Key Insights

- The Sandbox experienced declines across most KPIs tracked, such as primary and secondary sales volumes, while the number of secondary sales transactions increased.

- New LAND parcel mints were paused in Q3 as The Sandbox team and its partners chose to delay most NFT launches until market conditions improve.

- The Sandbox Alpha Season 3 has been a major success thus far, reaching a record 341,000 players and recording growth in average play time and player engagement KPIs.

- Traditional and crypto-native brand partners continue to be onboarded at a similarly impressive clip as in previous quarters, despite lower trading activity across digital assets.

A Primer on The Sandbox

The Sandbox (TSB) is a platform for creating and hosting entertainment experiences in virtual worlds. In The Sandbox, anyone can create 3D assets like buildings, in-game items, and non-player characters. These assets can then be used to build diverse experiences such as games, music and fashion events, social activities, quests, art exhibits, and contests. The Sandbox offers creators a set of intuitive tools that neither require a background in coding nor in designing experiences. These tools include a 3D editor for making and animating items, a game maker for making experiences, and a game client. The Sandbox is actively working on making these tools as user-friendly as possible to unleash the creativity of its community. For instance, the 3D editor combines different in-game tokens to create user-generated assets.

These user-generated assets are ERC-721 non-fungible tokens that can be monetized on open markets. The Sandbox ecosystem leverages a series of tokenized gaming features including:

- SAND – a digital in-game currency used for purchases, monetization, and asset creation

- LAND – ownable digital land within The Sandbox virtual world

- ESTATE – a combination of LANDs to create a larger plot

- GAMES – a bundle of assets and scripting logic to create interactive experiences

- ASSETS – 3D virtual images created by players

- GEMS – tokens burnt to give attributes to assets

- CATALYSTS – tokens burnt to create ASSETS

Thanks to the tradeable nature of these user-generated assets within its virtual world, The Sandbox has robust in-game economics.

Performance Analysis

LAND Parcel Distribution

There is a finite amount of LAND in The Sandbox — 166,464 parcels. New LAND parcels are typically minted (primary sales) through publicly scheduled minting events (fixed price or English Auction), but private sales to partner projects also occur. During these auctions, LAND is usually sold on a first-come-first-serve basis. Prices also vary based on rarity (regular vs. Premium), and larger ESTATES are often auctioned on OpenSea. Not all mints result in immediate sales, however. The Sandbox will also mint LAND for the purpose of private sales to partners to be completed at a later date.

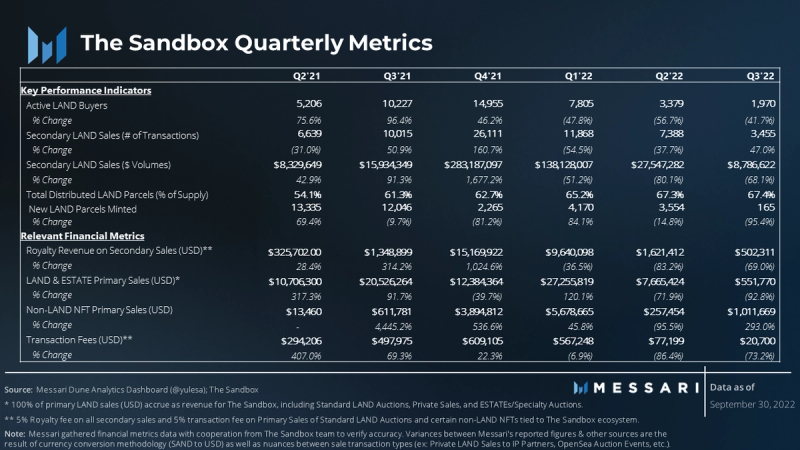

With only 165 LAND parcels minted in Q3, the proportion of LAND parcels that have been distributed has increased by a modest 0.1% of the max LAND supply since the previous quarter. As of Q3, 67.4% of the maximum supply has been distributed. The rate of mints has slowed dramatically over the past quarter, as public LAND mints have effectively been paused in the face of recent market turbulence. The subsequent loss in user appetite for digital assets — a phenomenon experienced across the broader crypto market — has also had an effect.

The 165 LAND parcels minted in Q3 were solely related to private sales that The Sandbox regularly conducted with new partner brands joining the ecosystem. This conscious slowdown in LAND circulating supply growth is prudent given the recent market volatility and has at least partially offset some of the negative price pressures caused by a more risk-averse collector-base. The Sandbox anticipates releasing new LAND to the public through a series of brand partner launches planned for mid/late November. Though, more details regarding these minting events have not yet been announced.

LAND Primary Sales

Note: On-chain tracking of Private Sale, ESTATE Sale, and other non-standard sales data is limited without first having details on transaction size, wallet address, or other identifiable characteristics (often not readily available information). The Sandbox Team provided primary sales, feesalty fee, transaction fee, and secondary sales data to fill gaps in publicly available datasets.

The Sandbox recorded $0.6 million in primary LAND sales volume on 165 parcels minted in Q3‘22. The sales are wholly attributable to private sales conducted with brand partners that recently joined the ecosystem. Private sales to brand partners are often used to bootstrap the formation of a new community within The Sandbox, which will be built and supported by the underlying brand partner. These private sales are typically followed by a public sale to mint and distribute additional LAND parcels in the surrounding area. The party purchasing LAND through a private sale is often not revealed until the subsequent public minting event has been announced.

The $0.6 million in primary LAND sales in the most recent quarter is a steep 93% decline from the $7.7 million in Q2 sales and a continuation of the trend since the Q1’22 peak. This decline is at least partially attributable to the ~39% QoQ collapse in average USD/SAND conversion rate, with SAND ending the quarter at $0.85 and averaging $1.11 throughout Q3. The price of SAND peaked in Q4’21 at ~$7.62 and has since fallen 89% as of Sep. 30, 2022.

Using LAND mints as an imperfect proxy for LAND parcels sold, average sales price during the latest quarter was ~$3,344 per unit, which has rebounded from the $2,156 estimated average sales price for Q2. However, this rough estimation neither accounts for the rarity of the parcels (normal vs. premium) nor other qualitative variables that may impact the price of any individual parcel (e.g., location).

Non-LAND Primary Sales

Non-LAND primary sales represent other NFTs sold and used within The Sandbox Ecosystem. The category refers primarily to Partner IP Avatar Collections, ASSETS, and User-Generated Content (UGC is currently only available in a limited capacity and not available for purchase). Due to the collaborative nature of the partner IP collections, these sales tend to be more volatile in regularity and size.

During Q3, The Sandbox generated $1 million in non-LAND primary sales. Most of these sales came through Special IP partners (typically in-game avatar NFTs) driven by People of Crypto and Steve Aoki’s Avatars and Metazoo collections. Specifically, Special IP collections sales accounted for ~$790,000, while general in-game ASSETs accounted for the remaining ~$220,000. This compares very favorably to the $257,000 in non-LAND primary sales captured in Q2, representing a 293% increase QoQ. The high growth speaks to the irregular cadence in which these sales are generated. Also, the undulating sales may be an indication that markets have somewhat stabilized since the highly turbulent Q2 months.

Revenue

Revenue for The Sandbox can be divided into three main categories:

- LAND & ESTATE primary sales via public auction or private sales.

- Non-LAND primary sales via Special IP collections, avatars, and in-game ASSET NFTs.

- Royalty fees and transaction fees are generated on secondary sales volume and public primary sales volume, respectively, as a 5% commission. The Sandbox Foundation and The Sandbox Company split this fee evenly (2.5% each).

Historically, Primary LAND & ESTATE sales have typically accounted for 65%-95% of total revenue. The second largest revenue contributor has historically come from royalties, given the large volumes from LAND trading on the secondary market. Transaction fees are a function of primary sales and have typically only accrued meaningful revenues when LAND minting volumes are high. Of the three main categories, Non-LAND primary sales have often been the smallest contributor to revenue due to the inconsistency of transactions, which are often non-recurring and dependent on the brand partners that collaborate with The Sandbox.

Total revenue for Q3 landed at $2.1 million, down 78% QoQ. Q3‘22 primary sales only generated $20,700 in transaction fees, down 73% QoQ. The decline in transaction fee revenue is primarily the result of a pause in public LAND minting in Q3, along with a delay in Special IP collection launches as partners have chosen to wait for market conditions to improve. The $500,000 in Q3 royalties was a notable 69% QoQ dropoff on account of a 68% decline in secondary sales volume. In contrast to typical trends, non-LAND primary sales ultimately led the revenue categories in Q3, with $1.0 million in sales.

As all of The Sandbox’s revenue and sales volume is denominated in SAND, the 39% depreciation in USD/SAND average conversion rate was a major driver of the revenue figures listed above. The other major driver being general risk-averse buying behavior demonstrated by market participants that impacted all risk assets, and especially those more speculative categories such as digital assets.

Secondary Sales Volume

Despite experiencing a 68% QoQ drop, secondary sales remain the leading contributor to USD volumes for The Sandbox, with the vast majority coming from g LAND parcels trading. Secondary sales peaked at $283 million in Q4 2021, followed by a 97% retracement over the three consecutive quarters since. The $8.8 million in Q3’22 volume is actually the first YoY decline in quarterly secondary sales that have been recorded, given the rapid rise in 2021 LAND sales has made for a difficult comp period while in the depths of this bear market.

The QoQ drop in USD volumes is driven entirely by the average selling price of LAND, given that The Sandbox actually saw a 47% increase in the number of secondary LAND sale transactions in Q3. This price decline is at least partially caused by the ~39% QoQ fall in average USD/SAND conversion rate in the most recent quarter, which has fallen as low as $0.84/SAND and has averaged $1.11 throughout Q3 ($1.84 average in Q2).

Network Activity

The number of distinct wallets purchasing land (“Active LAND Buyers”) continued to slide in Q3 to 1,970 unique buyers, down 42% QoQ. This follows last quarter’s 57% QoQ decrease from the 7,805 active buyers recorded in Q1‘22 and well below the ~15,000 distinct wallet addresses recorded during the Q4‘21 peak. The number of distinct land parcels changing ownership (“Active LAND IDs”) declined at a steeper 61% QoQ, as landowners have seemingly braced for the deepening bear market.

As referenced in our previous report, participants in Alpha Seasons can also be used as a proxy indicator of network activity. Alpha Season 3 started on August 24 and will be open until Wednesday, November 3. Per gameplay figures provided by The Sandbox, 341,000 players have thus far participated in AS3, representing a ~16% increase from AS2, with one more week remaining in the current season. Average playtime per user also increased an impressive 88% from 203 to 382 minutes, which aligns with the increase in experiences this quarter to ~90 compared to ~35 in Alpha Season 2. Additionally, peer-to-peer engagement has risen through the past three seasons, with chat messages per user growing from two in AS1, to five in AS2, and most recently reaching 29 messages per user in AS3.

Qualitative Analysis

The Sandbox Ecosystem: Notable Events

Partnerships, Integrations, and Investments

Source: The Sandbox

Note: Recently announced partnerships plan to unveil their location through a future LAND auction and thus aren’t currently reflected on the game map.

As highlighted on the new metaverse map, now with enhanced 1×1 LAND parcel detail, The Sandbox partner community continues to grow in both size and diversity. Given the recent turbulence in the market, many partners have chosen to delay the launch of their special IP NFT collections until conditions stabilize. However, throughout Q3, new partnership announcements continued to roll in. As a result, the list of likely partner IP collections to launch down the road has grown. The following entrants were welcomed into The Sandbox community:

- Gaming

- FaZe Worldby FaZe Clan (gamified experiences to engage with one of the world’s largest gaming organizations).

- Sofstar Metapark by Softstar (experiences showcasing IP from the classic PC games developed by this iconic Taiwanese brand).

- Monkeying Around Experience by Animoca Brands’ Metaprints and Forj.

- Atari is showcasing two exclusive experiences during Alpha Season 3 (Sunnyvale and Crystal Castles)

- Music

- deadmau5 Tower of Light collection and playable experience in Alpha S3.

- Steve Aoki “Metazoo” NFT Collection and Aoki Avatars for use in the Aokiverse Alpha Season 3 experience.

- The Sandbox launches WMG LAND and Sueco’s “Split Personalities” experience in The Sandbox Alpha Season 3.

- Avenged Sevenfold launched their first experience in The Sandbox in Alpha Season 3.

- Entertainment

- Care Bears virtual experience developed for Alpha S3.

- The Walking Dead NFT collection and multiplayer survival game in Alpha S3.

- Paris Hilton announced experiences for fans to celebrate Halloween and interact with her in her virtual Malibu Mansion.

- Playboy’s “MetaMansion” digital gaming experience is based on the Rabbitar community.

- Hell’s Kitchen with Gordon Ramsay by ITV Studios opens up the first “virtual restaurant” and chef-themed game in The Sandbox.

- Diversity and Inclusion

- People of Crypto Lab’s debut as the first-ever diversity, equity, and inclusivity hub in the metaverse.

- Metaverse Prideas part of the “Sandbox Belonging Week” contains three unique experiences.

- Fashion and Lifestyle

- ISART Digital School, an exhibit in the NFT Institute experience in Alpha S3.

- Tony Hawk and Autograph partner to create the largest virtual skatepark ever made along with an accompanying NFT collection of avatars and skateboards.

- ComplexLand 3.0 by Complex Networks, a collab with The Sandbox that will focus on streetwear and sneaker culture within the metaverse.

- Traditional Industries & Infrastructure

- Keb Hana Bank to provide banking services via a virtual branch in the metaverse in an effort to cater to the next generation of customers.

- AXA Hong Kongjoins the Mega City cultural hub within The Sandbox to engage with customers in a new interactive way.

- Renault Korea Motors to offer digital automotive experiences as a new medium of customer engagement.

- DBS BetterWorld launched to showcase the Singaporean bank’s ESG principles and engage with customers.

The Sandbox Invests $1.7 million in INDEX GAME

In addition to the growing list of brand partners planning to invest their resources to build within its metaverse, The Sandbox also announced an investment of its own in Q3. In August, INDEX GAME, a Hong Kong-based metaverse agency, welcomed a $1.7 million investment from The Sandbox. The agreement includes an option for The Sandbox to increase its investment up to $6 million by 2023.

Launching in 2021 as just a small independent game studio, INDEX GAME has expanded its scope over the past year by developing a wide array of play-to-earn style content, adding robustness to virtual worlds. The metaverse agency has worked with over 15 brands and IPs to build engaging experiences within The Sandbox. As more brands and industries choose to onboard into the virtual world, INDEX GAME will now be able to work even more closely with The Sandbox to better facilitate the conversion of these IPs into immersive experiences.

The Sandbox Alpha Season 3

Source: The Sandbox

On August 24, The Sandbox launched its highly-anticipated Alpha Season 3 event. This third installment lasts 10 weeks, making it the longest season to date. Over these weeks, participants can access more than 90 digital experiences while completing quests and leveling up their avatars. As with past seasons, there are numerous raffle opportunities for prizes as well as a leaderboard for those seeking competitive play. In fact, the leaderboard has been tweaked via the implementation of Ethos Points, which players gain by completing quests. A certain number of Ethos Points will be awarded depending on the difficulty of the challenge and how the player performs compared to peers. The top 5000 players will earn SAND tokens, and at the end of the season (November 3) the first-place winner will earn a whopping 30,000 SAND (USD $25,000).

The Sandbox and The Sandbox Game Maker Fund will be responsible for ~37 available experiences. One of the emblematic features of Season 3, however, is the vast diversity in “experiences” representing well-known brands across traditional and crypto-native media and entertainment, including:

- Snoop Dogg

- The Walking Dead

- Deadmau5

- Sueco

- Warner Music Group

- Ubisoft’s Rabbids

- The Smurfs

- Steve Aoki

- Care Bears

- Atari

- BAYC

- World of Women

- Metapride

Even more refreshing will be the 12 user-generated content (UGC) experiences from independent creators as well as the 16 “Game Jams” contest submissions that will be competing for SAND.

Beyond Season 3, The Sandbox is preparing multiple experiences around brands’ and celebrities’ universes to create more immersive experiences for their individual communities and highlight new ways to engage in the metaverse.

Source: The Sandbox

Additionally, for the first time, “playable external avatars” have been introduced into The Sandbox. This means that some of the most iconic NFT brands have been integrated into the game as voxelized avatars, with their owners able to play as them. The debut of these “external avatars,” along with the implementation of guaranteed SAND awards for those playing with avatars closely partnered with The Sandbox, are just some of the ways TSB is attempting to reward their most loyal, crypto-native players.

On July 12, Sandbox announced that all users could now publish the assets they create using the Game Maker tool. At the moment, these custom experiences can only be shared publicly through the Game Maker Gallery. However, eventually, the minting and sale of these assets as NFTs on The Sandbox Marketplace will also be made available. This rollout represents another step in the development of enhanced LAND functionality for LAND owners. The core investment thesis behind LAND speculation sits the expectation that one day landowners will be able to monetize their parcels via immersive in-game experiences.

Enhanced SAND Staking Option for LAND Owners

On September 22, The Sandbox unveiled a new “high APR” SAND staking option for LAND owners. LAND owners on the Polygon network are eligible to receive increased SAND rewards when they stake their SAND tokens. This program will distribute up to 250,000 SAND rewards per week for the first 12 weeks, with a cap of 500 SAND able to be staked at the higher APR per LAND parcel owned by the user. Notably, The Sandbox team developed a tool to detect LAND transfers, meaning LAND owners will not need to lock their land in the staking contract to be eligible for the increased SAND rewards. As such, LAND owners will be able to stake their SAND while maintaining complete custody of their digital assets.

This release comes as The Sandbox continues to seek ways to deliver additional value to LAND owners, with a focus on rewarding the loyal users choosing to remain in the ecosystem during this bear market. While this new staking option is exclusive to LAND owners, all TSB users can stake their SAND through the existing SAND staking contract or earn additional SAND through liquidity provided via the SAND/Matic Pool. The various staking options available are displayed in the Staking Dashboard, able to be viewed when users sign into their profile page on The Sandbox official website.

Roadmap

Enhanced Integration with the Creator Economy via User-Generated Content

Currently, in-game “user-generated content” (UGC) on land parcels is limited in scope and availability, but there are plans to gradually roll out additional functionality as the development of The Sandbox continues. With the unlock of asset creation for all users via the Game Maker tool, The Sandbox team has demonstrated its commitment to adding value for landowners. This unlock is a step in the direction that users have been waiting for. At the moment, UGC can only be shared via the Game Maker Gallery, without an option to list these in-game assets to The Sandbox’s marketplace. However, The Sandbox team has relayed plans for further functionality by the end of 2022.

The Sandbox has also partnered with Digital Hollywood, a school for human resource development in IT and digital content. This partnership was described as an opportunity to train voxel artists and game makers in Japan, preparing them to create content in The Sandbox. This move aligns with a global trend focusing on the expansion of the “creator economy,” which mirrors many of the same principles of Web3. The Sandbox’s business model, which is rooted in the free flow of digital goods from independent creators to users, fits perfectly in this global shift toward creator empowerment.

Full Transition to Layer-2

In an effort to promote sustainable, more affordable participation in the ecosystem, the following features are expected to transition to Polygon over the coming year:

- LAND sales on Polygon (the next public minting event will be held on Polygon)

- LAND staking features

- ASSET smart contract to be deployed/bridged

- Open ASSET minting contract to be deployed

- ESTATE creation and modification

- Experience publishing on LAND through Polygon

Closing Summary

In Q3, a chill swept through the crypto gaming space as crypto summer turned to winter – an extension of trends that began in Q2. User figures, sales, and general trading activity all fell with many market participants entering “hibernation”. Many of these same trends impacted KPIs we track for The Sandbox. However, The Sandbox team has no plans to hibernate.

While some users have surely left the ecosystem, who remains are the crypto-natives. Here to stay, they were treated to the latest Alpha Season, which focused on rewarding The Sandbox’s most loyal users and NFT holders. Alpha Season 3 brought with it the most content yet. It also showed off one of The Sandbox’s biggest strengths – an ability to procure partnerships and develop a community that melds the traditional and crypto worlds into one.

Even now, as the market freezes over, new partners have chosen to invest time and resources into this virtual world. For many brands, The Sandbox will be their first venture into “the metaverse”. That’s a powerful reputation that will pay dividends to The Sandbox and its loyal users for years to come. In the meantime, though, the core team should continue focusing on delivering rich, new experiences, while empowering creators that will ultimately shape its future.

________________________________________

Looking to dive deeper? Subscribe to Messari Pro. Messari Pro memberships provide access to daily crypto news and insights, exclusive long-form daily research, advanced screener, charting & watchlist features, and access to curated sets of charts and metrics. Learn more at messari.io/pro

This report was commissioned by The Sandbox, a member of Protocol Services. All content was produced independently by the author(s) and does not necessarily reflect the opinions of Messari, Inc. or the organization that requested the report. Paid membership in Protocol Services does not influence editorial decisions or content. Author(s) may hold cryptocurrencies named in this report.

Crypto projects can commission independent research through Protocol Services. For more details or to join the program, contact ps@messari.io.

This report is meant for informational purposes only. It is not meant to serve as investment advice. You should conduct your own research, and consult an independent financial, tax, or legal advisor before making any investment decisions. Past performance of any asset is not indicative of future results. Please see our terms of use for more information.

Let us know what you loved about the report, what may be missing, or share any other feedback by filling out this short form.