Key Insights

- Stacks 2.1 rolled out a slew of new features and updates like removing PoX sunset, continuous Stacking and improving developer tooling, and more.

- A surge in BNS registrations was a key driver in network activity in Q3.

- Overall network usage was down, consistent with the broader market.

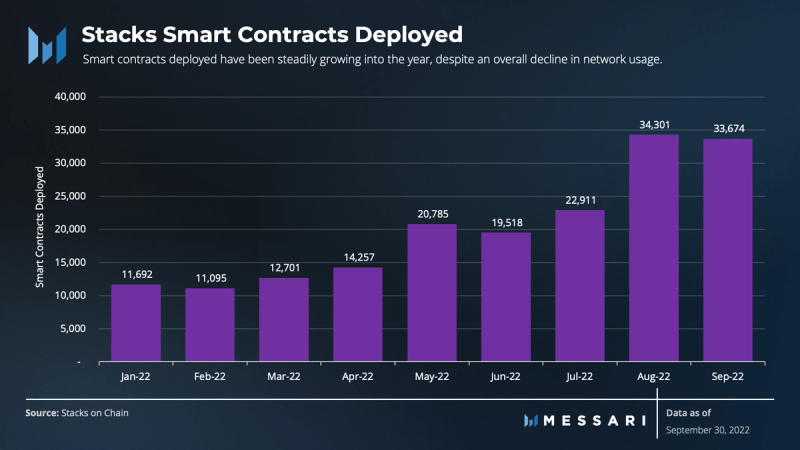

- Stacks continued to show strong signs of development, with smart contracts deployed growing by 60% QoQ.

- The average number of Stackers and Miners securing the network fell QoQ.

Primer on Stacks

Stacks is a Bitcoin layer that utilizes a novel consensus mechanism, Proof-of-Transfer (PoX). It runs parallel with Bitcoin’s Proof-of-Work (PoW) consensus, using it as a settlement layer. Metadata from newly mined Stacks blocks is anchored to every Bitcoin block, providing proof of every Stacks block ever produced. PoX is an extension of the Proof-of-Burn mechanism. Instead of miners burning BTC as a proxy for computing resources, miners now commit BTC to eligible Stacks addresses that participate in consensus.

Stacking launched as part of Stacks mainnet launch in January 2021. The upgrade added a new element to the consensus mechanism where Stackers lock a predetermined amount of STX tokens into a smart contract. This lockup sets the stage for mining, where Stacks miners commit BTC in exchange for a chance to mine a Stacks block. Miners who produce new blocks are rewarded with newly minted STX tokens and STX fees, whereas select Stackers receive yield denominated in BTC.

Introduction

Layer-1 (L1) blockchains, Layer-2 (L2) solutions, and their ecosystems have been feeling the brunt of crypto winter. Total value locked (TVL) across many chains declined significantly since the overall markets peaked in Q4 2021. However, it’s worth noting that Stacks ecosystem is still nascent and in a class of its own.

The broader ecosystem in crypto has an entirely different foundation than Stacks. Most developers built decentralized applications on Ethereum virtual machine (EVM)-compatible blockchains.

EVM-compatible chains operate using Turing-complete smart contract programming languages like Solidity or Rust. Stacks, however, uses a smart contract language called Clarity, which is intentionally Turing incomplete.

Turing-complete languages are inherently more flexible but require compilation. This flexibility opens up attack vectors on EVM-compatible chains. As a result, these chains have suffered countless hacks over the years. Turing-incomplete languages are not vulnerable to reentrancy attacks like their complete counterpart, making Clarity inherently more secure.

Clarity is a human-readable and interpreted language that allows users to know where a code will terminate before executing it, thus removing additional attack vectors.

Performance Analysis

Stacks Network and Financials Overview

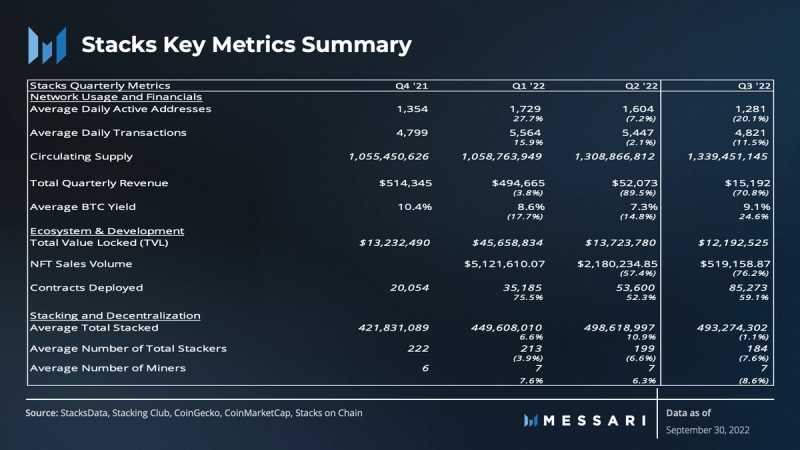

Network usage on Stacks, defined by daily active addresses and transactions, was down for the second subsequent quarter. In addition, the cost of using the network has fallen drastically since the beginning of the year.

As expected, the circulating supply grew as miners produced new blocks. Liquid supply, however, grew over 50% QoQ, following a downward trend in past quarters. Liquid supply is calculated by subtracting the total STX tokens locked (e.g., Stackers) from the circulating supply. On average, there were 280 million STX tokens unlocked in Q3. The implications will be discussed in more detail later in the report.

Average daily active addresses have declined steadily since the beginning of the year, dropping 20% QoQ. This trend is consistent with other chains, especially in H1 2022.

There is a strong relationship between the amount of daily registered Bitcoin Name System (BNS) addresses and daily active addresses. Stacks V1 only allows one BNS address for each Stacks address. Users get around this restriction by creating multiple Stacks addresses to register additional BNS names, which can artificially inflate unique users.

In contrast, Ethereum Name Service (ENS) can have infinite ENS addresses associated with an Ethereum address. Considering the ENS craze, in which three-letter domains sold for exorbitant amounts of ETH, Stacks users could be creating new addresses to acquire and speculate on BNS addresses.

The average daily transactions in Q3 was 4,800 (-12%) QoQ, mirroring activity in Q4 2021. Despite the downward trend, daily transactions picked up toward the end of the quarter due to the increased demand for BNS addresses. The last two weeks of September had 70% more transactions than the first two weeks.

During the same period in September, registered BNS addresses and their subsequent transaction activity grew by over 300% and 230%, respectively. This overall BNS activity catalyzed the uptick in transactions at the end of Q3.

Average transaction fees are driven by network usage and the price of its native token (STX). Stacks’ steady decline in average daily transactions (-13% YTD) and price (-85% YTD) in 2022 drove average transaction fees to their lowest in over a year. Although cheaper fees typically incentivize more users to participate on the network, Q3’s user data showed the opposite effect.

Stacks’ mempool, on average, had 1.5 million pending transactions in Q3, up (7.7%) in Q2. This is generally in line with its average (1.6 million) YTD.

Simply put, the mempool is a transaction-ordering queue for transactions pending confirmation. These pending transactions are correlated with network congestion, which in turn directly impacts transaction fees.

Unusual spikes in mempool size are correlated to increased transaction fees. However, February had a disproportionate spike in fees relative to the mempool size. Network congestion is generally caused by increased activity but can be caused by network instability. In February, a spike in traffic uncovered issues with software resulting in abnormally high transaction fees. The Stacks V2.05.0.1.0 release addressed the issue by incorporating a batch of new updates and changes, including a new fee estimator.

Revenue is synonymous with STX fees, which are fees paid to miners who produce a block. The value of these revenues relies on the demand for block space and the market price of STX. During periods of increased network congestion, evidenced by the mempool chart above, the likelihood of revenue generation increases substantially.

Stacks’ fully diluted valuation (FDV) fell by 27% QoQ and 78% YTD. Declines in price and decreased network activity were key drivers for quarterly revenue falling (-70%) to $15,000 in Q3. At its peak, total quarterly revenue was as high as $514,000, but it has since fallen (-97%) from its highs.

Ecosystem and Development

As mentioned earlier, Stacks’ ecosystem is still young and lacks the maturity of its competition. The protocol remains focused on increasing awareness around Clarity, attracting developers, and demonstrating the value of building applications using Bitcoin as a settlement layer. Stacks is also focused on building a trustless peg mechanism where BTC can move freely, in and out of the Stacks layer, and deploy Bitcoin in Clarity contracts.

Decentralized Finance (DeFi)

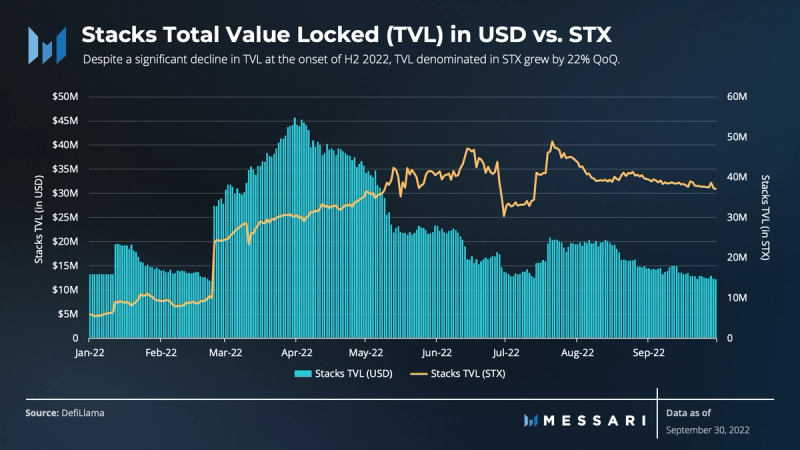

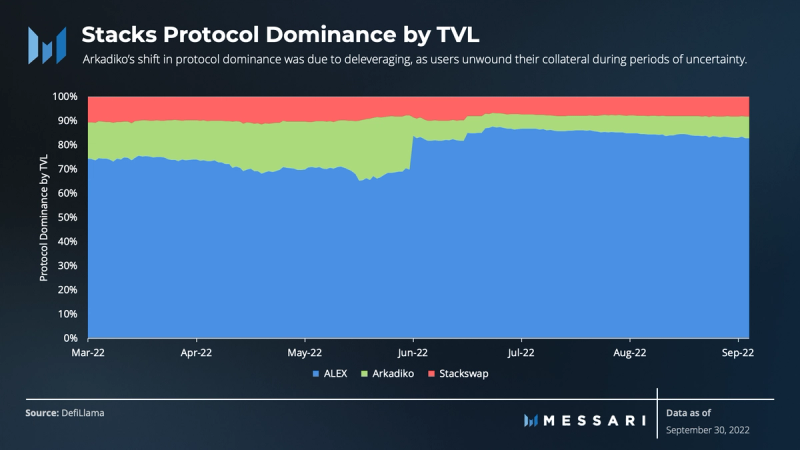

After another volatile quarter, Stacks followed along with other protocols, seeing its TVL drop by 11% QoQ. Stacks’ TVL has shaved off over a third of its value since peaking in H1 2022. Despite the considerable declines in the first half of the year, TVL denominated in native STX has grown steadily QoQ. Total STX held in DeFi applications increased by 22% in Q3, suggesting a sustained utility.

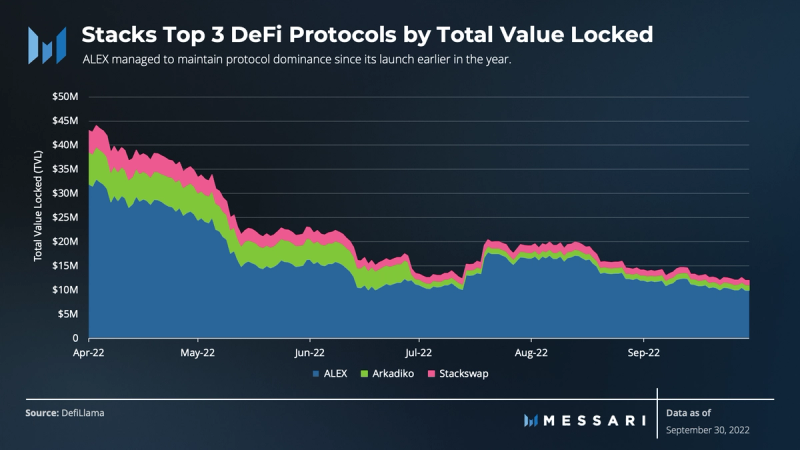

ALEX is a full-service DeFi protocol on Stacks that launched early this year. It has since taken the Stacks ecosystem by storm, securing the top spot as the largest DeFi protocol. ALEX serves as a token launchpad, decentralized exchange (DEX), and lending platform with the ability to use leverage. ALEX’s TVL fell by 11% QoQ. As the largest DeFi protocol, its falling TVL was the primary contributor to the overall decline in Stacks’ TVL in Q3.

Arkadiko is one of the first major DeFi applications launched on Stacks. It primarily allows users to access self-repaying loans and functions as a decentralized exchange (DEX). STX tokens are deposited in a vault and used as collateral in exchange for loans denominated in the USDA stablecoin. Arkadiko’s protocol dominance has shifted significantly since the end of Q2. Its TVL has declined since its peak (-84%) but was relatively flat QoQ (-1.4%). This shift is consistent with the broader ecosystem, where users have deleveraged and unwound collateral rapidly during these extended periods of uncertainty and volatility.

Stackswap is the first DEX built on Stacks. It leverages liquidity pools, yield farming, and staking. Its dominance is virtually the same as Arkadiko in Q3 but fell 19% QoQ. Many users have reverted to fundamentals to preserve capital, choosing to reduce their exposure to riskier platforms.

NFTs

Stacks’ NFT market experienced substantial trading and minting volumes in H1 2022. Sales and minting volumes exceeded $7.8 million and $1.8 million, respectively, YTD.

However, the negative market sentiment also made its way toward NFTs. Q3 had $520,000 in sales volume, down 76% QoQ. Whereas NFT minting volume declined 77% QoQ, totaling $144,000.

The overall decline in trading and minting volumes did not affect NFT creators, as there were over 20,000 NFTs minted in Q3, growing by 120%.

Considering there were fewer users and transactions on the network, metrics like contracts deployed took the spotlight, growing 60% QoQ. The number of contracts deployed is a great signal of development and the use of smart contracts on Stacks.

Stacking and Decentralization

Technical Primer

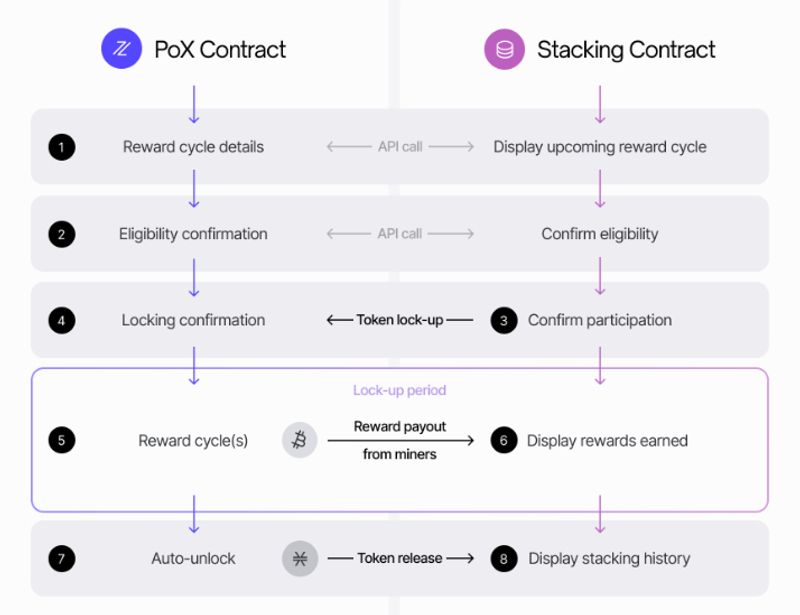

Before diving into the Stacking and Decentralization metrics, it is essential to bring more context to the underlying mechanics, nuances, and relationships of Proof-of-Transfer (PoX). As mentioned in the Primer, there are two key participants in the PoX consensus mechanism: Stacks miners and Stackers.

Source: Stacks.co

PoX occurs over reward cycles in the Prepare and Reward phases. The Prepare phase identifies a new reward cycle and takes a snapshot of Stackers, confirming their eligibility. The snapshot determines which Stackers will be included in the reward cycle, and all confirmed Stacker addresses are then broadcasted to active miners.

Following the snapshot, active miners must commit an equal amount of bitcoin to two Stackers’ addresses for every block. These addresses are chosen randomly using a verifiable random function (VRF).

The miners’ minimum recommended commitment is 11,000 satoshis (0.00011 BTC), i.e., 5,500 satoshis per Stacker address. Miners can increase their odds of winning the chance to produce the next block by making larger commitments. After all active miners broadcast their commitments, a miner for each block is chosen randomly using a VRF.

Each reward cycle spans approximately 2,000 Bitcoin blocks (~14 days) and 4,000 reward slots. Reward slots are filled by confirmed Stackers who have met the minimum requirement. For example, if a confirmed Stacker locks up the minimum of 150,000 STX, they get one reward slot. Any unused reward slots during a reward cycle are filled with burn addresses.

After a miner produces a block, BTC rewards are released to either of the two Stackers’ addresses. If either of the addresses was a burn address, BTC would be burned. Miners only receive newly minted STX tokens and accrued STX fees (released after 100 blocks) after releasing the BTC to Stackers. The active miner who produces a block is rewarded accordingly. Conversely, every active miner who loses a block forfeits their BTC commit for that block.

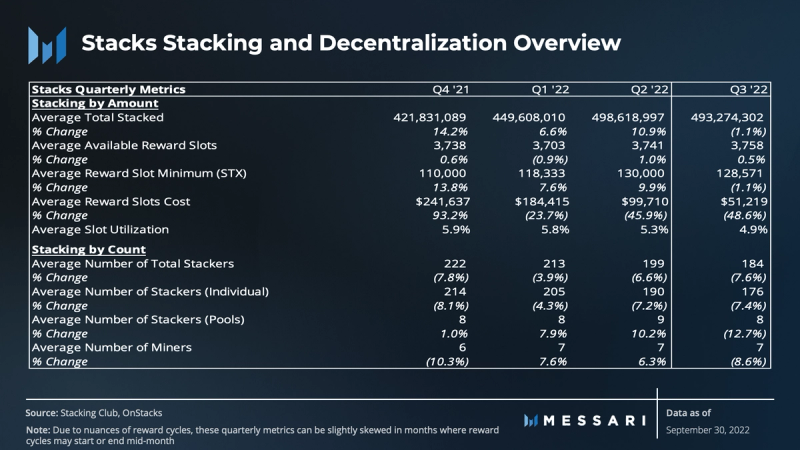

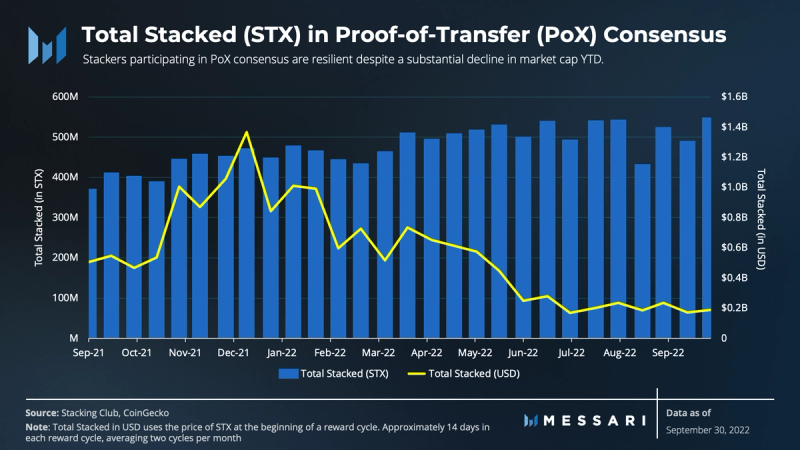

Despite solid growth in prior quarters, the average total stacked was relatively flat QoQ (-1.1%). However, the average total stacked denominated in USD didn’t fare nearly as well. It peaked at $1.3 billion at the end of 2021, but it has since been hovering at just under $200 million on average in Q3.

The data suggests Stackers are holding for the long term and are undeterred by Stacks’ market capitalization falling by 81% since Q4 2021. The total stacked during a reward cycle is driven by the Stackers’ meeting the dynamic threshold to be eligible for Stacking rewards.

The dynamic threshold (e.g., reward slot minimum) is based on the percentage of liquid supply (LS) of STX participating in consensus. For example, if less than 25% of the LS of STX is participating, the minimum requirement per reward slot is 1/16,000 of the total LS of STX. If greater than 25%, it changes to 1/4000 of the total STX participating.

Stackers

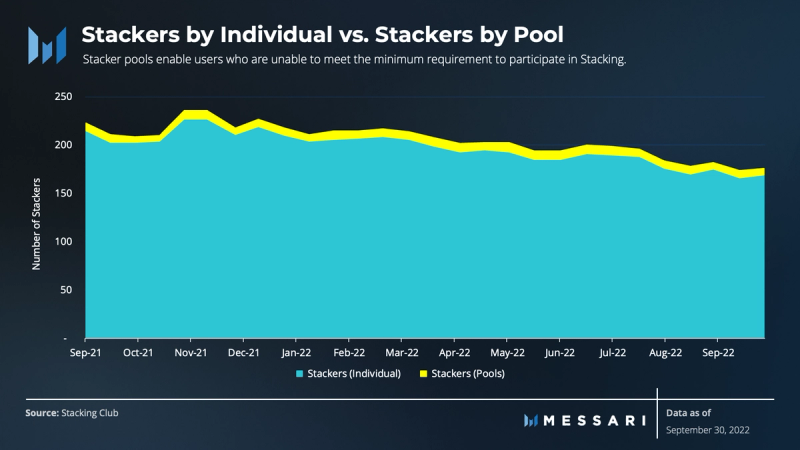

The average number of Stackers has steadily declined over the last 12 months. There were 14 fewer (-7%), individual Stackers, on average in Q3 and 29 (-14%) less than at the beginning of the year. This is largely due to a consolidation of holdings between individual Stackers and pools, as the average total stacked was mostly unchanged.

Pools, on the other hand, have grown each of the last three quarters except for in Q3, where there were 1 (-4%) fewer pools. The number of pools in Q3 is in line with the average over four quarters.

The use of pools allows users to still participate in Stacking even if they can’t meet the minimum requirement. Various custodial and non-custodial pools have substantially lower stacking requirements. For example, Friedger’s Pool is non-custodial and has a 40 STX minimum with zero fees. Planbetter is another pool that has a 200 STX minimum with a 5% fee. Users also have the flexibility to Stack on exchanges like Okcoin and Binance, except that they lose custody of their STX.

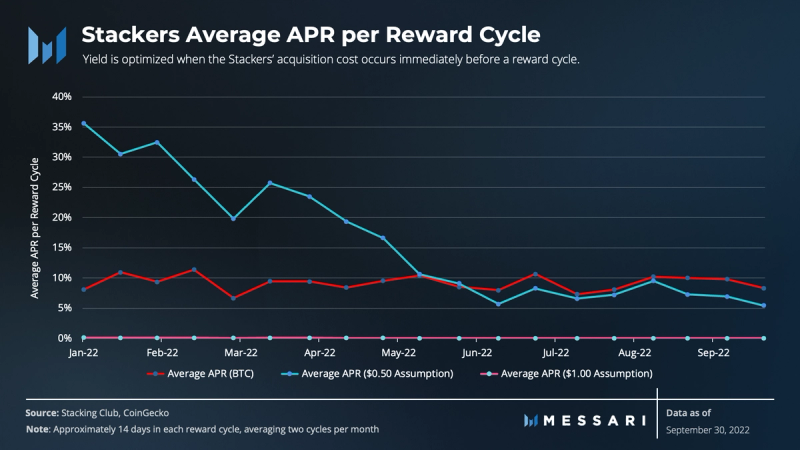

Bitcoin paid out to Stackers on average yielded 9% in 2022, with yields growing by 24.6% to 9.1% in Q3. However, these yields use assumptions based on the price of STX at the beginning of each reward cycle.

A distinction needs to be made between yield and real yield. The 9% yields assume that the cost basis for reward slots is the cost to secure a slot at the beginning of each reward cycle. However, assuming Stackers accumulate STX at various prices, their real yields may vary greatly depending on their cost bases. For example, if a Stacker’s cost basis is $0.50, holding everything else constant, their real yield YTD would be greater than the yield before falling below its cost basis. In contrast, a Stacker with a cost basis of $1.00, holding everything constant, has a real yield of zero, ultimately losing any benefit from being a Stacker.

Broadly speaking, the Stacks consensus mechanism attracts Stackers by generating BTC yield. These yields are based on the reward cycle as a whole and not on individuals participating on their own or in a pool. Participation does not guarantee rewards, though roughly ~95% of reward slots see rewards.

Stackers can sacrifice opportunity costs and expose themselves to the volatility of STX. At a minimum, a ~14-day lock-up, combined with uncertain and potential infrequent earnings, could pose a challenge to onboarding new stacking participants.

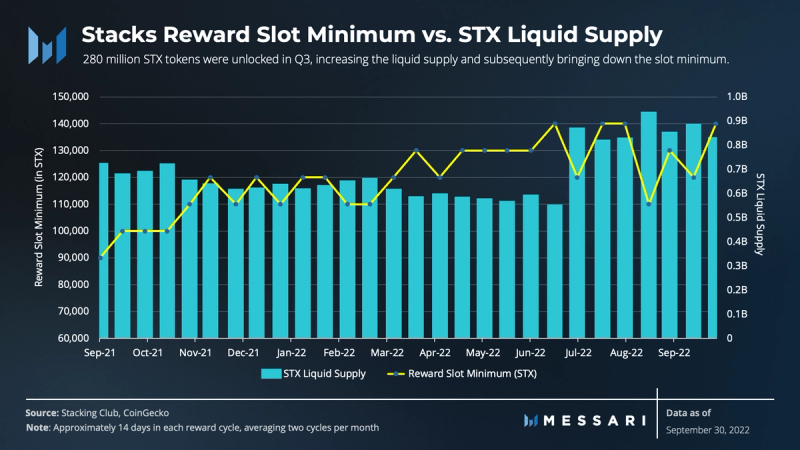

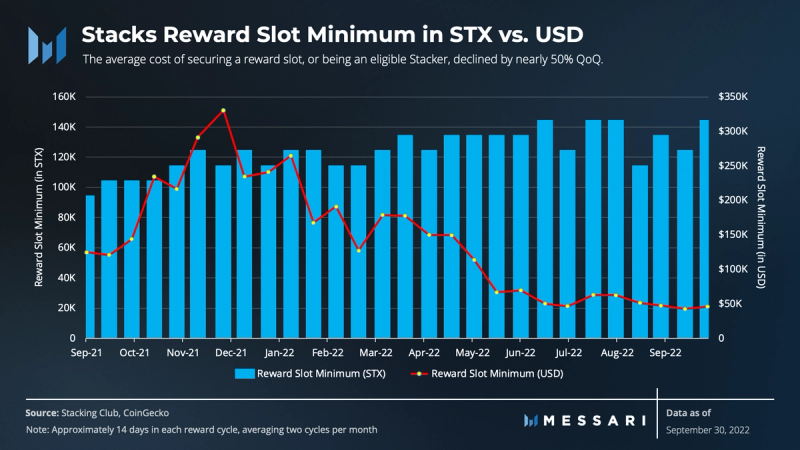

The reward slot minimum, also known as the dynamic threshold, has remained relatively flat this year, up 0.5% on average QoQ. The reward slot minimum determines the minimum STX needed to lock up during a reward cycle to be an eligible Stacker.

The dynamic threshold creates an inverse relationship between the reward slot minimum and the liquid supply of STX. In Q3, 282 million STX tokens were unlocked, increasing the liquid supply by over 51%, which resulted in a lower reward slot minimum.

Although the reward slot minimum was primarily unchanged QoQ in STX, the story wasn’t the same in dollar terms. The cost to secure a slot has diminished significantly since the beginning of the year.

For example, on average, the reward slot minimum in Q3 was 128,000 STX, up 9% from 118,000 STX in Q1. However, in dollar terms, the average reward slot was $51,000 in Q3, down 49% from $99,700. The average cost trended downward in line with the price of STX. Since reward slots are based on native STX, the downward pressure of its price made reward slots much more affordable.

Stacks Miners

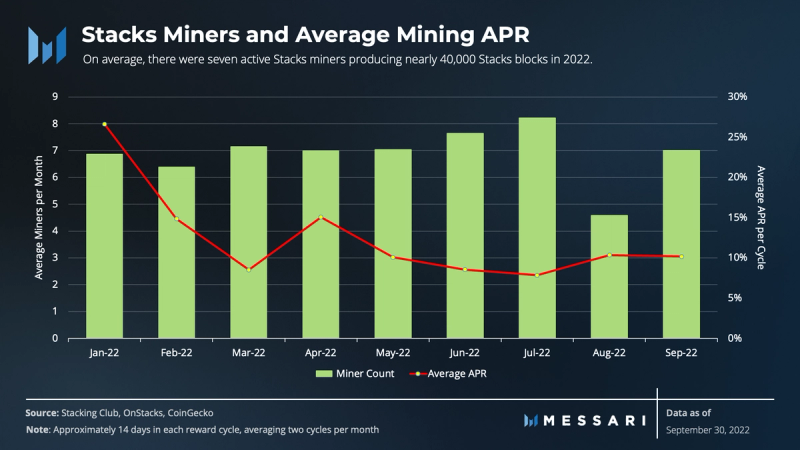

On average, seven active miners were simultaneously producing new blocks on the Stacks blockchain in 2022. The average APR for these active miners during Q3 was 9.5%, down from 11.2% in the prior period. The APRs are calculated using the daily price of STX and BTC, corresponding with daily BTC commits, STX block rewards issuance, and STX fees. STX fees generated during a reward cycle were also included since miners are entitled to these fees.

Using the minimum recommended commitment of 11,000 satoshis (0.00011 BTC) per block, the miner’s cost to compete with others is approximately $4,300 (as of 9/30) per reward cycle (~4,000 blocks). For comparison, the cost at the end of 2021 was $10,300. The odds of winning a block increase with an increase in their commitment, suggesting the cost to miners is likely greater.

Total rewards distributed in dollar terms to miners and Stackers fell to their lowest in 2022. The distribution, however, started stabilizing in Q3 as the overall market found its footing. Miner rewards fell by 48% from approximately $9.7 million to $5.1 million QoQ. Rewards distributed to Stackers, however, declined by approximately 41% to $4.9 million in Q3. The approximate proportion of BTC burned declined in Q3, a net benefit to Stackers as they earned more in return.

Qualitative Analysis

Key Events

Stacks 2.1

Stacks 2.1 was introduced to the network on August 23, 2022. The network upgrade confirmed the project’s blockchain design and included feature improvements for users and developers. The most critical highlights of 2.1 include:

- PoX Sunset: PoX sunset will be removed as part of the upgrade, allowing the Stacking contract to continue. Had PoX remained, the PoX/Stacking consensus would’ve reverted to Proof-of-Burn. However, the community can renegotiate this in the future.

- Continuous Stacking: The upgrade enables flexible Stacking and improved reward eligibility. For example, Stackers can commit to one-cycle intervals without missing out on the next reward cycle. Previously, Stackers were not permitted to participate in the subsequent delegation period for the reward cycle due to a cooldown period.

- Topping off: Stackers can now “top off” or add to their Stacked STX with any arbitrary amount. This allows Stackers who fall short of the dynamic minimum requirement to top off and remain eligible for an upcoming reward cycle.

- Attracting more miners: Miners can use native segwit or taproot UTXO to minimize transaction costs. This flexibility helps lay the foundation for decentralized mining pools, lowering the barriers to entry.

- Linking Stacks more directly with Bitcoin: To simplify the user experience and encourage increased adoption, Stacks now offers a more seamless UX to reduce the friction of exchanging assets between Stacks and Bitcoin addresses.

- Tools for Clarity: To attract new developers and retain existing developers, Stacks introduced two functions to improve the developer experience: 1) easy syntax for Bitcoin transaction reaction triggers and 2) easy syntax for onboarding off-chain data.

Rebranding Hyperchains to Subnet

In August 2022, Stacks renamed its hyperchain scaling solutions to “subnet” to avoid trademark infringement. The subnet is a layered scaling solution that allows transactions to be processed with higher throughput and lower latency. The team has continued testing various subnet models and is targeting to launch in Q1 2023.

Integration with QuickNode

On September 7, 2022, Stacks integrated with QuickNode to improve node scalability. QuickNode is a Web3-based software development kit (SDK) and analytics tool that allows developers to run Stacks nodes with QuickNode. Developers can use QuickNode to reduce the burden of node maintenance and synchronization, thus allowing developers to focus more on building applications.

Stacks.js Starters

Stacks keeps a repository of JavaScript libraries to enable a quick turnaround for developers in routine front-end application updates. On September 16, 2022, Hiro launched Stacks.js Starters to help developers move to production faster. These tools follow familiar JavaScript frameworks like React, Svelt, and Vue, which help to support quick iterations on the front end. These iterations also interact directly with Clarity through Stacks CLI (a pre-specified set of commands for front-end developers) and built-in features like wallets and voting.

Ecosystem Offsite

Community members gathered in September to address feedback from over 50 Stacks companies, align on technical priorities, and identify roadmap challenges. Discussions were conducted through working groups split into five strategic focus areas:

1) Network speed

2) Non-custodial BTC on Stacks

3) Bitcoin NFTs

4) Go to market non-custodial BTC

5) Marketing and communications The collaboration in the community resulted in strategic benchmarks for Stacks’ long-term vision, which will help align governance voting and milestone goals in the future.

Governance

SIP-018 for Structured Data

SIP-018 is a recent improvement proposal that suggests data be restructured in a friendlier, human-readable format so that its structure is directly compatible with smart contracts and can be easily implemented in decentralized applications.

SIP-019 for Token Metadata Updates

Token metadata refers to information contained within the token, including its transaction history. For NFTs specifically, metadata could refer to pixels in a jpeg, auditory characteristics, etc. In some instances, NFTs will have dynamic metadata, and SIP-019 specifically proposes a process that allows Stacks to track token metadata changes easily.

Stacks Foundation

Update on the Grants and Residency Program

The Stacks Foundation treasury reportedly enjoys a runway of around two years; nevertheless, the foundation is making careful adjustments to optimize fund allocations and effectiveness. To increase efficiency and convenience, the Stacks Grants program will transition its application process back to the GitHub Grants Launchpad. After a trial period that lasted a few months, both the Ambassador and Residency programs were paused due to concerns regarding the programs’ sustainability and efficacy. Specifically, there were doubts whether either program could function without the Foundation’s involvement. These challenges seemed to be general organizational issues that come with decentralizing operations.

Challenges

Stacks’ biggest obstacles are bringing more awareness to Clarity and demonstrating the value proposition for building on Stacks. The majority of developers in crypto use Solidity and Rust, which could make it challenging to convince them to learn another language. In addition to developers, DeFi users have been accustomed to EVM-based applications, which could dissuade users from switching to DeFi powered by Bitcoin.

Stacks’ focus on unlocking BTC capital comes with its own challenges due to the nature of its ecosystem. The current landscape of smart contract platforms is arguably more mature, however, it can be overshadowed by the array of exploits over the years.

Although network congestion is a result of welcomed network activity, it has caused growing frustration for users and builders. To address the growing user and developer base, Stacks must continue improving network efficiency and throughput with scaling solutions like subnets.

Through partnerships and initiatives, the team at Hiro Systems introduced new developer tooling and resources intended to make Clarity more developer friendly. Also, programs like Clarity Camp have proven to be an effective method of attracting developers. Lastly, Stacks continues to test its subnet scaling solutions to address these issues.

Roadmap

Stacks’ main priorities include successfully rolling out Stacks 2.1, addressing the critical needs in the ecosystem, onboarding more developers, and improving the infrastructure around Stacks. In addition, a focused effort on SIP proposals and subnet preparation is also a large priority.

The developments and objectives established at the Ecosystem Offsite will remain intact moving forward. The protocol aims to increase the number of developers, community leaders, and decentralized applications by approximately ~30% in Q4.

Stacks is setting an ambitious goal for July 2023 to have applications built on its infrastructure to collectively hold a valuation exceeding Stacks’ market capitalization or 3% of Bitcoin’s. The careful rollout of Stacks 2.1 and the strategic objectives outlined above help lay the foundation to achieve this vision.

Closing Summary

Metrics across the board were largely down in Q3, as with many other Layer-1 chains, Layer-2 networks, and their respective ecosystems. The global macro landscape and crypto market sentiment hindered crypto activity going into H2 2022.

Stacks is still a nascent Bitcoin layer with very unique fundamentals. It is looking to capitalize on Bitcoin and redefine DeFi by combining the forces of Proof-of-Work and Proof-of-Transfer consensus mechanisms. Post-Merge, Stacks positions itself as a smart contract protocol utilizing Bitcoin’s PoW to secure its applications. However, Stacks’ decentralization scores low compared to Bitcoin and its peers. The 2.1 upgrade aims to lower the barrier to entry for miners through decentralized mining pools. Future upgrades seek to improve decentralization and unlock Bitcoin capital to be deployed in Clarity contracts.

Like many protocols in the bear market, the team remains focused on building, improving user and developer experience, and onboarding the next cohort of developers and applications.