield in PCV in the form of buybacks while taking on risk as the backstop for FEI.

As the Fei-Rari partnership grew, Fei voted to increase TRIBE rewards for lending TRIBE into Fuse pools, which only increased post-merger. As a result, over 10% of circulating TRIBE was locked in Fuse Pool 8 (184 million as of March 31, 2022) to optimize rewards, which inhibited those holders from participating in governance. On March 22, Joey introduced xTribe, an ERC-4626-compatible token, to align governance and yield-seeking incentives.

Existing TRIBE locked in Fuse Pool 8 and existing RGT locked in Fuse pool 6 and 7 will be automatically upgraded, while future TRIBE staked in yield-generating strategies can receive xTribe for their TRIBE. The new token will offer auto-compounding for holders, the ability to participate in governance with multi-delegation capabilities, and the ability to be used as collateral in Turbo with the largest revenue share out of any token. xTribe is expecting a code audit this April and then will be waiting on a DAO vote.

An interesting dynamic will be the rewards direction that is empowered by xTRIBE. Like the Curve Wars model where stakers get to vote on rewards direction, xTRIBE will give stakers a vote that can direct TRIBE rewards in Fuse pools. So if xTRIBE stakers want to direct more TRIBE rewards to any specific pool or asset, they could do so. From a DAO liquidity standpoint, this means users can further incentivize liquidity in their token in the lending pools by directing rewards towards it.

Other Q1 Proposals and Changes

January 25, 2021 — Upgrade Dai Redeemability

The team discussed methods to tighten the peg given its underperformance in terms of volatility around the peg compared to other large DeFi stablecoins. The proposal was to tighten the FEI peg to DAI in the PSM. Coincident to the early January volatility and loss of DAI from the PCV via redemptions, the team decided to also remove mint fees from the DAI PSM in order to incentivize rebuilding DAI balances in the PCV. The tighter peg and incentives have helped reduce volatility around the peg and increase DAI in the PCV.

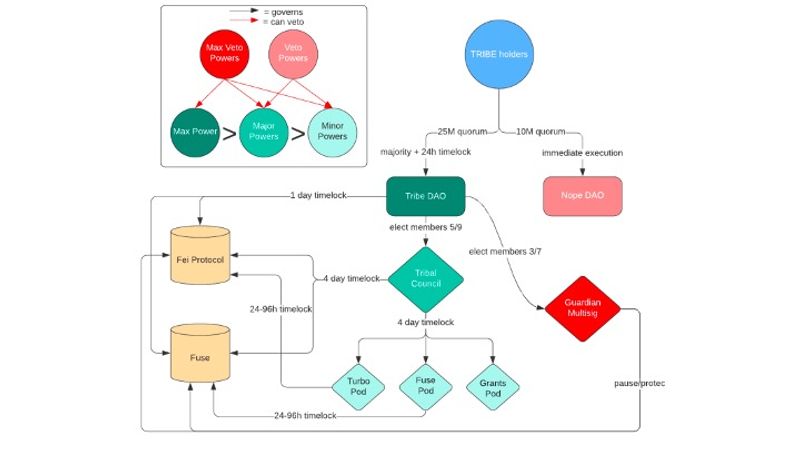

February 10, 2021 — Governance Enhancements

New governance enhancements proposed using Liquid Representative Democracy. According to Joey’s post,

“Liquid Representative Democracy means that a committee is elected by the DAO to operate the Optimistic Timelock with discretion. The DAO can at any time change the composition of the committee by adding or removing signers. This opens up more opportunities for the most committed community members to play an elevated role in governance.”

The committee will be the Tribe Council, operating a 5-of-9 multisig and made up of community, Fei core, and Rari infrastructure members. No group can individually reach a quorum. To balance the greater powers given to the Council, there will be a 4-day time lock on decisions as well as greater veto powers given to Tribe DAO (1-day time lock), Guardian (immediate execution), and Nope DAO (immediate execution). This is a novel structure using Orca Pods and optimizing for speed in the product suite with protection for the DAO as a whole. The structure will likely require greater transparency on actions and proposals for negative consent from the DAO.

March 21, 2021 — PCV Sentinel

DAO passed a vote to create the PCV Sentinel, giving the ability to create automatic guards to the DAO Guardian wallet. The Guardian wallet can pause or unpause any operations related to the PCV. A guard in the Sentinel is a smart contract capable of pausing PCV operations if a trigger is hit, empowering the team to have automatic fail safes on the PCV to protect assets.

March 24, 2021 — Volt joins the TRIBE

VOLT is a CPI-pegged stablecoin backed by a combination of user-deposited assets and PCV, incubated by Tribe DAO. With this proposal, the Tribe DAO agreed to a token swap, assuming control of 30% of VOLT and a 10 million FEI backstop for VOLT at launch.

Conclusion

Fei Protocol and the emerging Tribe DAO are in a strong position but lacking momentum. FEI usage has declined while other stablecoins are increasing adoption. The PCV is well-backed, the liquidity engine is stable, and the lending platform is running well. New product launches should offer an exciting use case and proof of concept for the combined team. The individuals involved in the project are highly capable and have proven their ability to learn, iterate, and build. Execution and product market fit for the new launches has yet to be proven, but the building blocks are well-made and in place.

This report was commissioned by Fei, a member of Protocol Services. All content was produced independently by the author(s) and does not necessarily reflect the opinions of Messari, Inc. or the organization that requested the report. Paid membership in Protocol Services does not influence editorial decisions or content. Author(s) may hold cryptocurrencies named in this report.

Crypto projects can commission independent research through Protocol Services. For more details or to join the program, contact ps@messari.io.

This report is meant for informational purposes only. It is not meant to serve as investment advice. You should conduct your own research, and consult an independent financial, tax, or legal advisor before making any investment decisions. The past performance of any asset is not indicative of future results. Please see our terms of use for more information.