Key Insights

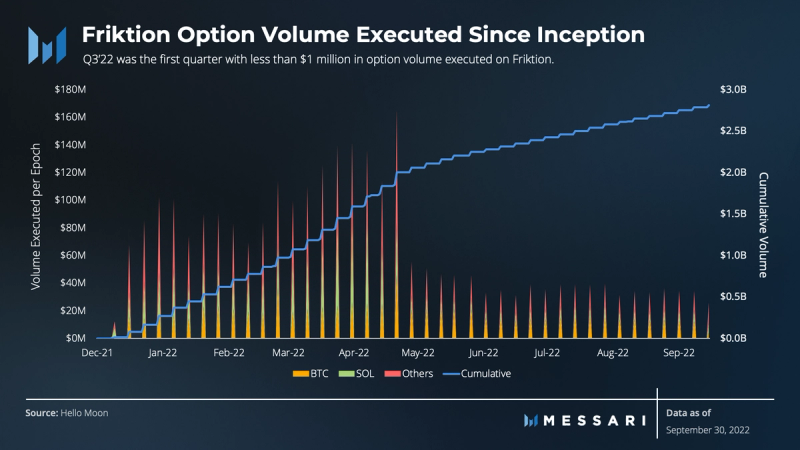

- Friktion has now executed nearly $3 billion in options volume from its platform, including the largest on-chain option strategies for BTC, SOL, and SRM again in Q3’22.

- Friktion Institutional made inroads with integrations with Fireblocks, Copper, and Snowflake Safe, allowing users to access Volts straight from their custodial wallets/UI. Adding Volt #06 Institutional Credit should drive more usage.

- On average across strategies, Friktion’s Volts earned depositors a 4.6% quarterly return in Q3’22. Volt #02 Cash-Secured Puts was the biggest earner at 7.65%, benefiting from high implied volatility and an end to the market selloff.

- Volt #05 Capital Protection was launched in September to Lightning OG holders. It earns yield from Tulip and uses that to make buy volatility in certain market conditions.

A Primer on Friktion

Launched in December 2021, Friktion offers systematic portfolio management strategies (known as Volts) for on-chain assets. The protocol offers a balanced portfolio of investing tools for users – including bullish, bearish, long volatility, and short volatility strategies. Volts are segmented by strategy and by asset, totaling 24 options. The protocol currently offers a Covered Call Strategy (Volt #01), Cash-Secured Put Strategy (Volt #02), Crab Strategy (Volt #03), and Basis Strategy (Volt #04), and recently announced Volt #05: Capital Protection. Friktion’s products allow users to deposit an asset into a Volt that is locked on weekly epochs.

The key differentiating factors between Friktion and other systematic option strategies are its execution infrastructure and strike-selection process. Friktion utilizes an on-chain, gradual Dutch auction process (using Channel RFQ, the protocol’s novel liquidity platform). For strike selection, an algorithm identifies the optimal strike range and timing for the protocol. The key factor is flexibility – in cases where implied volatility levels are meaningfully below recent realized volatility the auction can be delayed. This is both an advantage and disadvantage, depending on user preferences. Friktion has 20+ market makers on Channel, with typically five to seven winning trades each epoch.

Friktion is native to Solana but allows for multichain deposits from Ethereum and Avalanche.

Introduction

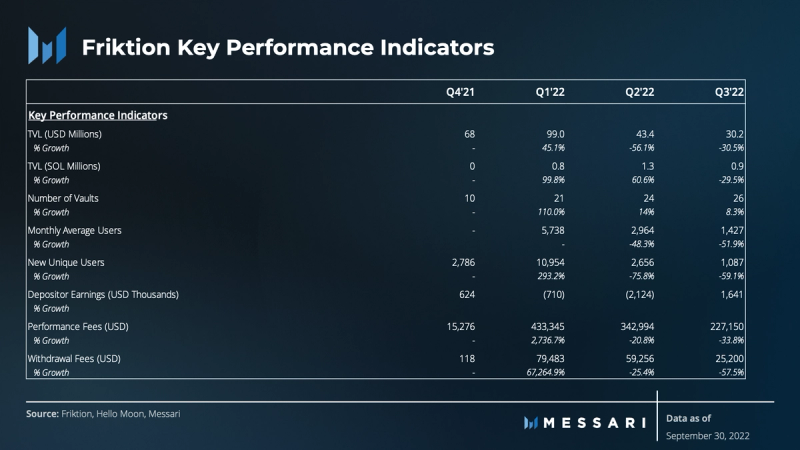

Friktion Volts returned to profitability in Q3, earning depositors a 4.66% return across the 4 strategies and 26 active vaults. Despite the fewer fee-paying monthly active users (MAUs) on Solana in Q3, Friktion attracted over 1,000 new users. In Q3, Friktion passed $1 million in lifetime fees collected, remaining aligned with its users as its earnings are 90% from performance fees, meaning Friktion only makes money when users do.

On September 2, Friktion Labs launched Volt #05: Capital Protection. Volt #05 accepts deposits in SOL or USDC. It uses Tulip, a Solana-native lending yield aggregator, to earn interest. With the interest earned, it buys a basket of options, giving the strategy long volatility exposure as well as directional upside. Volt #05 is unique in its capital protection characteristic, while still offering asymmetric upside from long volatility exposure. Though only open to Lightning OG holders currently, Volt #05 has already attracted nearly $300,000 in deposits.

The other big announcements of the quarter were institutional partnerships. Fireblocks, Copper, and Snowflake Safe are trusted names for large institutions with crypto exposure. Finding real yield in crypto is very difficult, differentiated from liquidity farming yield. Friktion offers a variety of systematic portfolio solutions for institutions to access, now through two of the largest custodians in the space. The next step is the launch of Volt #06: Institutional Credit. It will bring a new asset class to the Friktion portfolio and in a deep, liquid market. Friktion is designing an undercollateralized credit risk management system to enable depositors to safely fund borrowers.

Performance Analysis

As a proxy for the market, SOL daily volatility averaged 73% in Q3 versus over 100% in the previous quarter. Meanwhile, the average 7d implied volatility on SOL at-the-money options was 108. The spread between implied and realized existed across most major markets, helping make this a great quarter for volatility sellers to collect premiums. All four strategies were positive over the quarter, earnings depositors 4.66%, or 20% annualized, returns.

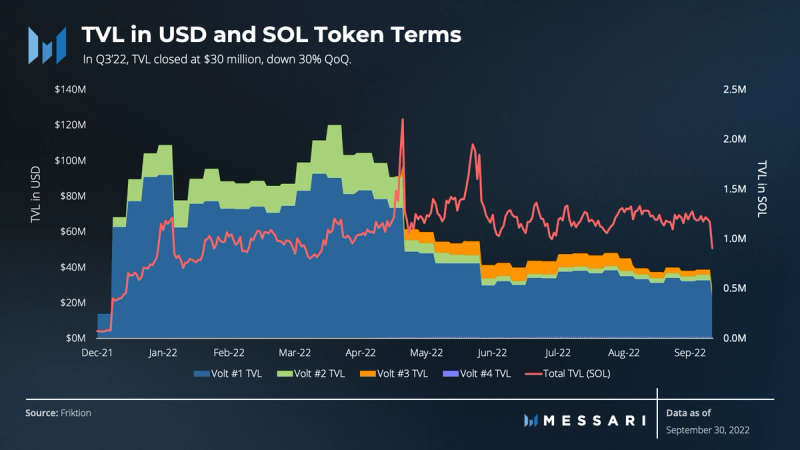

Despite strong performance across Volts in Q3, TVL fell 30% QoQ. The change is primarily a result of a big withdrawal from Volt #01 on September 30, depleting the BTC covered-call vault by over 70%. For most of the quarter, TVL was flat in the $40 million range.

Friktion continues to lead on-chain option execution in crypto with nearly $500,000 in options executed in Q3’22. A quarter of consistently lower prices was the primary driver of the 55% decrease in options volume from the $1.1 million executed in Q2. While BTC volumes only fell 37%, SOL volumes fell nearly 70% QoQ.

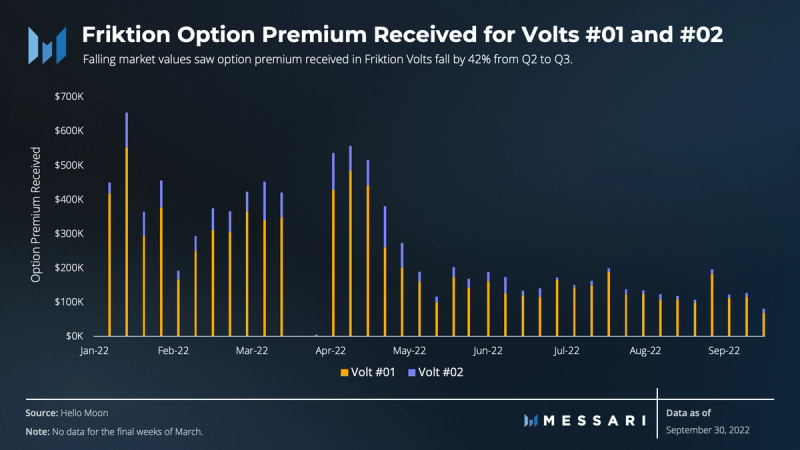

Premiums received in Volts #01 and #02 fell from $3.4 million in Q2’22 to $2 million in Q3. In dollar terms, most of the decline is from falling token prices impacting call premiums collected. Volt #01 received over $1 million less in premiums this quarter. Volt #02 premiums received fell 71%, which is only $400,000 as volt sizes shrunk dramatically in the selloff in Q2. Lower implied volatility levels also had a negative impact on premium sizes.

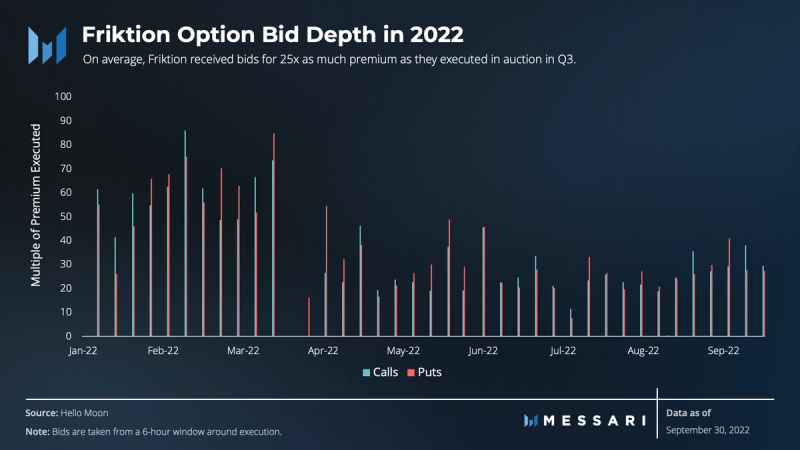

One of Friktion’s greatest strengths is its ability to source liquidity for its option vaults, including for underlying assets that don’t typically have deep liquidity. Friktion holds an auction to sell options for users in Volt #01 and #02, sourcing bids from many different counterparties. Based on the value of premiums bid for the options compared to the amount sold, Friktion had 25x more liquidity than required in Q3’22. When measured this way, falling depth could be a result of counterparties improving their capital efficiency or getting better at measuring the actual value of the options. The important takeaway is that even in a bear market, depth and liquidity for Volts #01 and #02 are robust.

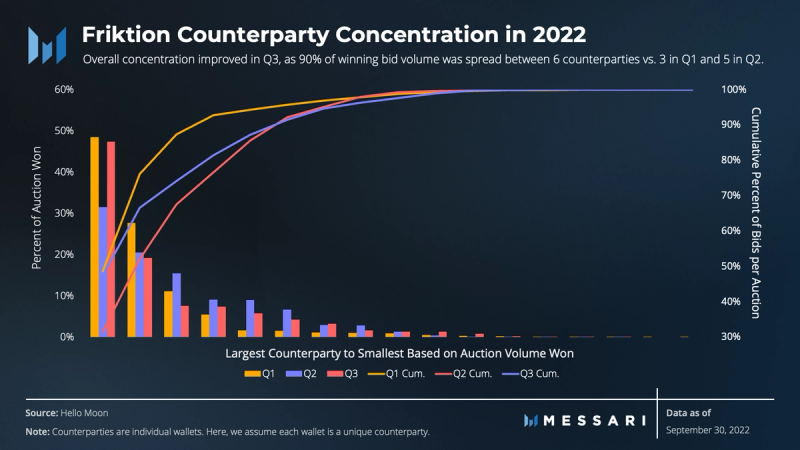

Over 35 wallets have placed winning bids in 2022 for Friktion. The concentration of winners has improved throughout the year. The largest counterparty made up 47% in Q3, but the right tail of winners was longer. The top six wallets accounted for 90% of winning volume, a broader outcome than five in Q2 and only three in Q1. Competitive auctions are essential for price discovery and best execution for Volt depositors.

Volt #01: Covered Calls

A covered call strategy is a yield-generation strategy for asset holders. Option premiums are collected from selling call options against their assets. However, the option seller forgoes the upside in exchange for collecting the premium yield. If the asset goes above the strike price, the holder will not participate in gains.

In Volt #01, users deposit tokens into the vault and lock them for weekly epochs (Friday to Friday). At the start of an epoch, Friktion sells an equal notional amount of one-week calls with strikes in the 5-10 delta range to maximize yield, while minimizing the chance of closing in-the-money. At the end of the epoch, the contracts are cash-settled.

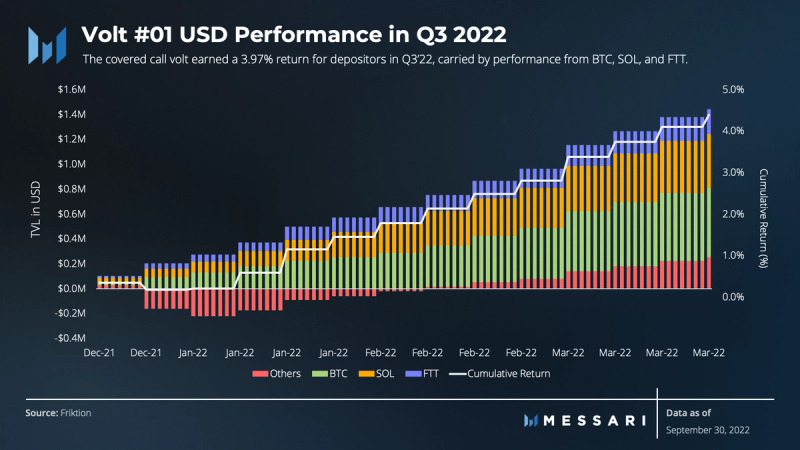

Volt #01 had another strong quarter for depositors. The strategy returned 3.97% for the quarter, annualizing a 17% yield.

BTC and SOL are the two largest vaults in the Covered Call strategy, averaging over $14 million and $7 million locked, respectively, over Q3. While prices fell, the number of BTC in the vault remained between 530 and 540, until the final epoch of the quarter. BTC in the volt fell over 70% on September 30, but SOL was largely unchanged.

Volt #01 again only had two epochs across underliers that experienced a negative return in the quarter (July 8 in SRM and July 15 in ETH, when ETH increased 25% in the epoch). Those losses were enough to make the quarterly return for depositors in ETH and SRM negative at -3.14% and -0.55%, respectively. The best-performing vault was again the SOL high-voltage vault, which offers depositors the option to increase risk and potential yield. It generated a 9.4% quarterly return for depositors.

Volt #02: Cash-Secured Puts

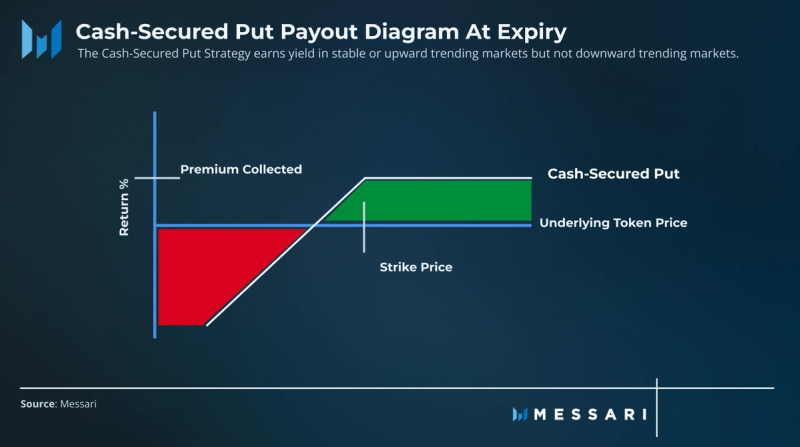

Similar to the covered call strategy, cash-secured puts are designed to generate yield for depositors by selling options. This results in a financial product that earns a positive yield in flat or upward markets and performs poorly in downward markets like the one experienced this past quarter.

Similar to Volt #01, Volt #02 users deposit USDC for an epoch, and Friktion sells one-week puts in the 5-10 delta range. European-style puts give holders the right to sell an underlier at a certain price on expiration. At the end of the epoch, the contracts are cash-settled.

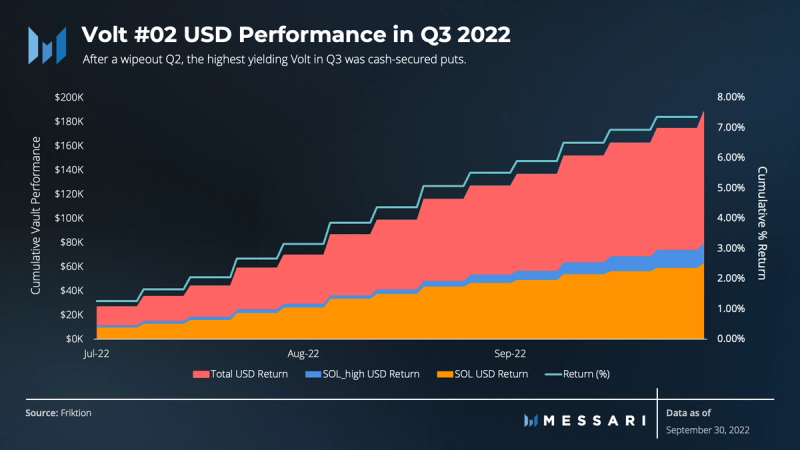

After falling almost 90% in Q2, TVL in Volt #02 increased 20% in Q3 to $2.6 million. The increase is credited to both new deposits (68%) and returns (32%). High implied volatility helped depositors in Volt #02 earn 7.65%, or a 34.3% annualized yield. The biggest contributors were the SOL and SOL high-voltage vaults, which made up 76% of the strategy’s return.

Volt #03: Crab Strategy

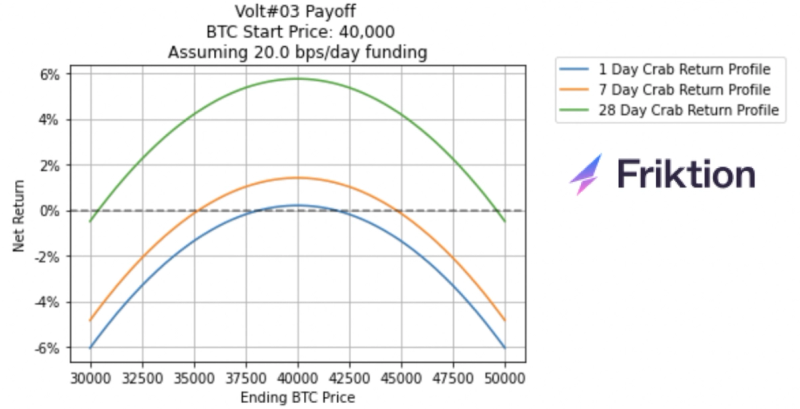

The Crab Strategy uses Power Perps. A power perp is an idea originally introduced by Paradigm and implemented by Friktion. Friktion Labs built Entropy, a central limit order book (CLOB) designed for exotic derivatives. Entropy creates a marketplace for volatility products. Power perps (e.g., BTC-squared) give holders asymmetric exposure to price moves. For example, the value of the power perp goes up more (21%) for a 10% move higher than it goes down (-19%) for a 10% move lower. This asymmetry does not come freely, of course. Funding rates on power perps reflect both leverage funding costs and the market’s risk premium to be short this convexity, and they are always positive.

The Crab Strategy sells a power-perp short and hedges the price (delta) risk with two long perps (short power-perp, long 2 perps). This isolates the convexity premium, creating a payoff similar to an options strategy that sells at-the-money options (called a straddle) while constantly hedging the delta risk. Higher funding rates on BTC^2 create a wider “profit range,” or BTC price range in which the strategy is profitable. Lower funding rates create a smaller “profit range.”

Source: Friktion Research

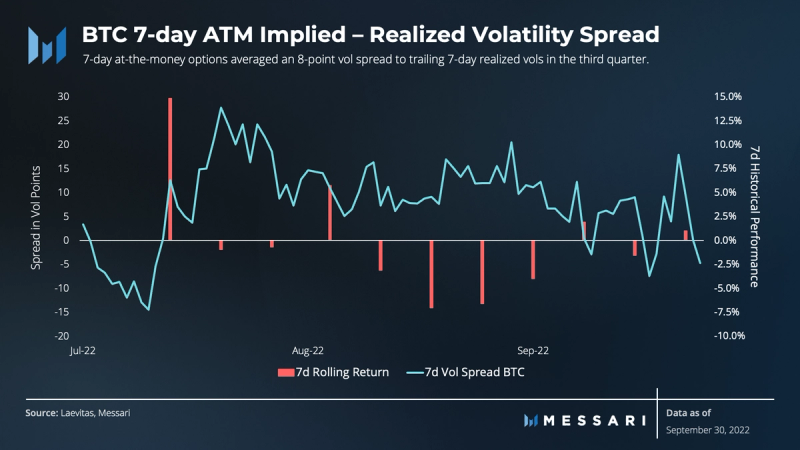

Volt #03’s performance is heavily impacted by the implied-realized volatility spread as the strategy attempts to profit by capturing the difference between the implied volatility it sells and pursuant realized volatility. BTC at-the-money seven-day implied volatility is used here to track the risk premium the Crab Strategy aims to collect. This is a conservative measure that understates the premium received due to volatility skew – it does not take into account that the implied volatility of strikes away-from-the-money typically has a higher implied volatility than at-the-money.

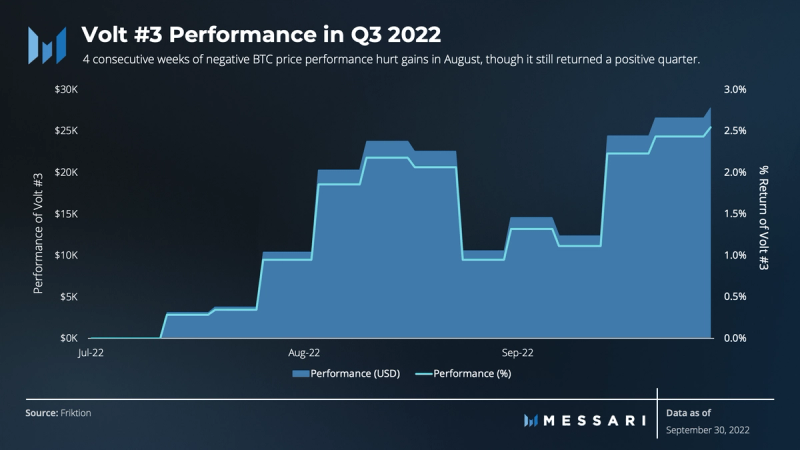

Uncertainty in markets has led to high volatility, and the average vol spread between the seven-day implied (at the money strike) and seven-day realized increased. Along with a high implied volatility, Volt #03 benefits from choppy rather than trending markets. Bitcoin is the only vault actively running this strategy today. The strategy has been at its $1.1 million capacity nearly every epoch this quarter.

In its first full quarter, Volt #03 earned depositors a 2.53% return (10.5% annualized). BTC fell for four straight weeks from August 10 to September 1. The consistent downward trend led to losses in Volt #03, as it benefits from choppy, directionless markets. Still, volatility premiums were enough to offset the bad stretch and earn a positive quarter.

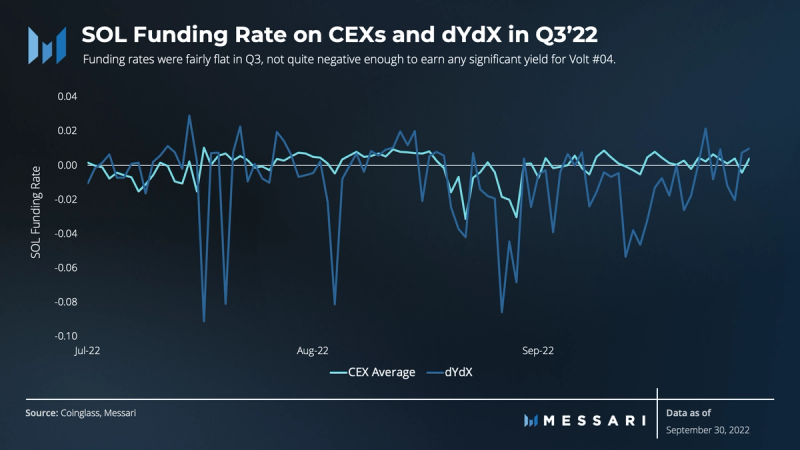

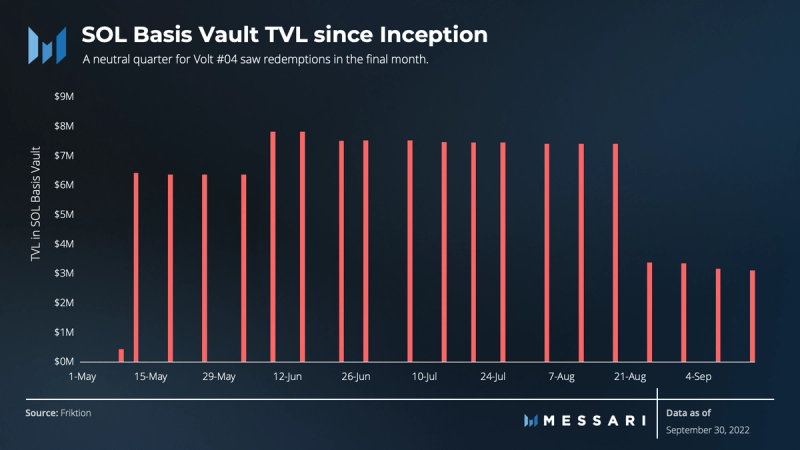

Volt #04: Basis Yield

Using perpetual futures, the basis strategy is another way for cash holders to generate yield. Users deposit stablecoins into one of the currently live vaults: BTC and SOL. The strategy is to long perpetuals and hedge the price (delta) exposure by shorting the spot of the underlying token. Therefore, returns for the strategy are dependent on directional demand for leverage.

The basis strategy is profitable in markets where the perpetual funding fee is driven negative by demand for short-side leverage. This happens when short-side leverage outweighs leverage demand from the long-side. While the strategy profits from a negative funding rate, the opposite holds true when the funding rate flips positive. Historically, funding rates have been positive due to excessive long demand. However, with the recent bear market, this has shifted. Funding rates are now on average negative and thus earning yield for Volt #4 depositors.

Performance in both the SOL and BTC vaults was flat again this quarter. Through two quarters, Volt #04 has yet to generate meaningful returns for depositors. The SOL vault likely benefits from a structural seller of SOL perps in UXD, but the demand has not driven borrowing rates low enough to earn significant yield using this strategy, yet.

Revenue

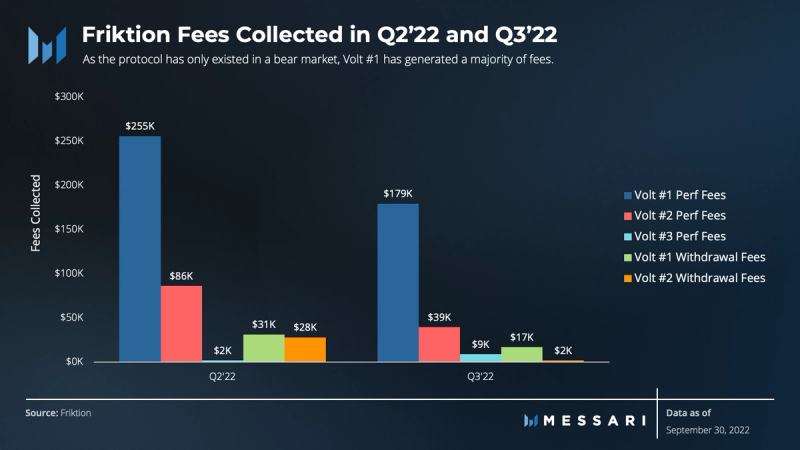

Friktion earns fees in the form of a one-time withdrawal fee and a per-epoch performance fee, only during Epochs with positive net returns. Currently, withdrawal fees are 0.1% and performance fees are 10% for Volts #01-03. Volt #04 has a 1% withdrawal fee and the same performance fee.

As of September 30, 2022, Friktion has now earned over $1.2 million in fees in its first nine months. The protocol earned $265,000 in Q3, 90% from performance fees.

Qualitative Analysis

Institutional Offering and Fireblocks Partnerships

Friktion has built the leading suite of portfolio management products on the Solana blockchain. Their next growth phase emphasizes onboarding institutions to the Friktion platform and associated products. Specifically, the new Friktion Institutional division is “focused on scaling their DeFi product offering to Treasuries, DAOs, and Asset managers.”

To that end, in the final week of August, Friktion announced two big partnerships in the institutional wallet and custody space. Snowflake Safe is a multisig wallet platform on Solana, which is now integrated with Friktion. On August 30, Friktion and Fireblocks announced a partnership. With over 1300 institutional accounts, Fireblocks is a behemoth in crypto’s wallet and custodian space. Using the Wallet V2.0, Fireblocks users can directly access Friktion’s suite of portfolio solutions.

Friktion Institutional will focus on offering these new users with real yields in DeFi. One of the biggest headwinds is liquidity, as its products are limited by general crypto adoption. An earlier partnership with Paradigm, an “Institutional Liquidity Network for Crypto Derivatives Traders,” should help there. Lastly, the expected launch of Volt #06 Institutional Credit this year will provide another avenue for yield in a deeper market.

Portfolio Manager UI

Historically, the term full-stack hasn’t been used to describe portfolio management solutions. However, Friktion is building tools to define the category. The process has focused on Volts; these automated solutions are able to collect different types of market risk premia. Along with new tools, better execution is a key part of that process, too. This quarter, Friktion launched a novel Portfolio Manager to add to its quiver.

DeFi, and crypto in general, has so far failed to provide transparency and a good UI to articulate transactions and sources of yield/return. Portfolio Manager by Friktion can be connected to a user’s wallet or linked to any wallet address. It displays the wallet’s participation in different volts and the value changes driven by those volts. The UI breaks down exposure to each volt, along with respective activity/transactions.

Part of a holistic, full-stack portfolio management solution includes tracking and deriving the source of changes in the value of a portfolio. With the launch of this new product for its users, Friktion continues to lead in UI/UX development.

Source: Friktion Labs

Closing Summary

The Friktion portfolio solutions stack continued to execute for users in Q3’22. All strategies were profitable in the quarter, while the cash-secured put Volt benefited the most from high implied volatility in a trendless quarter. Friktion Labs continues to add strategies for users, launching Volt #05: Capital Protection for Lightning OG holders in September. This should be more broadly open later in 2022. Since the portfolio solutions are now battle-tested, Friktion announced important integrations and partnerships to bring its solutions to institutional users of DeFi. The protocol continues to execute, and the team continues to innovate entering Q4.

______________________________________________________________________

Let us know what you loved about the report, what may be missing, or share any other feedback by filling out this short form. All responses are subject to our Privacy Policy and Terms of Service.

This report was commissioned by Friktion Labs, a member of Protocol Services. All content was produced independently by the author(s) and any opinion, estimate, or probability does not necessarily reflect the opinions of Messari, Inc. or the organization that requested the report. Paid membership in Protocol Services does not influence editorial decisions or content. Crypto projects may commission independent research through Protocol Services. For more details or to join the program, contact ps@messari.io. Author(s) may hold cryptocurrencies named in this report, and each author is subject to Messari’s Code of Conduct and Insider Trading Policy. Additionally, employees are required to disclose their holdings, which are updated monthly and published here. This report is meant for informational purposes only and should not be relied upon. This report is neither financial nor investment advice. You should conduct your own research, and consult an independent financial, tax, or legal advisor before making any investment decisions. Nothing contained in this report is a recommendation or suggestion, directly or indirectly, to buy, sell, make, or hold any investment, loan, commodity, or security, or to undertake any investment or trading strategy with respect to any investment, loan, commodity, security, or any issuer. This report should not be construed as an offer to sell or the solicitation of an offer to buy any security or commodity. Messari does not guarantee the sequence, accuracy, completeness, or timeliness of any information provided in this report. Please see our Terms of Service for more information.