Key Insights

- Fundamentals like a foundational user base, network stability, and improved transaction activity drove fundamental network value during Q3.

- Solana’s position in the NFT sector remained the second largest by secondary sales volume, behind Ethereum, and narrowed the gap.

- Strategies to boost GameFi are underway, and unique use cases like Helium are coming to the Solana network.

- Efforts to improve decentralization through greater geographic, hosting, and ownership distribution continue.

- The Slope mobile wallet hack and network outage were separate and isolated events that were not recurring.

- The ecosystem is positioned to continue growing with network upgrades, technical integrations, community building, and improved user accessibility.

Primer on Solana

Solana is a public, open-source blockchain that aims to deliver scalability and support smart contracts without sacrificing decentralization and security. It accomplishes this through a novel timestamp mechanism called Proof-of-History (PoH). Using PoH, the network can order and batch transactions before they’re processed through a Proof-of-Stake (PoS) mechanism. Additional design goals include sub-second settlement times, low transaction costs, and support for all LLVM-compatible smart contract languages, including Rust, C, C++, and eventually Move.

The Third Quarter Narrative

Despite the market headwinds during Q2, Solana continued implementing solutions to expand its ecosystem and improve network reliability. To improve network reliability and reduce downtime during periods of congestion, core developers built out QUIC and a novel fee prioritization mechanism. The solutions were clearly working by the end of Q2 as degraded network performance stabilized. Additionally, the team implemented strategies to expand the ecosystem through the rollout of NFT marketplaces, progress toward EVM compatibility, advancement of Solana Pay, and Solana Mobile.

In Q3, the bear market highlighted the network’s fundamental user base and ability to advance its growth strategy. At the same time, more challenges arose. The Solana ecosystem suffered the Slope mobile wallet exploit in early Q3 and a network outage at the end of the quarter. Nonetheless, Solana’s mission toward adoption remains intact, as evidenced by further integrations, ecosystem expansion, and advancements in network functionality stemming from the Mainnet Beta V1.10 series. As a follow-up to the State of Solana Q2 2022 report, this report will dive into the quantitative performance over the quarter and the qualitative evidence that Solana is continuing to overcome challenges and progress through adverse market conditions.

*Subsequent events, such as the recent Mango Markets exploit, will be covered in the State of Solana Q4 2022 report.

Performance Analysis

Network and Financial Overview

During Q3, network and financial performance differed from Q2, despite a similar macroeconomic environment.

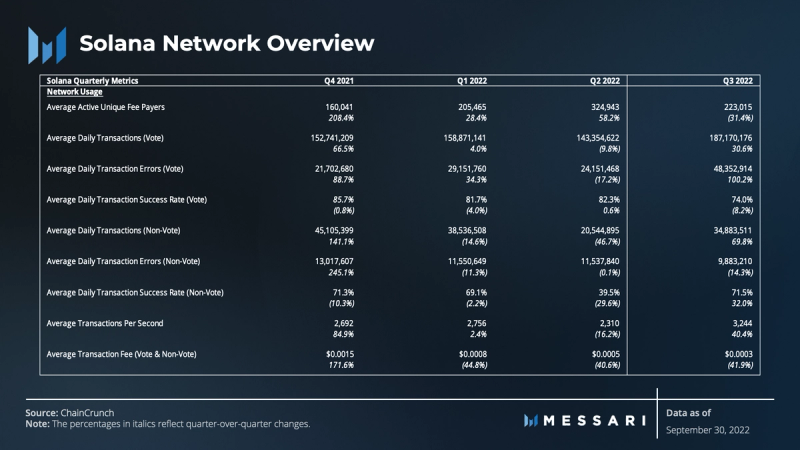

User activity, measured by Unique Fee Payers and Unique Signers, was down quarter-over-quarter (QoQ) while average daily transactions and transactions per second (TPS) increased. Both metrics experienced the reverse in Q2.

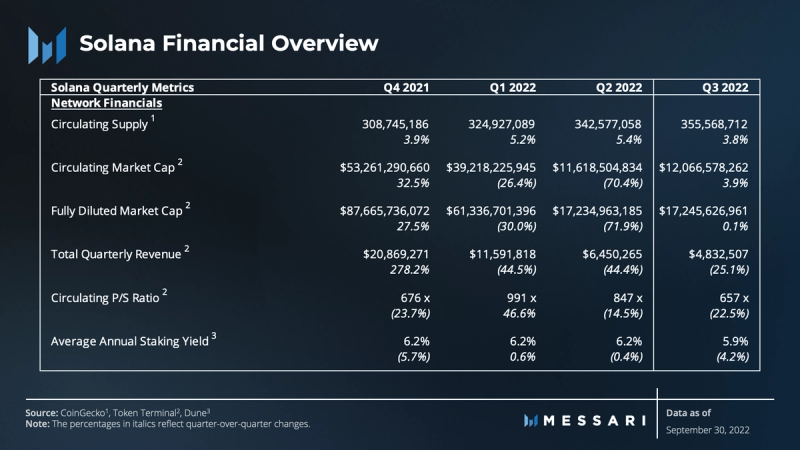

Revenue (-25%) and average transaction fees (-42%) continued to decrease in Q3. Revenue did not decline by as much as it did last quarter, while average transaction fees did.

Market cap (i.e., network value) remained stable despite the decline in revenue.

While performance behaved differently and changed directionally, the relationship between each measure reveals more about the network’s fundamentals.

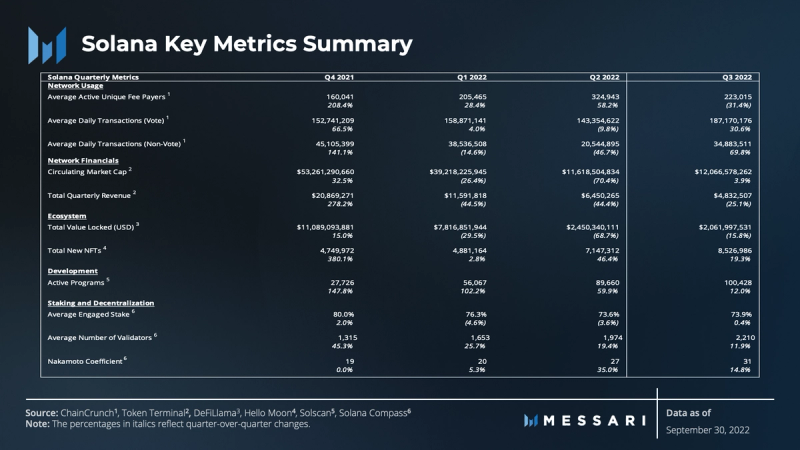

The daily Unique Fee Payers metric consists of the number of unique accounts that pay for at least one transaction per day. Despite market conditions during Q2, Unique Fee Payers continued an upward trend. However, the trend reversed course at the end of Q2 and stabilized during Q3.

Because some protocols use a single fee-payer account to cover the fees for their user base transactions, the Unique Fee Payers metric stated in absolute numbers may underestimate the number of unique wallets interacting with the Solana network. For that reason, tracking Unique Signers could be a more accurate way to gauge user activity.

Nonetheless, the trend of Unique Signers closely mirrored Unique Fee Payers over the quarter. It is unclear why user activity according to these metrics reversed course as activity across different sectors (NFTs, DeFi, GameFi, etc.) was mixed.

Considering the context of the bear market, these metrics could be revealing the fundamental and sustainable user base. For perspective, the average number of daily Unique Fee Payers over the nine months prior to Q3 was 230,000. Amid the crypto winter of Q3, the daily Unique Fee Payer metric reverted to the average, suggesting a foundational user base.

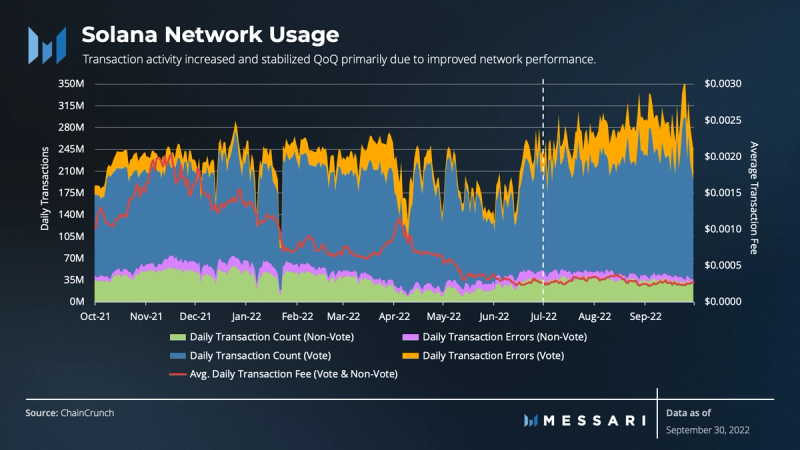

Transactions on Solana can be divided into consensus and non-consensus (token transfers and smart contract logic) transactions. Solana’s PoS mechanism is unlike other smart contract platforms because its consensus votes are registered as on-chain events. Non-vote transactions are analogous to EVM transaction counts. They represent the actual economic activity on the network. The sum of consensus and non-consensus transactions is considered total transactions.

Transaction activity on the network did not follow a similar pattern as daily Unique Fee Payers. Transaction activity increased (+70% QoQ in non-vote transactions), maintaining a steady quarter compared to the drastic volatility seen in the past. Further, TPS continued to reach all-time-highs, and average TPS (~3,200) improved by 40% QoQ. Transaction activity increased and stabilized QoQ primarily due to improved network performance rather than more users.

Previously, the main issue with network performance arose from Gulfstream, Solana’s alternative to the mempool for pending transactions. Gulfstream allowed bots to propose an arbitrary number of transactions. Because bots proposed so many transactions, the network experienced frequent congestion leading to degraded performance.

There were dozens of events recorded in prior quarters, ranging from network congestion to halts. In Q3, Solana continued to implement stages of the Mainnet Beta V1.10 series, and the fee prioritization mechanism went live, subsequently bringing more network stability. The network avoided degraded performance or network halts during Q3 except on September 30. This exception was unrelated to the previous sources of network degradation and will be highlighted later in this report.

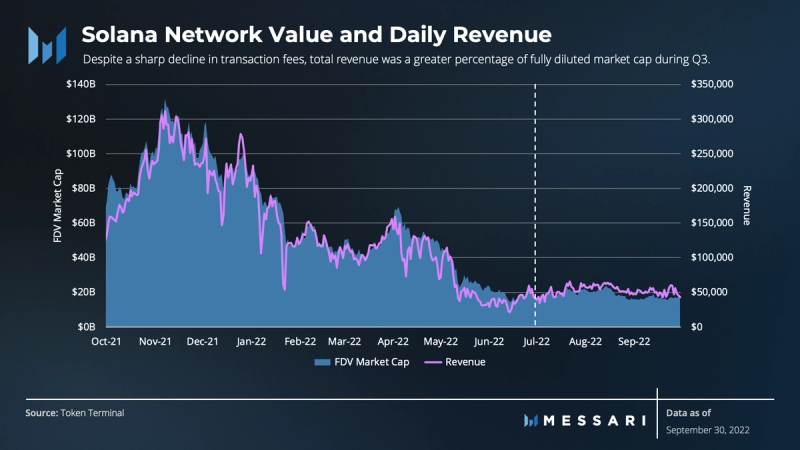

Having fee payers and stability in daily transactions drives revenue and value accrual to the network. Across crypto, network usage is becoming a more significant portion of network value. The question is how statistically significant the relationship between metrics like revenue and network value is and what’s contributing to it. Is network value driven predominantly by a greater number of users and transactions or changes in transaction fees? Ideally, more users and transactions, albeit lower transaction fees, drive revenue, and represent the fundamental value accrual. This outcome would be preferred compared to value coming from higher transaction fees or speculative value.

To that end, the correlation between revenue and network value continues as the volatility and trend of daily revenue are generally accompanied by movements in network value.

As seen in 2021 and throughout Q1 and Q2 of this year, degraded network performance decreased network transaction activity and reduced the network’s continued revenue flow. This put downward pressure on network value during that time. However, more stability was found after the implementation of V1.10. User activity through fee payers reverted to the longer-term average and stabilized during Q3, and transaction activity was more significant due to the improved network stability. The 40% decline in transaction fees combined with the 25% decline in revenue suggests that fundamentals like network stability, users, and transaction activity are what’s driving fundamental network value.

Despite the sharp decline in transaction fees, total revenue was a greater percentage of the fully diluted market cap during Q3 than ever before. From a valuation perspective, this relationship is also in line with the direction of the P/S ratio.

Ecosystem & Developer Overview

In sum, fundamentals like network performance, users, and transaction activity impact value accrual. The natural follow-up question would be what drives fundamental activity. This question can be answered by evaluating Solana’s ecosystem, developer engagement, and growth strategy.

DeFi

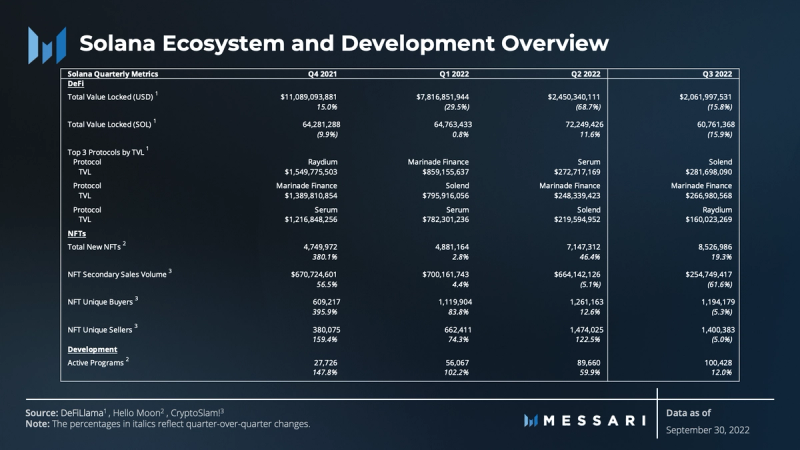

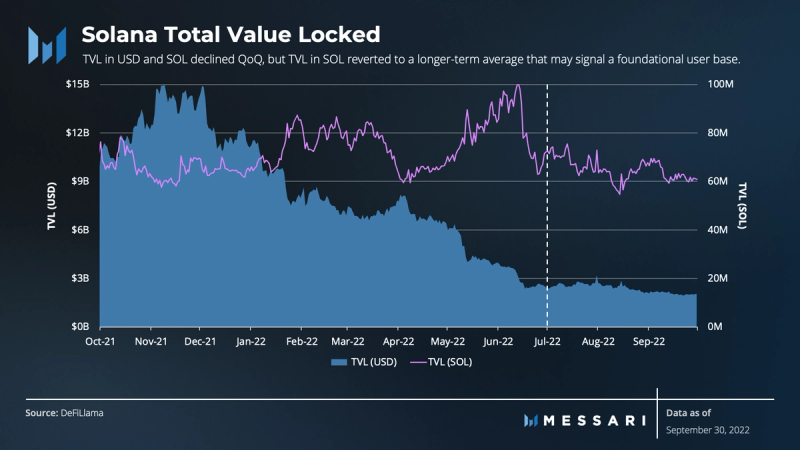

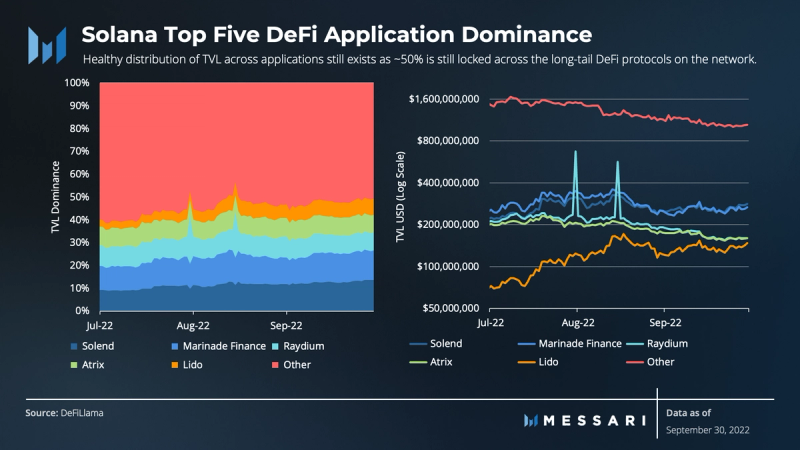

Like other Layer-1 networks, Solana’s Q3 TVL fell roughly 16% denominated in both USD and SOL QoQ. However, over the 12 months prior to Q3, the average amount of TVL denominated in SOL was ~65 million, which was the average during Q3. From this perspective, TVL in SOL stabilized in Q3. As TVL reverts to its mean, it may reflect sustainable utility rather than value catalyzed purely by price volatility, speculation, or DeFi incentives.

In prior quarters, there was a notable trend of long-tail DeFi protocols on Solana with at least $1 million in TVL. This led to over 80 protocols outside of the top five housing ~60% of the TVL across the Solana DeFi ecosystem. This trend and relationship shifted during Q3, with 50% of TVL spread across the longer-tail DeFi protocols, representing a -10% shift of TVL to the top five.

TVL grew most notably in Solend (28%), Marinade Finance (8%), and Lido (111%). However, the growth in liquid staking on Lido may have catalyzed the increase in TVL on Solend and Marinade Finance. Liquid staking allows stakers to use their staked assets on lending protocols like Solend.

Nonetheless, a healthy distribution of TVL across applications still exists on Solana. Currently, 50% of TVL is locked across most of the long-tail DeFi protocols on the network. The continued level of diversified TVL helps mitigate overall ecosystem risk. Some top networks by TVL have exposure to single applications with anywhere from 50-60% of the ecosystem’s TVL. In contrast, no single Solana application appears “too big to fail,” with Solana’s largest DeFi protocol, Solend, capturing only 14% of TVL at the end of Q3.

NFTs

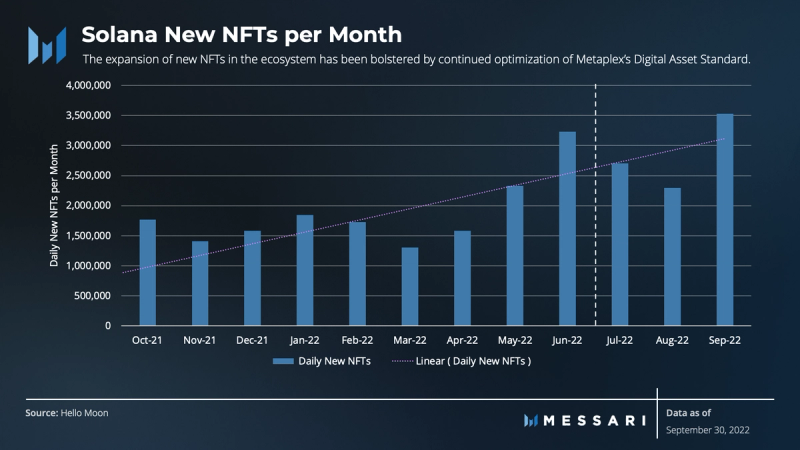

Unlike Solana’s DeFi sector that both decelerated and stabilized, its NFT ecosystem continued to grow. The total number of daily new NFTs increased to over 8 million, representing 19.3% growth QoQ. For perspective, this growth continued after increasing by 46.4% in Q2 and is ~8.5x the level minted a year ago.

Solana’s NFT ecosystem has been fueled by the continued optimization of Metaplex’s Digital Asset Standard, which is the foundational token standard for all NFTs on Solana. Metaplex continues to iterate on its popular, open-source minting solutions such as Candy Machine, recently announcing no-code solutions for less technical creators. Collectively, Solana and Metaplex have continued to offer creators a place to launch NFTs efficiently.

Metaplex’s announcement of compression for NFTs during Q3 will likely continue this trend. Compression will reduce the cost of on-chain storage of NFTs, enabling enterprise-level users like airlines and live events to store on-chain tickets and launch at a scale currently unavailable on Ethereum. Compression will allow as many as 1 million NFTs to be minted simultaneously for ~6 SOL ($204) and 100 million for ~50 SOL ($1,700).

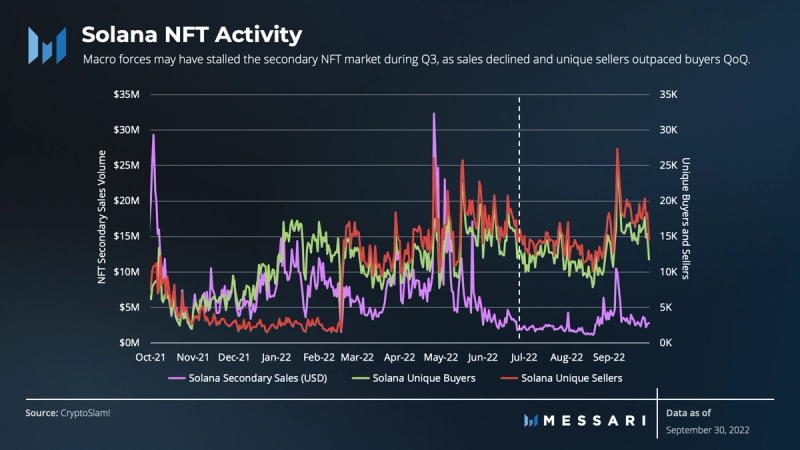

While daily new NFTs continued to accelerate, secondary sales volume declined 62% QoQ. Macro forces may have stalled the secondary market during Q3, as unique sellers outpaced buyers. For perspective, Q2’s secondary sales volume spiked and was largely supported by the rapid success of Magic Eden, OpenSea’s integration with Solana, and the adoption of Metaplex’s Collection Standard.

Nonetheless, sales volumes rebounded off the lows experienced at the end of Q2. The culmination of more streamlined NFT minting solutions, additional marketplaces, and enhanced user experience applications will likely grow the NFT ecosystem in future quarters. Phantom enabled users of its browser extension to list their NFTs on Magic Eden directly. Atomic Wallet rolled out support for Solana NFTs on its desktop and mobile versions. Solana NFTs also began to trade on additional NFT marketplaces such as Rarible. Further, Dust Labs announced a $7 million fundraising that included funds from Metaplex and Solana Ventures’ $150 million fund. Dust Labs is building value-add software to facilitate greater user access and experience for NFT communities.

Despite the bear market, Solana’s strategy and position in the NFT sector remain strong. Solana remains the second-largest network in terms of secondary sales volume, behind Ethereum, and is narrowing the gap.

GameFi

GameFi is clearly on the cusp of catalyzing a wave of activity across the crypto space. It is also clear that networks like Ethereum, Solana, Avalanche, and others are strategically moving towards growing GameFi ecosystems.

Solana Ventures’ $150 million fund to boost GameFi was underway heading into 2022. Additional investment funds have since joined in that effort, and Solana has gathered some traction in the gaming arena.

During Q3, gaming platforms like Eternal Dragons described the opportunity of gaming on Solana, pointing at Solana’s “speed, features, developer community, and carbon footprint.” Several other platforms seem to agree with Eternal Dragons’ reasoning.

For example, Magic Eden announced its launch of Magic Ventures, a fund focusing on investing in blockchain games and gaming infrastructure, and Ancient8, a significant developer of GameFi infrastructure, introduced Dojo, Solana’s first GameFi launchpad.

Unique Use Cases

A notable expansion of a unique use case beyond DeFi, NFTs, and GameFi came when Helium, the crypto-powered decentralized wireless network, proposed moving from its native blockchain to Solana. Through on-chain voting, the proposal passed, and as a result, Helium will move all of its operations onto the Solana blockchain.

Developer Activity

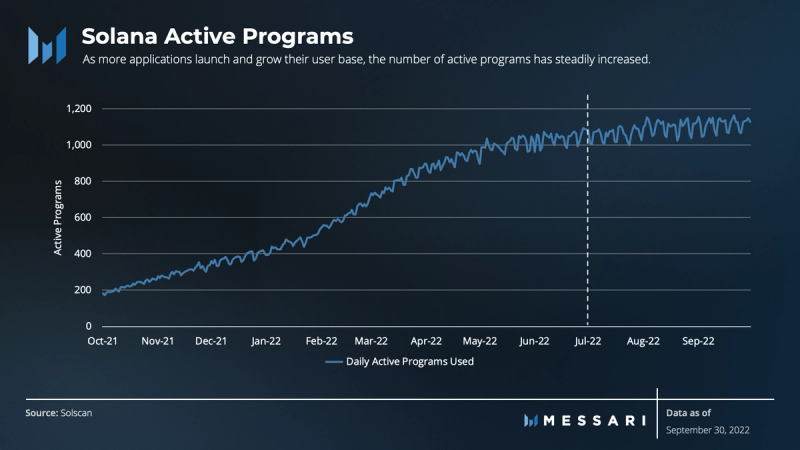

Active programs in a given period are another indicator of ecosystem development. The active program metric represents applications with at least one successful daily instruction based on a single program address. As more applications launch and grow their user base, the number of active programs has steadily increased.

In previous reports, core developer involvement was also measured by data sources tracking the events in the Solana Lab’s GitHub repository. The data indicates that core development has been volatile but growing modestly on average over the last several quarters.

However, the current data sources on developer data are imperfect as they exist today. Not all commits are created equal. Data sources work by primitively measuring GitHub events across different repos, resulting in an incomplete picture of core developer activity.

While there is evidence that core developers are contributing to the Solana infrastructure, future reports will aim to evaluate activity with more reliable data sources and methodology.

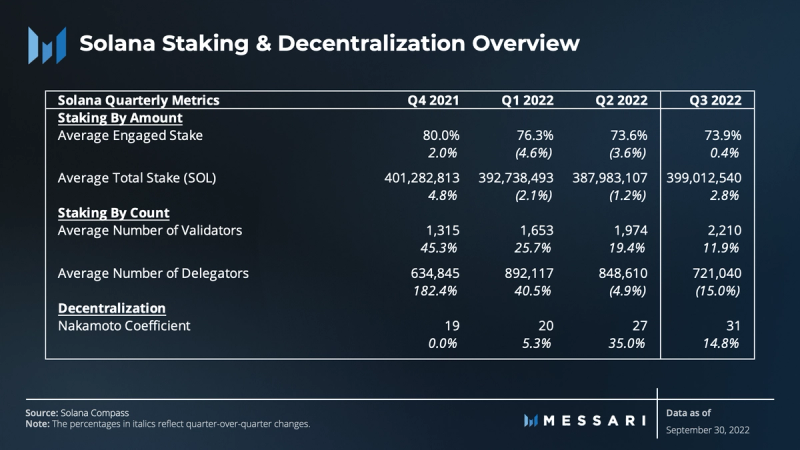

Staking and Decentralization Overview

Staking and decentralization of the network remain strong despite coming off a volatile Q2. The average engaged stake on Solana has held strong at ~75% over the last year. This stability mitigates network value volatility to some extent.

Staking amounts during Q3 were relatively uneventful, with average total stake growing by 2.8% QoQ.

The average number of delegators declined for the second consecutive quarter. Solana delegators are referred to as active stakers and are measured by the number of accounts that received staking rewards. Because most wallets only have one stake account, delegator count is a rough indication of the number of stakers.

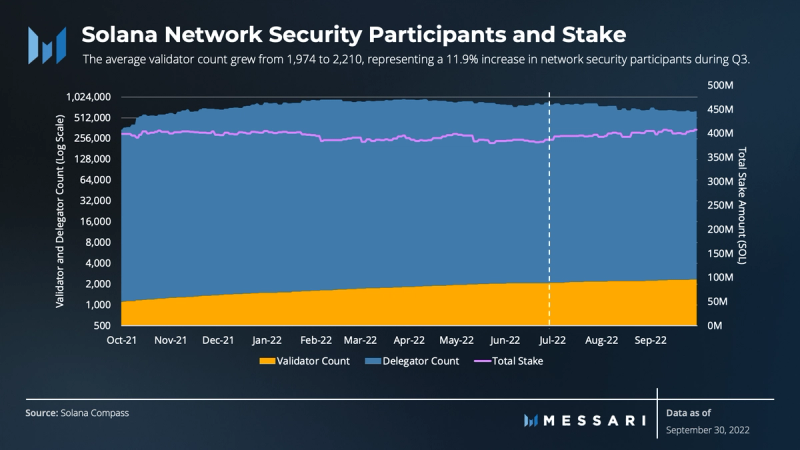

Every quarter since Q2 2021, Solana has maintained a double-digit percentage point increase in the average number of validators. The average validator count grew from 1,974 to 2,210 in Q3, representing an 11.9% increase in network security participants over the quarter.

Despite a decline in active stakers, the lack of volatility in the total stake amount, paired with an increase in validators, is a sign of a healthy PoS network.

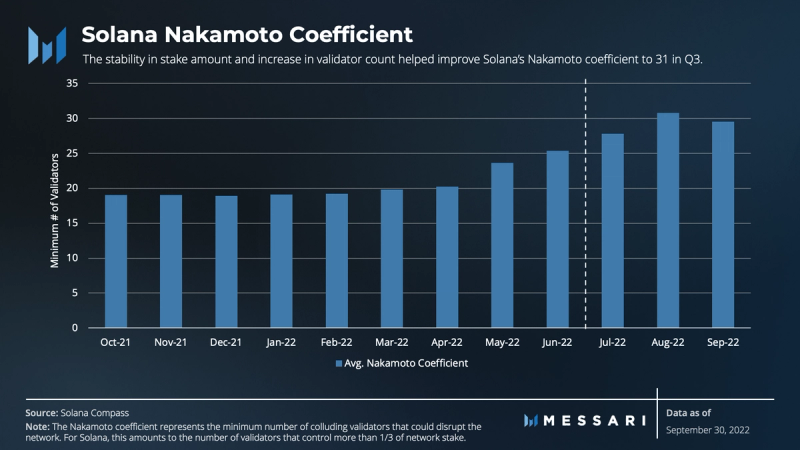

Solana’s Nakamoto coefficient hovered around the mid-teens throughout 2021. But because the stake amount remained stable while validator count increased, it improved to 27 in Q2 and 31 in Q3. The improvement continues to put Solana above the industry average compared to other Layer-1 networks.

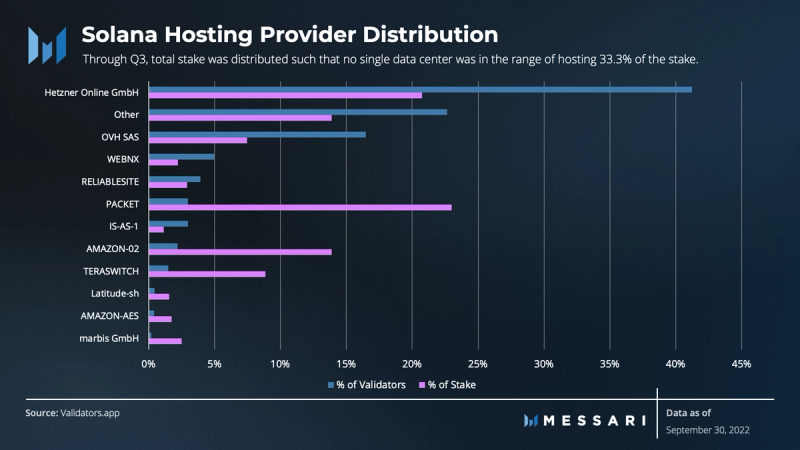

A network with a high Nakamoto coefficient and a growing number of validators is still vulnerable to external factors. The Solana Foundation extended beyond the Nakamoto coefficient to evaluate different aspects of decentralization and released a network health report during Q3. The other decentralization metrics include geographic diversity, data center ownership, and entity control over validators.

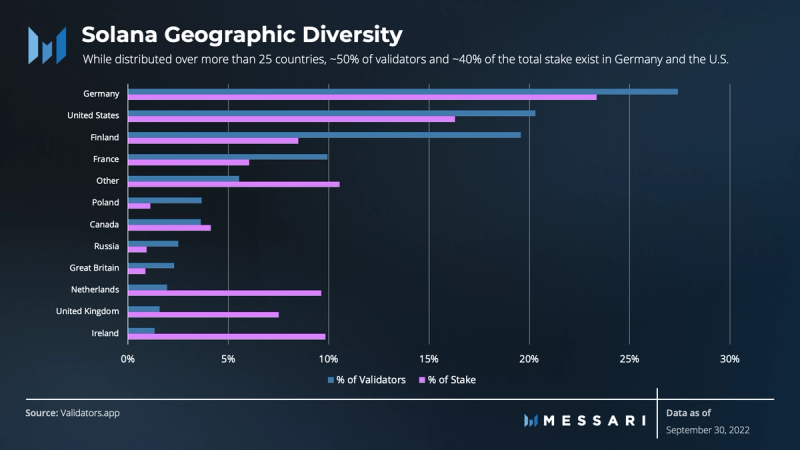

At the end of Q3, while distributed across more than 25 countries, ~50% of Solana validators and ~40% of the total stake were located in Germany and the U.S. Geographical concentration is typical for Layer-1 networks and is an area of concern Solana aims to address. Too many validators in the same location could jeopardize the health of a network due to geopolitical risks, regulations, and acts of nature, among other reasons.

Data center concentration is another area of concern regarding decentralization.

Using private data centers like AWS to run validators could give the owners of data centers disproportionate power over the network. However, through Q3, the total stake on Solana was distributed such that no single data center was in the range of hosting 33.3%.

Lastly, the concentration of validator ownership is another decentralization factor. It’s critical that no single entity owns all of the validators (whether hosted by a data center or not) and obtains majority control over the validator set. As of Q3, there were over 2,000 block-producing nodes on the Solana network. The Solana Foundation verified in their network health report that independent entities run ~88% of the validator set.

Competitive Analysis

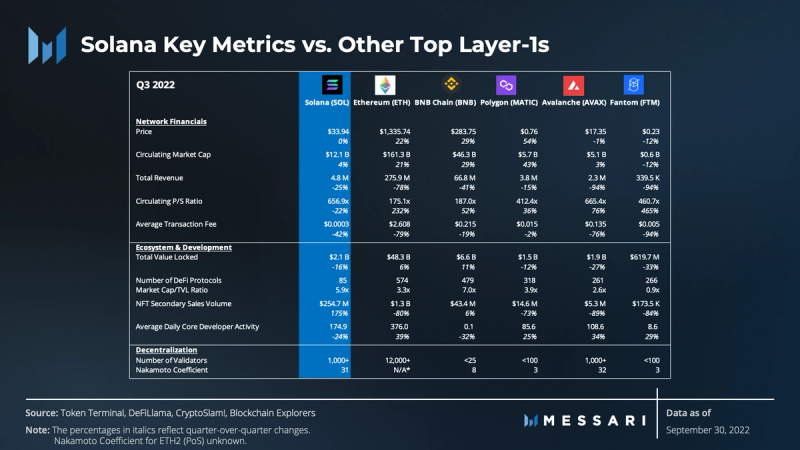

Solana has witnessed high growth since its inception, successfully maintaining its position as one of the most valuable Layer-1 networks. Here, we evaluate Solana’s progress versus the top five Layer-1s by TVL (including Solana) and those with the largest number of DeFi protocols. This peer group was derived by grouping the top five chains with the largest TVL and number of protocols.

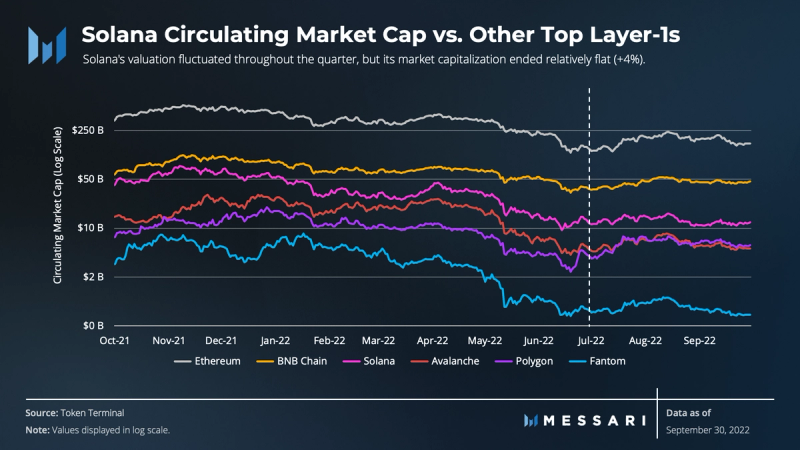

Solana’s valuation fluctuated throughout the quarter, but its market capitalization stayed relatively flat (+4%). Market cap dominance was regained by Ethereum, BNB Chain, and Polygon over the quarter as each experienced double-digit percentage point increases. In terms of value accrual, Fantom continued to struggle.

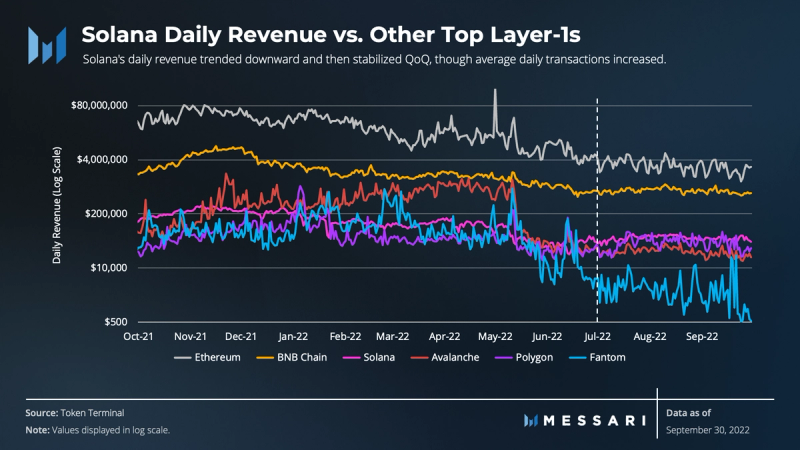

Similarly, Solana’s daily revenue trended downward, though average daily transactions increased. Therefore, the decline in revenue was attributed to the decline in transaction fees. Like Solana, Ethereum transactions were up on average, but post-Merge, Ethereum experienced a dramatic decline in transaction fees, pushing the protocol’s revenue down by ~80%. On the other hand, the rest of the peer group experienced declines throughout the quarter as a result of both lower average transaction fees and daily transactions.

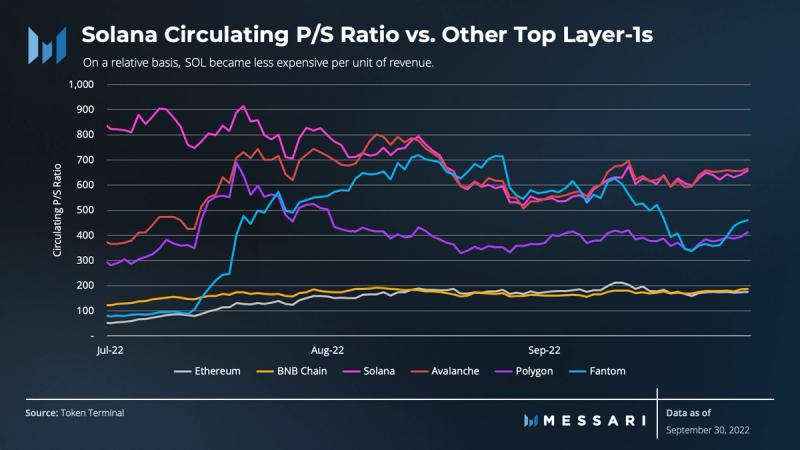

Over the quarter, Solana’s P/S ratio decreased compared to the peer group. The change in P/S gauges a protocol’s revenue and gives a sense of the amount and cost of transactions processed by the protocol. Because Solana’s change in value was flat and its transaction activity supported revenue, SOL became less expensive per unit of revenue compared to the peer group.

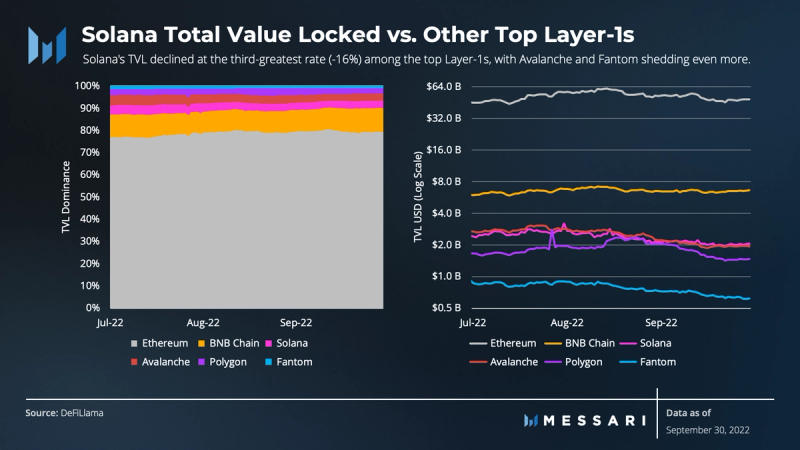

Q3 was flat for the crypto DeFi market, with aggregate TVL beginning and ending with ~$54 billion in USD terms. Solana’s TVL declined at the third-greatest rate (-16%) among the top Layer-1s, with Avalanche and Fantom shedding even more. Because declines in TVL are generally evaluated in USD, the asset’s decline in value represents the price shift in TVL versus the actual utilization of DeFi. While TVL in USD was down, the amount locked denominated in SOL was relatively stable.

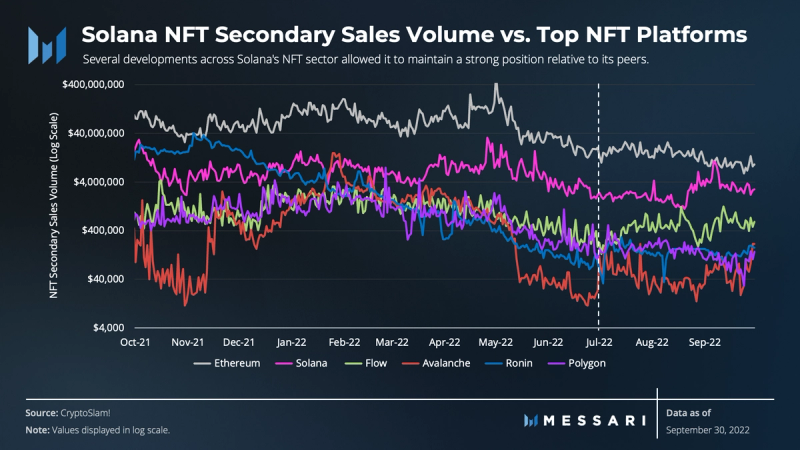

Several developments across Solana’s NFT sector allowed it to maintain a strong position relative to a peer group of the top L1s by secondary NFT sales volume. Secondary sales volume managed to eclipse Ethereum in early September. The majority of the activity during that period took place on Magic Eden V2.

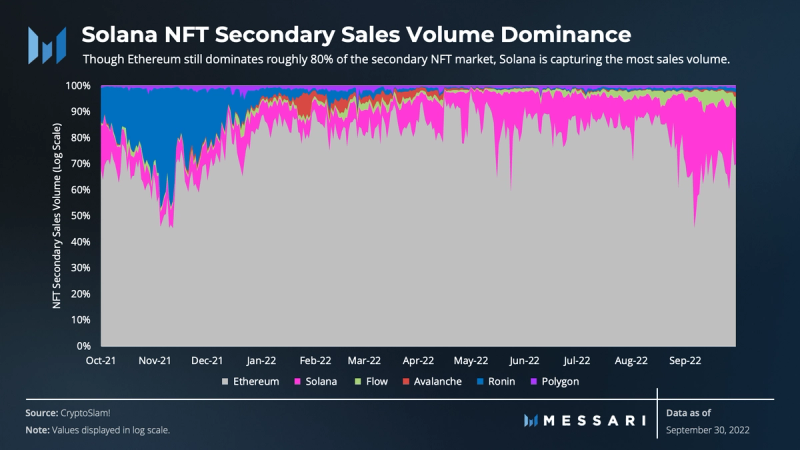

Though Ethereum still dominates roughly 80% of the secondary NFT market, Solana is closing the gap in sales volume. Ethereum’s dominance dropped from ~85% on average to ~80% over the quarter. Solana’s share rose from ~10% on average to just under 20%.

Qualitative Analysis

Key Events, Catalysts, and Strategies for Ecosystem Growth

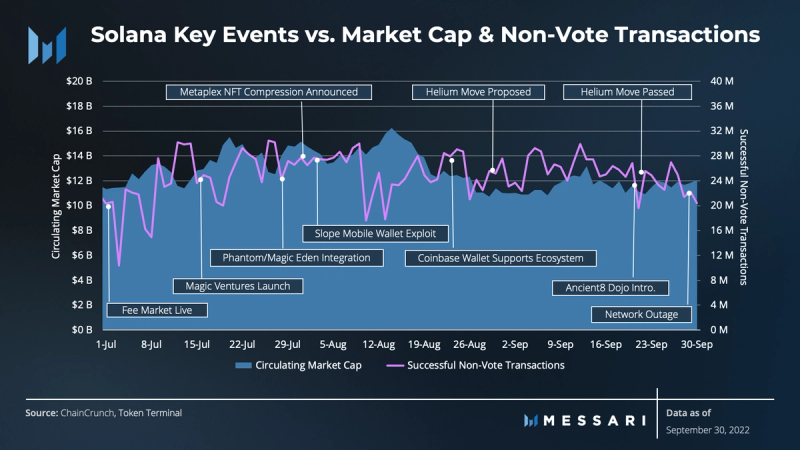

Though the bear market continued, Solana’s expansion strategies and network upgrades pushed forward throughout Q3. Ecosystem participants like Solana Ventures and Metaplex deployed strategic capital to usher creatives into the NFT and gaming space. Further, a unique case unfolded as the Helium network chose Solana’s value proposition for its new home. Aside from these attention-grabbing events, other aspects of the Solana strategy have been running in the background as key elements of growth since its inception. While not mutually exclusive, the relevant strategic elements over Q3 can be generalized into three areas:

- Technical — Integrate, decentralize, and improve functionality.

- User access and experience — Captivate users with greater user access and experience.

- Community — Acquire developers and drive adoption through community building.

July 2022

Greater user access and experience kicked off the quarter when Coinbase enabled Coinbase Wallet and Coinbase Exchange customers to send and receive USDC on Solana.

The push for greater accessibility was also evident when Dialect (protocol for Web3 messaging) partnered with Solana Mobile. They plan to build out core messaging infrastructure and developer tooling for Solana Mobile Stack (SMS). Dialect will launch a consumer-grade, open-source messaging application for the Saga smartphone.

The developer experience also improved with Alchemy’s support for Solana. Alchemy is a developer platform offering infrastructure services and toolkits for easier blockchain development.

Finally, community-building efforts continued as the Solana Foundation and Jump organized another round of Solana Hacker Houses before the Solana Breakpoint in Q4. In addition, the Solana Summer Camp initiated and featured several development tracks and $5 million in prizes and seed funding.

August 2022

Coinbase followed up its July efforts by integrating the Coinbase Wallet with applications across the Solana ecosystem. The integration allows users to connect directly to the Solana ecosystem with the Coinbase Wallet extension.

At the same time, Fireblocks, an all-in-one platform for building digital asset businesses and driving operational efficiency and security, began offering support for the Solana ecosystem.

On the technical side, Jump Crypto announced it is developing a new, open-source validator client for the Solana network called Firedancer. Written in C++, Firedancer aims to increase the throughput and resilience of the network by introducing client diversity on the Solana blockchain.

September 2022

Coinbase made another contribution in September when Coinbase Cloud launched Solana Archival Nodes. The launch aims to enable the Solana developer community to access archival data more efficiently.

On the developer side, September surfaced activity around Solana supporting the smart contract language Move. Move is a programming language for smart contracts. It contains unique value propositions and is designed to be a platform-agnostic language. Once it’s fully implemented, Move may attract developers down the line and join Solana’s LLVM-compatible smart contract languages

On the technical side, Nitro came out of stealth in September. Nitro is a Solana VM-based Layer-2 that will be deployed on the Sei Network, a new Layer-1 blockchain in the Cosmos ecosystem. Nitro gives credence to the idea that Solana’s developer community is growing while other ecosystems are trying to court developers and leverage components of the Solana stack.

Finally, community-building efforts continued through the end of the quarter. The Solana Foundation launched Solana U, a new program for university students. It will equip them with tools to connect to the Solana ecosystem, learn Rust, and launch new projects.

The above events are just a handful of the collection of efforts in Solana’s overarching strategy to grow its ecosystem.

Ecosystem Challenges

Solana addressed previous quarters’ network challenges by rolling out V1.10, QUIC, and the fee prioritization mechanism. It executed well on its growth strategy overall. Nevertheless, the Solana ecosystem was faced with new challenges to overcome during Q3.

During the quarter, the ecosystem experienced a series of events, including a mobile wallet exploit and a network halt.

Slope Mobile Wallet Exploit

8/2/2022 – Magic Eden stated that there appeared to be a widespread SOL exploit that was draining wallets throughout the ecosystem. The team advised Solana users to revoke wallet permissions for any suspicious or untrusted links.

The Phantom wallet team stated that they were working closely with other teams to get to the root cause of the vulnerability. At the time, the team did not believe the issue was a Phantom-specific issue.

8/3/2022 – Solana Labs confirmed the exploit and shared details on the current state. Approximately 7,767 wallets were affected. Engineers continued working with multiple security researchers and ecosystem teams to identify the root cause of the exploit.

The exploit affected several wallets, including Slope and Phantom. Users were encouraged to use hardware wallets and to treat the drained wallets as compromised and abandoned.

Solana Labs issued a statement attributing the exploit to an attack that compromised the private keys of Slope mobile wallet application users. The team explained that the exploit was isolated to one wallet on Solana, and hardware wallets used by Slope remained secure.

Network Halt

9/30/2022 – The network halt was not related to Gulfstream and spamming issues that the V1.10 and QUIC upgrades addressed. Instead, the halt was due to an anomalous consensus bug. By the following day (start of Q4), block production resumed on the Solana network following a 7-hour chain halt.

While the quarter presented difficult challenges for the ecosystem and its participants, the issues were isolated and unique cases. Moreover, the core Solana protocol and its cryptography were not compromised.

The Road Ahead

A public roadmap is not maintained by Solana at this time. Much of the road ahead continues to reflect what the Solana ecosystem has been outwardly working on for several quarters.

Further implementations of V1.10, the fee prioritization mechanism, and other developments will continue to roll out. As these upgrades are implemented, there should be continued improvement in network performance.

Another significant development still on the horizon is Neon. While the project has released Neon Alpha (the development network), it has yet to go live on mainnet. Another upcoming development is that of Nitro, which aims to combine Solana’s execution environment with the Cosmos and IBC ecosystem. With Neon and Nitro serving as gateways, there could be significant growth similar to how other Layer-1s have acquired developers and catalyzed network effects.

Introducing Move as a new smart contract language on Solana could attract more developers. While still in the early stages, Move could catalyze additional developer activity in the Solana ecosystem once it’s implemented.

Lastly, the open-sourcing of the Solana Mobile Stack (SMS) for Android is still underway. The SMS will enable native Android Web3 applications on Solana. In addition, Saga, the first Solana Mobile Android phone, will begin shipping with the SMS by Q1 2023. These developments are aimed at bridging smartphones and bringing unique functionality and features that will tightly integrate with the Solana blockchain. Its features will include the open-source messaging application that Dialect and Solana Mobile are building. For Saga and SMS to succeed, more partnerships like the one with Dialect should be sought out.

Closing Summary

In Q3, the bear market surfaced the network’s fundamental user base and ability to advance its growth strategy. User activity reverted to the longer-term average and stabilized during Q3. Transaction activity was more significant due to the improved network stability. Fundamentals like a foundational user base, network stability, and transaction activity continued to drive network value.

The ecosystem continues to expand. A healthy distribution of TVL across applications still exists. Solana’s strategy and position in the NFT sector remain strong. Its second-largest secondary sales volume is narrowing the gap with Ethereum. Strategies to boost GameFi are underway, and Solana is seeing more unique use cases like Helium join the ecosystem.

Staking and decentralization of the network remain strong. Solana aims to improve decentralization through geographic diversity, hosting, and entity distribution of validators.

While the network’s fundamentals improved along with its ability to advance its growth strategy, the quarter presented challenges. The issues were isolated and are not recurring in nature.

Ultimately, the Solana ecosystem is continuing its efforts to grow by incorporating growth strategies that include network upgrades, technical integrations, community building, and improved user accessibility.

Let us know what you loved about the report, what may be missing, or share any other feedback by filling out this short form.

This report was commissioned by Solana Foundation, a member of Protocol Services. All content was produced independently by the author(s) and does not necessarily reflect the opinions of Messari, Inc. or the organization that requested the report. Paid membership in Protocol Services does not influence editorial decisions or content. Author(s) may hold cryptocurrencies named in this report. Crypto projects can commission independent research through Protocol Services. For more details or to join the program, contact ps@messari.io. This report is meant for informational purposes only. It is not meant to serve as investment advice. You should conduct your own research, and consult an independent financial, tax, or legal advisor before making any investment decisions. The past performance of any asset is not indicative of future results. Please see our terms of use for more information.