Key Insights

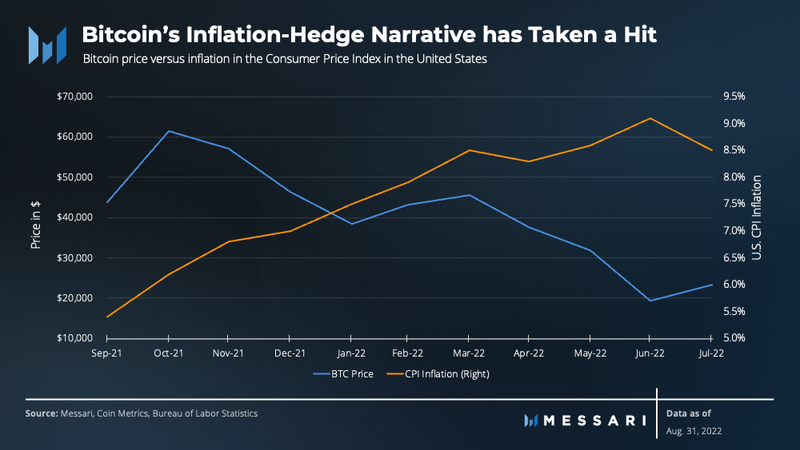

- Within Q3, Bitcoin largely lost its inflation hedge and store-of-value narratives in the market after falling 72% from ATHs.

- As demand for blockspace falls, Bitcoin transaction count and transaction fees have fallen 3% and 23%, respectively. Average daily value settled declined 44% QoQ.

- Due to steep increases in energy prices, all-time-highs in hashrate, falling bitcoin prices, and lower transaction fees, miners found themselves in an increasingly difficult position.

- The White House Office of Science and Technology Policy (OSTP) raised concerns on how Proof-of-Work could hinder U.S. efforts to combat climate change and how energy-intensive mining could negatively affect electricity grid reliability and prices.

- Despite criticizing Proof-of-Work, the OSTP’s report highlights how Bitcoin mining can help reduce greenhouse gas emissions and help accelerate the transition to a renewable grid.

Primer on Bitcoin

Bitcoin is the first distributed consensus-based, censorship-resistant, permissionless, peer-to-peer payment settlement network. Bitcoin (BTC), the native asset of the Bitcoin blockchain, is the world’s first digital currency without a central bank or administrator. Often referred to as digital gold, Bitcoin has a predictable, stable monetary policy that operates autonomously, giving it the ideal store-of-value properties. To secure its network, Bitcoin uses a consensus mechanism known as Proof-of-Work (PoW) to solve the “double-spend problem.” PoW requires participants (miners) to contribute computing power to solve arbitrary mathematical puzzles in order to add a new block to the blockchain. Bitcoin is awarded to the miner who solves the puzzle first, thus minting new bitcoins.

“Bitcoin is like a mirror, its hottest narrative reflecting what society most needs” -Chris Burniske

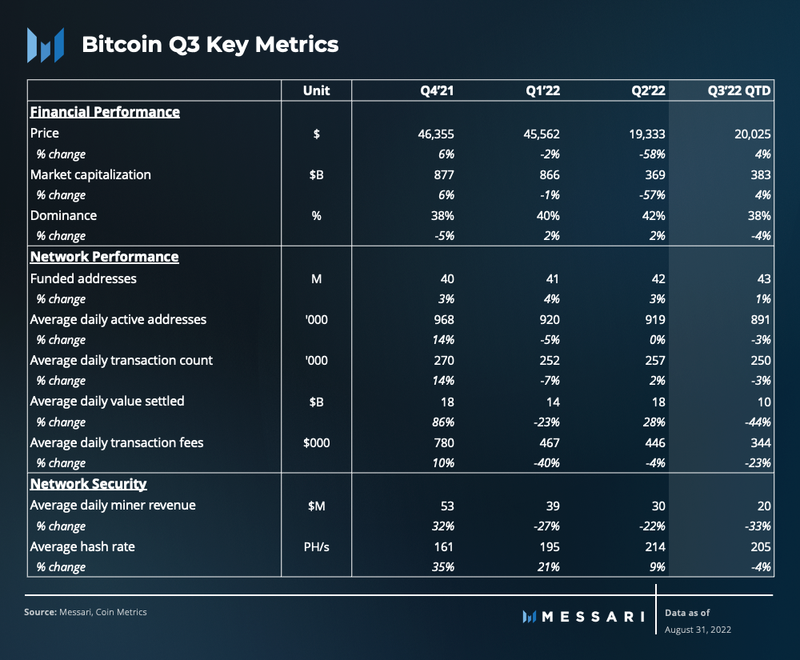

Key Metrics

Performance Analysis

Quarter Highlights

The latest market crash has been a narrative breaker and reality check for the top cryptoasset.

- Inflation hedge — With its fixed supply and hardened monetary policy, the narrative goes that bitcoin should act as a hedge against inflation. Instead, bitcoin has made new cycle lows even as the CPI inflation in the U.S. hit multi-decade highs.

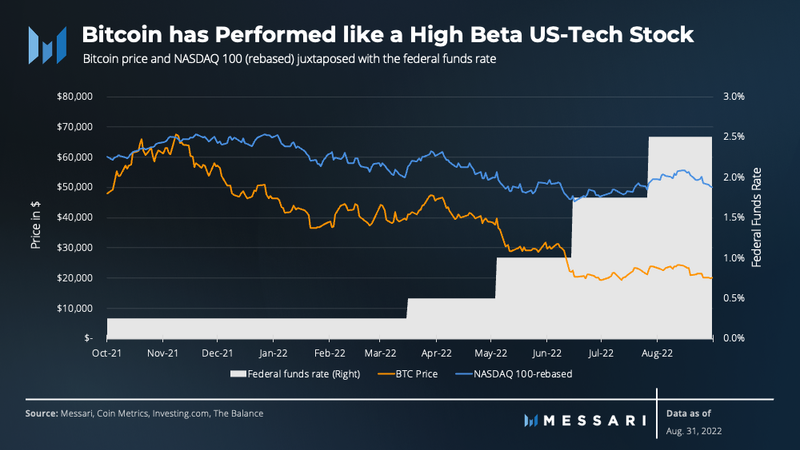

- Store of value — Since hitting an all-time-high of $69,000 in November 2021, bitcoin has fallen 72% amidst a risk-off macro environment. Instead of a store of value, the price action has been similar to that of a high-beta U.S. tech equity. Bitcoin price suffered as the Federal Reserve turned to a more conservative regime with lower liquidity and higher rates.

- Bear asset outperformer — Even in the throes of a bear market, the top coin lost market cap dominance. The primary reason was Ethereum’s outperformance as it progressed towards its transition to Proof-of-Stake.

- Maturing institutional asset with lower volatility — Many institutions capitulated, with Tesla most notably selling most of its bitcoin in Q2 of 2022. Capitulation from large lending platforms and funds further contributed to the volatility. As such, the asset has yet to “mature” to a lower risk spectrum, even though some institutions did come.

Over 70% drawdowns are hardly new for Bitcoin and its holders. Bitcoin has been known to rise from the ashes. While user and transaction growth may be hard to find, activity did not fall as much as price. With price at multi-year lows, the tourists have left but the network continues to chug along. The bear market is the time for builders to build and believers to accumulate.

“Bitcoin is dead. Long live Bitcoin.”

Market Metrics

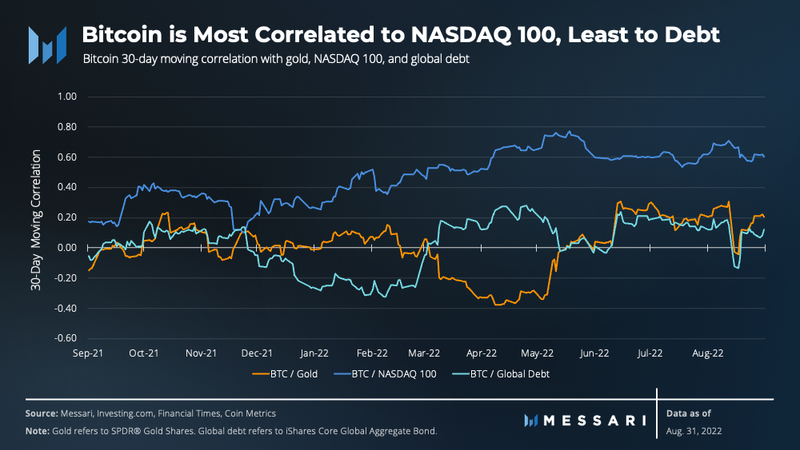

Bitcoin returns have increasingly correlated with US-tech stocks since the liquidity-fueled bull market ended in late 2021. For the quarter, the average correlation between Bitcoin and NASDAQ 100 was 0.6 as inflation and rate hikes dominated the narrative. Surprisingly, digital gold and physical gold are far less correlated. The average correlation for the quarter between the two assets was 0.2.

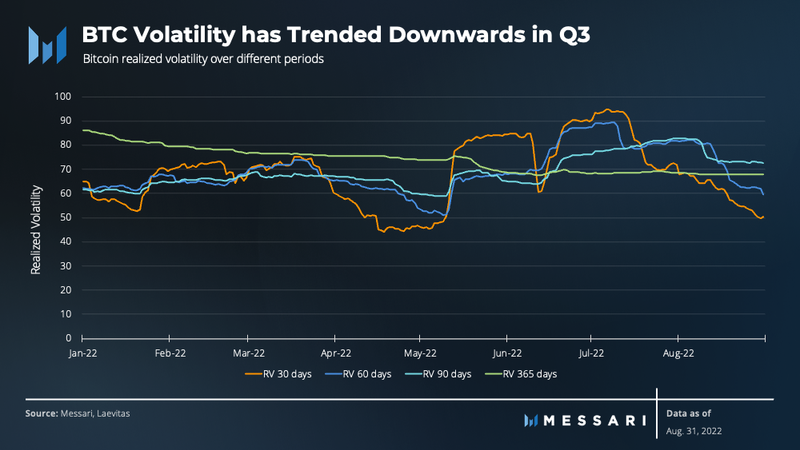

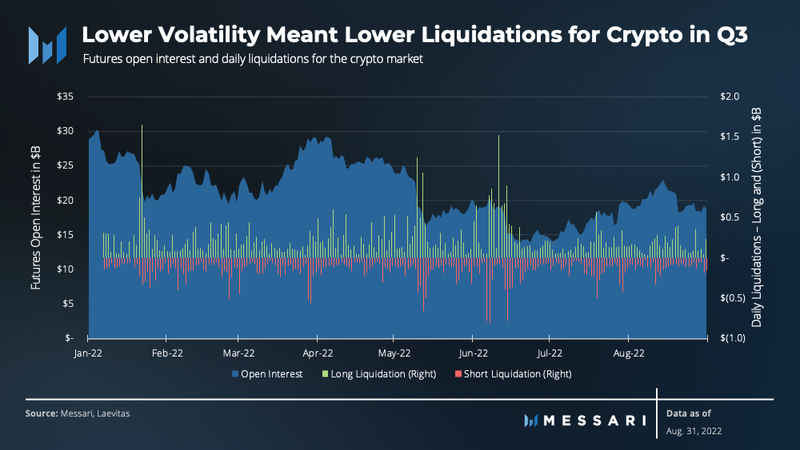

Bitcoin realized volatility trended downwards as it made a gradual recovery in Q3. Average 30-day volatility for August was 60% compared to over 80% for June. Lower bitcoin volatility resulted in lower liquidations for the broad crypto market. The total long liquidations in August were $5 billion, less than half of that in June ($10.8 billion). Total short liquidations were significantly lower as well, $3.5 billion in August compared to $6.6 billion in June.

Network Overview

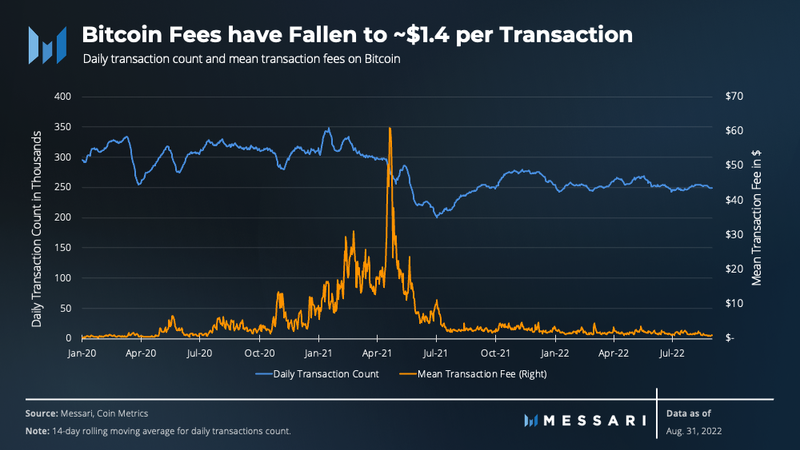

Daily transactions for the network have remained largely unchanged for the whole year, averaging around 250,000 per day. Average transaction fees have been very low since the first bull run of 2021. Quarter to date, the average fee per transaction was only $1.4, down 21% for the quarter and 55% for the year.

The last fee spike occurred in early 2021 when bitcoin’s price made new highs. Typically during bull runs, users are willing to pay higher fees to make sure their transactions are included as early as possible.

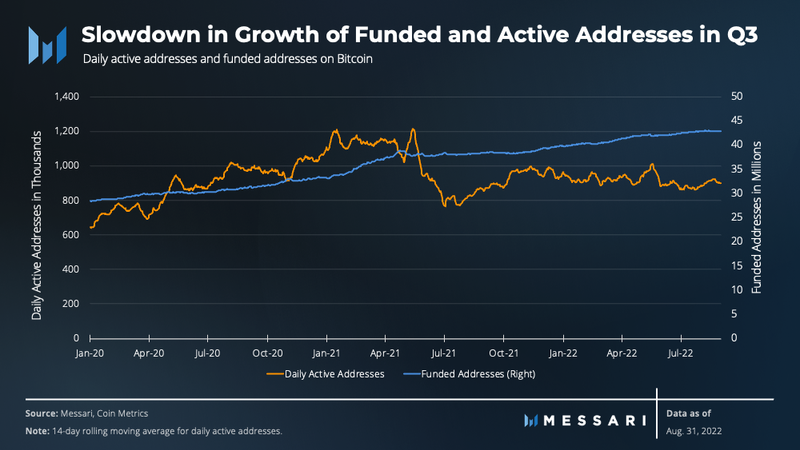

Growth in funded addresses slowed for the network. During Q3, funded addresses only grew by 1.1% compared to 2.5% in Q2 2022. On a monthly time frame, the number of funded addresses experienced its first decline in August 2022 after 10 months of consistent growth.

Average daily active addresses at 890,000 were down 4% compared to Q2 2022. Active addresses seem to have returned to their baseline of activity, after the cycle peaked in Q4 2021 along with the prices. Some of the activity also moved onto Layer-2 solutions like the Lightning Network, also explaining the fall in fees.

Lightning Network

The Lightning Network (LN) is a Layer-2 payment channel network anchored to the Bitcoin protocol. It intends to increase the network’s throughput while decreasing transaction settlement time. First introduced in 2015, Lightning’s scaling approach has gained popularity over time and is now considered to be the de facto scaling solution for Bitcoin.

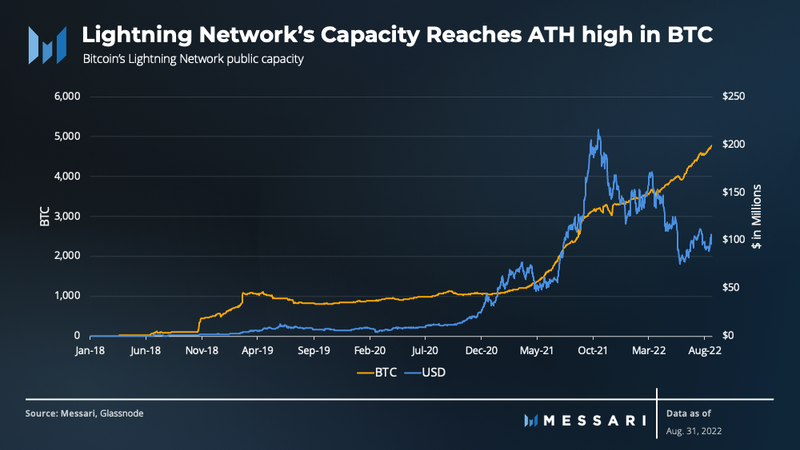

The LN has been in its own siloed bull market over the past year, insulated from the overall market downturn. As token prices fall, network usage and activity tend to follow. However, LN’s key metrics have steadily grown, despite bitcoin’s price dropping 57% over the past year.

Additionally, Lightning’s adoption increased as the technical foundation of the network reached maturity. Additionally, many companies have built the tools and services needed for Bitcoin and LN to reach mainstream adoption. Voltage, for example, provides easy-to-use hosting services for Bitcoin and Lightning nodes on the cloud.

The bitcoin capacity held in public channels on the LN reached a new high of 4,618 bitcoin valued at $93 million. The combination of the increase in adoption and integrations led to capacity drastically increasing by 96% in the past year. Some of the companies that adopted Lightning in 2022 are Cash App, Kraken, BitPay, and Robinhood.

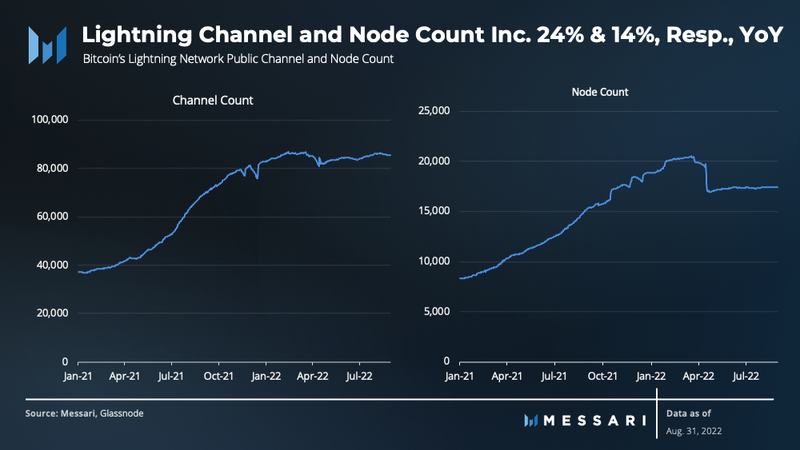

Lightning channel and node counts have also grown steadily, increasing 24% and 14% YoY, respectively. This growth indicates that the LN is moving away from a hobbyist network towards being a mature financial payment network.

Mining

2021 was an exceptional year for Bitcoin miners. Virtually all mining operations became profitable as Bitcoin’s price rose faster than the network’s hashrate. During the 2021 bull market, many mining companies took advantage of rising bitcoin prices by raising capital through the issuance of new equity and debt in order to grow their operations. Public mining stocks exploded upwards alongside Bitcoin. However, the broader macro environment caused the euphoria to come to an abrupt halt in 2022.

The biggest expense for Bitcoin miners is their cost of energy. Just this year, energy prices across the United States increased 15% YoY. With energy prices rising globally, many miners found themselves under pressure, especially those without power purchase agreements (PPAs) in place.

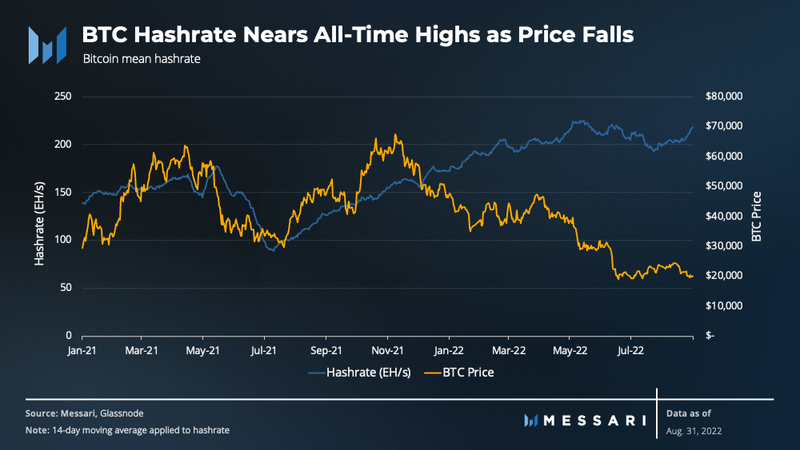

Going into 2022, there was roughly $5 billion worth of outstanding ASIC purchase orders set to be delivered to public miners. As bitcoin’s price trended downwards, miners were plugging in new ASICs as they arrived in order to begin getting paid back. This pushed the network’s hashrate and difficulty upwards. As hashrate and energy prices increased while bitcoin price decreased, miners found themselves in an increasingly difficult position. Many public miners resorted to selling bitcoin to continue financing their operations and service their debts. Miner’s selling bitcoin instead of HODLing added to the downward price pressure.

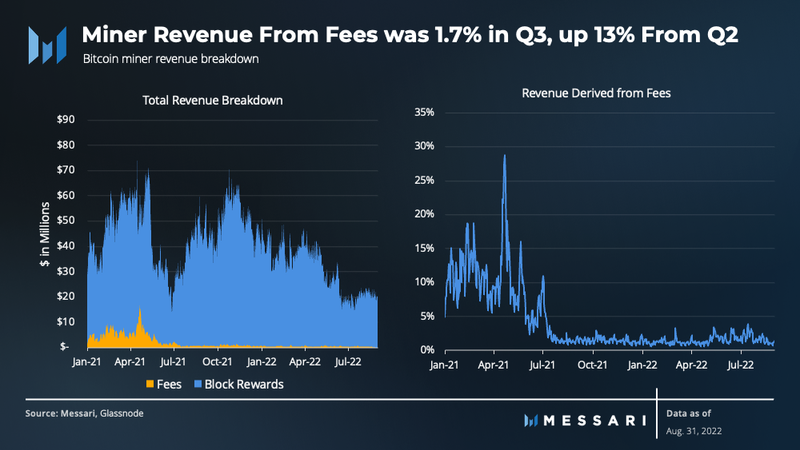

Miner Revenue

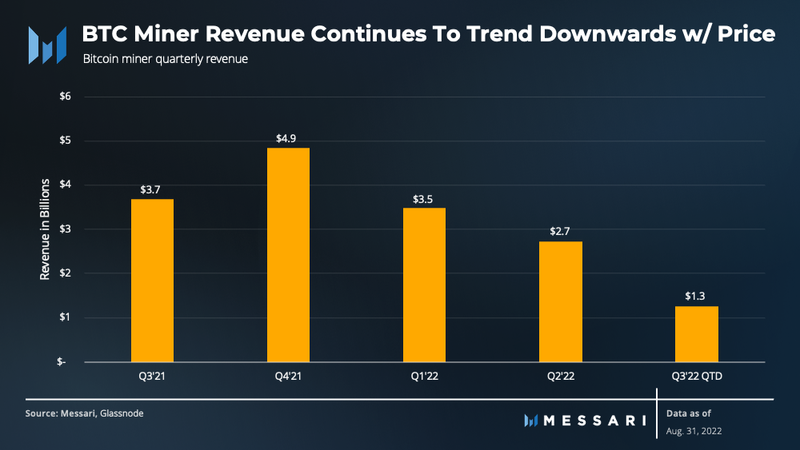

Miners have two sources of revenue: block rewards and transaction fees. Their revenue is determined by bitcoin’s price and demand for Bitcoin blockspace. In Q4 2021, miner revenue peaked at $4.8 billion, but it has been declining alongside the price of bitcoin ever since. Quarterly revenue for miners in Q1 2022 and Q2 2022 declined 28% and 22%, respectively. In the event that Bitcoin’s price remains range bound through the end of Q3, quarterly miner revenue will likely continue the downward trend given the high energy prices.

Bitcoin’s block rewards make up the majority of miner revenue. This quarter, total miner revenue derived from fees was 1.7%. Although the fee level is up 0.1% from last quarter, it is significantly lower than the fees miners earned during the 2021 bull market. Currently, low fees are not a big issue because miners are more incentivized by block subsidies than fees to secure the network. However, Bitcoin’s long-term security could be at risk if these low fees persist as the block subsidy approaches zero.

Hashrate

In May 2021, China’s ban on Bitcoin mining resulted in a 50% rapid decline in hashrate. Two months later, hashrate began to increase after mining machines exported from China were turned back on. By December, the network’s hashrate had completely recovered to pre-May levels.

In June 2022, hashrate began declining as energy prices continued increasing, leading some miners to unplug their machines. Due to the continued delivery of ASICs to miners who ordered them back in 2021, the hashrate is now near its all-time-high. As hashrate increases during a declining bitcoin price period, miners may be forced to divert from their HODL strategy and sell bitcoin held on their balance sheet.

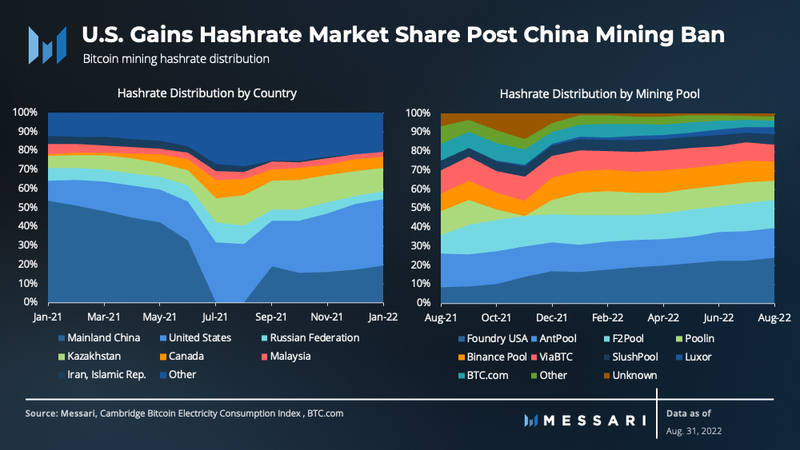

Although China’s mining ban negatively impacted Bitcoin’s hashrate and price initially, it ended up benefiting the network. Prior to the ban, Chinese miners had the dominant portion of the network’s hashrate on a country-by-country basis. After the ban, Chinese mining operations migrated to countries like the U.S., Kazakhstan, and Canada where there was less regulatory uncertainty. As a result, the Bitcoin network became more decentralized and resilient, avoiding the geopolitical risk of one country having an outsized portion of the hashrate.

The U.S. total hashrate increased from 16% in May 2021 to 38% in January 2022. U.S. mining pools also benefited from China’s mining ban, with Foundry USA becoming the largest pool. As of August 31, 2022, the Foundry USA pool has 24% of the network’s hashrate, up 180% YoY.

Energy Consumption

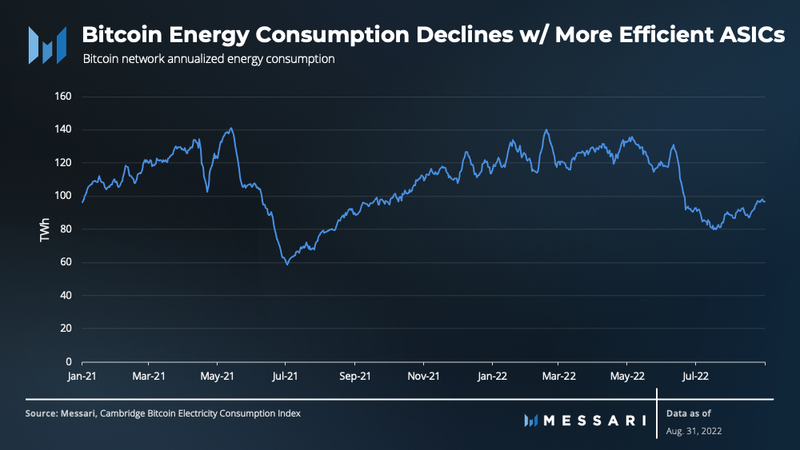

It is nearly impossible to determine the exact electricity consumption of the Bitcoin network due to its decentralized nature. The Cambridge Center for Alternative Finance (CCAF) uses a real-time model to estimate the Bitcoin network’s daily electric load within a hypothetical range.

Compared to Q2 2022, estimated energy consumption only increased 2% while hashrate increased 6% and reached a new all-time-high. The decoupling could be attributed to newer ASICs coming online, which are more energy efficient and have a higher hashing rate.

Sentiment Analysis

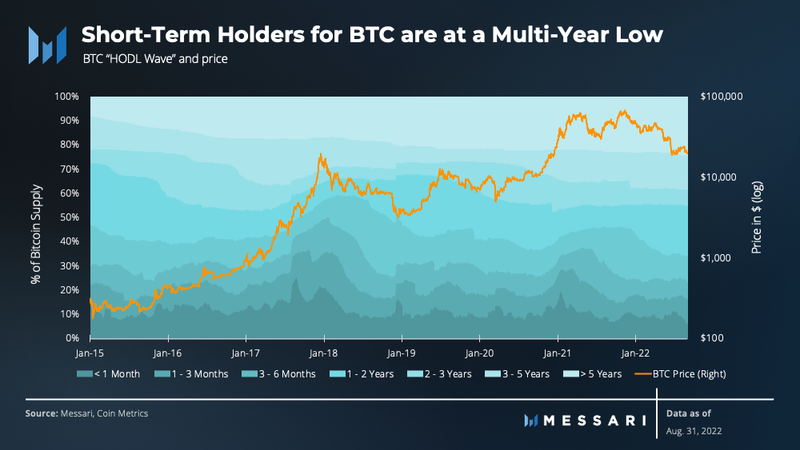

The HODL wave categorizes Bitcoin unspent transaction outputs (UTXOs) by when they last moved on-chain. Short-term holders (under 6 months) are at a multi-year low and own just 23% of the Bitcoin supply as of August 31. Over the last 7 years, Bitcoin’s short-term holders have bottomed six times, with the following year always yielding positive returns.

The number of short-term holders has historically been a leading indicator of bitcoin price peaks. As Bitcoin starts making new highs, it gets into the news cycle and attracts more buyers. However, the last peak in November 2021 did not attract new investors in the same way, perhaps due to macroenvironmental factors.

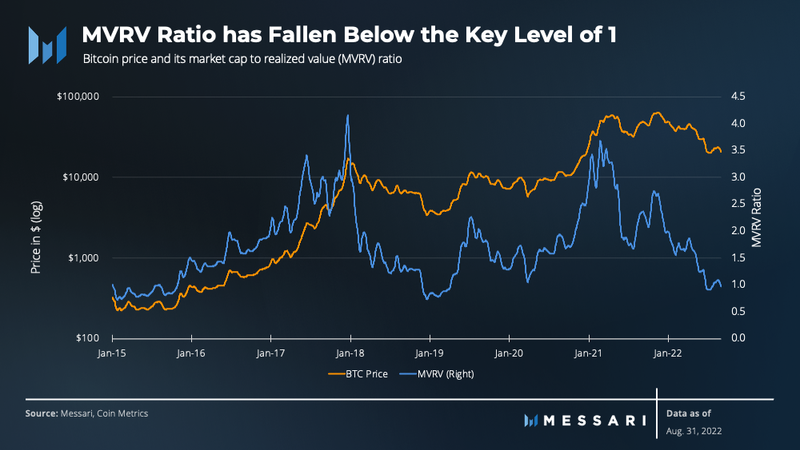

The market cap to realized value ratio (MVRV) compares the current market cap to the price of Bitcoin when they last moved for all circulating BTC. As such, it shows the cumulative degree of profitability of the holders.

At the end of August, the MVRV fell below the key level of 1, implying that holders are at a loss on aggregate. Disposition effect in behavioral finance suggests that investors hold onto their loss-making investments in hopes of turning them into winners and therefore MVRV below 1 is a zone of accumulation for long-term investors.

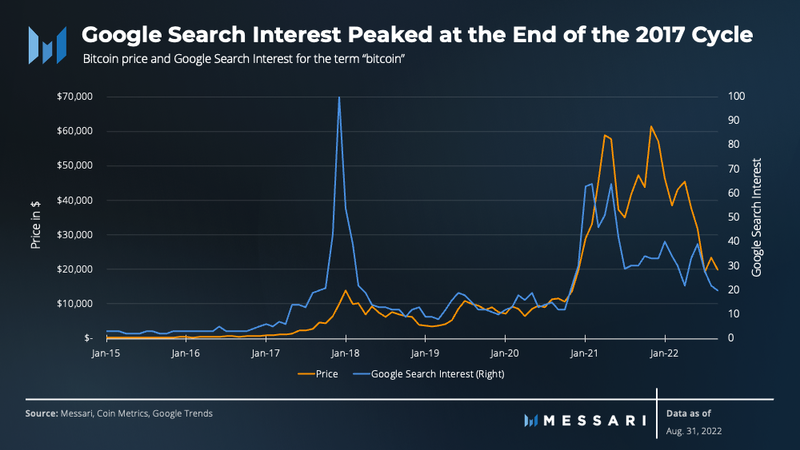

Google search trends help reinforce the idea that not many new entrants entered in the last cycle. Typically, the number of Google searches declines with the fall in BTC’s price. However, Bitcoin has had lower highs in searches since 2017. On top of that, the second bull run of 2021 had only half the search interest as the first. The decoupling between Google search trends and BTC’s price could indicate that fewer newcomers are entering the space.

Qualitative Analysis

Regulation

PoW

With rising energy prices and climate change becoming an increasingly important political issue, Bitcoin’s energy consumption and environmental impact have come under increased scrutiny. On September 8, 2022, the White House Office of Science and Technology Policy published a report on crypto mining’s climate and energy implications in response to President Biden’s executive order. In general, the report raises concerns on how Proof-of-Work could hinder U.S. efforts to combat climate change and how energy-intensive mining could negatively affect electricity grid reliability and prices.

The report calls on several federal agencies to develop standards that minimize negative environmental impact and ensure energy reliability. If these measures prove ineffective, the report states that Congress and the Administration should explore limiting or eliminating PoW mining.

Despite the White House’s criticism of PoW mining, the report does mention how PoW mining can yield positive results for the climate through alternative mining operations. Additionally, the report states that PoW mining can accelerate the transition to a renewable grid by contributing to needed rapid demand-response services and providing additional revenue to renewable developers.

Texas has served as an excellent case study in validating both positive PoW impacts identified in the White House’s report, due to the state’s business-friendly stance towards mining. But not all states have been as friendly towards PoW mining as Texas. Back in June 2022, the New York Senate passed a bill placing a two-year moratorium on new PoW mining operations using fossil fuels. The bill has yet to be signed by New York’s governor, but it is expected to pass.

Outside of the U.S., the European Union has been working on its own set of regulations known as Markets in Crypto Assets (MiCA). Introduced in 2020, the legislation aimed to create legislation for governing crypto assets. The initial draft included a proposal to ban crypto services from using PoW-based cryptoassets. However, this proposal was voted down by lawmakers in March 2022. In June 2022, EU lawmakers and members finalized the regulatory framework after excluding the proposal to ban PoW mining.

Regulatory Oversight

Over the last several years, the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CTFC) have been at odds over who should have jurisdiction over the crypto industry. In August 2022, the Digital Commodities Consumer Protection Act was introduced to the U.S. Senate which would give the Commodity Futures Trading Commissions (CTFC) direct regulatory oversight over bitcoin’s and ether’s spot market.

Early in September 2022, Gary Gensler, Chairman of the SEC, signaled his support for handing the CTFC authority over non-security tokens such as bitcoin. The move potentially opens up the regulatory path for a Bitcoin spot ETF and the possibility of eliminating the problematic GBTC discount.

ESG

From an ESG perspective, Bitcoin mining appears to be troublesome. Bitcoin mining consumes a significant amount of energy and generates a carbon footprint approximately half that of the data center sector. However, as stated in the White House’s mining report, mining can, under the right circumstances, reduce greenhouse gas emissions and accelerate the transition to a renewable grid.

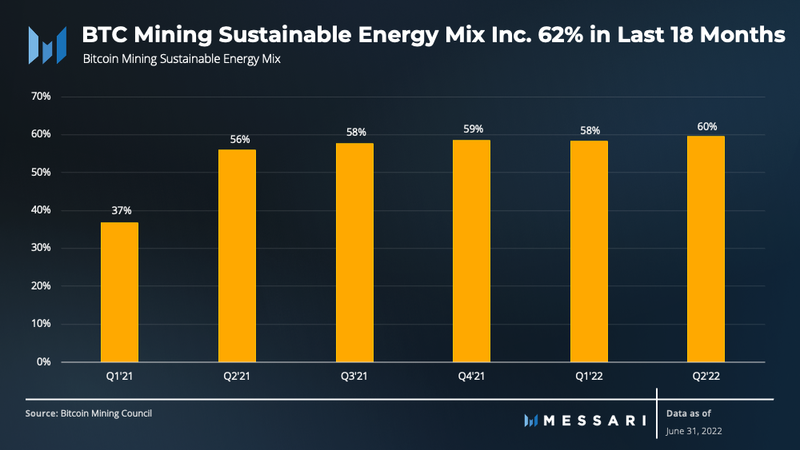

Even with the benefits observed from Bitcoin mining, the industry is still pushing towards a more sustainable energy mix. The Bitcoin Mining Council (BMC), a voluntary global forum of miners, has been working to bring transparency and best practices to the mining industry since June 2021. The BMC consists of 45 mining companies from five countries representing 50.5% of the Bitcoin network’s hashrate. In its Q2 report, the BMC reported that the global Bitcoin mining network had a 59.5% sustainable (carbon neutral) power mix. Compared to countries, Bitcoin has the largest sustainable power mix, with the runner up being Germany at 48.5%.

According to the BMC, the network’s sustainable power mix has increased 62% in the last 18 months due to increased reliance on renewable energy. BMC data, however, is under scrutiny as it is based on self-reporting by miners. To confirm the network’s progression toward more renewable energy, Daniel Batten performed an independent analysis using publicly available information. He found that in the past 18 months, there was a 10.9% minimum increase in the network’s sustainable energy mix, suggesting that the network is moving in the right direction.

Carbon-Negative Energy Sources

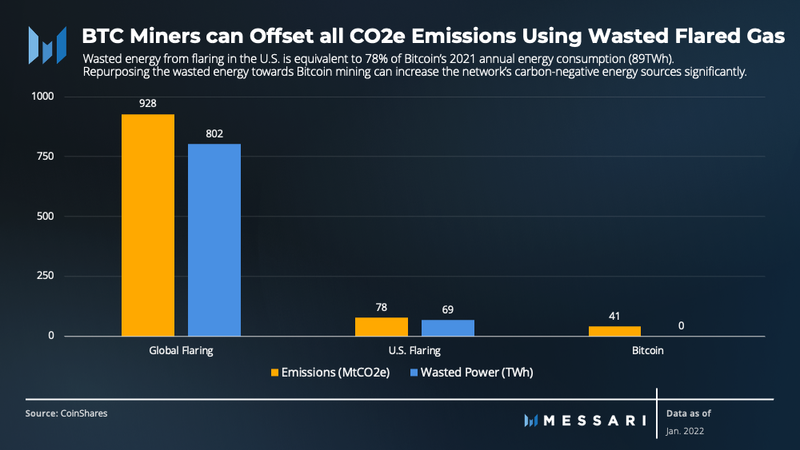

While the BMC quantifies the carbon-neutral portion of the network, it has not evaluated the carbon-negative power sources. Batten found that 2.36% of the network is powered by carbon-negative sources. Bitcoin miners use natural gas that would have otherwise been flared by the oil and gas industry. When Bitcoin miners combust the gas rather than it being released as methane into the atmosphere, they reduce the carbon dioxide equivalent (CO2e) emissions by 63%. As a result, the 2.36% of carbon-negative energy sources end up lowering the carbon-intensity of the network by 4.02%.

CoinShares estimates that 69 TWh of wasted power in the U.S. is lost annually to flaring, which results in a carbon footprint of 78 million tons of CO2e emissions. In other words, the wasted energy from flaring in the U.S. is equal to 78% of the energy used by the global Bitcoin network in 2021 (89 TWh). Repurposing flared energy towards Bitcoin mining would drastically reduce the amount of greenhouse gasses entering the atmosphere — enough to potentially offset all the network’s CO2e emissions or even make it carbon negative.

Protocol and Ecosystem Development

Bear markets are for building. Contrary to popular belief, there is a lot of development going on in the ecosystem:

- BIP-119 aims to give users more control over how bitcoin is spent.

- BIP-300 and 301 aim to expand Bitcoin’s functionality with opt-in sidechains without altering the base layer. The proposals could bring smart contracts to Bitcoin and provide a feasible way to sustain the protocol through transaction fees.

- Taro is a new Taproot-powered protocol introduced by Lightning Labs. It aims to bring stablecoins and other assets onto the Lightning Network.

- Lightning Pool and Magma have made it possible to generate yield on Bitcoin in a noncustodial way.

During the quarter, multiple developers left their roles maintaining Bitcoin Core. In July, Peter Wuille announced that he is scaling back his contributions. In August, Wladamir van der Laan, longest-serving Lead Maintainer for Bitcoin Core, announced his resignation.

Smart Contract Capability

Bitcoin’s functionality is limited by design to reduce the surface area for potential vulnerabilities. While Bitcoin does have smart contract capability, it is not Turing complete, meaning it doesn’t allow for logical loops. Instead of altering the Bitcoin base layer and sacrificing security for programmability, one option for bringing smart contracts to Bitcoin is using a Layer-1 blockchain with a native bridge to Bitcoin.

Stacks is a Layer-1 blockchain that enables developers to write smart contracts that benefit from Bitcoin’s security. It uses Clarity, a decidable programming language, to read and react to Bitcoin’s blockchain. Stacks uses a novel consensus mechanism known as proof-of-transfer (PoX) to secure its blockchain. PoX recycles Bitcoin’s PoW, allowing it to benefit from its decentralization without any additional environmental impact.

Key Events

July

- Tesla sells 75% of the bitcoin on its balance sheet at a loss.

- The Virtual Currency Tax Fairness Act is introduced, aiming to make bitcoin transactions up to $50 tax exempt.

August

- BlackRock launches a spot bitcoin private trust for institutionals clients.

- New York Digital Investment Group (NYDIG) announces a Lightning accelerator project geared towards developers working on Lightning, Taro, and covenants.

- Iran passes legislation establishing a framework for bitcoin to be used as payment for imports.

September

- Fidelity Investments plans to allow individual investors to trade bitcoin on its brokerage platform.

- Russia’s Ministry of Finance and the Bank of Russia have reconsidered their position towards cryptoassets and acknowledge that it is necessary to legalize them for cross-border settlements.

- MicroStrategy files with the SEC to sell up to $500 million in stock to buy more bitcoin.

Closing Summary

During Q3’22, several Bitcoin narratives failed to hold up. Over the year, BTC wasn’t a hedge against inflation or a store of value. Additionally, on-chain metrics showed a slow down in transactions, new users, and active users. However, development activity and usage in off-chain Bitcoin ecosystems such as Lightning and Stacks significantly increased.

On the mining front, a dark cloud looms over the industry as energy prices and inflation continue to increase in the low-liquidity macroenvironment. In addition, with hashrate hitting all-time-highs and the bitcoin price struggling to stay above $20,000, miner revenues are approaching unprofitable levels. If bitcoin’s price remains range bound or declines further, some miners and companies will be forced to sell additional bitcoin to service debt payments and operational expenses.

With that said, Bitcoin has survived much worse throughout its history. Eventually, new narratives are likely to emerge to replace the old ones. Developers are building to bring new functionality to the protocol and smart contracts to Bitcoin. Bitcoin mining could also become a way to fight climate change by reducing emissions and strengthening the grid. With how unpredictable Bitcoin can be, it’s possible that the next cycle could be driven by the narrative of bitcoin as an ESG asset.