State of Fei Protocol Q2 2022

July 8, 2022

Key Insights

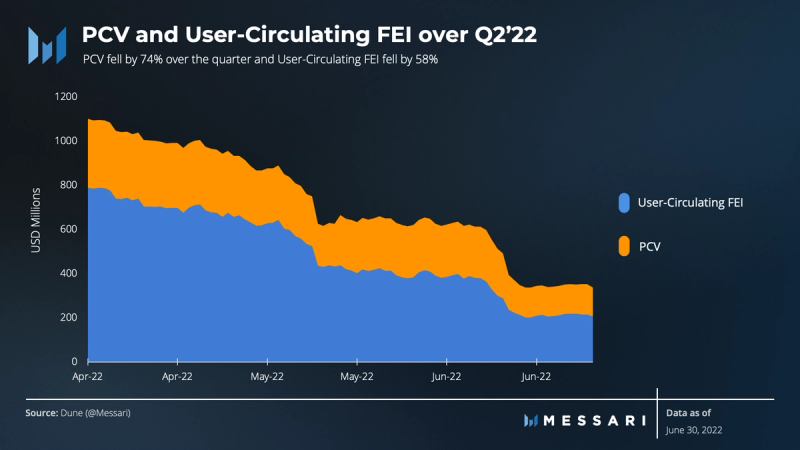

- The top priority was to maintain backing for the peg by keeping the Protocol Controlled Value above user-circulating FEI as the Collateral Ratio fell to 1.54 from 2.41.

- FEI didn’t have issues defending its peg this quarter, but usage continues to decline. With no strong demand driver for FEI, supply fell over 36% in the quarter.

- The new governance structure is functioning as intended, making some decisions require a stronger consensus from the DAO.

- Rari faced headwinds. Fuse, Rari’s main product, was hacked for $80 million and Rari’s co-founder departed.

- Market conditions require delayed product launches and a focus on survival.

A Primer on Fei Protocol

Initially launched in April 2021, Fei Protocol is a decentralized ERC-20 stablecoin project. The team innovated Protocol Controlled Value (PCV), using protocol-owned equity to backstop the algorithmic incentives it had created to manage a stablecoin peg. Because PCV is not debt or seigniorage, there is no risk of a liquidation event or death spiral. The risk lies in the fidelity and volatility of the PCV’s assets, relative to the outstanding liabilities in minted stablecoins. The Fei Protocol PCV consists of decentralized assets and is currently deployed to provide liquidity and earn yield. The “collateral ratio,” which measures circulating FEI supply to PCV, is a key metric in determining the credibility of the peg.

Fei V2 was announced in October 2021, removing the direct incentives mechanism in favor of 1:1 redeemability of FEI for decentralized assets ETH, DAI, and LUSD. The DAO manages the reserve pools that back these mint/redeem mechanisms, currently with a 50 bps spread. As part of V2, the DAO aligned TRIBE (the project governance token) with the stablecoin as seigniorage. TRIBE now benefits from the PCV’s earnings in the form of buybacks, while also playing backstop (seigniorage) if the PCV can’t backstop the existing stablecoin supply. In January 2022, Fei Protocol merged with Rari Capital to form Tribe DAO.

Introduction

In a quarter that saw multiple stablecoins depeg, FEI showed no such stress. The protocol’s primary objective, maintaining a USD stablecoin, was decidedly a success this quarter, despite the many other trials and tribulations for the protocol and DAO.

The goal is for FEI to be a PCV-backed stablecoin. The DAO controls the PCV and so decides how to allocate it. The tradeoff is found between taking risk to grow PCV and preserving the backing for FEI. Practically speaking, it really didn’t matter which asset the protocol chose as its reserve this quarter – almost all assets fell in USD terms (crude oil was up small). Therefore, the DAO made many decisions this quarter to consolidate PCV assets and increase stablecoin holdings.

An $80 million Fuse pool hack on the last day of April certainly didn’t help. This is the second Rari hack in its young life, and the second that TribeDAO holders are being asked to pay back. Another headwind after last year’s mega-merger between Fei and Rari is the core team from Rari leaving. One of the key upsides pitched for TRIBE holders was the combination of these two great teams, but less than six months in and only one core team member from Rari remains.

An important and related change this quarter was the implementation of a new governance structure. “Optimistic governance” is intended to speed up easy decisions and slow down hard ones. The Tribal Council was elected and has permission to execute most transactions for the DAO. They are limited by a timelock, whereby every action goes to a veto-able vote for the newly formed NopeDAO. All TRIBE holders can vote in NopeDAO proposals. Some proposals like selling ETH to increase stablecoins backing FEI faced no issues. A tougher decision like the implementation of the Rari hack repayment is taking much longer. The first attempt was vetoed, and governance discussions are now fully underway searching for the best method.

TribeDAO has been working on products to increase the adoption of FEI. Its target clients are other DAOs, which have obviously had a tough quarter, alongside TribeDAO. Product launches have been delayed as Fuse (Rari’s main product) is frozen post-hack and the DAO continues to focus on preserving FEI backing.

Performance Analysis

FEI Stablecoin

From an average daily price perspective, FEI remained more volatile around its dollar peg than the four leading stablecoins. Note that the table below is not based on tick-level data but average daily prices.

Although increasing adoption should help reduce this volatility, some of it is just due to the design of the price stability modules. The primary mechanism for the DAO to manage the peg is through price stability modules (PSMs). FEI’s PSMs allow users to swap FEI for DAI, LUSD, ETH, and RAI. The price for FEI in these PSM transactions is determined by a DAI TWAP oracle, with a 1-USD oracle wrapper in case of a DAI depeg.

The DAO controls the funding for each PSM. When empty, there is no enforcement mechanism for the peg. In volatile times, there is often more opportunity for arbitrageurs to trade with the PSM and help maintain the peg. The DAO must ensure there is ammunition there for this mechanism to function properly. The DAO also generates fees for mints and redeems of FEI at peg. They adjust these fees to incentivize/decentivize usage of the PSMs.

Where is FEI in the system? Currently, mostly in TribeDAOs lockers. As the team has reduced risk, they have taken protocol-owned FEI out of lending markets and DEXs. As not much FEI is used as collateral, the main home for FEI is currently on DEXs.

Protocol Controlled Value

Adverse market conditions, increased liabilities from the recent exploit, and an increase in FEI redemptions put stress on the protocol’s PCV. As a result, the DAO voted in favor of simplifying its PCV allocation towards the end of the quarter which increased FEI’s reliance on stablecoin backing.

We adjusted the Reserve Ratio (discussed last quarter) to include protocol-owned FEI on the assets and liabilities side, instead of just liabilities (suggested by Joey in this forum post). So RR = (PCV + Protocol-Owned FEI) / Total FEI Supply. This measure more accurately represents the DAO’s current risk/ability of minting new FEI against the PCV. Any minting of FEI pushes this ratio towards one, implying increased risk. Protocol-owned FEI could be stolen (like in the hack), swapped on a DEX, or borrowed in a loan and become user-circulating. While PCV would also increase on the other side of those transactions, there will be more volatility of the collateral ratio.

There are two limitations of this measure:

- It stops being useful once the ratio breaches 1, as minting new FEI would push it back towards 1.

- It does not take into account minted FEI that is sitting idly in TribeDAO wallets.

The former use of Collateral Ratio where CR = PCV / User-Circulating FEI will be kept. We believe this accurately represents the total borrowing capacity of the DAO.

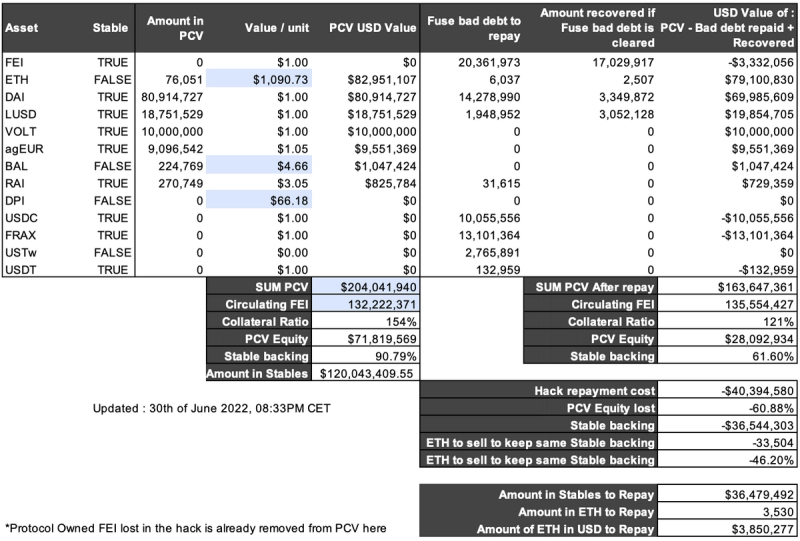

To execute the repayment, the Tribal Council has to allocate existing PCV assets or sell assets to buy back the stolen assets. The hack repayment burden, as of prices on June 30, 2022, is roughly $40 million. Only ~$4 million of this is in ETH, with the remainder in stablecoins. A detailed look at the hack repayment math looks like this:

Source: @Eswak (TribeDAO Community Member and Contributor), Messari. Link

At current prices (as of June 30, 2022), we update the collateral ratio and stable backing ratio assuming full repayment to hack victims. We also run a PCV scenario analysis based on varying ETH prices.

The Stable-Backing (SB) Ratio was suggested by the Core Team. This measure helps inform the market risk currently in the PCV relative to user-circulating FEI. With the recent PCV consolidation, the SB Ratio sits at 91%. This gives the PCV ample breathing room — down to sub-$200 ETH to back their stablecoin liabilities.

A situation where the DAO fully repays the hack greatly changes that picture. Assuming full repayment (stablecoins in FEI and ETH in ETH) and no PCV allocation changes, the PCV would be much more sensitive to changes in ETH. The SB Ratio would fall to 63%, and just below $700 ETH could put FEI at risk.

TRIBE

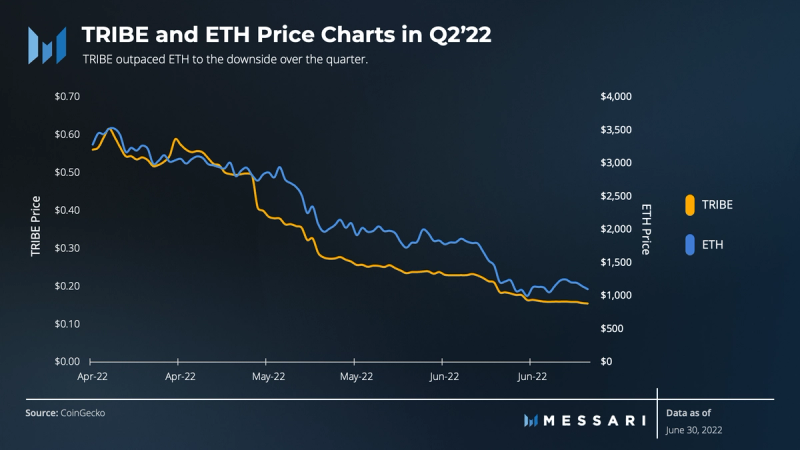

The governance and seigniorage token for the TribeDAO fell 72% in the quarter, while Ethereum fell 66%. The token currently sports a market cap of $124.8 million (as of June 30, 2022, assuming 832 million TRIBE circulating supply).

Equity value of the protocol can be measured by subtracting the user-circulating FEI (liabilities) from PCV (assets).

It is difficult to track the equity value per circulating TRIBE over time, as definitions of circulating supply can change. For example, the previous Liquidity Mining wallet holds about 30 million TRIBE. Previously, this would have been included as it was emitting TRIBE daily. Since those rewards have been shut off, the 30 million TRIBE in the Liquidity Mining wallet will be consolidated in the DAO Multisig and should no longer be considered circulating supply. Any TRIBE that was vesting to departed Rari core team members will also be consolidated.

Following these adjustments, we estimate there is roughly 832 million TRIBE in circulation. Over the next 3 years, there will be another 148 million TRIBE vesting to Fei Labs, investors, and individual contributors. The investor share is linear, while the contributor share is back-weighted.

Using 832 million as the circulating supply number, we calculate the TRIBE equity multiple by dividing the circulating market cap by protocol equity.

$125m / [ $204m – $132m ] = 1.74x

This metric helps us view the extrinsic value, or market’s growth expectations, of TRIBE. If the protocol were to liquidate today, TRIBE holders would take home roughly 57% of their current position. Therefore, the remaining 43% is based on expectations of future returns.

Lastly, the community ended last quarter with excitement around xTribe. The team is still working on the implementation here, but it is secondary to the defense of the PCV, hack repayment, Fuse fix, and other product priorities.

Qualitative Analysis

FEI Demand Drivers

Given the focus of the quarter on self-preservation, it is understandable that growth took a back seat. In less strenuous times, Fei Protocol is more focused on growing as a DAO-to-DAO (D2D) liquidity solution.

Turbo launched on April 20th but was not able to get off the ground given the Fuse hack and asset freeze. Turbo utilizes Rari Fuse Pools, so with that system frozen, Turbo had nowhere to go.

To review, Turbo helps DAOs productively use stagnant treasury assets while increasing liquidity for the protocol’s native token. It is a zero-interest stablecoin loan from TribeDAO. The borrower puts up collateral (typically native treasury assets, but we will broadly refer to these assets as TKN) and receives an equal amount of FEI. This FEI must be allocated to a lending pool and matched with an equal amount of TKN. The borrowing DAO and FEI will split fees and interest earned from this lending pool. The borrowing DAO now has a productive use for its treasury assets while providing liquidity for holders in the form of a lending pool with a stablecoin. In return, TribeDAO receives yield.

Will Turbo be a demand driver for FEI? It certainly could be, as TKN holders add TKN as collateral and take out FEI or vice versa. For example, the first Turbo partner was slated to be Balancer. Given veBAL rewards, it could be economically attractive to buy FEI, deposit as collateral and withdraw BAL. Then, users could participate in veBAL tokenomics and receive revenues that way. Although there are certainly more dynamics and risks to that trade than discussed here, it is very reasonable to expect this setup to drive demand for FEI.

The core team has hinted at other products like Flywheel. Building was underway, but the GitHub shows very little activity since April 25.

The community has stayed involved. There have been discussions led by @Sebventures and @Cozeno on embedding a sustainable interest rate in the protocol. On May 1, an off-chain vote actually passed to add a native interest rate to FEI. The proposal hasn’t gone into effect, given it was right after the Rari hack and followed shortly by the UST collapse. Assuming a Collateral Ratio greater than 1, the DAO can earn yield on its PCV and pass some on to FEI holders. This would increase adoption, further increasing the PCV, and so on.

PCV Yield Optimization

In a similar boat as FEI demand growth, it was a tough quarter to create new yield generating opportunities for FEI’s PCV.

Historically, the DAO’s primary usage of PCV has been to borrow against it to mint FEI and deposit it into Fuse pools. A similar strategy is used on DEXs for FEI/wETH or other pairs. The main issue with these tactics returns to demand for FEI, for which the drivers are not very strong.

The DAO has been quite open to new use cases for diversifying PCV and generating a return.

Certainly, staking ETH as stETH is a big one, given its principal protection and yield offerings. A perhaps unknown risk was the liquidity-premium risk being taken, as the market has repriced the liquidity premium in ETH-stETH pools. In fact, if a protocol isn’t hamstrung by liquidity needs, it might actually be a great time to add stETH because of the discount offered. Although stable backing is at 91%, it is likely beyond the current risk/liquidity profile of the Tribe.

The DAO has a PSM that uses LUSD to maintain the peg. Therefore, they need to hold LUSD in the PCV. As a result, the DAO could easily participate in Liquity liquidation pools for additional yield, while stacking LUSD stablecoins. Liquity is a borrowing platform like MakerDAO but with a smaller initial collateral ratio requirement and faster liquidations. As part of the PCV consolidation, this participation has been unwound.

Treasury swaps were also a big tool for PCV diversification and investment. With the introduction of veBAL, Fei has used its metagovernance and BAL lock tokens and has directed rewards to the FEI/wETH pool. This should both provide yield in the form of revenues that veBAL holders earn as well as rewards for FEI/wETH liquidity providers (LPs). Further, because this increases the yield for LPs, it could increase demand for FEI. Current APRs in this pool are over 30%. As part of the PCV consolidation, Fei’s allocation to the pool has been unwound.

Prior to the PCV consolidation at the end of this quarter, the DAO used its partnerships with other protocols to generate yield. Two examples:

- The DAO held LUSD as a PCV asset, needed to fund its PSM. Therefore, the DAO could also participate in Liquity liquidation pools for additional yield. Liquity is a borrowing platform like MakerDAO but with a smaller initial collateral ratio requirement and more frequent liquidations.

- As part of its partnership with Balancer, TribeDAO received 200k BAL in a treasury swap. Pairing this with ETH, TribeDAO could participate in veBAL rewards. Using its voting power, the DAO was able to create 30% APRs for the FEI/wETH liquidity pool on Balancer.

Governance

Last quarter, TribeDAO voted to change their governance structure to Liquid Representative Democracy. As a refresher, the DAO elects nine Council members who manage the Optimistic Timelock 5-of-9 multisig. The Tribal Council can effect almost any change through the Timelock — a smart contract that executes predetermined actions after a certain time period. The Timelock action can be vetoed by an on-chain governance vote by the NopeDAO, which is made up of all TRIBE holders. This check gives TRIBE holders oversight powers over the Tribal Council.

This structure was put to the test immediately with the Fuse hack repayment. Although the press has been critical, the structure seems to be operating exactly as designed. On May 15, the DAO voted off-chain to repay hack victims. The complication is now in the implementation – which PCV assets to sell or use as payment. The first attempt at this was vetoed by the NopeDAO.

The hot-take reaction is that the DAO is reneging on a commitment to pay back victims. The truth is that the DAO exercised its power to veto the current implementation of the repayment. There are many proposals still coming, and a lot of potential good to come from this.

0xMaki (of Sushi, Aura, LayerZero, and more) also voted to veto the proposal. Maki suggests alternative paths to repaying the debt that don’t rip away so much PCV. One suggestion is to issue a new token that is sent to hack victims and use PCV yield to buy back the token supply. Another is to give back some of the lost funds and offer a contract to redeem the rest when a certain KPI is met, such as the PCV resetting to a higher level (though Maki might mean relative to circulating FEI, i.e., when the Collateral Ratio gets to a certain level). Maki added a day later that he is building a coalition with other DAOs and whales who lost funds.

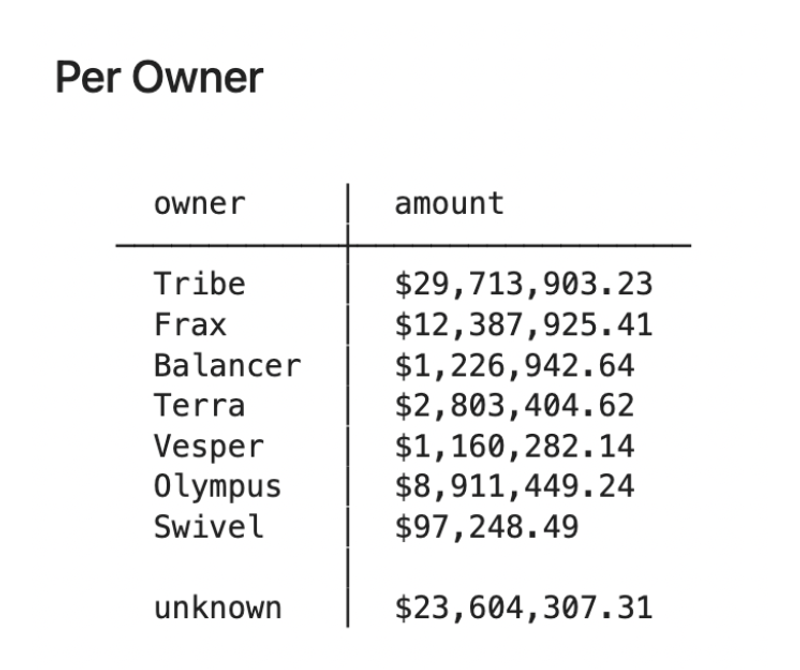

Another interesting proposal was shared before the above coalition info. It proposes paying back the smaller wallets first and then dealing with the DAOs, which make up over 50% of the non-Tribe original value lost. Considering how many of the affected parties are partners, this seems like a reasonable idea as well.

Source: @Storm (Link)

It is most likely that the DAO prioritizes small borrowers, which make up the majority of hack victims by number but the minority by USD value lost. This way, TribeDAO can help the most people while still protecting the PCV. For DAOs and whales, a secondary solution can be worked out over time. All options are on the table, but it will take a strong consensus (that does not get vetoed by 10 million TRIBE) to get anything passed.

In sum, the governance process is functioning appropriately. Because this is a difficult and important decision for the DAO, it will be hotly debated and will take some time to get to the right answer.

Fei-Frax Alliance

On May 18th, Joey pitched the Frax x Fei Stablecoin Alliance. In brief, FEI would replace UST in the Curve 4pool and a new FEI-FRAX-DAI 3pool would be created on Balancer. Frax, one of the largest veCRV holders, would direct rewards to the 4pool, and Fei would direct veBAL rewards to the 3pool. Initial traction on both sides was strong.

The hack repayment has put a spanner in the works. Frax lost roughly $13 million in the hack. As discussions about how to pay back victims are still ongoing, Frax is holding off on any agreements. Frax community members have offered to commit the funds repaid to a protocol-owned Curve pool. This would effectively create a FEI-FRAX PSM, helping the FEI peg.

The positive outcome could be quite helpful for Fei for PCV protection as well as stablecoin demand perspective. Depending on the state of the PCV and the community view on repayment methods, it could also be dangerous.

Other Notable Events

April 1, 2022 – Rari White-Hate Security Upgrade

April 26, 2022 – Lock 100% of PCV BAL in veBAL for 1 year and Direct Rewards to the FEI/wETH Pool

April 27, 2022 – Adding VOLT to the Tribe

May 14, 2022 – Rari Hack Post-Mortem

May 15, 2022 – Fei Savings Rate for VOLT

May 22, 2022 – Reinforce the PCV

June 10, 2022 – End TRIBE Incentives

June 11, 2022 – Jai Departs

June 13, 2022 – End Departed Rari Founders Vesting of TRIBE

June 19, 2022 – Increase FEI Stable Backing to 90–100%

June 27, 2022 – Collateralization and Operations Update

Closing Summary

Like much of crypto, it was a tough quarter for Fei Protocol and the TribeDAO. By way of difficult decisions, they have positioned themselves to survive the bear market. FEI is well-backed by stable PCV. The governance structure might have saved the DAO, as it preserved PCV and re-focused the community to find a new solution. That said, the structure also produces risks to the process in the future. Products and growth are frozen until some of the clouds clear. For FEI, survival is the name of the game right now.

—–

Looking to dive deeper? Subscribe to Messari Pro. Messari Pro memberships provide access to daily crypto news and insights, exclusive long-form daily research, advanced screener, charting & watchlist features, and access to curated sets of charts and metrics. Learn more at messari.io/pro

This report was commissioned by Tribe Grants, a member of Protocol Services. All content was produced independently by the author(s) and does not necessarily reflect the opinions of Messari, Inc. or the organization that requested the report. Paid membership in Protocol Services does not influence editorial decision or content. Author(s) may hold cryptocurrencies named in this report.

Crypto projects can commission independent research through Protocol Services. For more details or to join the program, contact ps@messari.io.

This report is meant for informational purposes only. It is not meant to serve as investment advice. You should conduct your own research, and consult an independent financial, tax, or legal advisor before making any investment decisions. Past performance of any asset is not indicative of future results. Please see our terms of use for more information.