Let’s imagine a nuclear power plant that integrates bitcoin mining on site. How does its profitability compare to a standard operation’s?

Welcome to part two of this series on Bitcoin and nuclear energy. Let us recap what we went through in part one before we dive deeper into the topics we’ll cover in part two.

Key Takeaways From “Why Bitcoin Is The Future Of Our Energy Grid”

- Bitcoin has great utility and is important for humans. Not everyone may use or appreciate its utility today, which is fine, but that does not mean it holds no utility to others. Currently, close to $400 billion of the world’s wealth is stored in it, that’s a lot of monetary energy to disregard.

- Bitcoin uses only about 0.1% of global energy. Current energy usage is between 100 to 200 terawatt hours (TWh) per year and per the projections shared in part one, Bitcoin’s energy usage will always be a rounding error with regards to global energy consumption. It would most likely be sub-1% for a long time to come.

- Bitcoin, in fact, may use too little energy for the value it may store in the future. Considering that Bitcoin likely grows over this coming decade and could store $20 trillion of world’s wealth, maybe even $50 trillion or $100 trillion, that’s a lot of monetary energy to be secured safely and protected. We should invest and use more energy to protect the network than we do currently.

- Bitcoin miners are highly mobile, look for the cheapest and lowest cost energy to mine and do not compete with other industries or your personal use for energy.

- Energy usage is a good thing. You want to live in a place where there is a good amount of energy available to use and enjoy, rather than too little. We need to use and harness more energy to become a Kardashev Type-I civilization which will take decades.

Nuclear plants have always fascinated people over the years but very few average people to date actually understand the economics behind constructing a nuclear power plant at scale. Today we deconstruct this very topic and in a fun and innovative way.

As the industry saying goes, “There are only two things that matter in construction of a nuclear power plant — capital cost and the costs of capital”

A Tale That Begins In 2009

All good tales need to start from the very beginning. Why should we do it any differently? So here we go.

The year is 2009. There are two nuclear reactor technology companies in the market competing to bring their technology online, deploy reactors and sell electricity. We’ll call these companies Alpha Labs and Beta Labs.

Both companies are currently in their R&D phases and going through their conceptual design for the reactor deployment. The next six or so years would be grueling. Both of these companies will go through extensive R&D, engineering decision making processes, supplier and vendor selections, component testing, hardware testing, conceptual design reviews and iterations and a thorough licensing review by the Nuclear Regulatory Commission (NRC) before they get a construction permit for building a nuclear reactor site. This period will be filled with challenges, both technological and otherwise. Like working on any deep technology, there are always things that need detailed design and engineering to be worked through and iterated upon before you’re ready to bring that technology to reality. The nuclear sector is no different.

However, another thing happened around 2009: the invention or discovery of Bitcoin. In the initial years no one took any notice, at least not in the nuclear industry, since they were pretty occupied in their technology work and Bitcoin was only heard about or really found in the weeds of the internet. And who was really busy searching for that in those days? But this changed. In 2012, one engineer working at Alpha Labs discovered Bitcoin by chance, going through a Reddit blog post. This engineer was intrigued and started looking into it more. Being from an engineering background with deep experience in energy markets, he started thinking about bitcoin as a commodity with a production cost associated with it like any other commodity. He discovered proof-of-work mining. This led him down a rabbit hole which changed the very nature of Alpha Labs’ history and, more importantly, the future of nuclear energy, power markets, the energy grid and humanity forever. This is the story of that one engineer.

The engineer started with mining bitcoin at his home in the beginning. He figured there was no better way of learning about mining than to do it himself and be in the trenches. The year was now 2013 and he had been mining for a good six months and had developed deep thinking about mining. He soon realized the repercussions of this innovation, how mining could be used to monetize energy that could otherwise never be monetized. Bitcoin mining offers a buyer of first resort for any energy that is low cost — wasted, stranded, curtailed, surplus or underutilized. The engineer realized this. He was way way ahead of his time, the world would not figure out the profoundness of this innovation until about 2030.

The engineer, having realized this in 2013, started pitching the idea of a co-location bitcoin mining site on the nuclear island that Alpha Labs was designing for its first site. He received severe pushback in the beginning since no one was aware of Bitcoin, much less of bitcoin mining. But he was persistent and did not give up.

Bitcoin had also started to get into the mainstream news because of a price surge, then a subsequent crash due to the Mt. Gox debacle, and more people were at least becoming aware of it. He started giving talks and presentations to the executive team and orange pilled a few of them. After six months of thorough design and engineering work in early 2014, Alpha Labs announced its plan to co-locate a bitcoin mining center on its nuclear island site, which was supposed to begin construction in 2016.

The engineer got switched to a newly-created bitcoin mining division inside the company and started leading that group. Over the next year, the team worked through the details of the build out and integrated the mining center co-location design into its nuclear island design. Alpha Labs went with a highly-mobile construction design for its mining center, so that in case it had to move or shift the mining center elsewhere it would be relatively easy to do, plus this limited its risk of owning an asset which cannot be moved if the circumstances demanded it. It realized the footprint that the mining center took as part of the nuclear island itself was not substantial and did not have a huge impact (increase) to the size of land it would need to get to build the site.

Alpha Labs received the permit approval for construction of Alpha-1, its flagship nuclear plant with the bitcoin mining co-location in the second half of 2016. It was now ready for construction.

All this was happening while Beta Labs was itself busy developing its own technology for the nuclear reactor and making amazing progress. It had gone through the design process, completed its entire hardware and component testing by 2014 and had itself been keeping engagements with the NRC around the licensing piece as early as 2012. Beta Labs went with a traditional nuclear plant with no bitcoin mining co-location, since it was not sold on the idea of this innovation by anyone particular, even though it had heard about the announcement of Alpha Labs in the early part of 2014.

It had held some preliminary discussions to understand Alpha Labs’ decision making but decided against pursuing a similar strategy, partly due to the fact that there were no resources out in the public markets to guide it around the use case for bitcoin mining colocation with its reactor build out. Beta Labs itself received its permit approval for construction in the second half of 2016 and was ready for its own build out.

Both Alpha Labs and Beta Labs were pursuing a nuclear plant construction of 1 gigawatt electrical (GWe) (or 2.5 gigawatt thermal (GWth), with 40% efficiency) capacity from the very early days. In 2014, Alpha Labs shifted track and announced a 2 GWe (or 5 GWth, 40% efficiency) reactor deployment and construction plan, with 1GWe to be used for selling electricity to the grid while the balance of 1GWe was to be used solely for mining bitcoin onsite.

So, to recap, here is the construction plan for both companies:

Alpha Labs: 2 GWe cap., 1 GWe sell to grid wholesale, 1 GWe to mine bitcoin onsite

Beta Labs: 1 GWe cap., 1 GWe to sell to grid wholesale

Economics Of Nuclear Power Plants

We’re in the second half of 2016 now. Both Alpha and Beta Labs have announced their nuclear power plants (NPPs) constructions and are actively looking to raise capital.

NPP financing can take many different, exotic forms and arrangements. The structure of financing for NPPs is not part of the scope for this article. Here we would assume that both Alpha Labs and Beta Labs get funding on equal terms for their construction plants, so as to do an “apples-to-apples” projection of their capital costs, revenue and profits/losses.

Assumptions

- Let us assume that NPP construction for both companies will take six years to complete. So, from 2016 to 2022. This is in line with construction times of most NPPs to date.

- Let us assume that the capital costs for NPP construction for both companies are $5,000 per kilowatt (kW). This ballpark estimate is in line with the construction costs of NPPs to date.

Based on this number, here are the capital requirements for both companies:

Alpha Labs: $5,000 * 2 Gw/Kw = $10 billion

Beta Labs: $5,000 * 1 Gw/Kw = $5 billion

Now, keep in mind that Alpha Labs would also require capital to buy miners and deploy them onsite at its co-located mining center. But this would only be required when it is ready to produce electricity, which would not happen until 2022. So, it decides to get a higher limit of capital line which they can draw upon when needed six years down the line. At this point in 2016, bitcoin ASICs were going mainstream, new and more efficient machines were expected to come to market over the coming years, which Alpha Labs was keeping a track of. It was still quite a few years away from placing orders for miners, that would consume 1 GWe of nuclear generation, so the only thing to do right then was to track the mining industry and see it evolve.

Here are the funding terms received by both companies:

Alpha Labs: $10 billion at 3% interest, with a debt service period of 25 years. The capital line would be extended up to $15 billion at the same terms if needed in the future. Alpha Labs would draw $2 billion in each year for the first five years of NPP construction.

Beta Labs: $5 billion at 3% interest, with a debt service period of 25 years. Beta Labs would draw $1 billion in each year for the first five years of NPP construction.

Now, based on the terms, Beta Labs would need to pay about $57 million every year for the next 25 years for every $1 billion it drew from its capital line during the first five years of construction.

And, on similar lines, Alpha Labs would need to pay about $114 million every year for the next 25 years for every $2 billion it drew from its capital line during the first five years of construction.

Now, we’ll use blocks of capital to represent the economics of both Alpha Labs and Beta Labs over the next many years so as to compare what their debts and profits would look like.

Let us assume about $57 million is one block. We’ll represent this as a green block on the graph going forward.

So, it’s mid-2016 and both NPP constructions are about to begin.

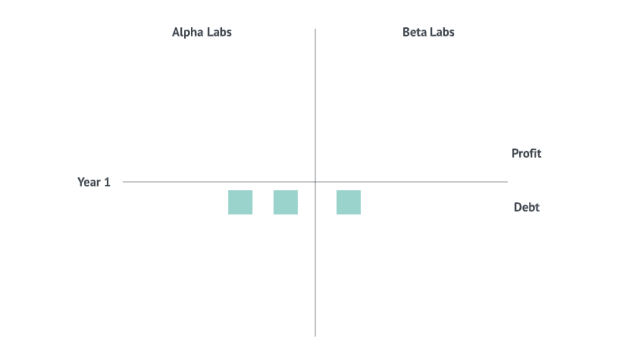

Year One: 2016

Beta Labs: Takes out its first $1 billion in capital to begin construction. Based on this, it would need to pay one block of debt, which is added to its balance sheet below.

Total capital drawn: $1 billion

Total debt: One block

Alpha Labs: Takes out its first $2 billion in capital to begin construction. Based on this, it would need to pay two blocks of debt, which is added to its balance sheet below.

Total capital drawn: $2 billion

Total debt: Two blocks

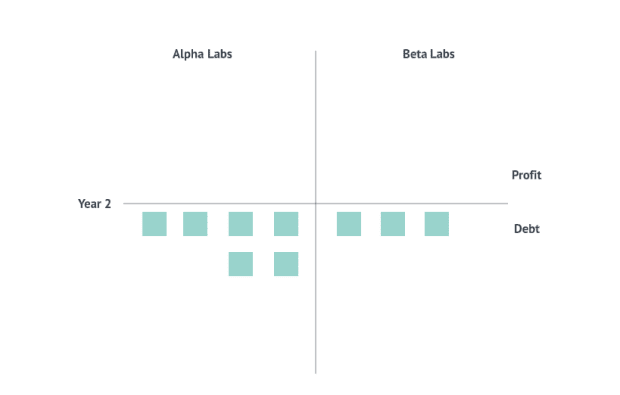

Year Two: 2017

Beta Labs: Takes out another $1 billion in capital. Based on this, it would need to pay two additional blocks of debt in year two, which is added to its balance sheet below.

Total capital drawn: $2 billion

Total debt: Three blocks

Alpha Labs: Takes out another $2 billion in capital. Based on this, it would need to pay four additional blocks of debt in year two which is added to its balance sheet below.

Total capital drawn: $ 4 billion

Total debt: Six blocks

Year Three: 2018

Beta Labs: Takes out another $1 billion in capital. Based on this, it would need to pay three additional blocks of debt in year three, which is added to its balance sheet below.

Total capital drawn: $3 billion

Total debt: Six blocks

Alpha Labs: Takes out another $2 billion in capital. Based on this, it would need to pay six additional blocks of debt in year three which is added to its balance sheet below.

Total capital drawn: $6 billion

Total debt: 12 blocks

Year Four: 2019

Beta Labs: Takes out another $1 billion in capital. Based on this they would need to pay four additional blocks of debt in year four, which is added to its balance sheet below.

Total capital drawn: $4 billion

Total debt: 10 blocks

Alpha Labs: Takes out another $2 billion in capital. Based on this, it would need to pay eight additional blocks of debt in year four which is added to their balance sheet below.

Total capital drawn: $8 billion

Total debt: 20 blocks

Year Five: 2020

Beta Labs: Takes out another $1 billion in capital. Based on this, it would need to pay five additional blocks of debt in year five which is added to their balance sheet below.

Total capital drawn: $5 billion

Total debt: 15 blocks

Alpha Labs: Takes out another $2 billion in capital. Based on this, it would need to pay 10 additional blocks of debt in year five which is added to its balance sheet below.

Total capital drawn: $10 billion

Total debt: 30 blocks

Year Six: 2021

Beta Labs: No additional capital. So, it would need to continue paying five additional blocks of debt in year six which is added to its balance sheet below.

Total capital drawn: $5 billion

Total debt: 20 blocks

Alpha Labs: No additional capital. So, it would need to continue paying 10 additional blocks of debt in year six which is added to its balance sheet below.

Total capital drawn: $10 billion

Total debt: 40 blocks

Year Seven: 2022

This is where things get interesting now. Both Alpha Labs and Beta Labs have completed their NPP constructions and are now ready to produce electricity. At this point, both companies’ balance sheets have nothing but a massive compilation of debt obligations based on the amount of capital they have taken out for their respective constructions.

Assumptions

- Let us assume that the all in revenue from selling 1 GWe electricity per year in the wholesale power markets is about $525 million with a clearing price of 6 cents per kWh. This means, based on our block model, that both Alpha Labs and Beta Labs would make about nine blocks of revenue each year going forward from selling electricity. We would assume that both companies will run their NPPs at full power or capacity factor of 100%.

- Let us assume that the operating cost of running the NPP per year is about $100 million per GWe. This includes the yearly fuel cost and variable operations and maintenance. This means, based on our block model, that both Beta Labs would spend about blocks in covering operating expenses every year going forward while Alpha Labs would spend about four blocks in covering operating expenses every year going forward.

Assumptions And Estimates For Bitcoin Mining

- Mining numbers and profitability analysis was done on June 18, 2022 for this article, when the bitcoin price was about $20,000, network difficulty was 30 T and the network hash rate (30 days) was 215 exahashes per second (EH/s). The mining revenue projections take into account the halving in 2024 and take an assumption that both bitcoin price and difficulty would increase 50% on average every year for the next five years.

- Let us assume that Alpha Labs is able to secure latest-generation ASIC miners at the cost of about $10,000 each for their 1GWe mining colocation center. Based on the average power draw from a single miner, Alpha Labs would need around 300,000 miners. The total capital cost for this side of the operation would be about $3 billion which it would draw from its existing capital line at the same terms as before. This means that they would need to pay an additional debt of about $172 million (or the equivalent of three blocks) every year going forward for this new capital draw.

- Let us assume that the mining hardware would have a life of five years.

- Let us assume that Alpha Labs keeps no bitcoin on its balance sheet from this exercise and therefore converts all mining revenue into USD.

- Let us run some mining profitability numbers using Braiins OS to get a projection of how much revenue Alpha Labs would make over the next five years of mining with this mining equipment:

- Here are the mining revenue results that Alpha Labs would make each year:

- Year seven: $1.5 billion or about 27 blocks

- Year eight: $1.6 billion or about 29 blocks

- Year nine: $970 mil or about 17 blocks

- Year 10: $1.1 billion or about 19 blocks

- Year 11: $1.25 billion or about 22 blocks

Now, let us continue with our block analysis of both companies’ balance sheet.

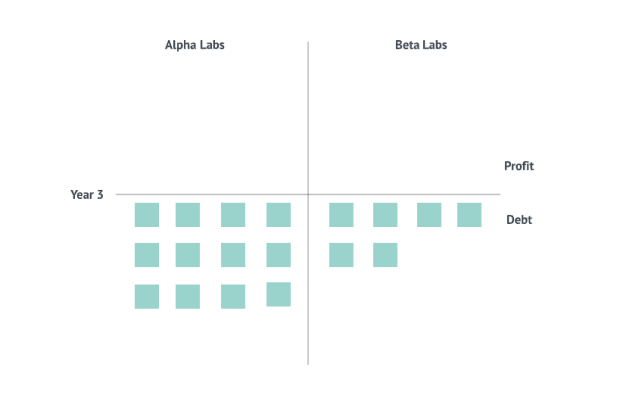

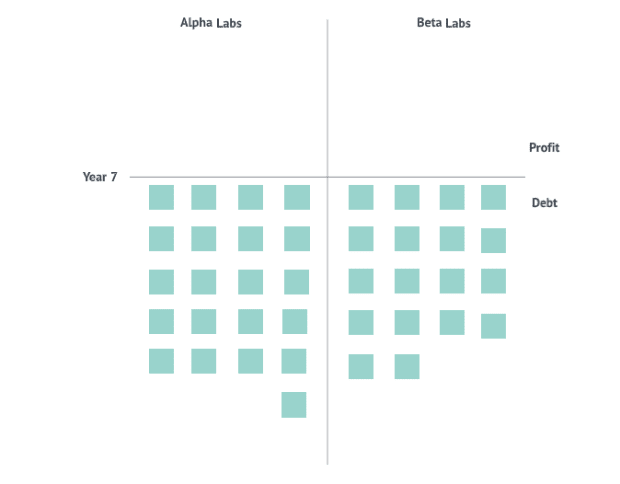

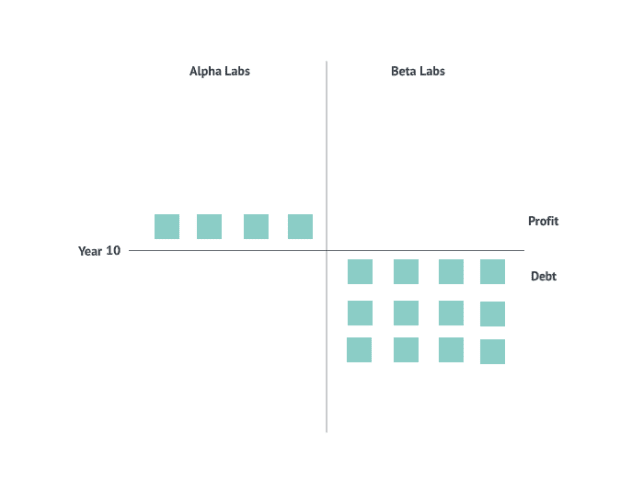

Beta Labs: 20 blocks in debt already, five additional blocks in debt for year seven, two blocks in operating expenses, nine blocks in 1GWe to grid revenue

Yearly profit and loss = 9 blocks – (5 blocks + 2 blocks) = 2 blocks

Total debt = 20 blocks – 2 blocks = 18 blocks

Alpha Labs: 40 blocks in debt already, 10 additional blocks in existing debt for year seven, three additional blocks in miner debt taken for year seven, four blocks in operating expenses, nine blocks in 1 GWe to grid revenue, 27 blocks in 1 GWe mining revenue

Yearly profit and loss = (9 blocks + 27 blocks) – (10 blocks + 3 blocks + 4 blocks) = 19 blocks

Total debt = 40 blocks – 19 blocks = 21 blocks

As you can now see, Alpha Labs is moving up from the trenches of debt collection much quicker than Beta Labs, which would take a long time to turn profitable.

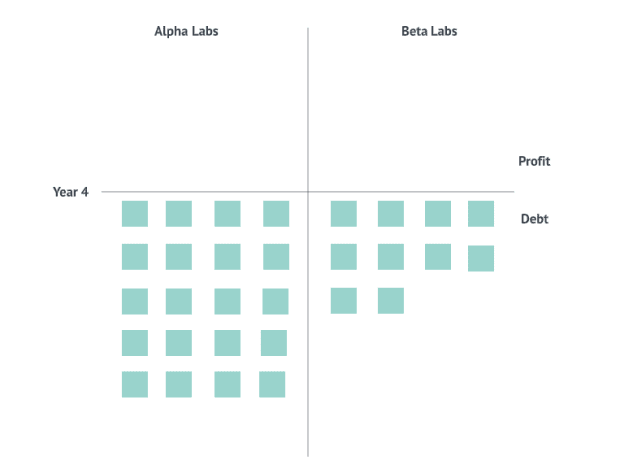

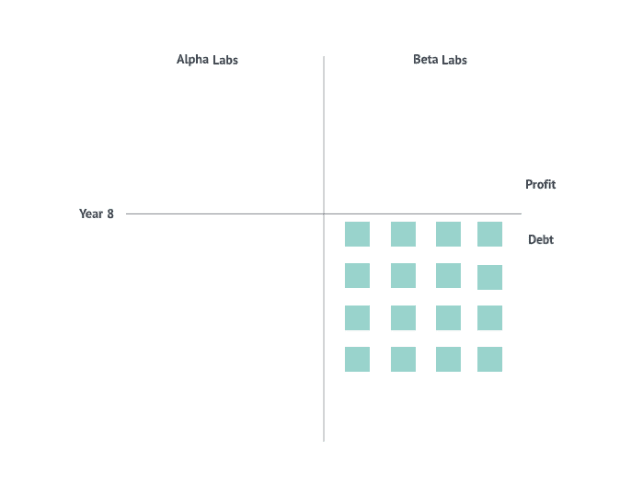

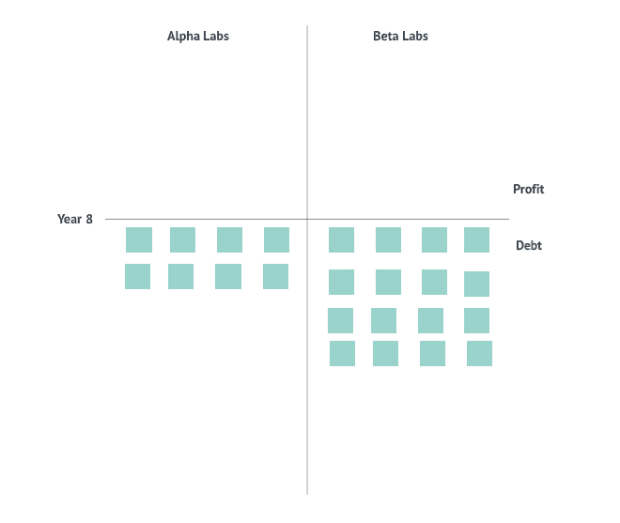

Year Eight: 2023

Beta Labs: 18 blocks in debt already, five additional blocks in debt for year eight, two blocks in operating expenses, nine blocks in 1 GWe to grid revenue

Yearly profits and losses = 9 blocks – (5 blocks + 2 blocks) = 2 blocks

Total debt = 18 blocks – 2 blocks = 16 blocks

Alpha Labs: 21 blocks in debt already, 10 additional blocks in existing debt for year eight, three additional blocks in miner debt taken for year eight, four blocks in operating expenses, nine blocks in 1 GWe to grid revenue, 29 blocks in 1 GWe mining revenue

Yearly profits and losses = (9 blocks + 29 blocks) – (10 blocks + 3 blocks + 4 blocks) = 21 blocks

Total debt = 21 blocks – 21 blocks = 0 blocks

Alpha Labs has broken even in year eight in just its second year of NPP operation while Beta Labs still has 16 blocks in debt remaining on their balance sheet. The difference on the balance sheets between the companies has suddenly become astonishingly wide. Alpha Labs has been able to wipe off 40 blocks of debt over just two years of operation.

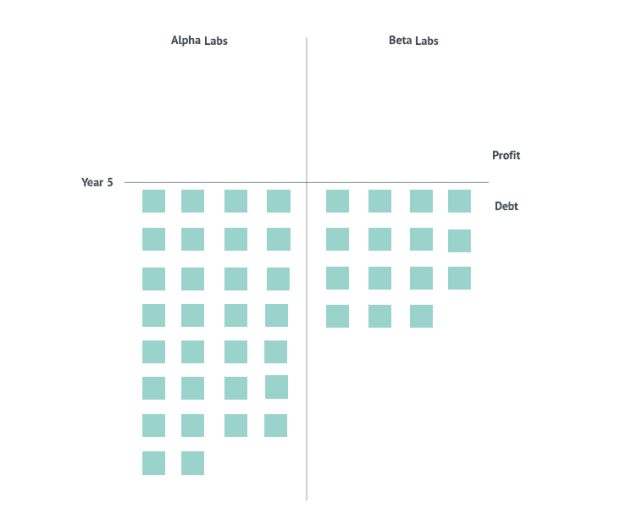

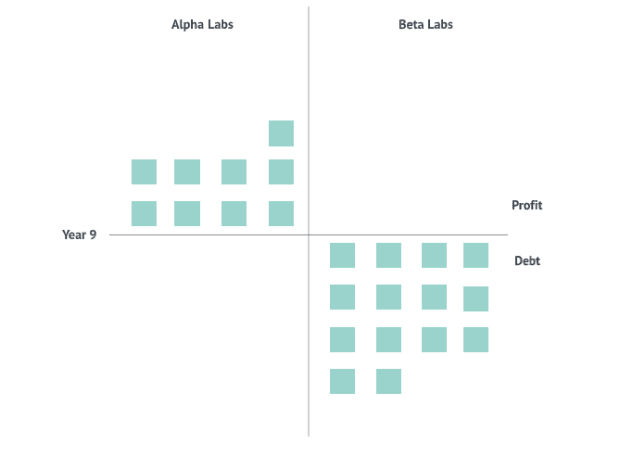

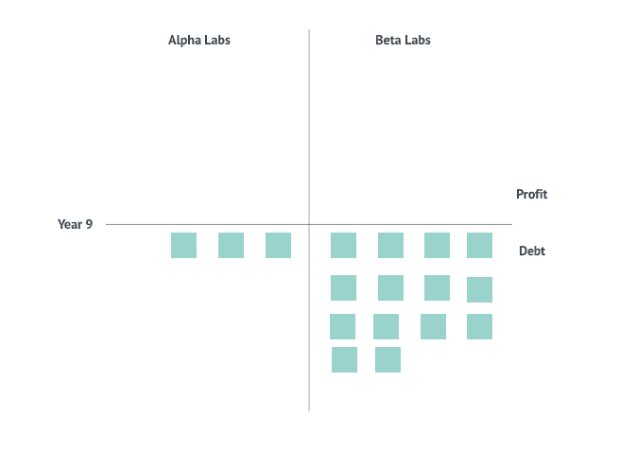

Year Nine: 2024

Beta Labs: 16 blocks in debt already, five additional blocks in debt for year nine, two blocks in operating expenses, nine blocks in 1GWe to grid revenue

Yearly profits and losses = 9 blocks – (5 blocks + 2 blocks) = 2 blocks

Total debt = 16 blocks – 2 blocks = 14 blocks

Alpha Labs: Zero blocks in debt already, 10 additional blocks in existing debt for year nine, three additional blocks in miner debt taken for year nine, four blocks in operating expenses, nine blocks in 1 GWe to grid revenue, 17 blocks in 1 GWe mining revenue

Yearly profits and losses = (9 blocks + 17 blocks) – (10 blocks + 3 blocks + 4 blocks) = 9 blocks

Total Profit = 9 blocks – 0 blocks = 9 blocks

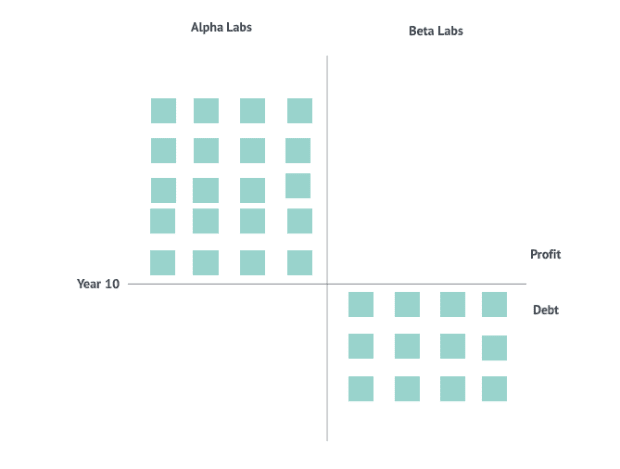

Year 10: 2025

Beta Labs: 14 blocks in debt already, five additional blocks in debt for year 10, two blocks in operating expenses, nine blocks in 1 GWe to grid revenue

Yearly profits and losses = 9 blocks – (5 blocks + 2 blocks) = 2 blocks

Total debt = 14 blocks – 2 blocks = 12 blocks

Alpha Labs: Nine blocks in profit already, 10 additional blocks in existing debt for year 10, three additional blocks in miner debt taken for year 10, four blocks in operating expenses, nine blocks in 1 GWe to grid revenue, 19 blocks in 1 GWe mining revenue

Yearly profits and losses = (9 blocks + 19 blocks) – (10 blocks + 3 blocks + 4 blocks) = 11 blocks

Total Profit = 9 blocks + 11 blocks = 20 blocks

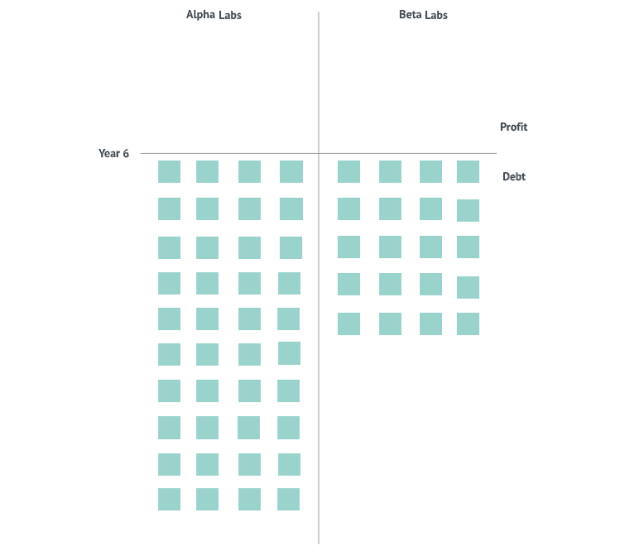

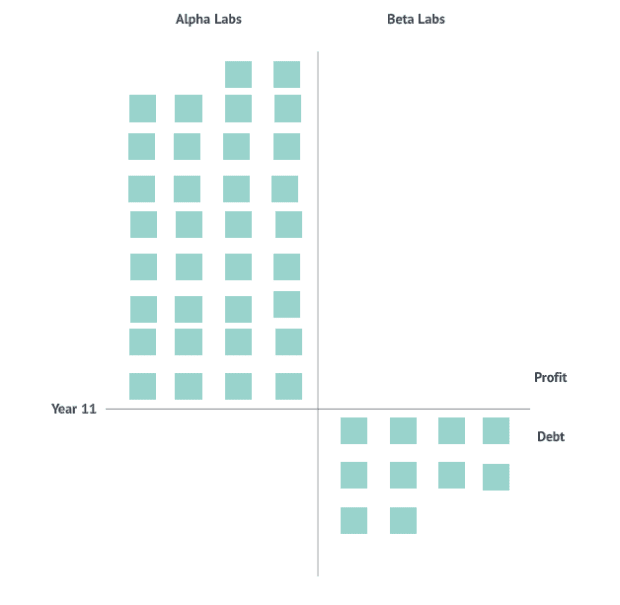

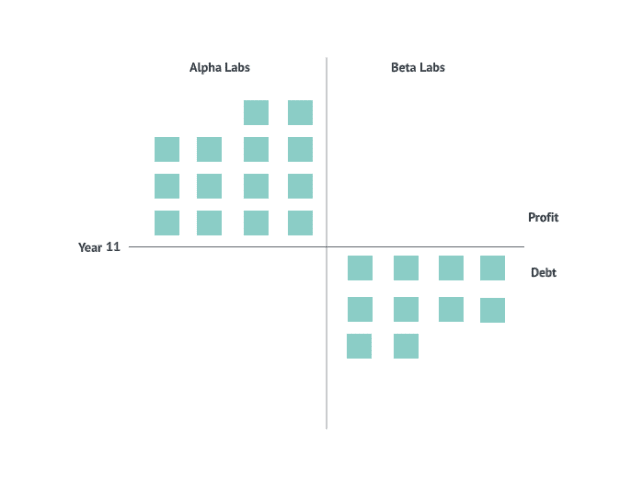

Year 11: 2026

Beta Labs: 12 blocks in debt already, five additional blocks in debt for year 11, two blocks in operating expenses, nine blocks in 1 GWe to grid revenue

Yearly profits and losses = 9 blocks – (5 blocks + 2 blocks) = 2 blocks

Total debt = 12 blocks – 2 blocks = 10 blocks

Alpha Labs: 20 blocks in profit already, 10 additional blocks in existing debt for year 11, three additional blocks in miner debt taken for year 11, four blocks in operating expenses, nine blocks in 1 GWe to grid revenue, 22 blocks in 1GWe mining revenue

Yearly profits and losses = (9 blocks + 22 blocks) – (10 blocks + 3 blocks + 4 blocks) = 14 blocks

Total Profit = 20 blocks + 14 blocks = 34 blocks

As you can now see very clearly, it would take Beta Labs around 16 years to break even (around 2031) while Alpha Labs broke even in only its second year of operation (in 2023) and year eight from the start of NPP construction in 2016.

Co-location of a bitcoin mining center onsite was truly a game-changing decision for Alpha Labs, thanks to that one visionary engineer who has now been promoted to the executive team. Well deserved indeed.

As we get to see from this case study, co-location of bitcoin mining onsite at the NPP improves both the project revenue and pay back period, which makes the investment capital more attractive. Could bitcoin mining actually help push nuclear power into the mainstream again? Something to think about.

Near-Free Electricity: A Thought Experiment

Now, how about we do a little thought experiment and see if Alpha Labs can sell its 1 GWe electricity to the grid at half the price it was selling in the case study before. How would its balance sheet look in this case?

Until year six, there would be no difference, as NPPs are just finishing construction, so we’ll pick up from year seven onwards. Here’s how both companies’ balance sheets look like at the end of year six:

Year Seven: 2022

This is where things get really interesting again. Both Alpha Labs and Beta Labs have completed their NPP constructions and are now ready to produce electricity.

All of our assumptions from the previous case study remain valid for this thought experiment. The only difference is that Alpha Labs is monetizing 1 GWe of its electricity generation by mining bitcoin the exact same way while its 1 GWe portion which it was previously selling to the grid for about $525 million or nine blocks of revenue is now making them half, so about $267 million or five blocks of revenue. This would mean selling at a clearing price of 3 cents per kWh instead of 6 cents per kWh.

Beta Labs: 20 blocks in debt already, five additional blocks in debt for year seven, two blocks in operating expenses, nine blocks in 1 GWe to grid revenue

Yearly profits and losses = 9 blocks – (5 blocks + 2 blocks) = 2 blocks

Total debt = 20 blocks – 2 blocks = 18 blocks

Alpha Labs: 40 blocks in debt already, 10 additional blocks in existing debt for year seven, three additional blocks in miner debt taken for year seven, four blocks in operating expenses, five blocks in 1 GWe to grid revenue, 27 blocks in 1 GWe mining revenue

Yearly profits and losses = (27 blocks + 5 blocks) – (10 blocks + 3 blocks + 4 blocks) = 15 blocks

Total debt = 40 blocks – 15 blocks = 25 blocks

Year Eight: 2023

Beta Labs: 18 blocks in debt already, five additional blocks in debt for year eight, two blocks in operating expenses, nine blocks in 1 GWe to grid revenue

Yearly profits and losses = 9 blocks – (5 blocks + 2 blocks) = 2 blocks

Total debt = 18 blocks – 2 blocks = 16 blocks

Alpha Labs: 30 blocks in debt already, 10 additional blocks in existing debt for year eight, three additional blocks in miner debt taken for year eight, four blocks in operating expenses, five blocks in 1 GWe to grid revenue, 29 blocks in 1 GWe mining revenue

Yearly profits and losses = (29 blocks + 5 blocks) – (10 blocks + 3 blocks + 4 blocks) = 17 blocks

Total debt = 25 blocks – 17 blocks = 8 blocks

Year Nine: 2024

Beta Labs: 16 blocks in debt already, five additional blocks in debt for year nine, two blocks in operating expenses, nine blocks in 1 GWe to grid revenue

Yearly profits and losses = 9 blocks – (5 blocks + 2 blocks) = 2 blocks

Total debt = 16 blocks – 2 blocks = 14 blocks

Alpha Labs: 18 blocks in debt already, 10 additional blocks in existing debt for year nine, three additional blocks in miner debt taken for year nine, four blocks in operating expenses, five blocks in 1 GWe to grid revenue, 17 blocks in 1 GWe mining revenue

Yearly profits and losses = (17 blocks + 5 blocks) – (10 blocks + 3 blocks + 4 blocks) = 5 blocks

Total Debt = 8 blocks – 5 blocks = 3 blocks

Year 10: 2025

Beta Labs: 16 blocks in debt already, five additional blocks in debt for year nine, two blocks in operating expenses, nine blocks in 1 GWe to grid revenue

Yearly profits and losses = 9 blocks – (5 blocks + 2 blocks) = 2 blocks

Total debt = 14 blocks – 2 blocks = 12 blocks

Alpha Labs: 18 blocks in debt already, 10 additional blocks in existing debt for year nine, three additional blocks in miner debt taken for year nine, four blocks in operating expenses, five blocks in 1GWe to grid revenue, 19 blocks in 1 GWe mining revenue

Yearly profits and losses = (19 blocks + 5 blocks) – (10 blocks + 3 blocks + 4 blocks) = 7 blocks

Total profit = 7 blocks – 3 blocks = 4 blocks

Alpha Labs has broken even in year 10 in this case instead of year eight, or four years after beginning operation. Still quite amazing considering Beta Labs would not turn profit until year 16 and Alpha Labs is selling 1 GWe electricity at half price compared to them.

Year 11: 2026

Beta Labs: 16 blocks in debt already, five additional blocks in debt for year nine, two blocks in operating expenses, nine blocks in 1 GWe to grid revenue

Yearly profits and losses = 9 blocks – (5 blocks + 2 blocks) = 2 blocks

Total debt = 12 blocks – 2 blocks = 10 blocks

Alpha Labs: 18 blocks in debt already, 10 additional blocks in existing debt for year nine, three additional blocks in miner debt taken for year nine, four blocks in operating expenses, five blocks in 1 GWe to grid revenue, 22 blocks in 1GWe mining revenue

Yearly profits and losses = (22 blocks + 5 blocks) – (10 blocks + 3 blocks + 4 blocks) = 10 blocks

Total profit = 4 blocks + 10 blocks = 14 blocks

Co-location of a bitcoin mining center onsite was truly a game-changing decision for Alpha Labs and even if it sold their electricity at half price compared to Beta Labs, it is considerably more profitable compared to that operation at this stage.

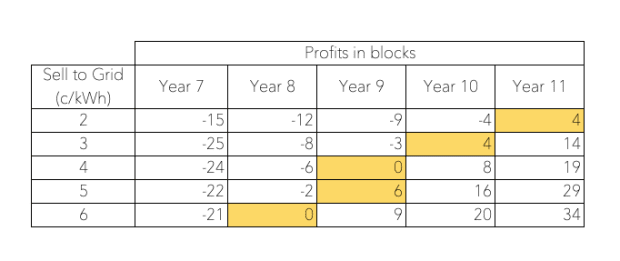

Here is a sensitivity analysis on the clearing price of electricity sold by Alpha Labs and its balance sheet based off of block increments:

As you can see from the table above, in all cases up to 2 cents per kWh, Alpha Labs would turn a profit by year 11 (all highlighted in yellow).

Having worked through the math on both Alpha and Beta Labs’ balance sheets, here are some important things to point out and keep in mind:

- Raising north of $10 billion at 3% interest with the terms outlined in this article for constructing NPPs with bitcoin mining co-location (two heavily misunderstood industries) is no easy task in today’s environment. NPP constructions are very sensitive to the capital cost and cost of capital and it is imperative to get the best terms to build NPPs with mining colocation for long-term profitability.

- NPP constructions can take a long time, around six years for full construction, assuming there are no delays caused due to multiple possible reasons, including public outcry and protests. Compared to this, a natural gas power plant can be up and running in about two years. NPPs are costly to construct and incredibly cheap to operate while the natural gas power plants are the other way around. Given how cyclical and evolving the mining industry is and how competitive it could become over time, it is difficult to project mining revenues six years down the line with any given certainty for raising capital and building capacity expansion upfront for mining onsite.

- Bitcoin mining is going to become incredibly cost competitive over time and revenues are going to shrink to the point where running large mining centers would only be possible behind the meter in some form. Nuclear provides the best case base load for building mining centers for 24/7 reliable energy and no tie in to the grid is required. Even if you are co-locating your mining center with solar or wind, you’ll need some tie in to the grid, since solar and wind are both intermittent sources of generation, unlike nuclear.

- NPP construction costs and timelines might both go down considerably with the advent of modular reactors and next generation reactor types which do not require design and materials of the past, which had led to cost and construction times both ballooning previously.

- The NPP and bitcoin mining model of electricity generation could be adopted by nation states at scale as a matter of energy and national security. These projects could receive state funding and subsidies/credits to make them even more attractive for investment capital.

The intention of this article was to provide a thorough case study on what bitcoin mining co-location with a nuclear power plant construction could look like and how much of a difference it could actually make to the balance sheet of the company owning that generation asset. As we see, you’d rather take the strategy of Alpha Labs than Beta Labs. All you need is one engineer in your company to understand this and pitch it to you.

References

- “The Economics Of Nuclear Energy,” Real Engineering

- “Economics Of Nuclear Reactor,” Illinois EnergyProf

Disclaimer: The information provided in this article is based upon our forecasts and reflects prevailing market conditions and our views as of this date, all of which are subject to change. The article contains forward-looking projections which involve risks and uncertainties. Any statements made in the article are based on the authors’ current knowledge and assumptions. Various factors could cause actual future results, performance or events to differ materially from those described in these statements.

This is a guest post by Puru Goyal and Tina Stoddard. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.