Download the PDF version of this report by clicking here.

Key Insights

- dYdX announced a new Cosmos SDK-based blockchain called dYdX Chain; the sovereign network is needed to achieve the protocol’s goal of launching a fully decentralized V4

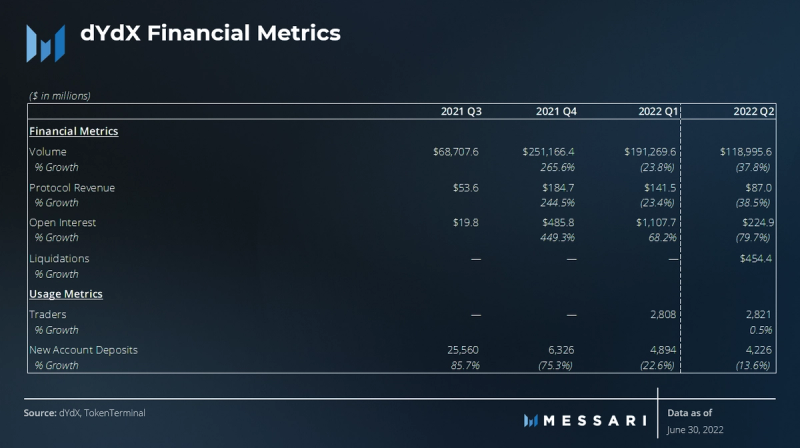

- Trading activity fell 37.8% from the previous quarter, though dYdX outperformed the decline of crypto’s market cap as a whole

- BTC and ETH continue to drive roughly 85% of all volume

- The number of weekly traders fluctuated depending on market volatility but averaged more than 3,000

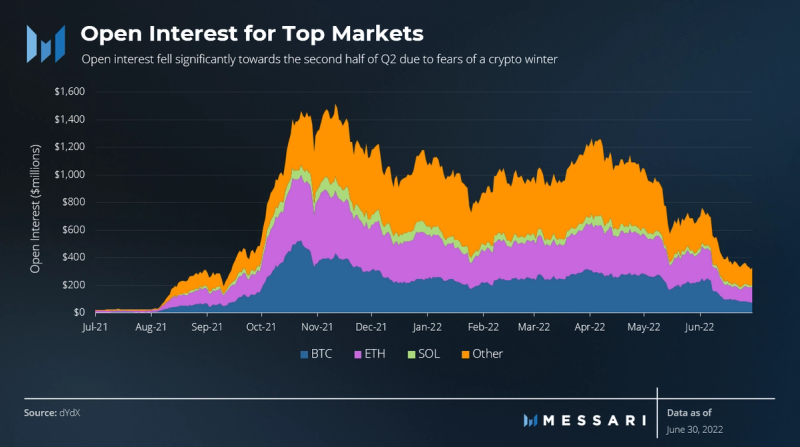

- Open interest (USD) declined 79.7% as underlying token prices dropped

A Primer on dYdX

dYdX Protocol operates a derivatives exchange on the Layer-2 StarkEx network. Cleverly named after the mathematical notation, the hybrid-decentralized exchange offers perpetual futures (perp) contracts similar to the ones found on Binance, FTX, and other centralized exchanges. The protocol’s ultimate goal is to build a fully decentralized derivatives exchange where no single party, including the team itself, can claim authority over the protocol’s fundamental operations.

dYdX was founded by Antonio Juliano, an ex-Coinbase engineer, who began working on the idea in the summer of 2017. The protocol’s first two products, Expo and Solo, were built for margin trading on Ethereum. After seeing the explosion of perp trading on Bitmex in 2019, dYdX decided to become the first DeFi protocol to provide perp trading. The launch of perps for major tokens like BTC and ETH quickly grew in popularity among traders seeking to use margin. Ease of use was further improved with the addition of StarkEx Layer-2 (L2) rollups in 2021.

This past quarter, dYdX announced a transition from StarkEx to its own native blockchain, called dYdX Chain, as part of its effort to fully decentralize by the end of 2022. It is a milestone moment for DeFi and another step in the protocol’s journey as a trailblazing derivatives exchange.

Performance Overview

dYdX now has 38 perp markets, up from 33 at the end of last quarter. Governance has already targeted 15 new assets for further listing, highlighting the protocol’s continued focus on serving its user base. Of those 38 markets, BTC and ETH continue to comprise the majority of trading volume at 44.6% and 40.2%, respectively. This is in line with the previous quarter when those two tokens made up 85.4% of volume.

Macro Overview

dYdX trading volume is down 37.8% from $191 billion last quarter to $119 billion this quarter. Part of that is due to a decline in token prices.. Comparing dYdX’s volume trend to the Q2 performance of crypto’s market cap , provides a better picture of the performance of the protocol. In this light, dYdX outperforms. Market cap of all tokens fell 50%; market cap of blue chip tokens like ETH fell almost 70%.

Q2 did see an increase in SOL trading in relative terms. The token replaced AVAX as the third-most active market, edging the latter out by roughly $500 million. This increased activity may be attributable to SOL’s heavy price movement. Backed by venture capitalists and crypto influencers, SOL benefitted from the ‘Solana Summer’ trade rotation amidst the last bull market; its price peaked at $250 but fell to less than $30 this past quarter, a nearly 90% decline. Such a crash could have appealed to traders who wanted to open a short position on the perp market.

Open interest is another high-level metric for perp exchanges. It is the indicator used to track open, outstanding contracts. Open interest on dYdX peaked last year, fell in Q1, and continued to fall in Q2. All markets, including BTC and ETH, followed this pattern though the two assets seemed to trend positively on their way to recovery before another precipitous drop occurred in June.

What’s most attributable to the decline in open interest is the collapse of the Terra ecosystem and its subsequent effects. Those effects include the liquidation of prominent crypto hedge funds and the insolvency of large centralized lenders. The market moved quickly as investors rapidly flushed capital out of the system, which explains the closing of perp contracts and the drop in open interest. For now, crypto does appear to be in a bear market, but the beauty of perps is that they can be traded as both a bearish or bullish indicator. What happens next for this metric is yet to be seen.

While open interest is down, the average number of weekly traders is higher for Q2 than Q1, which might be a signal of continued growth. That said, weekly trader counts are volatile and can swing widely from one week to the other. Weekly traders peaked at 4,530 for the week of May 8th. Not surprisingly, that was the same week the price of Terra’s native stablecoin, UST, began to lose its peg. It is also the same week Terra’s token, LUNA, began to crash. Both ended up going to fractions of a cent. The chaotic trading frenzy that week likely forced individuals to take action on their positions, resulting in the quarterly high.

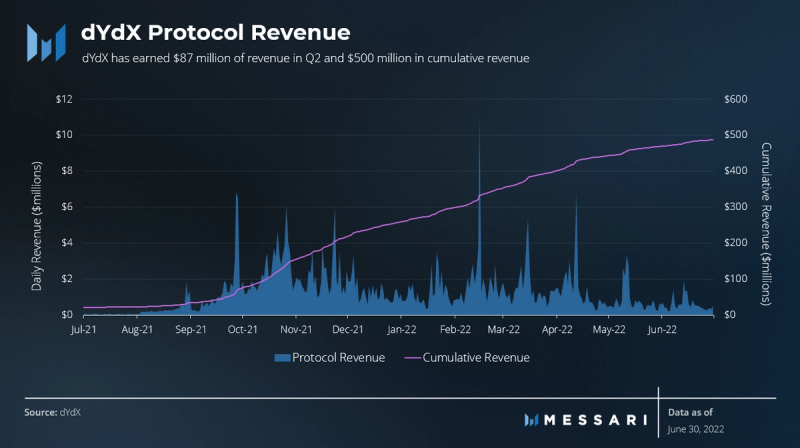

Revenue earned from trading fees continued to see spikes when high volatility occured, although daily revenue is lower than it was during most periods in Q4 of last year and Q1 of this year. In sum, revenue fell 38.5% from the previous quarter. Since volume was down this quarter by 37.8%, it makes sense to see revenue fall by a similar amount.

Perpetuals Market Spotlight

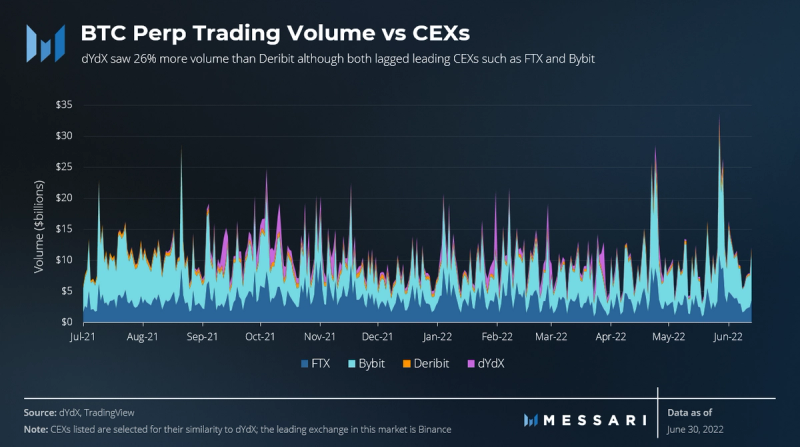

Our methodology benchmarks the top three markets by volume against the protocol’s major competitors. Three centralized exchanges are selected as a peer group for the protocol: FTX, Bybit, and Deribit. These three exchanges vary in size and geographic focus. Comparing the DeFi-equivalent of these services to the centralized option sheds insight into the inroad DeFi is making with traders.

BTC Market

The highest-volume market was BTC. Out of the peer group, dYdX was the third largest exchange, facilitating 26% more volume than Deribit. Roughly $53 billion of BTC perp trading was done on dYdX. That averages to about $583,000 each day this quarter.

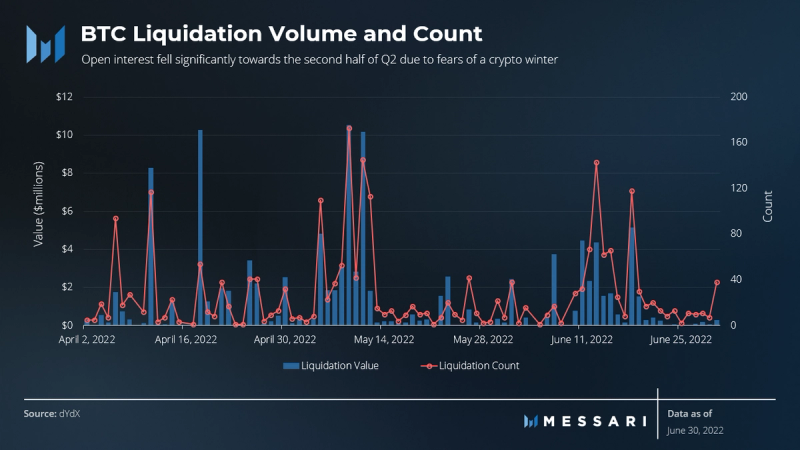

During the period, open interest expressed in BTC tokens was highest during the period of market volatility in June. It peaked on June 5th at 8,154 tokens worth of contracts equaling $248 million. Open interest does not give analysts a view of investor sentiment – bearish or bullish. However, the fact that new contracts were opening up leading up to this date, while the market was decreasing, hints traders were trying to take advantage of the downward pressure.

The sudden collapse of Terra created a contagion that affected BTC prices in particular. Multiple crypto institutions needed to liquidate their BTC holdings on the market, generating large selling pressure without many corresponding buyers. As a result, approximately 15 days in the quarter (8 in mid-May, 7 in mid-June) accounted for 50% of the number of liquidations alone. Those liquidations total 48% of the dollar amount.

ETH Market

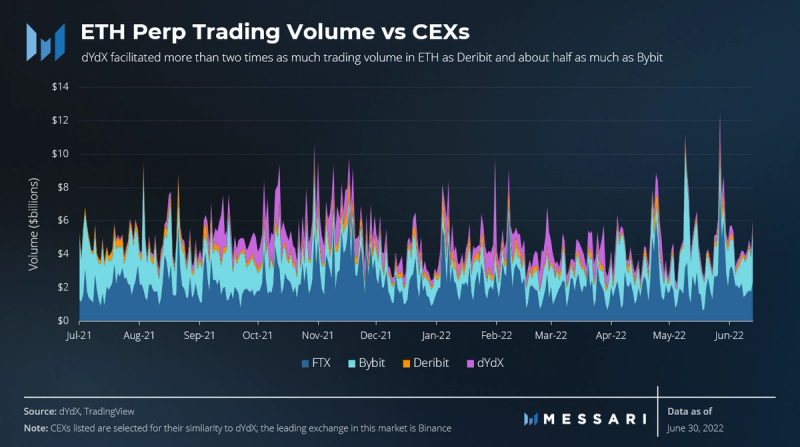

ETH is the other blue-chip market and crypto’s most active blockchain. All exchanges have now offered ETH trading for years, including dYdX. It is also where dYdX is strongest against the selected peer group. Whereas dYdX only manages 5.5% of BTC trading , its share of ETH trading is 14.3%, almost three times as much. This is likely because dYdX users are likely already familiar with the properties of ETH and are “arguably Ethereum-native”.

One remarkable thing about the ETH market is that open interest denominated in native tokens holds fairly steady throughout the quarter. This means investors are continuing to hold the number of open contracts steadily even during volatile markets. There are moments when open interest declines but it typically recovers quickly. Open interest as measured in USD terms does fall in the same manner as BTC due to the token’s price depreciation. On June 30th, 104,000 ETH were outstanding in contracts totaling $114.5 million.

SOL Market

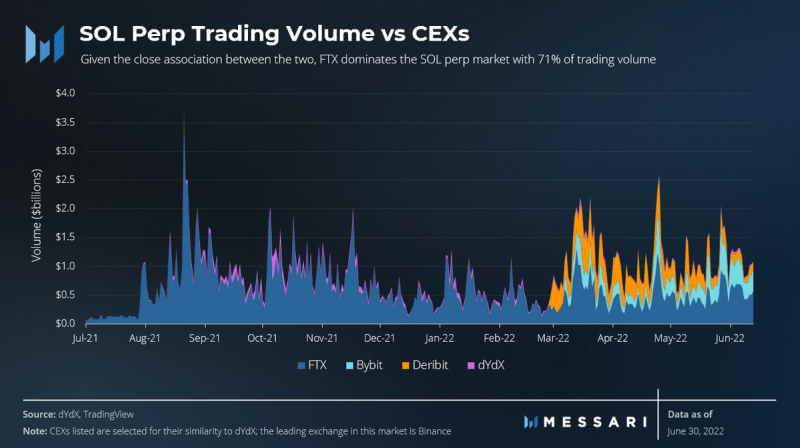

Solana is where dYdX is weakest relative to competitors – and for a good reason. Sam Bankman-Fried, the founder of FTX, is closely associated with both Serum, the largest DEX on Solana, and Alameda Group, a crypto trading firm with a large position in the SOL token. FTX was also among the first CEXs to support the trading of SOL perps. This was particularly advantageous for them when ‘Solana Summer’ occurred and traders wanted to find a way to take positions in the asset.

Hence, SOL continues to occupy a large mindshare in crypto. And although SOL overtook AVAX as the third-largest market on dYdX, it still accounts for less than 3% of trading volume on dYdX with $2.9 billion this quarter. A total of 880,730 trades were made in this time frame, resulting in an average trade size of $3,236.

Qualitative Analysis

Transition to Cosmos App-Chain

On June 22nd, dYdX announced dYdX Chain, a standalone blockchain built using Cosmos SDK and the Tendermint PoS consensus mechanism. The transition to this independent network is a significant departure from its current model built on StarkEx. For a protocol like dYdX with a blue-ship reputation, such a move has potential ramifications for builders and investors alike.

According to the team, the shift to a Cosmos app-chain model is needed for dYdX to meet its goal of launching V4 by year-end. At the heart of things was the balance between decentralization (the main selling point for V4) and having a high-throughput order book matching engine. The dual requirements left little choice but to build a decentralized off-chain network via a wholly independent chain.

The move has a few benefits for the community but the biggest advantage of this is it helps a long-standing question from all stakeholders: how the protocol plans to create a value proposition for those holding DYDX. In this new structure, DYDX could natively be used to secure the blockchain, though the decision will ultimately be left to governance. If governance does make this decision, it would entice people to hold the token for reasons beyond just the trading fee discount offered today.

The decision to build a sovereign app-chain is bullish for Cosmos bulls. For Ethereum proponents, it’s not definitively the end of the world either. Comparing the two, Cosmos today offers more decentralization, higher throughput, value accrual, and ease-of-development; L2 rollups offer more security, a larger user base, and in certain cases, quantum technology resistance. Strike this as a victory for the multi-chain future, but much remains to be seen.

New Trading Markets

Every week or two, dYdX introduces trading markets for new tokens. The protocol added markets for eight new tokens. The following is a list of new tokens that were added to the exchange at some point in Q2:

- Ethereum Classic (ETC)

- Terra (LUNA)

- Note: The LUNA-USD market was announced on April 12th. Due to the price action following LUNA’s collapse, the decision was made to put the market to close-only. No new positions were allowed beyond May 12th, exactly one month after going live

- NEAR Protocol (NEAR)

- Thorchain (RUNE)

- Celo Network (CELO)

- Internet Computer (ICP)

- Tron (TRX)

- Tezos (XTZ)

Governance Updates

Jun 21, 2022 – Adding 15 New Assets to the Starkware Priority Timelock Executor

After a review of the process to list assets on the exchange, a governance vote was submitted by Reverie to further increase the number of assets open for trading. 15 assets were included in the snapshot vote: APE, GMT, FTM, AXS, OP, WAVES, GALA, SAND, MANA, SHIB, THETA, RSR, ZIL, VET, and ENS. Of the 15 tokens, the greatest demand exists for GMT, which sees $2.2 billion in 24-hour perp trading volume. The snapshot proposal passed with 100% vote and a dydX Improvement Proposal will soon be submitted to add these assets to the Starkware Priority Timelock Executor for priority listing.

July 6, 2022 – Wind Down the Borrowing Pool

A proposal was submitted to wind down the USDC borrowing pool. The original intention behind the feature was to allow pre-approved institutions the option to borrow USDC to help make markets. However, the pool was underutilized; only 30.5% of the available capital was being borrowed, creating high levels of capital inefficiency. The vote to close the pool helped eliminate capital inefficiency for those supplying USDC. It also allowed the protocol to redistributed DYDX rewards to better use cases, such as those who stake USDC in the Community Treasury.

July 15, 2022 – Launch dYdX Grants Program v1.5

In light of the success of the dYdX Grants Program, the community voted to fund another round of grants. The timing of v1.5 would coincide six months ahead of the V4 launch. Capital would be utilized to support the dYdX ecosystem in the protocol’s ongoing quest to fully decentralize. It was decided $5.5 million from the Community Treasury would transfer to the Grants Multisig based on the price at the time of the proposal. As part of this proposal, Su Zhu and Zhuoxun Yin (COO of Magic Eden) would be removed as Trustees of the Grants Trust.

Closing Summary

Looking at Q2, on one hand, there’s the quantitative story: as goes the price of tokens, so do many high-level metrics. Like other exchanges, dYdX was hit by decreased volumes, open interest, and protocol revenue. All those metrics depend on trading interest, however. When activity recovers, so will those.

But there’s also the qualitative story. And by far the biggest shakeup from this quarter was the announcement of the dYdX Chain. It’s not hyperbole to say the success of dYdX’s implementation will influence the direction others go. There’s significant long-term ramifications at play. We all await and see.

Let us know what you loved about the report, what may be missing, or share any other feedback by filling out this short form.

This report was commissioned by the dYdX Grants Program, a member of Protocol Services. All content was produced independently by the author(s) and does not necessarily reflect the opinions of Messari, Inc. or the organization that requested the report. Paid membership in Protocol Services does not influence editorial decisions or content. Author(s) may hold cryptocurrencies named in this report.

Crypto projects can commission independent research through Protocol Services. For more details or to join the program, contact ps@messari.io.

This report is meant for informational purposes only. It is not meant to serve as investment advice. You should conduct your own research, and consult an independent financial, tax, or legal advisor before making any investment decisions. The past performance of any asset is not indicative of future results. Please see our terms of use for more information.