Interact with the real-time data that created this report on the Dune Analytics dashboard.

State of Balancer Q1 2022

Key Insights

- Balancer continues to have a healthy rate of new pool creation on its V2 product.

- First quarter swaps and volumes were down with the market in Balancer’s Weighted Pools and Liquidity Bootstrapping Pools, while Stable Pools saw a relative increase in usage.

- Balancer began collecting protocol fees on Ethereum in the first quarter, generating over $3 million for the treasury.

- Balancer announced a major governance overhaul in Q1, voting in the shift to veBAL tokenomics.

Project Overview

Balancer is a DeFi automated market making protocol using novel self-balancing weighted pools. The protocol allows anyone to create a pool of assets with predefined weights in the pool. Balancer strives to be a platform for DAOs and other protocols to build tools that provide useful liquidity to their end users and products. The protocol is managed by the Balancer DAO community and currently supports Ethereum, Polygon, and Arbitrum. Since launching V2 in August of 2021, Balancer’s product line has expanded to include:

- Weighted Pools: Fixed weight pools that allow liquidity providers to create a rebalancing index fund, decrease risk of impermanent loss, and take a directional view while providing liquidity.

- Stable Pools: Use different weighting math (stable math with an amplification factor, which balances constant sum and constant product math) to achieve deeper liquidity for price-similar assets (stablecoins, wBTC/renBTC/sBTC, etc). Stable Pools have tighter spreads and deeper liquidity for larger trades, benefiting from the vault introduced in V2.

- MetaStable Pools: A solution between Weighted and Stable Pools, MetaStable Pools are for correlated not pegged assets like yield bearing tokens against their native token DAI and cDAI or ETH and stETH.

- Liquidity Bootstrapping Pools (LBPs): Use weighted math with time-dependent weights, which allows for smoother token distribution releases. The pool can start with less capital (80% token / 20% stablecoin instead of needing to fund 50% stablecoin). The goal is to alleviate buy/sell pressure over fixed periods.

- Managed Pools: A feature-rich option that allows for up to 50 tokens. Some of the features include: Pool Manager(s), Management Fees (optional), Liquidity Provider Allowlists, Up to 50 Tokens, Active Token Management, Add, Remove, Change token weights, Circuit Breakers to protect from malicious/compromised tokens.

- Boosted Pools: Allows for tight stablecoin trading while using idle assets to loan on a lending platform. These pools offer increased capital efficiency for the liquidity provider and similar liquidity for the trader.

- Custom Pools: Use Balancer’s vault and pools infrastructure to create your own pricing equations.

Macro Overview

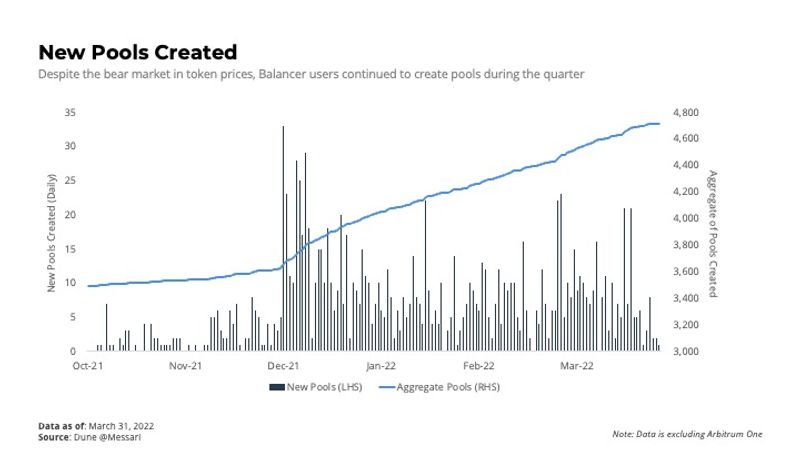

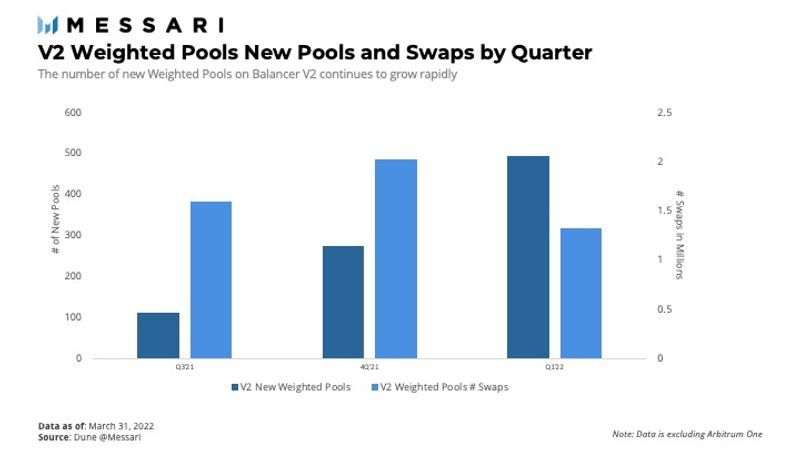

Because Balancer DAO’s goal is to optimize and manage a building block for other protocols, the number of new pools can gauge the adoption of the tools created by Balancer. In the first quarter, the growth in new pools accelerated again, increasing by 16.9% QoQ, growing faster than most leading DEXs. This growth clearly points to the increased adoption of the product.

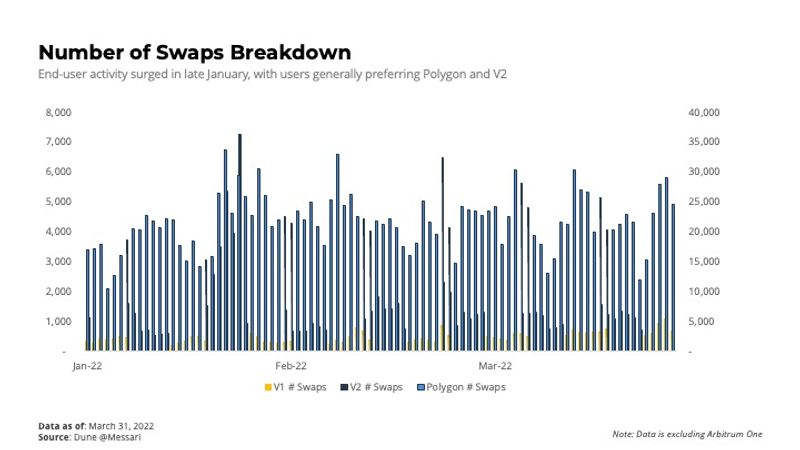

Given the market’s downturn, volumes fell dramatically from the Q4 2021. A less price-sensitive measure of usage is the number of swaps executed. Although end users executed 15.2% fewer swaps in the first quarter of 2022 than they did last quarter, it’s much less than the 31.1% reduction seen in the market-leading AMM Uniswap.

Balancer Liquidity Providers (LPs) did experience an outsized drop in revenues of 68.3%, falling from $43.7 million in Q4 to $13.9 million in Q1. The drops in market prices and number of swaps were certainly the largest contributors. A change in mix from volumes in Weighted Pools and Liquidity Bootstrapping Pools (LBPs) to stables had a large impact on revenue too, given the former two are typically much higher fee products.

On January 4, Balancer began taking a 10% protocol fee from LPs for the DAO treasury. So for each $1 of fees paid by traders, Balancer receives $0.10 and the LP receives $0.90. Without this change, fees still would have been down by 61% quarter-over-quarter.

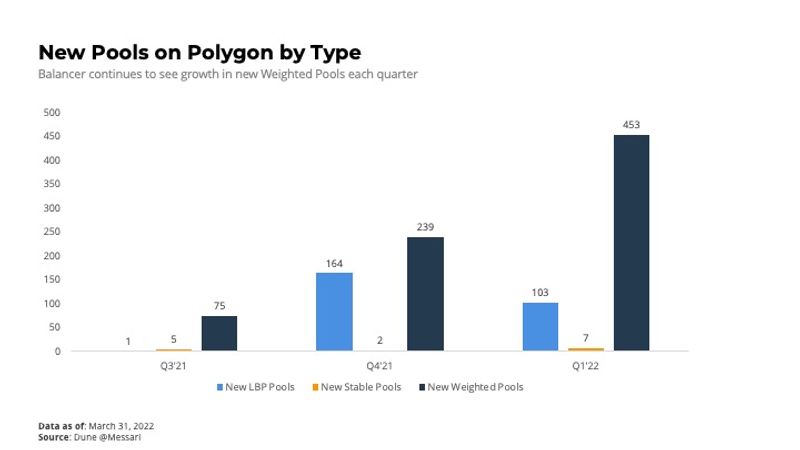

The protocol continued to grow on Polygon, unencumbered by the bear market conditions. A total of 563 new pools were launched on Polygon in the quarter, bringing the total number of pools that have launched on Balancer on the L2 network to 1,059. Weighted markets were the primary growth engine, adding 453 new markets to the existing 314. Liquidity and volumes saw higher growth in stable pools, likely because the volatility in stablecoin pegs allowed for more arbitrage opportunities as well as more users opting for safety.

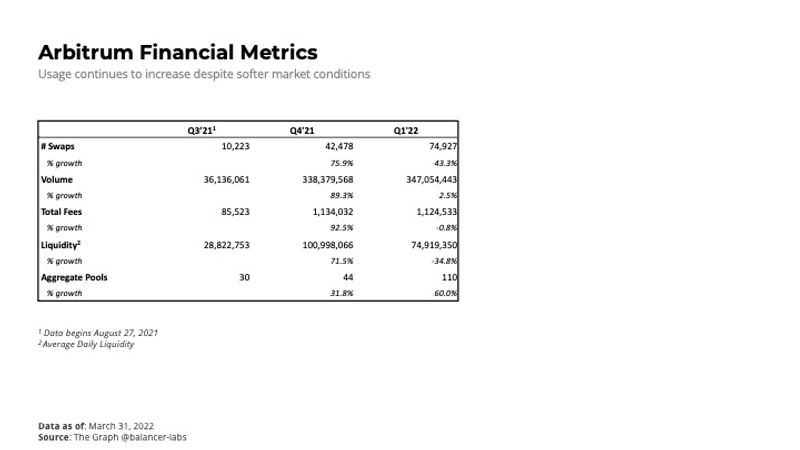

Similar to usage on Polygon, usage on Arbitrum continued to improve in terms of swaps, volumes, and new pools. Liquidity was net reduced from Balancer pools on Arbitrum in the first quarter. Pool count accelerated its growth from the fourth quarter of last year.

Micro Overview

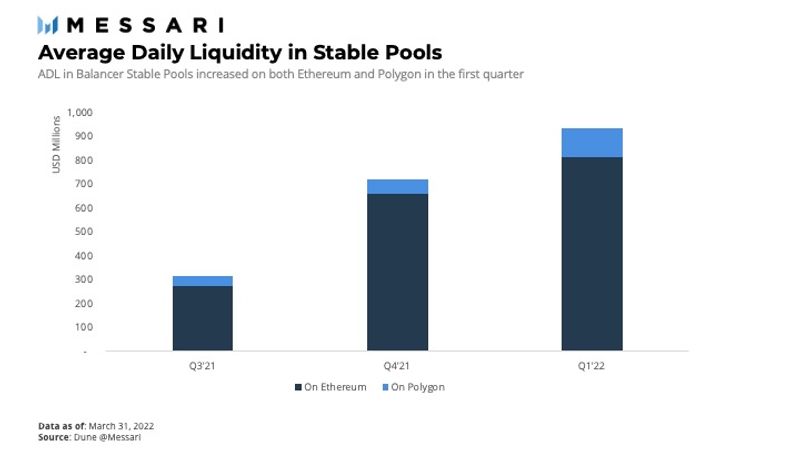

Almost all new activity on Balancer is now on V2, which was first launched in the second quarter of 2021. Isolating V2 on Polygon and Ethereum, adoption continued to grow at a rapid pace, with new markets growing by 89% in the quarter. Moreover, liquidity only dropped by 6% on V2 in the quarter despite the large drop in the markets. The divergence can largely be attributed to the increase of liquidity in Stable Pools on Balancer V2. Stable Pool liquidity doubled on Polygon, and it grew by 23% on Ethereum.

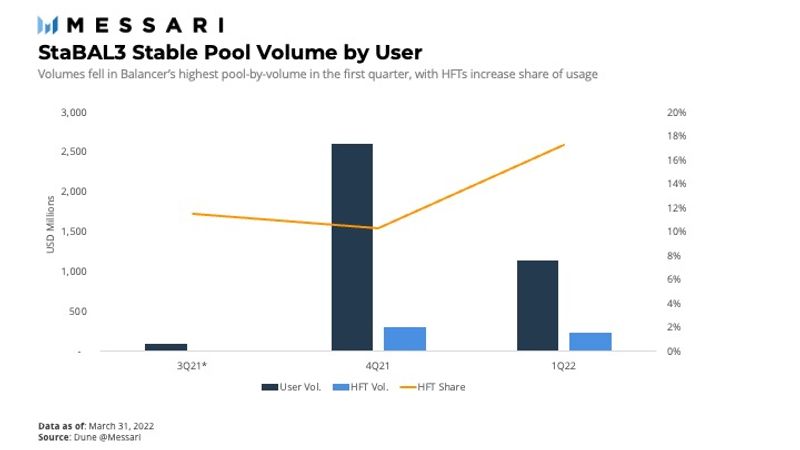

Balancer’s two highest volume pools in the quarter were both stable pools. The staBAL3 Stable Pool with DAI/USDC/USDT had the highest volume, with $1.4 billion in the quarter. Volume was dominated by whales (measured as users who have transacted over $1 million on Balancer).

High-frequency traders (a user who has made 50 or more trades in any one pool in a day) remained around flat in the quarter in absolute number versus the previous quarter. However, their share of total volume increased from ~10% to ~17%.

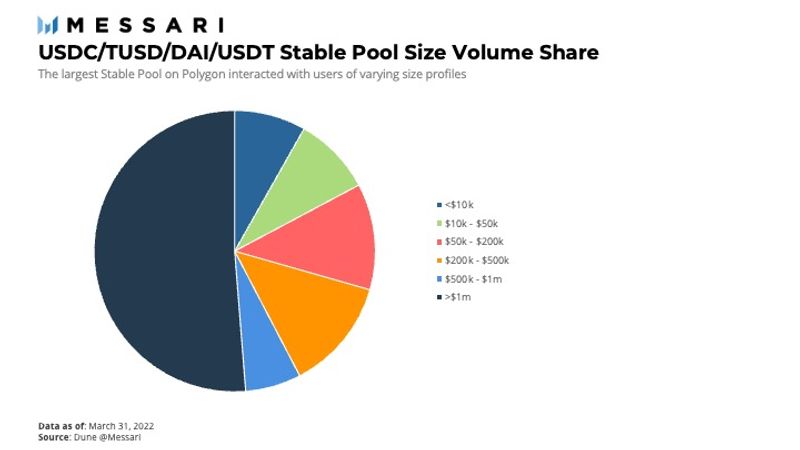

The USDC/TUSD/DAI/USDT Stable Pool on Polygon was the second highest volume pool with over $1.1 billion in volume in the quarter. The growth in Polygon’s largest stable pool was dramatic and widespread, with usage by over 350,000 unique users in the quarter and over $1 billion in volume. Less than a third of the volume was from high-frequency traders (measured as accounts that made more than 50 swaps in any pool in a day).

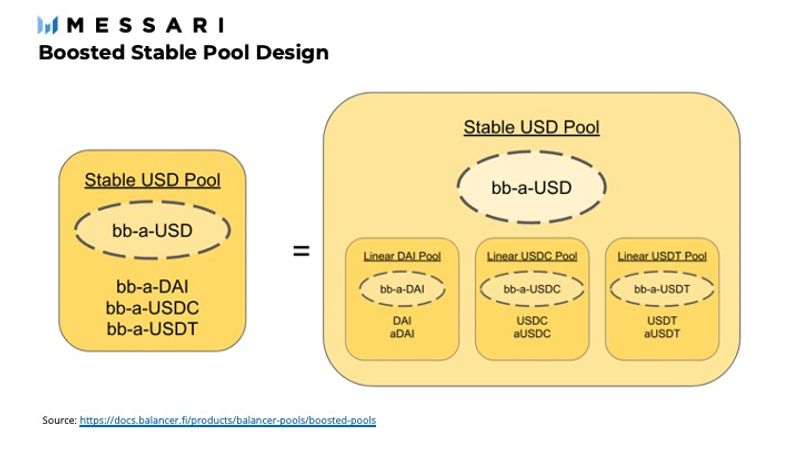

Most Stable Pools face the problems of capital efficiency for stablecoin liquidity providers. The largest stablecoin pool on Balancer averaged 21.4% utilization rate (average daily volume/average daily liquidity) in Q4’20, leaving a large majority of the capital unproductive. One solution to the problem is taking the liquidity from the pool and lending it on Aave, Compound, or other liquid lending platforms until it is needed. But this process quickly becomes inefficient because of the gas fees.

On December 13, Balancer launched Boosted Pools to solve this problem. The protocol created Linear Pools, which are pools of assets paired with the interest-earning version of the same asset (for example, DAI-aDAI) that use a linear pricing curve to incentivize arbitrageurs to keep prices in line. Balancer then builds a pool of different stablecoin Linear Pools. These nested pools make up the Boosted Pool. As a result, Balancer can now offer a more gas-efficient, more capital-efficient stablecoin pool without impacting daily liquidity. Instead of wrapping and unwrapping tokens on demand, the onus is on arbitrageurs to keep the Linear Pools balanced. Meanwhile, liquidity providers in the stablecoin pools can earn extra yield on their capital. It also creates a more liquid market for yield-bearing token holders to exchange those assets.

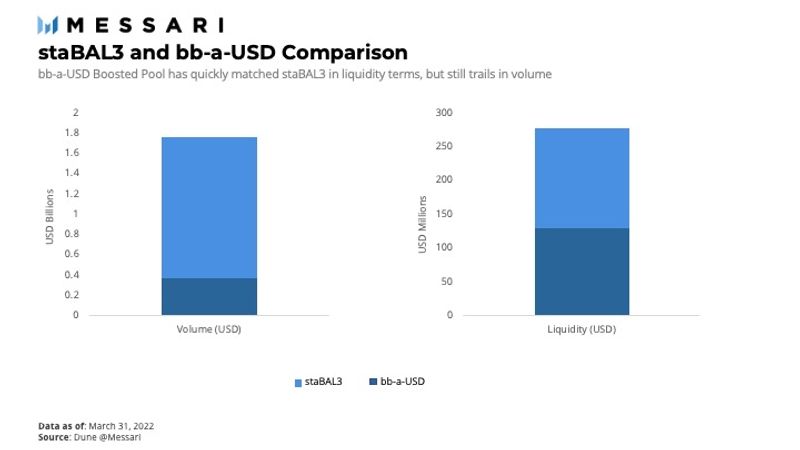

In its first full quarter, the Aave Boosted Stable Pool of USDC/USDT/DAI grew to be 16% of Balancer’s stable pool liquidity on Ethereum and 5.7% of its total liquidity. Though the Boosted Pool only did about a quarter of the volume of the regular DAI/USDC/USDT stable pool, the boosted pool almost surpassed it in liquidity (and did shortly after the quarter ended). Beneath the surface, trades on USDC and USDT were only by accounts totaling $10,000–$50,000 in volume while DAI was entirely traded by users doing over $1 million in volume. The usage of DAI by larger traders is likely representative of arbitrageurs, given the liquidations and volatility of DAI in the first quarter.

Focusing on V2, weighted pools continue to be the most utilized in terms of number of markets and number of swaps. V2 weighted pools more than doubled in the quarter. They also make up the vast majority of protocol revenues, collecting almost $2.4 million in the quarter, since Balancer turned on the 10% revenue-share on Ethereum on January 4. By volume, DAI/WETH 40/60 was the most active weighted pool on Balancer, churning over $840 million in volume in the quarter. It was followed by AAVE/WETH 80/20 (a V1 pool) and WBTC/WETH 50/50, with over $600 million each.

The largest Balancer pool by transactions on the Ethereum network is the DAI/WETH 40/60 pool. Volume, transactions, and users all increased in the quarter for this pool. It ranked third in total volume among all Balancer pools and was first among weighted pools by volume. This pool is also the second largest recipient of liquidity mining (LM) incentives from Balancer’s LM program.

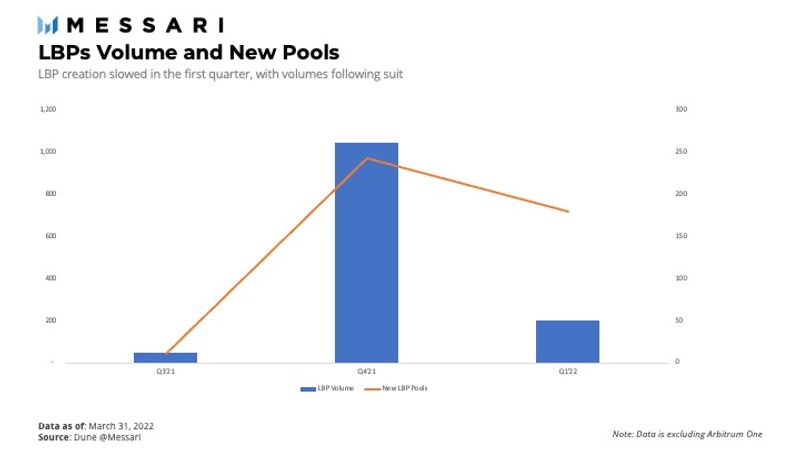

It was a much quieter quarter for Liquidity Bootstrapping Pools, likely due to the macro conditions and a less favorable environment to get liquidity. Volumes for LBPs were down 80%, and only 179 new LBPs were launched versus 243 last quarter. The three largest LBPs by volume were all launched using Copper, a platform to create an LBP using Balancer. The PDT launch saw $38 million in volume in 4 days, the SYNR launch did $30 million in 4 days, and the RSS3 launch did $25 million in volume.

Treasury

The total treasury holdings for Balancer fell from $79.5 million in Q4 2021 to $67.2 million in Q1 2022, with a fairly flat 98% of it in the DAO Multisig wallet. In Q1, the token balance of BAL tokens in the DAO Multisig dropped 5%, while the USD value of BAL in the treasury fell ~16%. The DAO Multisig made a few new allocations as well including allocations to the Aave Boosted USD Pool and into the WBTC/WETH 50/50 pool. Excluding the yield-generating investments, the Multisig is 99% BAL tokens. Balancer has three other treasury wallets on Polygon, Arbitrum, and Fantom. The first two have roughly $400,000 and $250,000 respectively invested in Balancer pools. The Fantom treasury wallet has a 10 million BEETS allocation, which was allocated to the treasury as part of a friendly fork by Beethoven X to bring Balancer pools to Fantom.

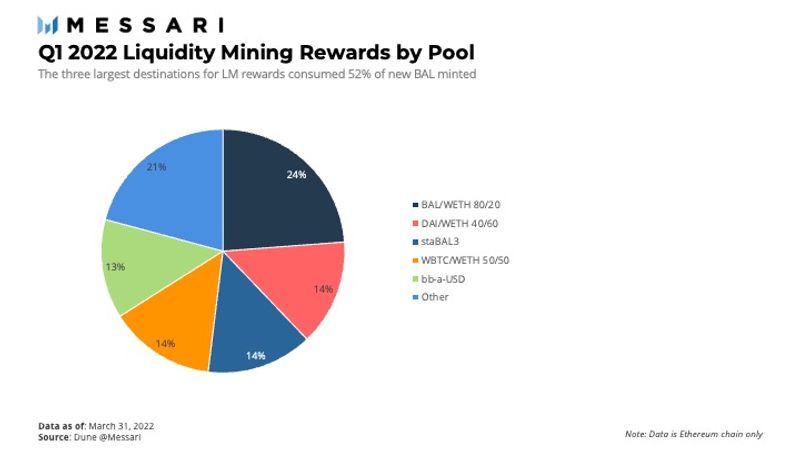

The liquidity mining program was active in the first quarter, though it has since changed in favor of a new incentive mechanism. In the first quarter, Balancer used 1.37 million BAL as liquidity mining incentives. The BAL/WETH 80/20 pool remained the largest beneficiary of incentives, receiving 325,000 BAL tokens. The DAI/WETH 40/60 pair, staBAL3 (USDC/DAI/UST), and WBTC/WETH 50/50 pairs all received 192,000. The last notable earner was the boosted stable pool which received 180,000 BAL. In total, 34 pools received liquidity mining rewards.

On March 21, the DAO empowered the Treasury subDAO to invest protocol fees. At quarter end, about 13% of the mainnet DAO Multisig was invested in Rari pools, Balancer V2 pools, Lido, and others with the remaining 87% balance in BAL tokens. The subDAO can sweep tokens worth more than $10,000 into the DAO Treasury. At the end of March, the first sweeps brought $1.3 million to be invested mostly in the WBTC/WETH 50/50 pool and the boosted USD pool, as well as $1.2 million to be invested in the WBTC/WETH pool.

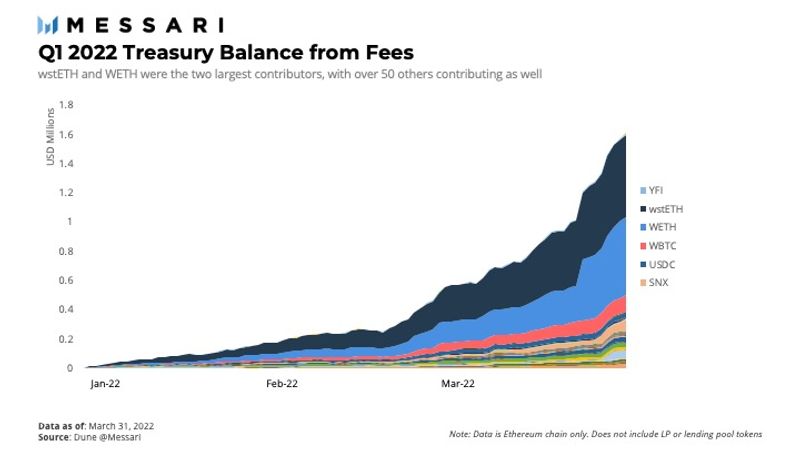

Balancer’s method of revenue collection creates a well-diversified income stream for the protocol, also allowing it to move away from reliance on BAL. In the first quarter, Balancer earned fees denominated in at least 57 different tokens, not even including LP tokens or pool tokens. The two largest token’s by USD income in the quarter were wstETH and ETH, both over $500,000. wBTC was the next largest at more than $100,000. Note that 28.36 wstETH was returned to LPs from a bug in the protocol fee collector.

Major Q1 Announcements

veBAL

Certainly the biggest news of the quarter was the tokenomics change to veBAL. Before we discuss how veBAL changes incentives for the protocol, let’s review how these tokenomics work.

Introduced by Fernando Martinelli on February 3, veBAL went live on Balancer on March 28th. veBAL brings vote escrow tokenomics to Balancer. veTokenomics offers tokenholders an incentive to lock-up their tokens for a fixed period of time. Based on how long a holder chooses to lock up their tokens, they receive tiered rewards like more weight in governance voting, boosted liquidity mining rewards, and voting power for reward boosts to certain pools. Under the new system, BAL will no longer be a governance token, and all votes will be done based on veBAL holdings.

The veBAL system takes vote escrow tokenomics and applies it to Balancer’s mission. Unlike Curve where veCRV is received for locking CRV, veBAL is not obtained by locking BAL. BAL holders must provide liquidity to the BAL/WETH 80/20 pool to receive Balancer Pool Tokens (BPTs) for this pool. Those BPTs are what is locked for veBAL. The longest lock period is one year, and the longer the lockup, the greater the boost (using the same boosting equation as the Curve system). These long lock-up periods ensure that voting power goes to users with long-term visions for the protocol.

This is a complete reset of Balancer governance and tokenomics. By switching to veBAL as the governance token, BAL becomes a utility token whose value is derived from a supply-demand market. The supply side of the equation is now known and fixed given the new inflation supply schedule. The demand side will be determined by market forces weighing demand for future protocol revenues plus a governance premium. The demand side is slightly more complicated than that because in order to get veBAL users must provide a liquidity pair, so there is an aspect where demand will have to weigh the relative value of BAL and ETH.

Most importantly, the new tokenomics attempts to better align incentives of veBAL holders and the protocol. In order to increase protocol revenues, one needs to drive more volume to the protocol (beta-adjusted). The incentive can enable veBAL holders to bootstrap new products and pools with short-term liquidity incentives. It can also direct incentives to pools where liquidity would otherwise not flow because of competing incentives or products.

However, the new system still has some friction points. The largest likely being that it is unclear if the veBAL incentivizes holders to create new use cases on Balancer or simply to direct rewards to existing pools. A later snapshot vote does help with this directly, and perhaps paired together can create better incentives.

The new tokenomics can also crowd out new projects that now have higher entry costs to fund a new pool. For example, on top of the liquidity needed to fund a pool on Balancer, the builder might need to buy BAL/WETH to get veBAL to direct rewards and compete. That said, it may still be cheaper to get subsidized liquidity incentives from Balancer at the cost of funding the BAL/WETH pool versus funding your own liquidity incentives.

Under the current system, veBAL holders vote to allowlist new pools to get votes for boosted rewards. There is the risk of incumbency overtaking long-term benefit and voters not wanting new pools added to the list and therefore diluting their own incentives. But if veBAL holders can bootstrap new pools, they can increase revenues for the protocol as a whole and get a share of said revenues.

The team wisely alerted the community of two other risks in the governance proposal: immutability of the system impairs the ability to adapt in the future, and platforms built on top of Balancer can take control of the majority of votes and create central points of failure. Lastly, many holders were frustrated that veBAL can only be earned on Ethereum L1 mainnet, since many prefer to use Polygon and Arbitrum to avoid gas fees. L2 pools can still receive rewards, but only BPTs from Ethereum will be eligible to be locked for veBAL.

subDAOs

On January 17, Balancer DAO voted to form subDAOs to improve governance as the protocol grows and evolves. Balancer DAO had already been operating with a Multisig and Grants DAO, but the new structure created Marketing, Ops, Partnerships, and Treasury subDAOs. Since the proposal passed and was implemented, the Treasury subDAO has been given approval to invest protocol fees (discussed above), and the Partnerships subDAO has provenance over liquidity mining rewards. The new structure should create focused teams executing defined purposes, all aligned under Balancer DAO. The teams have created a Notion page for the community to better track their efforts.

Other Q1 Proposals and Updates

March 24 – Grants DAO: Wave 3 Final Report

The Grants DAO continues to actively fund projects to improve Balancer DAO and benefit the community, approving 12 projects for over $300,000 in the first quarter.

February 16 – Increase the Protocol Fee

This proposal aims to increase the protocol fee activated at 10% to its maximum of 50%. The protocol fee is a percentage of trading fees earned by LPs. This proposition follows the introduction of a veBAL Tokenomics that incentivizes BAL emissions for locked LPs rather than revenue from trading fees. Hence, the goal is to drive the protocol’s growth through BAL emissions and increase protocol revenue for BalancerDAO Treasury and the APR for aligned LPs in incentivized BAL pools.

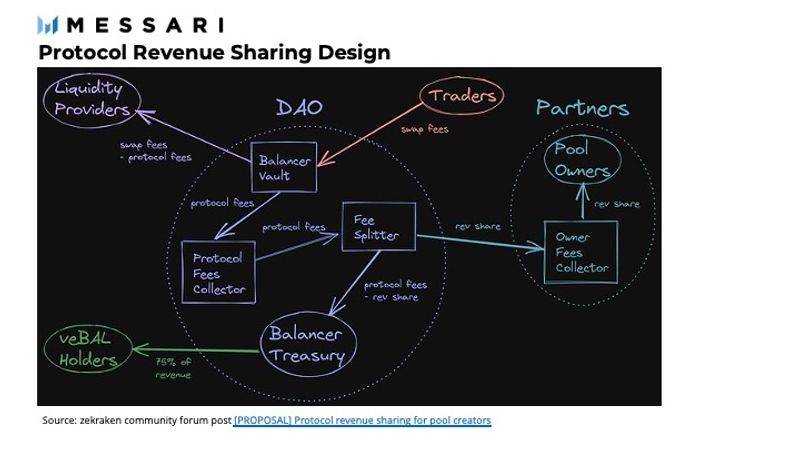

Feb 18 – Protocol Revenue Sharing for Pool Creators

This proposal aims to standardize protocol revenue sharing across all liquidity pool creators by implementing a FeeSplitter contract that interacts with the ProtocolFeesCollector so that a standard is enforced. This solution seeks to provide a frictionless revenue-sharing experience for developers building on top of Balancer as well as to minimize overhead for Balancer DAO by implementing an automated solution.

The initial proposed revenue share is ~10% with Balancer DAO maintaining authorization to boost the rate to a higher value for specific pools (i.e., 50%). The goal is to incentivize optimizing pools on Balancer.

February 27 – Governance Process Revamp 2.0

This proposal follows the Governance Process Revamp proposal. It aims to decentralize the BalancerDAO governance further and define valid proposals within the scope of veBAL holders and the duties of the Governing Council. These changes to the governance process can be summarized as follows:

- Remove the power of the Governing Council to determine whether a proposal has reached soft consensus to proceed to formal vote; instead, the Council assesses the progress of proposals based on whether the proposal is well-defined.

- Specifies the constitutions of a “well-defined” proposal to include a motivation, specifications with on-chain execution details when required, and applicable risks.

- Empowers the DAO to replace the Governing Council if they fail to execute their duties in good faith.

- It introduces a minimum quorum of 100,000 BAL and 51% majority for proposals.

March 28 – Handover Swap Fee Control to Balancer DAO

This proposal aims to terminate BalancerDAO’s contract with Gauntlet, which uses its Fee Optimization product to control Balancer protocol swap fees. The proposition seeks to handover the swap fee controller to the Treasury subDAO and eventually implement an open-sourced, fully automated dynamic fee control based on market conditions.

March 21 – Delegate Treasury subDAO the Power to Invest Protocol Fees

This proposal aims to delegate the management of Balancer DAOs collected revenue from fees to the Treasury subDAO. Under the new veBAL tokenomics, 75% of protocol fees will be sent to veBAL, and 25% will go to Balancer DAO. The initial framework for the utilization of protocol fees includes: reduce selling pressure on BAL, ensure operational runway for the DAO, maximize risk-adjusted yield, and build protocol-owned liquidity. The Treasury subDAO will initiate a sweep of all collected protocol fees just before the launch of veBAL and invest them on behalf of the DAO.

March 21 – Hexagon Friendly Fork

This proposal is drafted by the Partnership subDAO and aims to introduce a multifunctional platform, called Hexagon Finance. Hexagon will serve as a joint project between BalancerDAO, Ava Labs, and Terra Labs focused on bringing Balancer products and infrastructure (via a smart contract fork) to the Avalanche community. Balancer would be responsible for assisting in promotional activities such as public announcements, AMAs, the allowance of Hexagon Finance to use Balancer branding, and official approval of the Hexagon Finance protocol on Avalanche.

Hexagon Finance tokenomics would distribute 6%, or 6 million, of the total Hexagon Finance token supply to BalancerDAO. The release would be locked for 6 months upon launch and linearly vested for 12–24 months. Ava Labs will provide additional funds dedicated to the Liquidity Mining program, and Terra Labs will provide initial capital deployment of UST to build the initial phase of liquidity bootstrapping.

Conclusion

Despite Q4’s market drawdown, Balancer showed continued progress toward its goals in several key measures. By number of pools, Balancer continues to see DAOs and protocols use its platform to build. Although end users pulled back from the market, Balancer saw less of a downturn than some peers. The newly launched boosted stable pool continues to suck up liquidity, proving to be another useful tool on the platform.

The most important change in the quarter was the governance overhaul and announcement of veBAL. As a new incentive and voting mechanism, veBAL changes the dynamic for liquidity providers on Balancer and changes the utility of BAL. As the majority of DAO-directed liquidity mining rewards have started to wane, Balancer has turned to market forces to determine the allocation of its reward incentives going forward. The active community and strong team continue to work to improve the protocol and partnerships heading into the second quarter of 2022.

Appendix

This report was commissioned by Balancer, a member of Protocol Services. All content was produced independently by the author(s) and does not necessarily reflect the opinions of Messari, Inc. or the organization that requested the report. Paid membership in Protocol Services does not influence editorial decisions or content. Author(s) may hold cryptocurrencies named in this report.

Crypto projects can commission independent research through Protocol Services. For more details or to join the program, contact ps@messari.io.

This report is meant for informational purposes only. It is not meant to serve as investment advice. You should conduct your own research, and consult an independent financial, tax, or legal advisor before making any investment decisions. The past performance of any asset is not indicative of future results. Please see our terms of use for more information.