Key Insights

- Lido is a non-custodial liquid staking protocol for Ethereum, Solana, Kusama, Polygon, and Polkadot.

- Lido abstracts away the challenges and risks around maintaining staking infrastructure by allowing users to delegate their assets, in any sum, to professional node operators.

- Stakers receive liquid, tokenized staking derivatives, also known as Lido-staked assets (stAssets), to represent their claim on the underlying stake pool and its yield.

- stAssets effectively unlock liquidity and remove the opportunity cost of staking since they can be used on a number of popular DeFi protocols to generate additional yield.

- Node operators are added to Lido through a DAO vote and are responsible for the actual staking.

- Lido is currently the fourth largest protocol by total value locked (TVL) and accounts for almost one-third of all staked ETH.

Staking, a cryptoeconomic primitive that allows participants to earn yield in exchange for locking tokens, has taken center stage over the past two years. Much of the attention comes from the shift to Proof-of-Stake (PoS) as the dominant consensus mechanism for smart contract platforms. Under PoS, instead of using computational power, validators lock (“stake”) a certain amount of the network’s native cryptoasset as collateral to create new blocks. In return, they earn inflationary rewards and transaction fees.

Beyond reducing energy consumption and increasing throughput, the shift to PoS also expands participation in the consensus process. However, most PoS networks still have high barriers to entry and opportunity costs for prospective stakers. Large minimum capital (stake) requirements, technical complexity around the validation process, and extended lockup periods stand in the way of their ability and willingness to stake.

As a result, an entire industry called Staking-as-a-Service has spawned to give tokenholders simple, flexible, and capital-efficient access to staking. The leader of this industry is Lido, a non-custodial, cross-chain liquid staking protocol. Lido abstracts away the challenges and risks around maintaining staking infrastructure by allowing users to delegate their assets, in any sum, to professional node operators. In return, stakers receive a tokenized derivative that represents their claim on the underlying stake pool and its yield. These liquid staking derivatives, known as Lido-staked assets (stAssets), can then be traded or used as collateral on a number of popular DeFi protocols.

For Ethereum, Solana, Kusama, Polygon, and Polkadot tokenholders, Lido is simultaneously opening up the opportunity to stake while reducing the opportunity cost of staking. Not only does this democratize access and create a more robust DeFi ecosystem, but it can also lead to more secure decentralized PoS networks as Lido progresses along in its roadmap.

Background

The Lido DAO was founded in 2020 by a group of prominent individuals and organizations including P2P Validator, ParaFi Capital, Stani Kulechov (Aave), and Twitter personality Jordan Fish (@cobie). The initial goal was to resolve some of the user experience issues in the Ethereum staking process, i.e., the significant upfront capital investment (32 ETH minimum), technical challenges around the validation process, and illiquid funds (locked until after The Merge).

The Lido liquid staking protocol launched a few weeks after the Beacon Chain in December 2020. After gaining traction, Lido went multi-chain, adding support for Terra (March 2021), Solana (September 2021), Kusama (February 2022), Polygon (March 2022), and Polkadot (June 2022). Recently, however, the Lido DAO voted against launching on the Terra reboot (Terra 2.0). Lido also continued to diversify its validator set by onboarding additional node operators through governance.

How Lido Works

The Lido DAO governs the five Lido liquid staking protocols. While each of the five supported PoS networks, Ethereum, Solana, Kusama, Polygon and Polkadot, have differences in design, the general mechanics around their liquid staking protocols are similar.

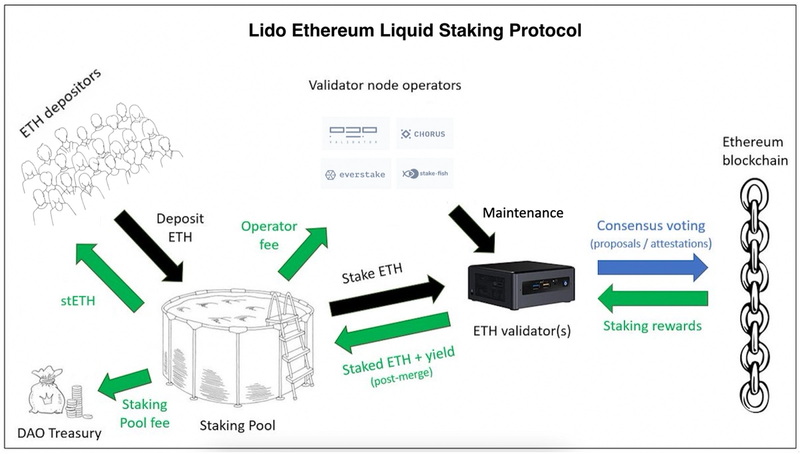

How Ethereum staking works on Lido. Source: @Leo_Glisic, Messari

The two main parties involved are the users (stakers) and node operators (validators). The key protocol components are the staking smart contracts, the tokenized staking derivatives (stAssets), and the external DeFi integrations (e.g., Curve).

Node Operators

The first critical component of a liquid staking protocol is its node operators because they are responsible for the actual staking. As of now, node operators are added and removed through the Lido DAO.

The whitelisting process starts with the Lido Node Operator Sub-Governance Group (LNOSG). The group currently consists of a representative from each of Lido’s twenty-one Ethereum node operators. Applications open up when Lido is launching on a new network or if LNOSG thinks a network can handle and benefit from additional node operators. The committee evaluates applicants based on several factors including reputation, past performance and the security, reliability, and novelty (uncorrelated nature) of their setup. Once LNOSG evaluates an applicant pool, it submits a list of recommended node operators to the Lido DAO for a tokenholder vote. A good validator set is critical for Lido since earnings and slashing penalties are socialized across all stakers in a given liquid staking protocol (e.g., all stETH holders).

Lido is also non-custodial, meaning node operators can’t directly access user funds. Instead, they must use a public validation key to validate transactions with staked assets. In order to align incentives, Lido node operators are compensated with a commission on the staking rewards generated from delegated funds.

Staking Contracts

Users delegate stake to node operators through Lido’s smart contracts. The three main smart contracts are the NodeOperatorsRegistry, the staking pool, and the LidoOracle.

Lido Ethereum staking; under the hood. Source: The Lido Blog

The NodeOperatorsRegistry holds the list of approved node operators.

The staking pool is the protocol’s central smart contract. Users interact with the staking pool by depositing and withdrawing their cryptoassets and minting/burning stAssets. The staking pool distributes the deposits uniformly (round-robin) to node operators using their addresses and validation keys. The staking pool contract is also responsible for distributing fees to the Lido DAO treasury and node operators.

How LidoOracle (“Oracle”) interacts with the staking pool on Ethereum. Source: The Lido Blog

The LidoOracle is responsible for keeping track of staking balances. The net staking reward, the difference between the staking yield and any slashing penalties, is tallied up daily and sent to the staking pool contract. The staking pool distributes 10% of the net staking reward by minting a proportional amount of the stAsset: 5% goes to node operators and 5% to the Lido DAO treasury. The remaining 90% of net staking rewards go to stAsset holders. Depending on the network, the rewards either show up as increases in the stAsset through its balance (via the rebasing mechanism) or its exchange rate.

Lido-staked Assets (stAssets)

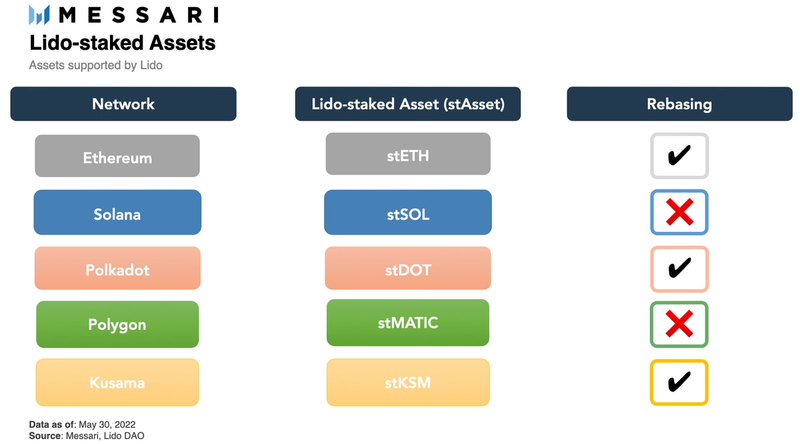

In exchange for depositing assets into one of Lido’s liquid staking protocols, users receive a staking derivative (stAsset). This tokenized claim on the stake pool effectively unlocks the liquidity of staked assets while they continue to secure their respective networks and earn rewards. stAssets come in two different forms: rebase and shares.

Rebasing tokens (stETH, stKSM, stDOT) are minted at a 1:1 ratio with the deposit asset. In order to match the underlying stake, the token balance rebases every day to factor in accrued staking rewards. The daily rebase occurs regardless of where the stAsset is acquired; whether it’s directly from Lido, a decentralized exchange (DEX), or another holder.

Value-accruing tokens (stSOL, stMATIC) earn staking rewards through appreciated value, reflected in the stAsset to deposit asset (e.g., stSOL:SOL) exchange rate. Rebase tokens can be converted to value-accruing tokens by being “wrapped.”

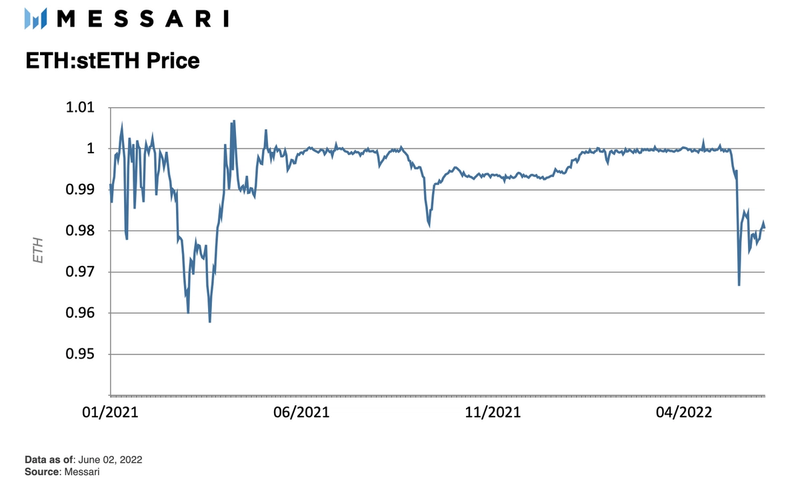

As of this writing, stETH accounts for over 98% of the value of stAssets in circulation.The stETH token is currently a purely synthetic, closed-end derivative since it can’t be directly redeemed for its underlying ETH until after The Merge. Instead, holders looking to convert their stETH to ETH rely on exchange (e.g., Curve, Uniswap, and FTX) pricing/liquidity.

DeFi Integrations

DEXs

In order to keep stETH liquid, the Lido DAO incentivizes the Curve stETH:ETH pool, currently the deepest AMM pool in DeFi. The Lido DAO token (LDO) and CRV incentives help attract liquidity by bolstering the pool’s APY. This pool, along with others like Uniswap and Balancer, gives stETH holders the ability to exit their staked positions for ETH before the unlock.

The price of 1 stETH should never really go above 1 ETH. This “ceiling” is in place because 1 ETH can always be used to mint 1 stETH through the Lido staking contract. However, the arbitrage mechanics aren’t as clear the other way around.

Since stETH can’t be burned for its underlying ETH on the Lido protocol, the exchange rate currently relies on the market’s price discovery under the ceiling. A number of factors come into play for the current (and historical) discount including the fact that stETH has less liquidity, less utility (e.g., can’t be used to pay gas fees), and more technical (smart contract) risk than ETH. However, the stETH price does not usually dip very far below 1:1 with ETH because it then starts offering arbitrageurs an attractive discount at future (post-unlock) redemption value.

Even for other stAssets, DEX liquidity is still useful because it gives holders the option to exit positions instantly, without having to wait through the stake deactivation period.

Lending and Borrowing

While Lido stakers can just hold their tokens or provide low risk (from impermanent loss) liquidity to a DEX, they multiply their opportunities when they start using stAssets as collateral. Some notable lending protocol integrations include Aave and MakerDAO for stETH and Solend for stSOL.

The most popular strategy so far has been recursive borrowing to get further leverage on stAssets. An example is leveraging stETH on Aave, which allows users to borrow up to 70% of collateral value. Repeatedly borrowing ETH and then resupplying stETH under this parameter allows users to triple their staking rewards, albeit with added risk to themselves and stETH.

Source: @Leo_Glisic, Messari

Recently structured products, like Index Coop’s icETH, have started offering leveraged stETH through Aave while mitigating some of the risks associated with managing collateralized debt. Nonetheless, an event like a hack, governance attack, slash across multiple node operators, or market-wide liquidity crunch could result in cascading liquidations and a large dislocation in the stETH/ETH pair. Nonetheless, the ability to borrow assets gets at the heart of capital efficiency and the illiquidity/lockup dilemma Lido is trying to solve.

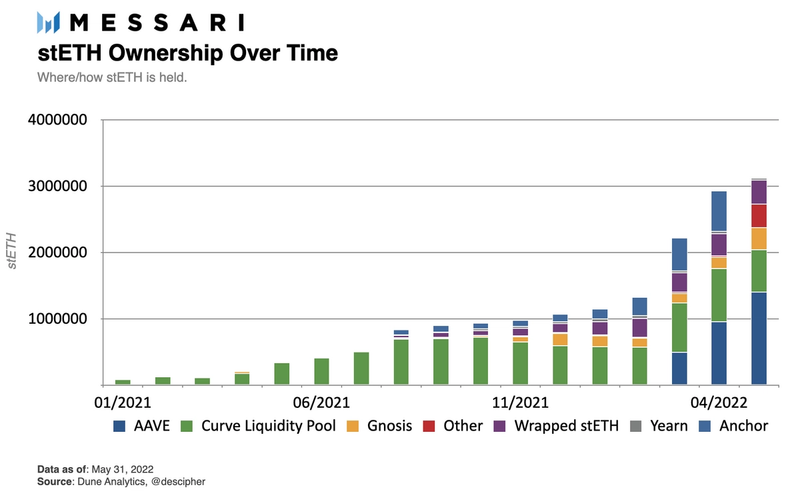

As shown above, there’s been massive growth in stETH on Aave since its integration at the end of February 2022. As of this writing, nearly 45% of stETH in circulation (almost 1.5 million stETH) is deposited in Aave. The second largest pool of stETH provides liquidity to the Curve stETH:ETH pair. Together, almost two thirds of stETH is split between the two protocols.

Traction and Competitive Landscape

At the beginning of May, Lido briefly overtook Curve to become the largest DeFi protocol by total value locked (TVL). Since the UST depegging, Lido’s overall TVL rank has hovered around fourth.

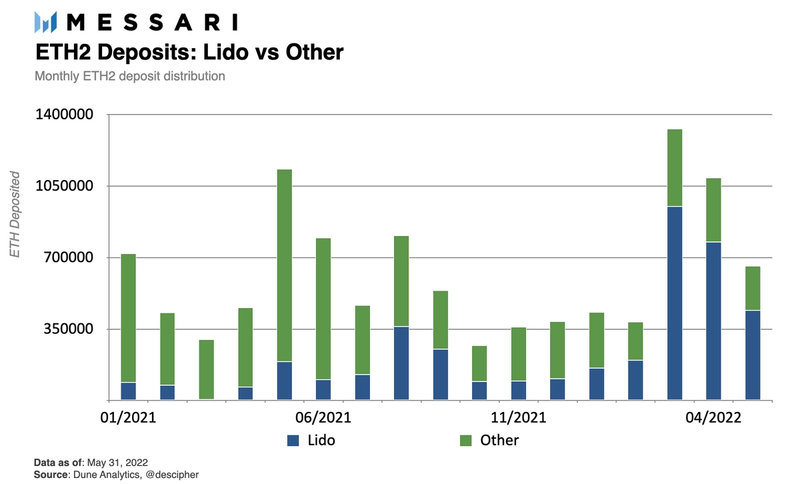

In May 2022, about 70% of new Eth2 staking deposits came from Lido. Overall, Lido accounts for 32.5% of all staked ETH.

However, Lido has over 90% market share in the non-custodial, decentralized liquid staking category.

The next closest competitor, Rocket Pool, has gained some ground and fanfare since launching in November 2021. However, despite more than tripling its staked ETH, Rocket Pool’s market share in non-custodial liquid ETH staking still remains under 4%.

The biggest difference between Rocket Pool and Lido is the validator set. Lido’s approach concentrates validators with professional, carefully selected node operators. Rocket Pool’s goal is to allow permissionless entry into the validator set and to secure stake through economic incentives rather than reputation/past performance. While Rocket Pool’s system does lead to wider participation in the validation process, it also creates capital inefficiency (i.e., requiring node operators to put up 16/32 ETH for each validator), which makes scaling a challenge.

Another major difference between the two protocols is around liquidity. The Lido DAO currently spends over 4 million LDO per month to incentivize liquidity across chains and their respective DEXs, with the vast majority of spend on the stETH:ETH pair. Rocket Pool, on the other hand, has no spend allocated towards liquidity. Lido’s incentive system boosts demand for stETH by simultaneously reducing slippage and creating a sort of “built-in”, base yield for stETH holders.

The bottleneck around onboarding stake, less liquidity and yield for rETH, along with the almost 1 year late start makes it difficult for Rocket Pool to catch up at this point. Thus, odds are high that stETH is already the schelling point for non-custodial liquid staked ETH.

The other major player in liquid staked ETH is Binance. Binance, however, is not a direct competitor given its custodial nature. And, while it does issue a liquid tokenized derivative (bETH), the token doesn’t accrue value when outside of the staker’s Binance wallet, making it considerably inferior to stETH and Rocket Pool’s rETH. bETH also lacks critical mass in terms of DeFi integrations. Zooming out, the three largest custodial staking solutions (Kraken, Coinbase and Binance) have deposited almost 2.7 million ETH combined, or about 60% of Lido’s stake. Looking forward, this gap is only widening since Lido is responsible for the vast majority (70%) of recent Eth2 inflows.

Even though Ethereum is clearly Lido’s bread-and-butter, Solana staking paints a more nuanced picture around Lido’s multichain expansion. First of all, Lido is not the category winner for liquid staking on Solana — that title goes to Marinade. Marinade currently has ~2.5 times Lido’s stake. However, more broadly, liquid staking is an incredibly small market on Solana, seeing as the top two protocols (Marinade and Lido) have roughly 2.5% of the total stake. In Eth2, Lido and Rocket Pool (the two top liquid staking protocols) make up almost 36% of the total stake. Some of the reasons behind this could be Solana’s native delegation feature combined with the higher liquidity on stake thanks to the 2–3 day unbonding period. While this complicates the outlook for Lido’s multichain expansion, in terms of competition and product-market fit, its brand, cross-chain synergy, and giant, somewhat cornered, market on Ethereum still paint a rosy picture overall.

LDO Token

LDO is the Lido DAO’s Ethereum-based, ERC-20 governance token. The Lido DAO is an Aragon organization, responsible for making decisions around the DAO itself (e.g., treasury) and the staking protocols (e.g., node operators, fees, etc.). A tokenholder’s voting power is commensurate with the LDO locked in their voting contract.

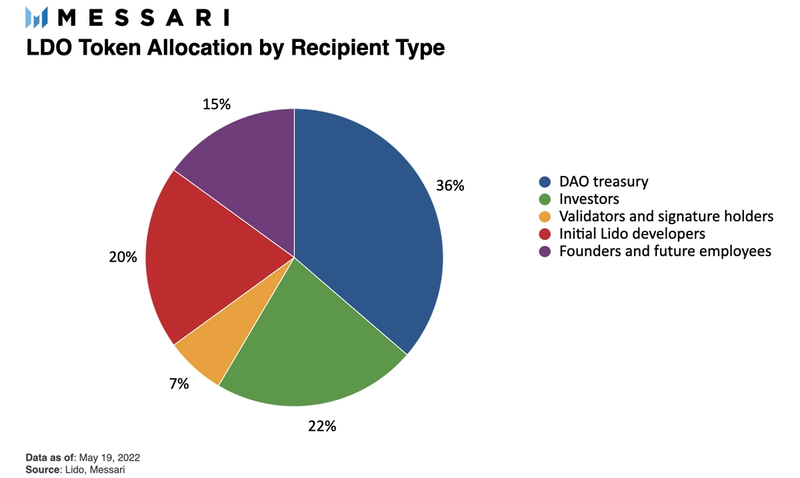

The distribution breakdown of the initial supply is 22.2% to early investors, 20% to initial Lido developers, 15% to future employees, and 6.5% to validators and withdrawal key signers. These groups were given roughly 64% of the total supply, with a 1-year lock, followed by a 1-year vesting period. The token generation event (TGE) took place on December 17, 2020; thus, these tokens will fully vest by December 17, 2022.

The remaining tokens, 36.2% of the total supply, belong to the Lido DAO treasury. They continue to be used on an ad-hoc basis, per DAO governance. Some uses so far have been liquidity incentives, advisory, VC sales, referral programs, and funding of the Ethereum Protocol Guild.

Risks

Given the Lido DAO’s heavy exposure to Ethereum, any setback around the timeline or execution of The Merge could be catastrophic. While a deep discussion around Ethereum 2.0 is out of scope, adverse events such as further delays in the transition date or a crisis of confidence around the transition itself could blow out the ETH:stETH discount. Given stETH’s rehypothecation, cascading liquidations could then put further downward pressure on the price. However, if The Merge executes smoothly, Lido will have a central role in the largest PoS chain.

The choice to gradually decentralize has allowed Lido to optimize for speed and scalability. While Lido has a first-mover advantage over competitors like Rocket Pool, Lido’s small node operator set has raised concerns about centralization on Ethereum. The LNOSG is a committee of insiders that controls the initial curation process around node operator selection. Even though there is eventually a Lido DAO vote on the finalized list, the LDO token has concentrated insider ownership as well. This has resulted in a system where 21 professional node operators manage all of Lido’s 32.5% share of ETH on Ethereum’s Beacon Chain. Furthermore, the withdrawal credentials for the ETH staked before July 15, 2021, are held by a 6-of-11 multisig. Once withdrawals are enabled, if more than five signatories lose their keys or go rogue, roughly 600,000 ETH (~15% of current total Lido ETH2 stake) could become locked. However, the Lido DAO team plans to migrate this stake to the 0x01 (upgradeable smart contract) withdrawal credentials as soon as it’s possible to do so.

In addition to this, Lido has laid out a plan for removing many of the other, remaining trust surfaces and decentralizing stake.

One part of the plan involves adding permissionless validation. Distributed Validator Technology (DVT) will allow Lido to onboard new, unknown, untrusted node operators by pairing them with trusted (whitelisted) node operators. These new validator groups will work together to propose and attest to blocks, while keeping each other in check.

The second part of the plan addresses the concentration of LDO ownership. It will give stETH holders the ability to provide oversight and veto decisions made by the DAO.

Closing Thoughts

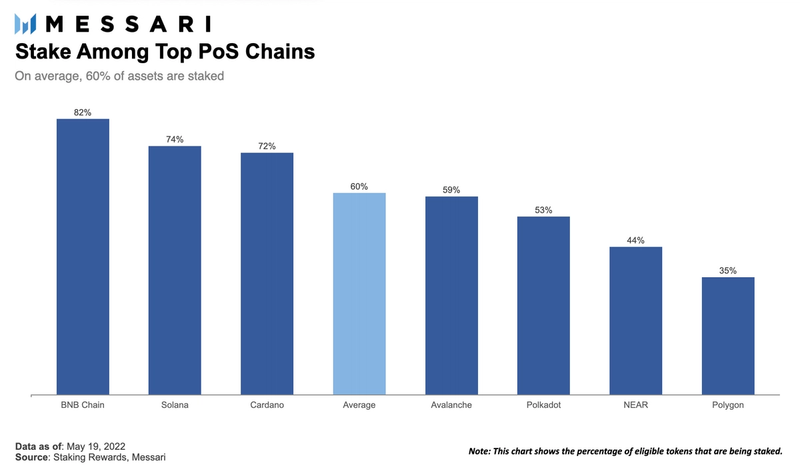

At the moment, only about 10% of ETH in circulation is staked. After the merge, stakers will have the option to withdraw, and staking rewards could double. If this catapults the proportion of ETH staked to the current average for top PoS chains, the percent of total ETH staked could increase by a factor of six. In addition to benefiting from a rising tide, Lido will also allow stakers to circumvent what could be a multi-month validator activation queue and immediately start earning staking rewards. Whether Lido offers lower yields or uses some of its treasury to plug the gap, Lido will have another great opportunity to cement itself as the market leader in Ethereum liquid staking.

However, with great power comes great responsibility. Lido will play a central role in securing the largest Layer-1 blockchain, and, directly or indirectly, billions of dollars in value, as of this writing. Contrary to what critics might say, this isn’t inherently wrong. The long-term consequences of Lido’s dominance on the Ethereum network, and the crypto ecosystem as a whole, will now depend primarily on the Lido DAO’s decisions around creating a safe and truly decentralized protocol. Regardless, the fact that Lido has ecosystem stakeholders thinking in years rather than days, weeks, or months, is a testament to the protocol’s projected staying power. Combining a robust ecosystem with a powerful flywheel effect is all it takes.

Looking to dive deeper? Subscribe to Messari Pro. Messari Pro memberships provide access to daily crypto news and insights, exclusive long-form daily research, advanced screener, charting & watchlist features, and access to curated sets of charts and metrics. Learn more at messari.io/pro

This report was commissioned by the Lido DAO, a member of Protocol Services. All content was produced independently by the author(s) and does not necessarily reflect the opinions of Messari, Inc. or the organization that requested the report. Paid membership in Protocol Services does not influence editorial decisions or content. Author(s) may hold cryptocurrencies named in this report.

Crypto projects can commission independent research through Protocol Services. For more details or to join the program, contact ps@messari.io.

This report is meant for informational purposes only. It is not meant to serve as investment advice. You should conduct your own research, and consult an independent financial, tax, or legal advisor before making any investment decisions. The past performance of any asset is not indicative of future results. Please see our terms of use for more information.