State of Balancer Q2 2022

July 13, 2022

Key Insights

- Despite battling early hiccups, veBAL is fully operational and paying out 75% of protocol revenues to veBAL lockers.

- Volumes and number of swaps increased by 22% and 43%, respectively. TVL fell 70%, in USD terms. Stablecoin liquidity also fell 70%.

- Balancer implemented major operational changes with the incorporation of a foundation and a new Operational Framework for Service Providers (SPs).

- With the new fee split, LPs receive 50% of the trading revenue, instead of 90%. The DAO receives 12.5% and veBAL lockers receive 37.5%.

A Primer on Balancer

Balancer is a DeFi automated market making protocol using novel self-balancing weighted pools. The protocol allows anyone to create a pool of assets with predefined weights in the pool. Balancer strives to be a platform for DAOs and other protocols to build tools that provide useful liquidity to their end users and products. The protocol is managed by the Balancer DAO community and currently supports Ethereum, Polygon, Arbitrum, and Optimism (managed by Beethoven X). Since launching V2 in August of 2021, Balancer’s product line has expanded to include:

- Weighted Pools: Fixed weight pools that allow liquidity providers to create a rebalancing index fund, decrease risk of impermanent loss, and take a directional view while providing liquidity.

- Stable Pools: Use different weighting math (stable math with an amplification factor, which balances constant sum and constant product math) to achieve deeper liquidity for price-similar assets (stablecoins, wBTC/renBTC/sBTC, etc). Stable Pools have tighter spreads and deeper liquidity for larger trades, benefiting from the vault introduced in V2.

- MetaStable Pools: A solution between Weighted and Stable Pools, MetaStable Pools are for correlated not pegged assets like yield bearing tokens against their native token DAI and cDAI or ETH and stETH.

- Liquidity Bootstrapping Pools (LBPs): Use weighted math with time-dependent weights, which allows for smoother token distribution releases. The pool can start with less capital (80% token / 20% stablecoin instead of needing to fund 50% stablecoin). The goal is to alleviate buy/sell pressure over fixed periods.

- Managed Pools: A feature-rich option that allows for up to 50 tokens. Some of the features include: Pool Manager(s), Management Fees (optional), Liquidity Provider Allowlists, Up to 50 Tokens, Active Token Management, Add, Remove, Change token weights, Circuit Breakers to protect from malicious/compromised tokens.

- Boosted Pools: Allows for tight stablecoin trading while using idle assets to loan on a lending platform. These pools offer increased capital efficiency for the liquidity provider and similar liquidity for the trader.

- Custom Pools: Use Balancer’s vault and pools infrastructure to create your own pricing equations.

Introduction

The launch of vote-escrow tokenomics has redefined the use and purpose of Balancer’s native token BAL. An estimated 32 of 64 Snapshot votes in Q2 2022 were to whitelist new pools as gauges. veBAL holders earned $14.6 million in new BAL tokens in reward emissions along with $5 million from revenue share. The new incentive system is not without risks due to the opportunity to direct inflationary rewards. As a result, new rules and tools were hotly debated this quarter to optimize the incentive alignment between veBAL voters and Balancer.

From a performance perspective, the protocol continued to operate without issues. The stated mission to be a DAO-to-DAO service provider was furthered with the integration of Boosted Pools on 1inch and the new Aura protocol built to support veBAL voting. Volumes and transactions were up, while TVL (in USD terms) fell over 70%.

The DAO added structure in a few forms. First, they adopted a Foundation to help broaden their reach off-chain. They also created an organizational framework that defines a process for service providers (SPs) to apply for funding.

The protocol expanded to Optimism by way of a partnership, working with partner Beethoven X. They also announced intentions to build and launch on Gnosis.

Performance Analysis

Liquidity Provider Perspective

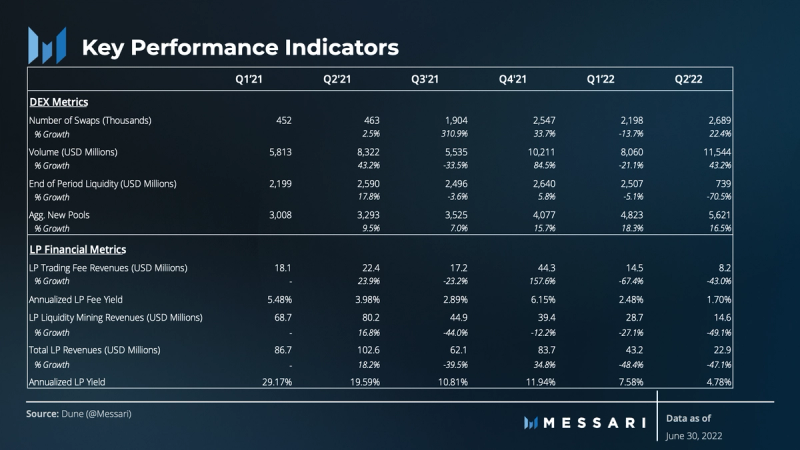

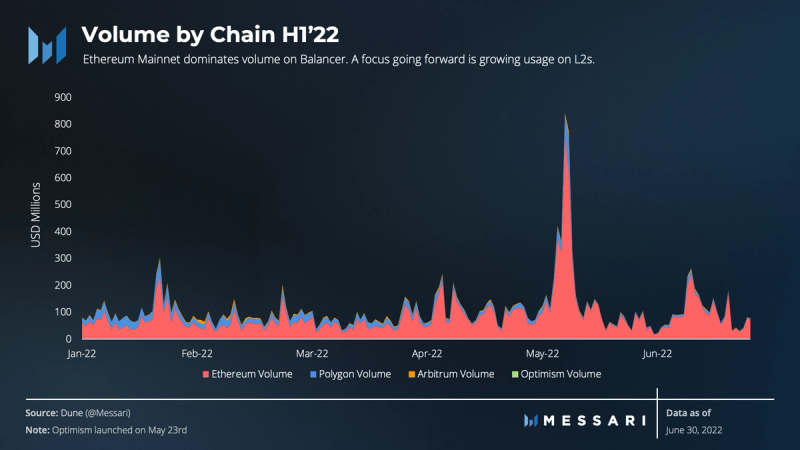

Volumes on Balancer were up 43%, growing from $8 billion in Q1 to $11.5 billion in Q2. 87% of volume was on Ethereum Mainnet. The UST collapse in May and pursuant contagion in June led to increased trade volumes. The 1inch integration also added a new source of demand for Balancer’s boosted stable pool.

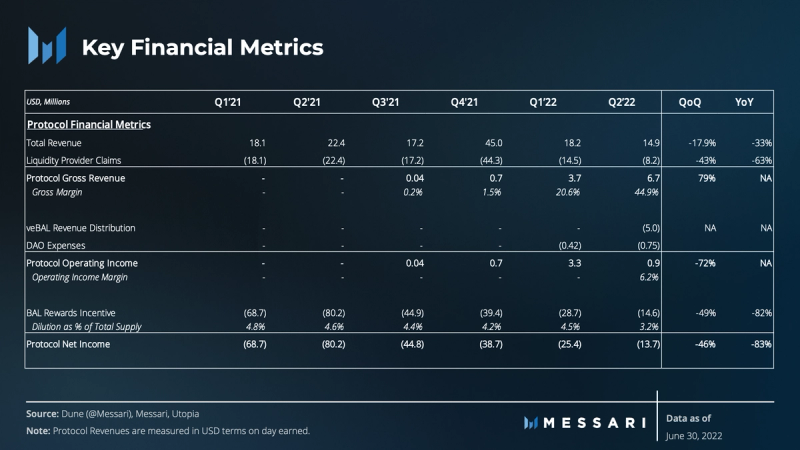

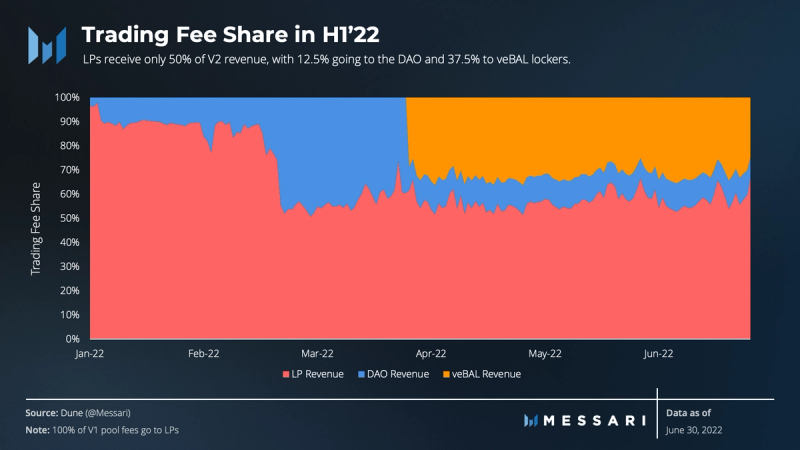

While volumes remained strong, revenue for LPs was down due to a change in the protocol tokenomics. With the expectation of veBAL, the DAO voted in February to change the fee revenue split between LPs and the protocol from 90:10 to 50:50. The new split contributed to LP revenue falling 43% to $8.3 million in the second quarter.

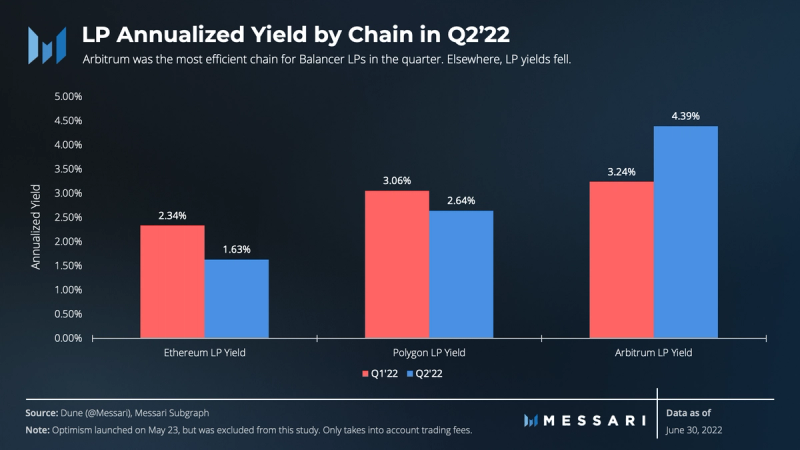

In terms of efficiency for LPs, Balancer’s Arbitrum instance offered the highest yield for LPs by chain on Balancer, excluding liquidity mining rewards. According to Arbiscan, volume increased 70% on Arbitrum this quarter, likely given expectations of a token airdrop coming soon.

Stable pools have much lower fee rates (0.04% or lower) than weighted pools (typically 0.1% to 1%) and LBPs. As a liquidity provider, there is an important risk-reward consideration when depositing in a stable pool. Stable pools have inherently much less impairment loss (IL) risk compared to a weighted pool. Despite a share of earnings going to LPs, stable pool yields were up this quarter as TVLs fell and volumes climbed.

LBPs yielded 41% this quarter versus 37% last quarter. They are a high-yield product for LPs, but they are not typically open to new LP deposits. LBPs are primarily used for token launches or for rebalancing, so only one DAO or holder can be the LP in a short (several days) window of high volume trading.

Trader Perspective

Bear markets and a tightening Federal Reserve can lead to harsh liquidity conditions for traders. Balancer’s veBAL incentive for liquidity providers likely helped attract capital, on the margin. However, liquidity conditions deteriorated across the market.

TVL on Balancer fell over 70% in the quarter. On Arbitrum and Polygon, TVL fell 88% and 86%, respectively. Ethereum still dominates the total value locked on the Balancer protocol, as its share of protocol TVL rose from 87% to 93% at the end of Q2’22.

The wstETH/wETH stablepool TVL remained the largest at the end of the quarter with over $87 million in TVL. In USD terms, the TVL fell by 75% in the quarter. The BAL/wETH 80/20 pool, which yields Balancer Pool Tokens that can be locked for revenue sharing, moved into second with $78 million in TVL. The pool’s TVL fell by 30% in the quarter. In native token terms, the BAL/wETH 80/20 pool increased its wETH by 124% in the quarter and its BAL by 149%.

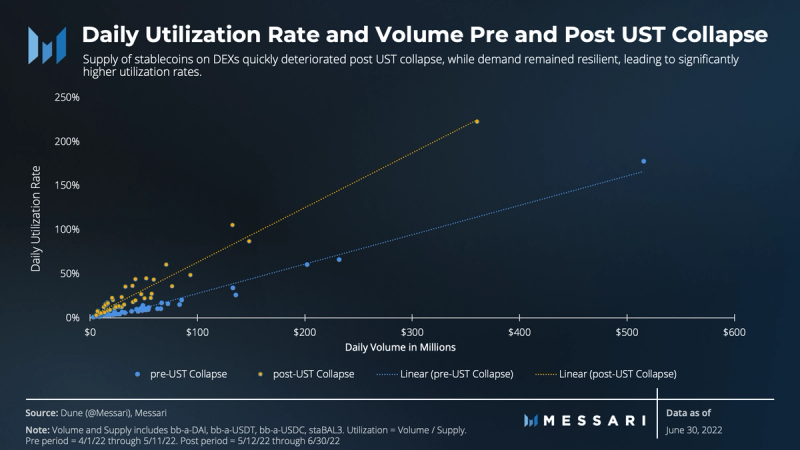

Stablecoin pool utilization rate is measured by dividing the daily volume by the daily supply. Utilization rates for the same daily volumes have been much higher since the UST collapse, even though there was no UST on Balancer. The numbers show that demand has been resilient, despite supply having decreased. Although slippage in stable pools is unlikely to increase dramatically, Balancer uses a vault that enables any trade to pull liquidity from any other pool. Therefore, the falling stablecoin supply will likely impact any large trade involving a stablecoin on the exchange.

Featured Pool Analysis

Diving into the pool data shows several changes this quarter. The market is white-knuckling liquidity, which has significantly affected the stablecoin supply on Balancer.

Aave Boosted Stable Pool (bb-a-USD) and staBAL3

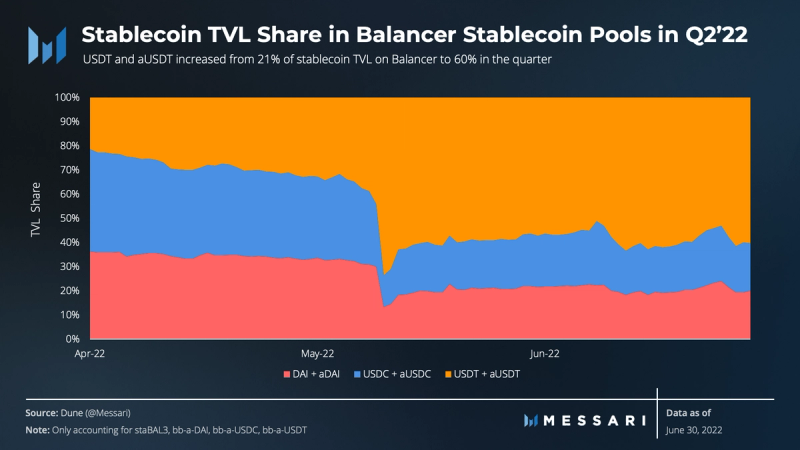

Balancer’s two largest stable pools are staBAL3 and bb-a-USD. staBAL3 is a DAI/USDC/USDT stable pool. bb-a-USD is a DAI/USDC/USDT boosted stable pool. It is made up of linear pools (discussed last quarter), each containing a stablecoin and a yield-bearing receipt for lending the token on Aave (aDAI/aUSDC/aUSDT).

Between Balancer’s two largest stablecoin pools, staBAL3 and bb-a-USD, stablecoin supply fell 70%. The bb-a-USD pool only lost 26% of its TVL to staBAL3’s 82% loss, though both are down over 80% from their TVL highs. In the quarter, the trading fees earned LPs a meager 0.01% APR for bb-a-USD, and the staBAL3 pool did more than twice as much in trading revenue in the quarter (including trading revenue from the linear pools that make up bb-a-USD). The yield on bb-a-USD was carried by boosted yields from Aave (roughly 0.75–1%) and primarily veBAL rewards.

Between the two pools, the UST collapse also marked a large change in makeup. USDT and aUSDT began the quarter at 21% of TVL but ended the quarter at over 60% of TVL. The price slippage for USDT being greater than USDC and DAI may have led to a greater share of it in the pool that has not reverted yet. The reduction in leverage across DeFi likely impacted DAI and USDC more than USDT given the larger role they play as collateral and debt assets.

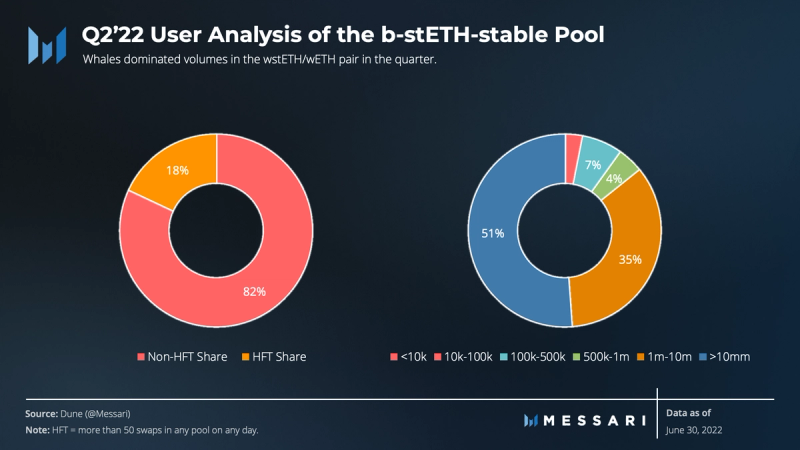

b-stETH Stable Pool (wETH/wstETH)

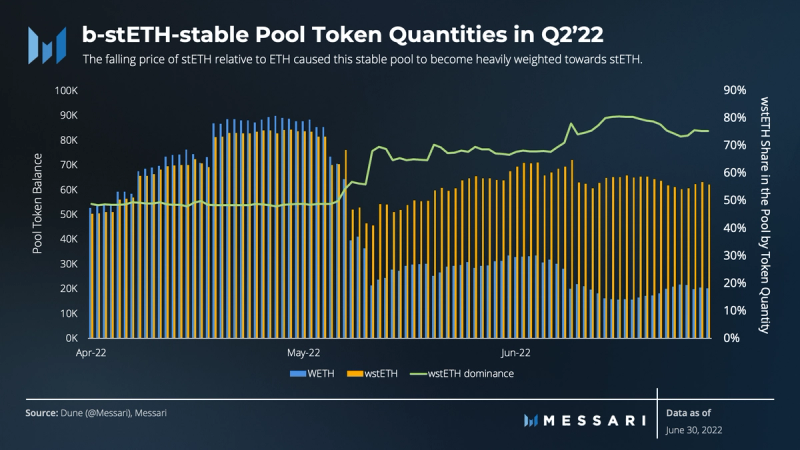

The increase in ETH’s market liquidity premium and pursuant fall in stETH prices relative to ETH have led to an imbalance in stable pools for these assets. wstETH ended the quarter as 76% of the pool, reaching a high of 81% on June 17 and 19.

Trading in the pool was dominated by large users in the quarter. Almost all of the volume was attributable to wallets who executed more than $1 million in volume in the quarter. These were likely not arbitrage players, given the lack of frequency with which they traded.

veBAL

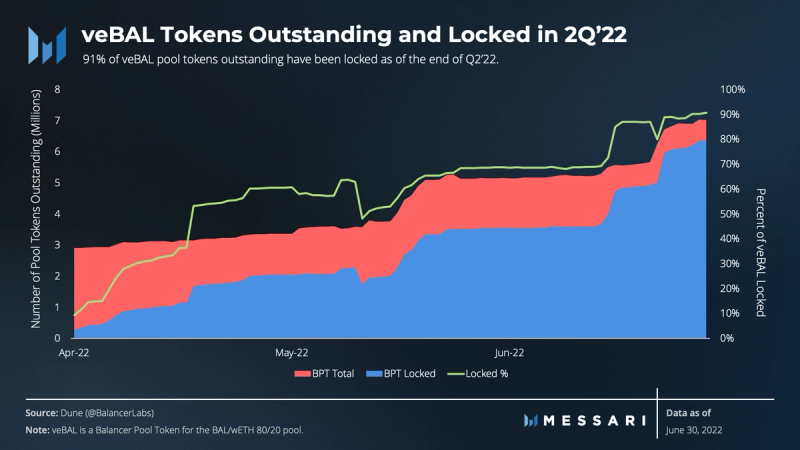

veBAL officially launched on March 29, with the first vote closing on April 7, and the first payout (after some technical difficulties) on April 27. Since launch, the number of Balancer Pool Tokens (BPTs) for the 80/20 BAL/wETH pool has increased from 2.9 million to 7 million. Over 90% of those are currently locked as veBAL (as of 6/30/22).

The experience so far has not been without surprises. For three weeks, the BADGER/wBTC 80/20 pool received nearly 50% of rewards. This pool earned only $7,506 in revenues for the protocol (DAO and veBAL holders combined) in the quarter (39th most), which led the DAO to adjust some gauge requirements. After the changes, the CREAM/wETH 80/20 captured 30–40% of the rewards the following 6 weeks. This pool has earned the protocol $20,196 in revenues (32nd most in the quarter).

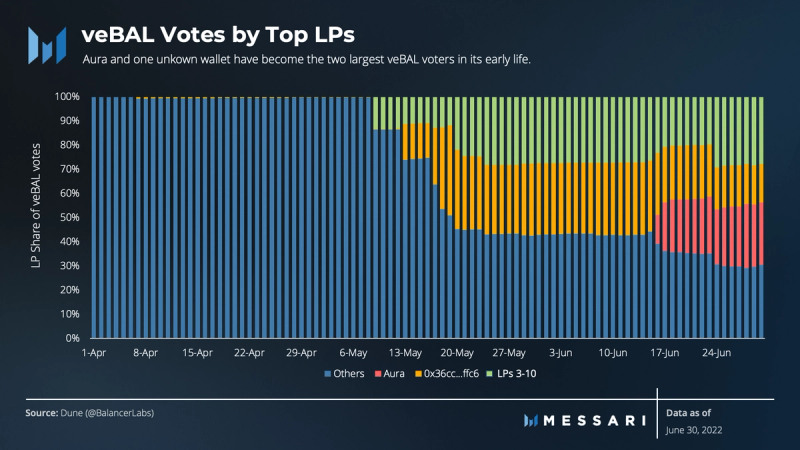

By quarter end, the top 10 voters comprise 70% of total votes. The largest two voters are Aura at 26% and an unknown wallet at 17%. Aura works for Balancer similar to how Convex works for Curve: users can deposit Balancer Pool Tokens in Aura for voting power and veBAL rewards.

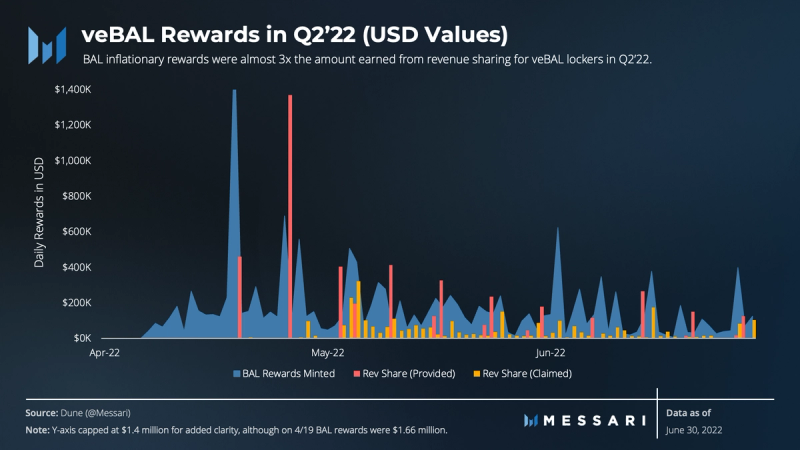

Liquidity mining rewards vastly outpaced the earnings from protocol revenue share in the second quarter. veBAL lockers earned $3.4 million dollars from their share of protocol revenues this quarter while the protocol paid out $14.6 million dollars worth of BAL inflationary rewards. This disparity creates an incentive misalignment, where inflationary rewards trump revenue share rewards. As a result, pools and voters may participate in veBAL for the liquidity mining rewards without attracting TVL to revenue-generating pools. An attempt to solve this kicked off on July 11.

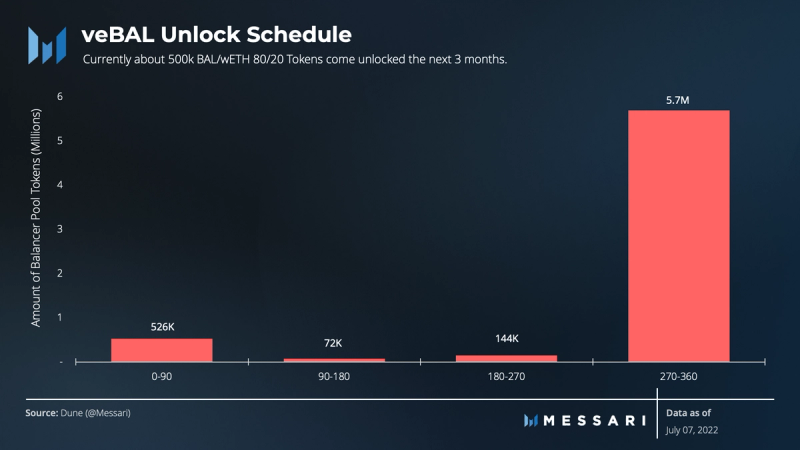

Lastly, we track the upcoming unlocks from veBAL to be aware of potential liquidity events for veBAL locked pool tokens and thus BAL (veBAL is a locked 80/20 BAL/wETH Liquidity Pool Token). As of the first week of July, 92% of locked veBAL is locked for nine months or longer. In the next six months, 10% of locked veBAL will come unlocked. That is roughly 600,000 Balancer Pool Tokens, which frees up roughly 1.3 million BAL using June 30 prices (BAL supply is roughly 50 million).

Treasury

With the introduction of veBAL, the DAO increased its revenue share from 10% of trading fees to 12.5%. However, from mid-February until the end of Q1’22, the DAO was earning 50% of trading fees, inflating Q1 numbers. The DAO implemented a weekly automated sweep of tokens earned from fees into bb-a-USD, while the above numbers were measured at daily value. Given the bear market and falling prices, actual revenues received in USD were lower than estimated here.

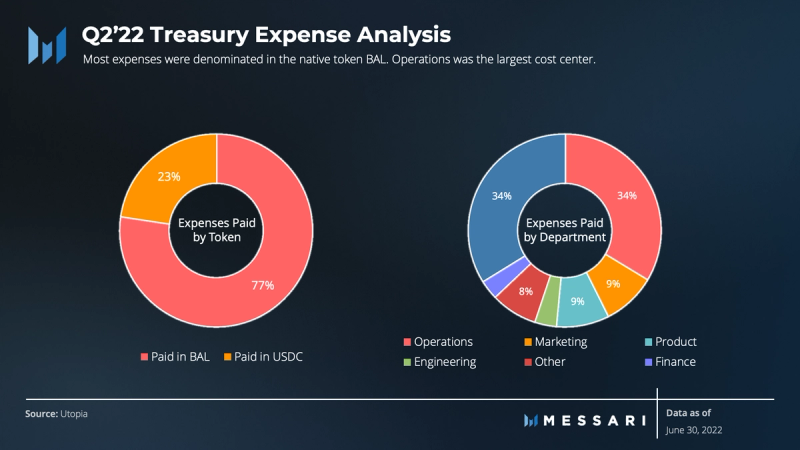

The DAO was focused on creating structure around protocol expenses this quarter. It spent ~$747,000 dollars, or 45% of revenue earned, last quarter. Importantly, 77% of the DAO’s spending was in native tokens (BAL) this quarter. Pending or recently passed proposals have significantly more spending in USDC, creating additional planning around treasury asset-liability management.

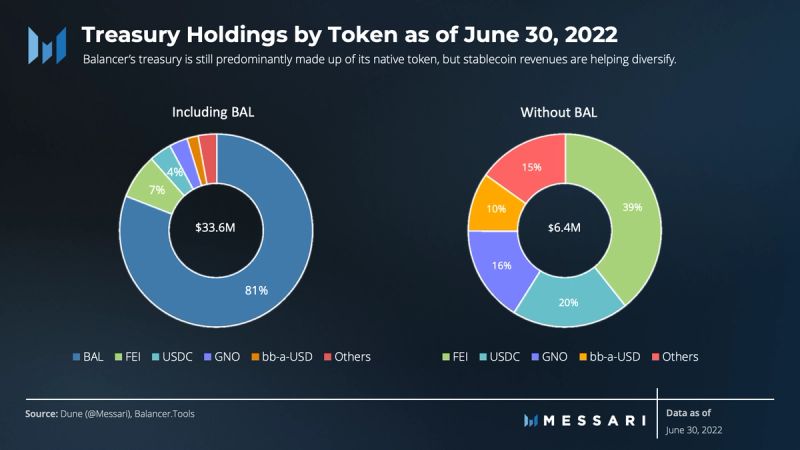

In USD terms, the DAO Multisig Treasury balance fell by 50% in the second quarter. In token quantity, the DAO increased its BAL holdings from 4.1 million at the beginning of Q2 to 5.9 million at quarter end. BAL concentration in the DAO multisig is over 80%. In only two quarters since turning on protocol revenues, the DAO has added over $5 million in other tokens and over $4 million is USD-pegged stablecoins.

Qualitative Analysis

DAO Structure Changes

On April 24, the DAO voted to incorporate the Balancer Foundation as a Cayman Island entity. This move would later require funding and specification, but it sets the stage for Balancer to have an incorporated entity. Tristan Relly, the Foundation’s new CEO, described the purpose of the Foundation in his funding post: “In short, the Balancer Foundation acts as an agent for the BalancerDAO in the structure of the traditional business world.”

Legal entity formation for DAOs has become a hot topic. Balancer leaned on precedents from ENS, dYdX, and PrimeDAO. The Foundation has not yet played a role in any notable Balancer operations or decisions.

Much more impact has been felt from the June 12 vote for a formalized Operating Framework for Balancer DAO. In January of this year, the DAO voted to form subDAOs in order to create focus groups for specific responsibilities and speed up decision making in those areas. It also formalized the creation, responsibilities, accountability, and dissolving of subDAOs. The Operating Framework aims to codify the funding process for any Service Provider (SP) to the DAO, including subDAOs.

The initial impact has been a more critical funding process — certainly impacted by tougher market conditions. There has also been some unfortunate animosity and potentially unproductive debate in the forums. Four of six proposals have achieved a yes vote to their funding proposal (including one that did not go to a vote). The largest proposal, to fund the Orb Collective, drew nearly 3.5 million veBAL votes. For reference, the quorum requires 200,000 and typically gets few more than that. The vote passed with 1.84 million votes for and 1.63 million votes against.

The Orb Collective is basically a transition for many of the Balancer Labs employees into a separate entity to focus on Partnerships, Marketing, Integrations, Design, and People Operations for Balancer DAO. The price tag is almost $4 million for a year of funding, all in USDC.

The Operating Framework and the Orb Collective are polemical but serve as a case study for DAOs. DAOs could potentially grow by being capital allocators, oftentimes to Service Providers (SPs). We have seen B2D (Business-to-DAO) SPs help with risk modeling and smart contract auditing. This new framework is a case study on how to create structure around that capital allocation process for a DAO.

veBAL Lessons So Far

Transitions can be tough, even when moving between two good things. The transition to veBAL rewards has come with such growing pains. The DAO has had to play a bit of whack-a-mole with incentive alignment issues/abuses of the new system. It is unclear if these games will continue or are simply growing pains.

In the first week of veBAL, the DAO was forced to re-vote on the gauge buckets available. Originally, a specified amount of BAL rewards were meant to be distributed to each chain and to veBAL holders (10%). The current code configuration made that impossible. Two options were presented: vote to change the buckets or vote to rebuild the code. Passing 58% to 42%, the DAO decided to keep the code configuration and change to buckets, removing a guaranteed BAL reward for veBAL holders.

On May 26, the DAO voted to create the Emergency subDAO and associated multisig wallet. The vote was a reaction to a rogue Element pool, which was grandfathered into the veBAL gauge system. Without getting into the mechanics, a single LP was able to vote BAL rewards to themselves in a pool with almost no liquidity. The Emergency subDAO is enabled with powers to kill any gauge (not a pool, just the gauge for that pool to receive rewards).

After the CREAM/wETH 80/20 pool gauge was approved by the DAO, the owners of the pool set trading fees to 10%. The goal was likely to be able to passively farm BAL rewards, without bringing any trading revenues to the DAO. Clearly, this is a misalignment of incentives. On June 12, the DAO voted to implement new gauge requirements. The changes require each gauge’s underlying pool owner to be set to Balancer governance. Exceptions are possible, but pursuant fee changes require clear and preemptive communication with the DAO. Failure to do so gives the Emergency subDAO the right to remove the gauge.

At quarter end, the DAO voted to create and incentivize core pool and L2 usage. The complex proposal essentially creates a 1-week delay in sending veBAL holders revenues, which will now be distributed bi-weekly instead of weekly. In the extra week’s time, veBAL lockers’ share of the fees earned from the protocol will be used to bribe voters to allocate rewards to core and L2 pools, thus aligning veBAL lockers and the DAO.

The mechanism allows the DAO to designate certain pools as core pools and then to use bribes to incentivize voters to send rewards to those pools. A key proponent is that core pools have yield-bearing tokens, where the DAO receives a portion of the yield generated. Therefore, by adding rewards to those pools, more TVL is attracted, and the DAO directly benefits from TVL increases because of its revenue share from yield generated. For L2 pools, the mission is simply to incentivize TVL.

Partnerships and Integrations

Balancer has taken many successful steps towards becoming a platform that creates liquidity solutions for DAOs. Previously, Balancer teamed up with COWswap to offer gasless trade options. Element builds custom pools on Balancer for their fixed-term lending solutions. Copper built an LBP platform. Lido and TribeDAO both use BAL to improve liquidity of their token offerings.

Beethoven X has emerged as a key partner. Last year, Beethoven X launched Balancer on Fantom as a “Friendly Fork.” This quarter, the two deepened their ties and launched Balancer by Beethoven X on Optimism with a 50/50 revenue-share agreement. The team was able to quickly spin up a Balancer instant on the L2 scaling chain that will be managed by Beethoven X.

In the quarter, Balancer also voted to fund an integration of Balancer Boosted Stable Pools with DEX aggregator 1inch. The DAO voted to do a treasury swap with Aave, though this has not been executed yet. Some votes failed, including an effort to create a reactor on Tokemak. A preliminary vote to use Ribbon yield strategies (selling calls) on treasury assets failed, but a second one with reduced commitments recently passed.

Perhaps the biggest partnership of the quarter was the launch of the vote aggregator Aura. Instead of locking BAL/ETH 80/20 Pool Tokens on Balancer for veBAL, users can stake the BPTs on Aura in exchange for auraBAL. This is a one-way transaction, as the BPTs are locked in Balancer for the maximum amount of time (1 year). There is a secondary trading market to get BPTs for auraBAL. Users can then stake auraBAL for AURA rewards, on top of receiving voting power to direct and receive veBAL rewards.

Since launching on June 9, Aura has amassed over 25% of veBAL voting power. The long-term implications are certainly unclear, but so far Aura is off to a strong start. They partnered with Redacted Cartel. With the new core pools and L2 incentives run on Hidden Hand, the duo will likely have a great opportunity to control much of the Balancer revenue share and governance.

Other Notable Events

April 15, 2022 – Balancer.Tools V2 launched

April 18, 2022 – Distribute Protocol Fees in BAL

April 18, 2022 – Fund BalancerDAO Q2 2022 Budget

April 28, 2022 – Empower BalancerDAO to Add Approved Gauges to veBAL Voting

April 28, 2022 – DAO Multisig Signer Replacements

May 3, 2022 – Balancer Grants Monthly Update #6

May 12, 2022 – Introducing Delegation for veBAL

May 13, 2022 – Medium Severity Bug Found

May 17, 2022 – Vulnerability Disclosure, Stable Pools, and Managed Pools

May 23, 2022 – Introduce ProtocolFeesWithdrawer

May 30, 2022 – Allocate BAL for Optimism Incentives

June 2, 2022 – Balancer plans to launch on Gnosis Chain

June 3, 2022 – Balancer Grants Monthly Update #7

June 5, 2022- Introduce ChildChainGaugeTokenAdder

June 7, 2022 – TWAMM Research Update

June 12, 2022 – Allocate BAL Towards Ethereum x Optimism Bridge Liquidity

June 20, 2022 – Update Snapshot Parameters

June 26, 2022 – Fund Balancer Maxis for Q3 2022

June 26, 2022 – Update DAO Multisig Replacement List

June 30, 2022 – Balancer Grants Wave 4 Final Report

Closing Summary

Balancer had no operational issues in the second quarter, and its usage measured by number of swaps or volume increased meaningfully. Balancer’s TVL fell as market participants withdrew liquidity across the board. The veBAL experiment is still in its early stages, paying out over $20 million in the quarter between revenue share with lockers and inflationary rewards to LPs. The DAO will continue to tweak the rules and management of veBAL incentives to best align gauge voters with the protocol. Balancer continues to lead the evolution of DAOs, implementing new frameworks and incorporating a foundation in the quarter.

Looking to dive deeper? Subscribe to Messari Pro. Messari Pro memberships provide access to daily crypto news and insights, exclusive long-form daily research, advanced screener, charting & watchlist features, and access to curated sets of charts and metrics. Learn more at messari.io/pro

This report was commissioned by Balancer, a member of Protocol Services. All content was produced independently by the author(s) and does not necessarily reflect the opinions of Messari, Inc. or the organization that requested the report. Paid membership in Protocol Services does not influence editorial decision or content. Author(s) may hold cryptocurrencies named in this report.

Crypto projects can commission independent research through Protocol Services. For more details or to join the program, contact ps@messari.io.

This report is meant for informational purposes only. It is not meant to serve as investment advice. You should conduct your own research, and consult an independent financial, tax, or legal advisor before making any investment decisions. Past performance of any asset is not indicative of future results. Please see our terms of use for more information.