(NOTE: This report was commissioned by Osmosis and written prior to the recent market crash of the Terra Protocol and its LUNA token and the depegging of the UST stablecoin. All data utilized refers to the Q1 period ending March 31st. For Messari reactions to recent events, please refer to this piece here.)

Key Insights

- Both Osmosis trading volume and supplied liquidity continued to grow in Q1 2022 even as the broader market capitalization of crypto fell 50% from $3 trillion to $2 trillion.

- The launch of superfluid staking increased the number of OSMO tokens staked with the protocol, but overall measurements of decentralization remain low.

- The top pools as measured by volume and liquidity all contained some combination of the OSMO, ATOM, LUNA, or UST tokens.

- A key governance event was the decision to match external rewards with OSMO tokens to incentivize outside protocols to launch liquidity mining rewards and help grow liquidity available on the DEX.

- Some roadmap items include updates to the Liquidity Bootstrapping Pool and stableswap AMM, integration with Ethereum, and rather famously, the addition of MEV-resistance.

Introduction to Osmosis

Osmosis is a sovereign DEX-focused app-chain in the Cosmos ecosystem, meaning it serves simultaneously as a blockchain and an application. The application operates similarly to other AMM functioning DEXs — that is to say, liquidity providers (LPs) are responsible for supplying liquidity to asset pair pools where traders can make trades from. It’s the same model for Uniswap or Balancer, though more similar to the latter as Osmosis places a high priority on offering asset pool customization. Tweaks to market-maker functions, swap costs, token weighting, and more, are all parameters that can be changed.

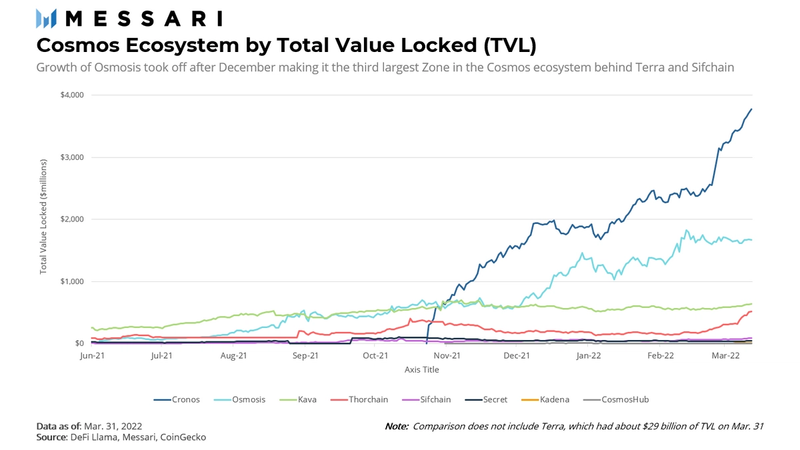

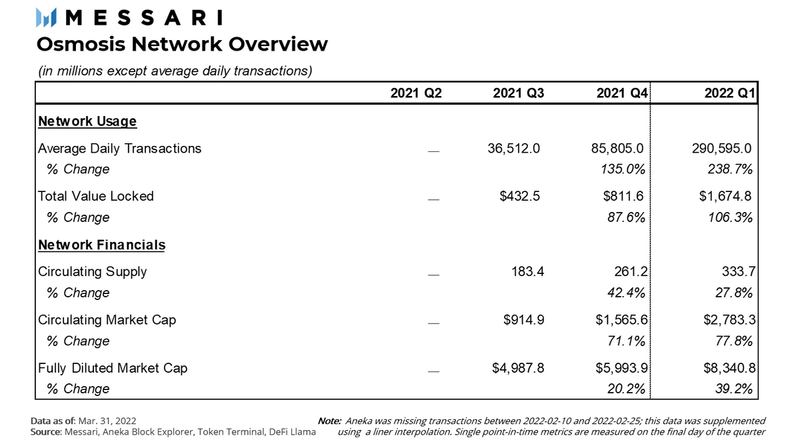

In Q1 2022, protocol-level total value locked (TVL) and validator count continued to rise, with validator count being a work in progress when evaluated by degree of decentralization. On the DEX side, Osmosis serves a key role as the primary exchange in the Cosmos ecosystem. Important governance updates include the expansion of superfluid staking to other OSMO pools and the approval of incentive matching for projects that choose to provide external liquidity rewards.

Layer-1 Metrics

As the Cosmos universe expands, early protocols continue to prove the importance of having first-mover advantage. Osmosis was the first IBC-enabled DEX in the Cosmos ecosystem, which led to it also being the first DEX to see significant IBC transfer volume. To date, Osmosis remains the leader in the Cosmos ecosystem for inter-protocol volume, leading second-place Terra by more than 150% and third-place Cosmos Hub by more than 250% in total volume. In fact, Osmosis is so far ahead of Cosmos’s own native DEX that it recently changed its name from Gravity to Crescent to rebrand, implement new features, and eventually attract more usage.

Despite the overall decline in crypto market capitalization, Osmosis actually saw accelerated growth in many metrics over Q1. In terms of activity on the network, the average number of daily transactions nearly tripled over the quarter (+238.7%). Even TVL, which is usually sensitive to overall market valuations, more than doubled (+106.7%).

A lot of this growth can be attributed to the popularity of the multi-chain, scaling and interoperability theses over Q1. The Cosmos ecosystem, of course, was a central beneficiary of the surge in adoption that followed.

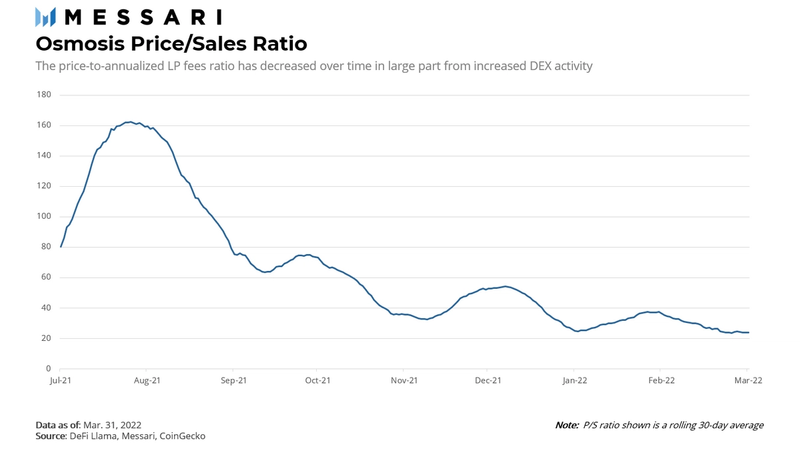

Despite the network’s extreme growth, traditional financial metrics managed to move towards a more favorable fundamental valuation. By dividing circulating market cap by annualized daily LP fees, we are able to derive a price/sales ratio. This metric now sits at a more attractive 13.6x at the end of Q1 after peaking above 260x in the summer of 2021. A big factor leading to the decline of the P/S ratio comes from recent surges in protocol revenue, which brings the denominator number up. Just in Q1 alone, LPs were able to bring in 187% more than in the previous quarter. The more attractive valuation metric at the end of the quarter also comes in line with more LP capital efficiency, which will be discussed further below.

Still there are other metrics to monitor. Those following the Cosmos ecosystem may know the so-called “Internet of Blockchains” has one unique challenge: decentralized validators. Since each Zone is its own independent blockchain and needs its own security, it can be difficult to attract a diverse set of validators. Compared to a singular blockchain-centric model such as Ethereum where security can be inherited, networks like Osmosis must bootstrap their own security.

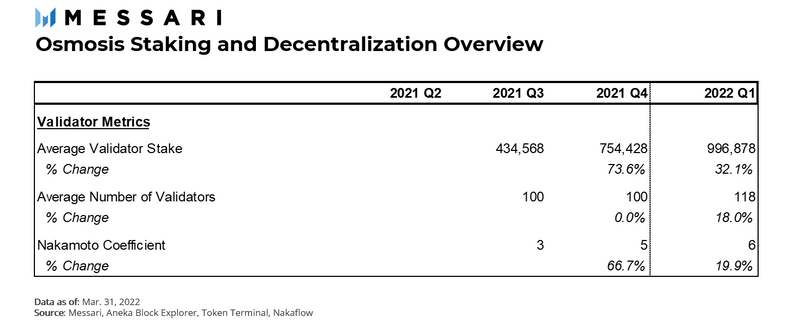

Osmosis ended Q1 with a total of 118 validators after adding 18 validators over the quarter. Although the growth of validator count follows a fairly linear path, the rate of growth is slower than the growth of block height, or the total length of the blockchain.

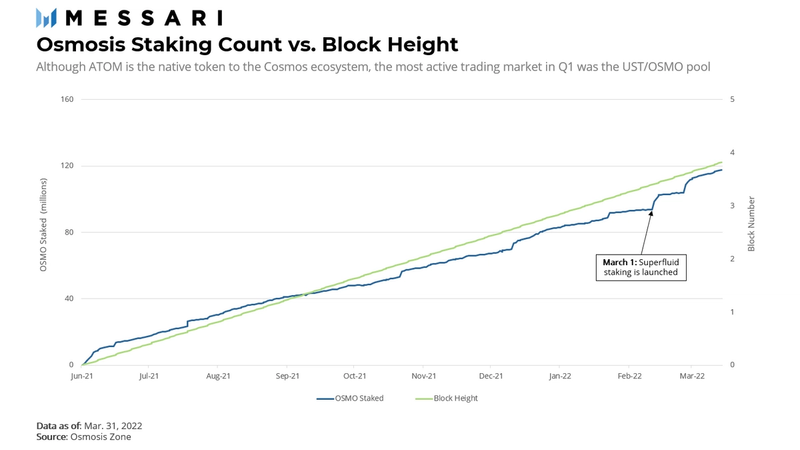

Meanwhile, those 118 validators benefitted from the Q1 launch of superfluid staking, one of Osmosis’s biggest protocol-level differentiators. Superfluid staking gives LPs the ability to simultaneously provide liquidity for OSMO-backed markets while also staking those same OSMO tokens in the network for traditional staking yield. The advantages of superfluid staking are twofold: LPs double-up on yields earned from providing liquidity and network security, and the protocol increases the number of staked tokens. Over the quarter, the number of OSMO tokens staked with those 118 validators grew 32% to 117.6 million. The average number of tokens staked with each validator approached nearly 1 million.

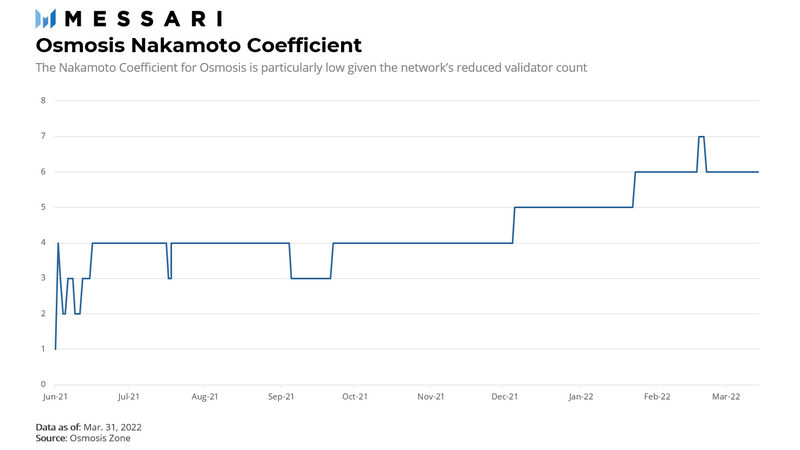

That said, overall network decentralization remains low, according to the Nakamoto Coefficient, which measures the number of validators needed to take control of a network. Although the metric has increased marginally over time, from five to seven in Q1, it continues to reflect how centralized Osmosis is when compared to other blockchains. Terra and Thorchain, two other Cosmos chains, have Nakamoto Coefficients of 12 and 29, respectively. Additionally, Solana, a network sometimes criticized for its higher degree of centralization, has a coefficient value of 20. Given how far Osmosis lags behind other blockchains in this respect, it still needs to significantly improve its decentralization.

DEX Metrics: Macro

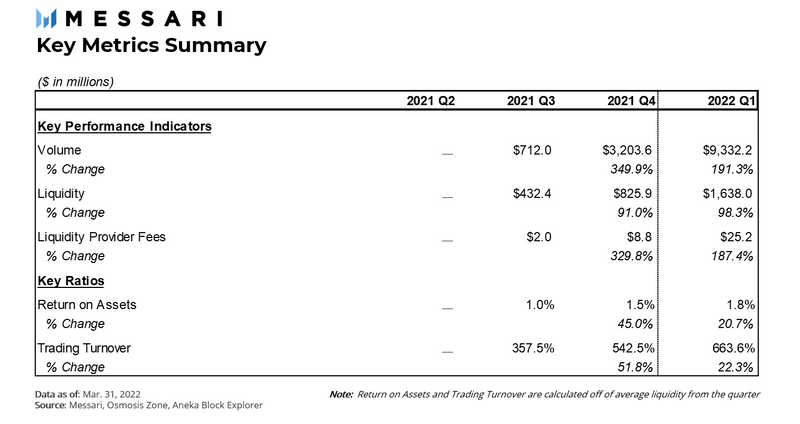

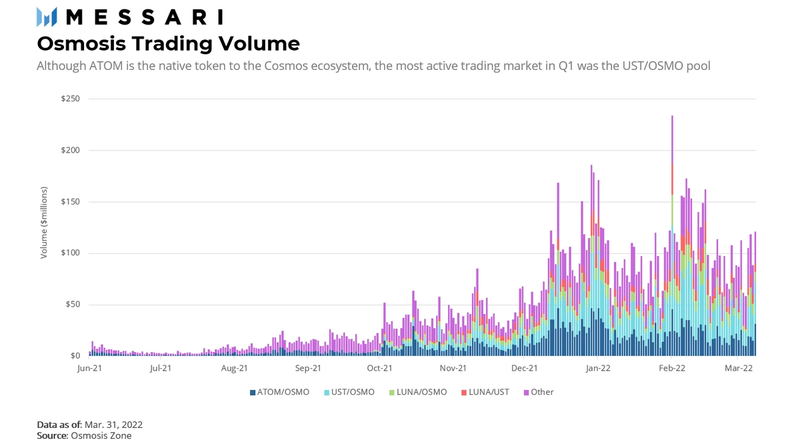

As mentioned prior, Osmosis leads all Cosmos app-chains in IBC transfer volume, a metric used to measure volume of tokens transferred between different app-chains. More than 50% more volume occurred on Osmosis over the quarter than the next most active all-chain. Furthermore, total trading volume – a different volume metric used to categorize total trading activity – across the DEX totaled $9.3 billion for Q1.

On a quarter-over-quarter basis, growth did slow in Q1 compared to Q4. Total volume jumped 191.3% from Q4 after growing 349.9% from the previous quarter. However, broader context puts this in a favorable light. First, while percentage growth slowed between quarters, growth in dollar-based terms continued to rise. $6 billion of volume was added while Osmosis volume grew $3 billion the previous quarter, so interest remains high. Second, it’s worth noting the market capitalization of cryptocurrency peaked in Q4 at $3 trillion and fell to $2 billion in the Q1 period. In light of the ecosystem falling as a whole, the fact that Osmosis grew while other spot-based DEXs such as Uniswap fell reflects positively for the young protocol.

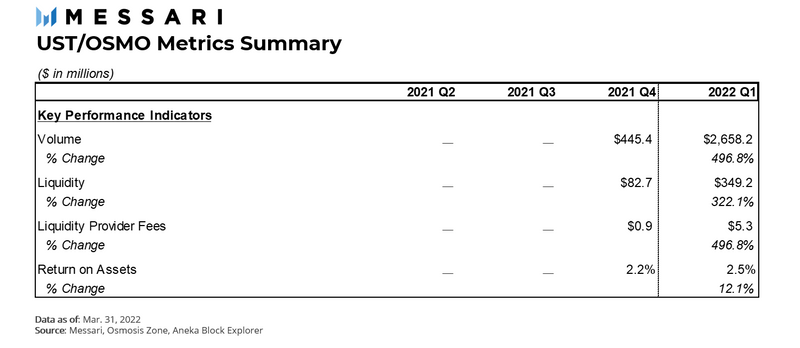

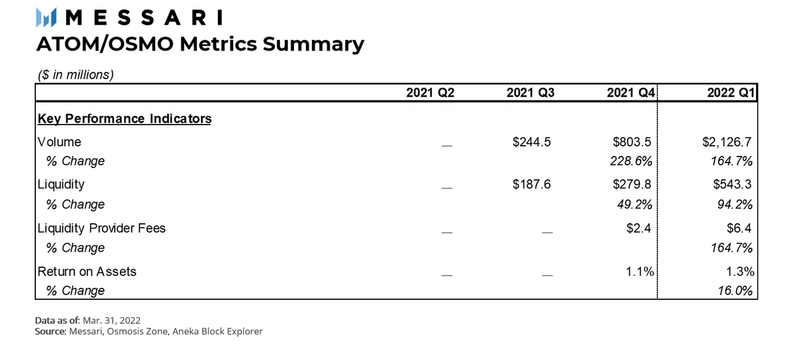

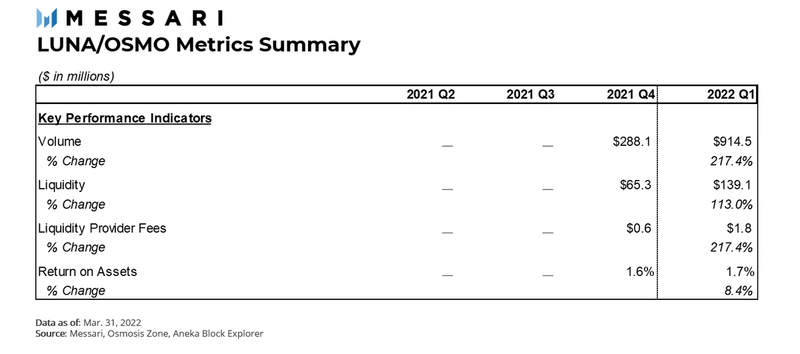

Big picture trading volume on the DEX tells a story: token swaps are on the rise as Osmosis rides the wave behind the emergence of Cosmos and the multichain investment paradigm. Analyzing specific markets supports that story: The most active pools are those related to the ecosystem’s largest assets. Four pools in particular comprise the majority of activity. On Osmosis, the (1) ATOM/OSMO, (2) UST/OSMO, (3) LUNA/OSMO, and (4) LUNA/UST pools add up to 69.1% of all volume. If you’ve been following the interest of Cosmos Zones, this shouldn’t be too surprising: Two of the four assets across the pools belong to the Terra ecosystem, LUNA, and its stablecoin, UST.

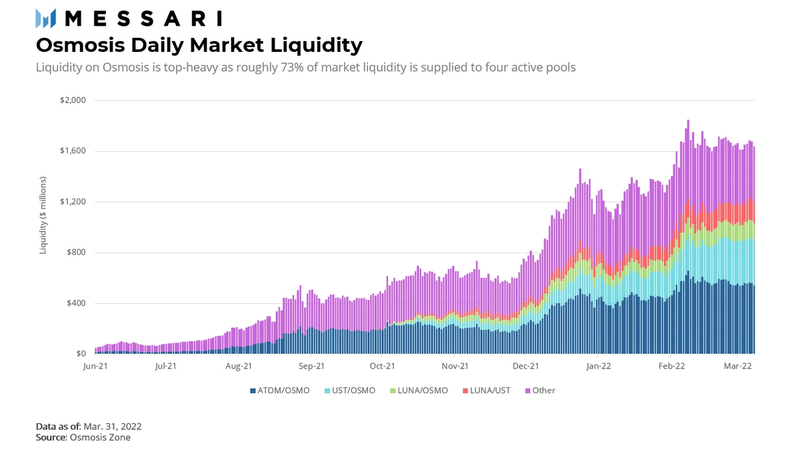

Which pools are liquidity providers choosing to supply capital to? The answer is the same pools as those above seeing the highest trading volume. Once again, those four pools represent 73.2% of all liquidity in the DEX. The UST/OSMO pool grew the most by percentage, followed by the LUNA/UST pool. It also grew the most by $266.5 million on a nominal basis, though that was closely followed by the ATOM/OSMO pool at $263.5 million.

The dramatic jump in percentage terms originates from the relative low liquidity in the UST/OSMO pool to start the quarter. In fact, liquidity in the UST/OSMO pool did not see capital until the end of October. To contrast, the ATOM/OSMO pool saw initial liquidity supplied back in June 2021 and already had $200 million in supplied liquidity when the UST/OSMO pool was just getting started.

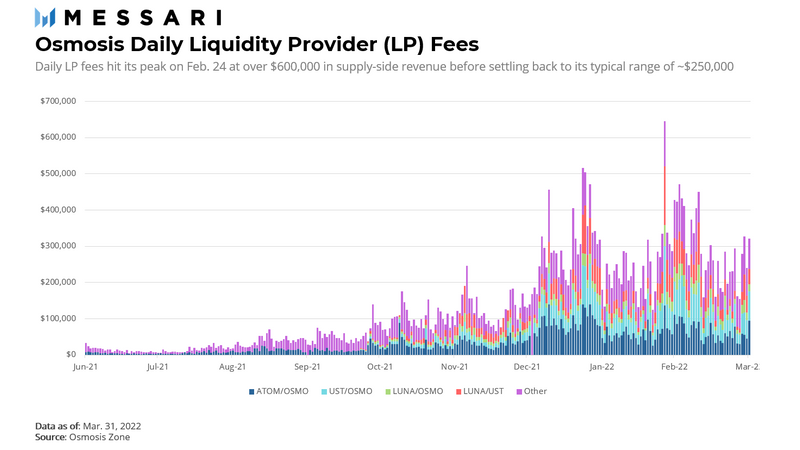

Liquidity provider fees (excluding impermanent loss or exit fees) brought in $25.2 million for liquidity providers. The 187.4% increase from Q4, which we can label as supply-side revenue, is in line with the increase in trading volume, which increased by 191.3%. Differences between the two numbers can be chalked up to the particulars of each pool. Unlike Uniswap V2, for example, Osmosis pool parameters are customized by LPs, leading to disparities between volume and fee increases.

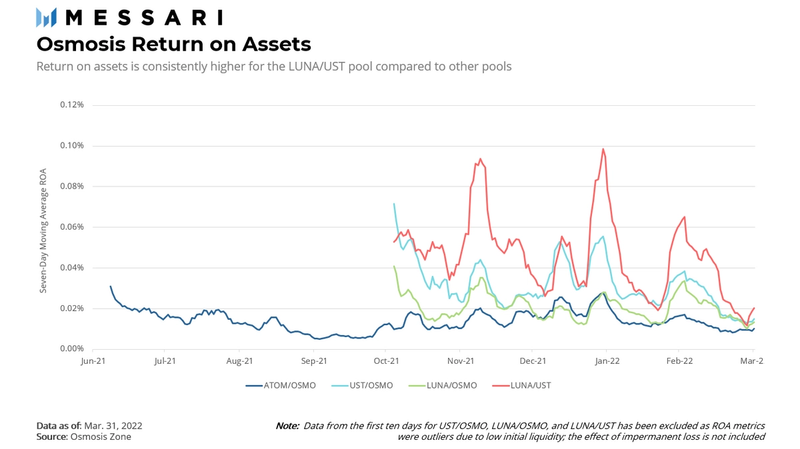

Taking the total supply-side revenue (LP fees) and dividing it by liquidity supplied introduces the return on assets (ROA) metric. The ratio is essentially the amount of revenue a liquidity provider is earning per dollar of liquidity supplied to the pool. It should be noted, however, that the supply-side revenue used here ignores both internal or external incentives, which are distributed to liquidity providers of top pools. It also ignores yields earned from those participating in superfluid staking or losses from impermanent loss; instead, only revenue earned as trading fees are taken into account.

The ROA among the four main pools is consistently highest for the LUNA/UST pool and lowest for the ATOM/OSMO pool. The high return for the UST-backed market is noteworthy for its efficiency (i.e. more trading volume per unit of base liquidity). Before UST-markets, Osmosis traders did not have any stablecoins markets to trade. The introduction of UST as a widely-used stablecoin introduced a new dimension to Osmosis – and the popularity of making swaps against stablecoins compared to other volatile assets led to higher LP ROA.

DEX Metrics: Micro

Since Osmosis is viewed as one of the primary capital facilitators of sorts for various app-chains in the Cosmos ecosystem, its position gives a unique viewpoint into what markets traders are trading.

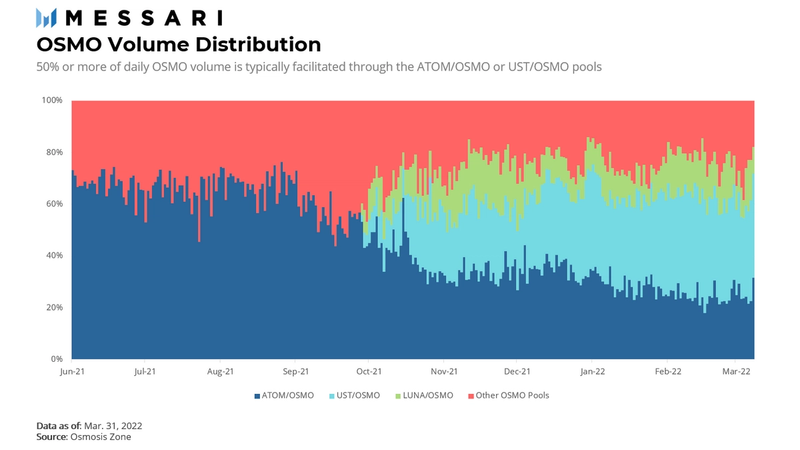

Starting in Q3 2021, over 60% of OSMO trades were conducted in the ATOM/OSMO pool. This should make sense: Attention at the time was focused on projects in the Solana ecosystem; the multi-chain investment thesis had not yet widely taken off as a scaling solution; and only a few other Cosmos projects had gained traction. If a trader were to make a trade with OSMO, it was likely that trade would be to swap between ATOM and OSMO. More importantly, any trade on the Osmosis protocol requires the possession of OSMO to pay for transaction fees much like ETH on Ethereum or SOL on the Solana blockchain. This need drives significant demand for the OSMO token as a native currency.

Starting around the second half of October 2021, OSMO trading volume began to pick up in other pools, specifically those related to the Terra blockchain. Both UST/OSMO and LUNA/OSMO saw increases in trading dominance. Those two pools now see 50% or more of daily OSMO trading volume whereas the ATOM/OSMO pool has fallen between 10% and 20% on a daily basis. All in all, volume is evenly distributed with no one trading pool accounting for the majority of volume.

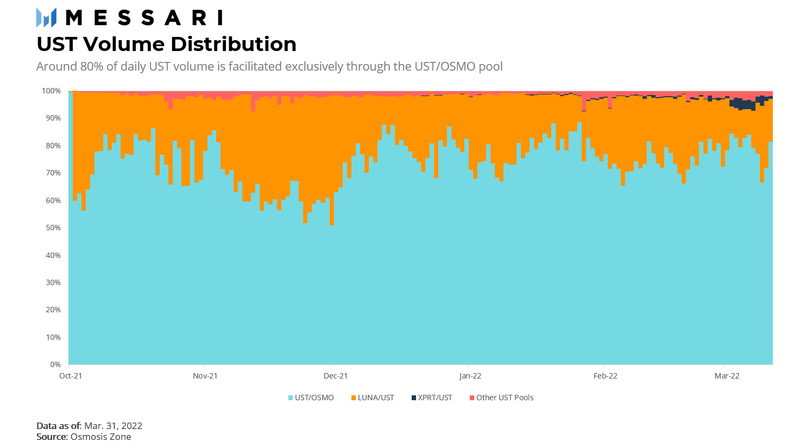

On the other hand, the trading dominance of UST is not quite as evenly distributed as the OSMO token. Around 70–80% of the token’s volume is found in the UST/OSMO pool. As briefly mentioned above, UST can be thought of as the Cosmos ecosystem’s native stablecoin: Traders require a widely available USD-pegged asset to eliminate one side of volatility when buying or selling OSMO. Thus, it makes sense to see the majority of activity facilitated by traders between OSMO (the token spent for transaction fees) and UST (the prevalent stablecoin).

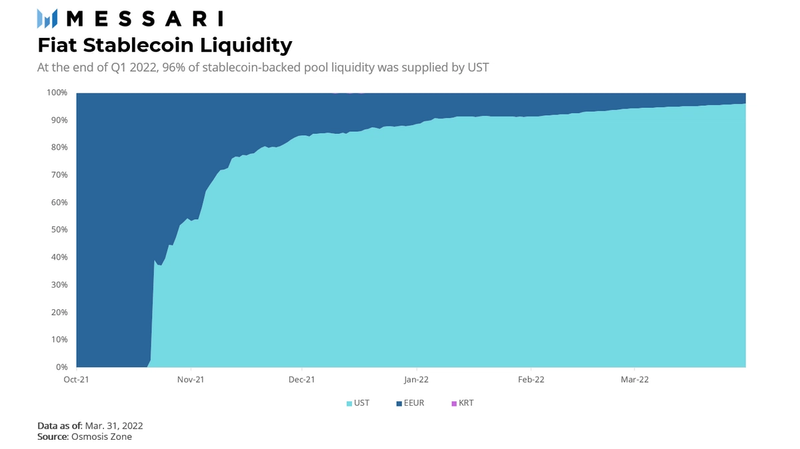

In actuality, UST’s presence in the Osmosis protocol is overrepresented and should be flagged as a risk. The algorithmic stablecoin accounts for 96% of stablecoin liquidity on the DEX with Euro-pegged stablecoins effectively comprising the remaining 4% (i.e. a small amount KRW-pegged stablecoin is used but both volume and liquidity are negligible). Should something happen to UST, a nonzero possibility given its algorithmic mechanism, Osmosis would be without any USD stablecoin markets. To its credit, the community has recognized the need for diversification and is preparing to vote on its choice of bridge to bring over ERC-20 assets.

Governance Updates

January 12, 2022 – Signaling Proposal: ION DAO and Treasury

ION, Osmosis’ enigmatic, blank-slate secondary asset, was fairdropped to over 16,000 addresses. Through Prop 32 all unclaimed IONs were clawed back and placed in the Osmosis community pool. This signaling proposal, which doesn’t outline implementation, pre-commits the clawed-back ION to an ION DAO once it exists.

January 30, 2022 – Incentive Matching Fee Based and 1:1 Caps

Osmosis matches external incentives with OSMO to encourage projects to provide liquidity rewards. This is a two part proposal, the first part ensures that a pool doesn’t receive more than twice the OSMO it would normally receive. The second part of the proposal limits external incentive matching at a 1:1 USD ($) value, of OSMO and the respective partner project token. The goal of this proposal was to protect APRs on non-externally matched pools, while still keeping rates on externally matched pools attractive.

March 14, 2022 – Enable Superfluid Staking on OSMO/UST and OSMO/LUNA

When superfluid staking launched on February 28, 2022, it only supported ATOM/OSMO (pool #1), the most liquid pool on Osmosis. Two weeks later OSMO/UST (pool #560) and OSMO/LUNA (pool #561), the second- and third-largest pools (by TVL) at the time, were the next two pools to add superfluid staking and the first pools enabled by governance.

Road Ahead

There are a few main roadmap items for Osmosis. The first is a second version of the Liquidity Bootstrapping Pool (LBP 2.0), Ethereum integration, and a stableswap AMM. While there hasn’t been much released around LBP 2.0, the community’s assumption is this will improve the processes around initial price discovery and stabilizing liquidity.

The second major roadmap item is Ethereum integration. Osmosis Labs will be integrating Axelar as the Bridge Service Provider into the Osmosis Zone. It will bring over canonical, bridged assets from Ethereum.

The final major roadmap item is a new stableswap AMM using Andre Cronje’s Solidly curve. This will make it easier to trade similarly priced, pegged assets (i.e., stablecoins).

Osmosis has also stated a desired goal to implement MEV-resistance. MEV-resistance refers to the ability for blockchain validators to order blocks in a manner advantageous to themselves. For example, validators could see arbitrage opportunities sent by transactors and choose to front-run them by placing the same transaction – conducted instead by themselves – instead of the other party. Osmosis intends to stop validators from seeing transaction-level detail until the blocks are finalized, thus preventing MEV. MEV-resistance is not yet live, but the team has announced their intent. This feature will likely launch relatively soon.

Finally, in a similar vein to Bitcoin’s halving, the new issuance of OSMO tokens will be cut by one third every year. The OSMO Thirdening will take place on June 19, 2022, at which point 200 million OSMO will be emitted over the following year. As a consequence, liquidity providers can expect lower APRs boosted by fewer OSMO token rewards thereafter.

Conclusion

All DEXs serve an important function as a means of price determination, liquidity, and capital formation. This applies for any crypto environment, but it’s especially pertinent for the Cosmos ecosystem, where a multitude of sovereign Layer-1 networks share high degrees of interoperable commonalities. Having ways to connect them – for example, by way of markets – is a must.

By all available data, Osmosis is capturing that niche well. Its Q1 trading volume, liquidity, and TVL are on the rise despite bleaker market sentiment, signaling interest from long-term, thesis-driven investors. And despite its achievements, it still has multiple key developments planned. Among them, bridging over ERC-20 assets will be vital. That alone will bring over to Osmosis all of crypto’s most widely-used stablecoins and open up new trading markets. Regardless of short-term trends, what matters is if crypto will move to a multi-chain world. And if it does, Osmosis plans to be prepared for it, heading into Q2 and beyond.

Appendix

This report was commissioned by Osmosis, a member of Protocol Services. All content was produced independently by the author(s) and does not necessarily reflect the opinions of Messari, Inc. or the organization that requested the report. Paid membership in Protocol Services does not influence editorial decisions or content. Author(s) may hold cryptocurrencies named in this report.

Crypto projects can commission independent research through Protocol Services. For more details or to join the program, contact ps@messari.io.

This report is meant for informational purposes only. It is not meant to serve as investment advice. You should conduct your own research, and consult an independent financial, tax, or legal advisor before making any investment decisions. The past performance of any asset is not indicative of future results. Please see our terms of use for more information.