Key Insights

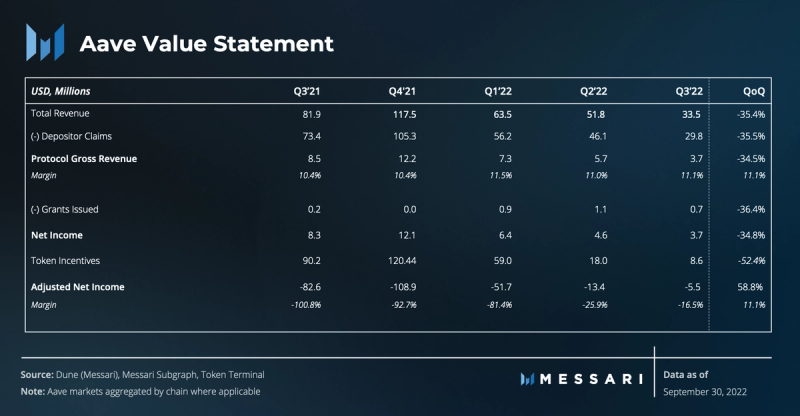

- Uncertainty in the broader market resulted in a decline in the demand for stablecoin leverage and led to a 35% reduction in revenue for Q3.

- Within 24 hours of Optimism launching a 90-day liquidity mining program on Aave, outstanding debt increased from $5 million to $790 million as users implemented recursive borrowing strategies aimed at maximizing incentives.

- Aave Companies recently released an update that noted their expectation to launch the native GHO stablecoin on the Aave V3 Ethereum market in Q4’22.

- Aave DAO voted to freeze markets on Harmony and Fantom following an exploit of the Harmony Horizon Bridge.

- Aave Dao voted to compensate Aave Companies $16.3 million for the development of Aave V3.

A Primer on Aave

Aave is a decentralized money market protocol that facilitates depositing and borrowing of various crypto assets. The protocol has two main versions (Aave V2 and V3) and is deployed across various Layer-1 chains and Layer-2 networks with the majority of activity on Ethereum, Avalanche, and Optimism. Outside of the core permissionless lending business, the protocol has introduced various complementary products such as a stablecoin (GHO), an open social protocol (Lens Protocol), and a permissioned instance of the core Aave protocol (Aave Arc).

Note: Data from the Polygon V2 market is not included in this report. We will be working in the coming months to improve access to this data.

Financial Performance

Due to lingering effects of the centralized lender collapse in Q2, and growing uncertainty in global markets, user demand for leverage contracted in Q3 and led to a 35% drop in revenue from $51.8 million to $33.5 million.

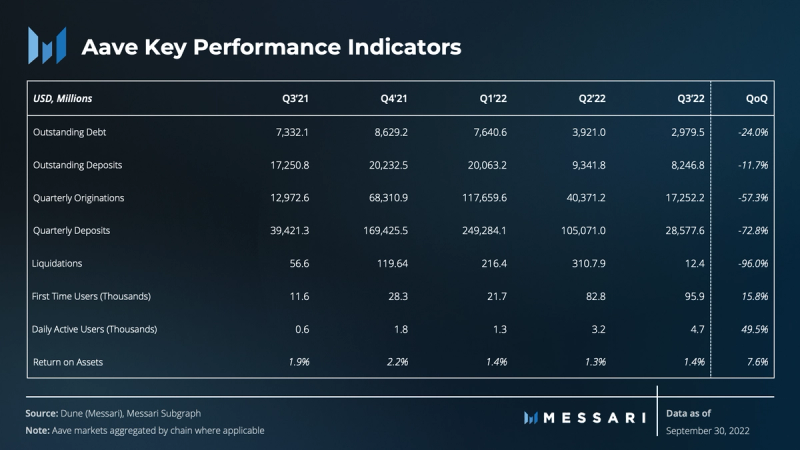

The overall revenue decrease in Q3 was the result of a 42% drop in outstanding debt. Simultaneously, the utilization of deposits decreased from 42% to 36%.

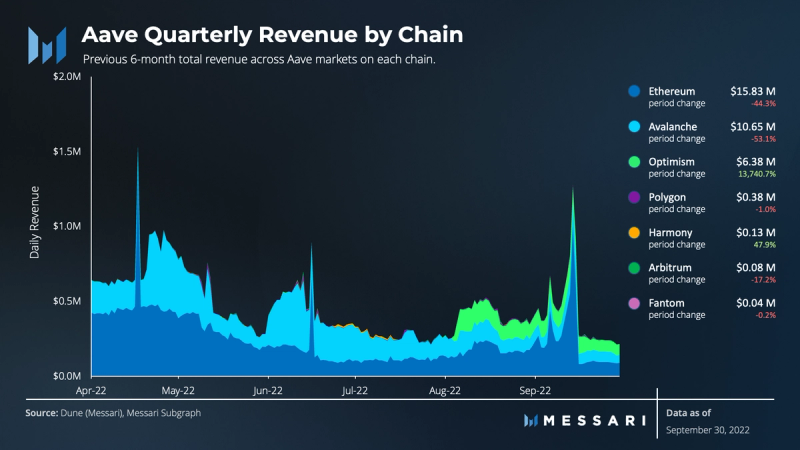

After outperforming in Q2, revenue generated from the Avalanche market reached new lows, falling 53% in the quarter from $22.7 million to $10.6 million. A decrease was anticipated to happen due to abnormally high utilization of deposits, while users recursively collateralized borrowed funds to maximize their share of Avalanche Rush liquidity incentives. The AVAX incentives issued by Ava Labs continued throughout Q3. However, the incentives fell 75% from $10 million to $2.5 million as quarterly originations were down 87% and debt repayments outweighed borrowing by $1.6 billion. Notably, USDT was the only major asset to have increased revenue on the Avalanche market due to a sustained 90% utilization rate and a $39 million increase in daily outstanding debt.

In August Optimism launched its own 90-day liquidity mining program with a distribution of 5 million OP tokens to users of Aave on Optimism. Within the first 24 hours of the program, the total value of deposits increased from $42 million to $1 billion and the total value of outstanding debt increased from $5 million to $791 million, surging utilization from 13% to 74%. As seen with Avalanche Rush, OP incentives offset the borrowing rate below the interest rate paid to depositors, allowing users to recursively collateralize borrowed funds and earn nearly risk-free yield. OP rewards totaled $1.1 million in Q3, and this incentivized usage led to an increase in daily revenue, from $315 pre-liquidity incentives to $110,000 post-liquidity incentives. Similar to Avalanche Rush, Optimism’s liquidity mining program and the resulting revenue surge come at no cost to Aave. However, the surge is not expected to continue once the program ends in November.

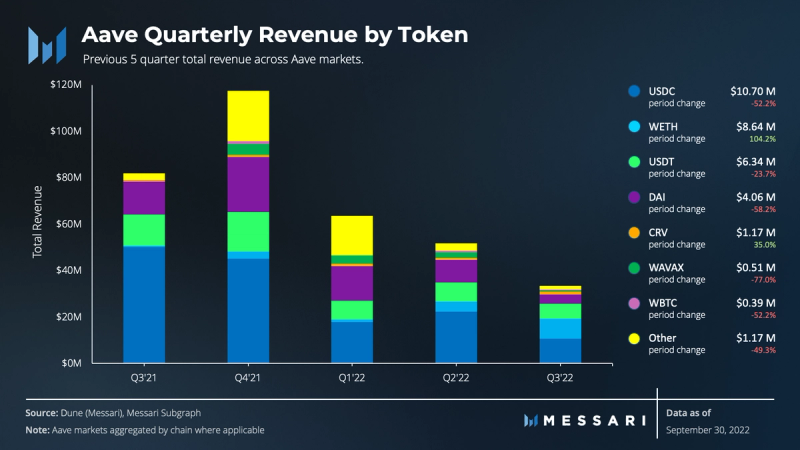

After contributing as much as 98% of all revenue in Q3 ’21, stablecoin revenue share fell from 82% in Q2 to 60% in Q3. The loss in revenue share is attributed to two things, a decrease in stablecoin demand and a 104% increase in Wrapped ETH (WETH) revenue. The share of WETH revenue increased from 8% in Q2 to 25% in Q3 as borrowing demand surged leading up to the Ethereum Merge. The fall in stablecoin revenue was not shared evenly as USDC and DAI revenue contributed 62% and 26%, respectively, to the fall in stablecoin revenue. Both revenue streams decreased roughly 59% in the quarter, while Frax and USDT revenue remained the strongest of the stablecoins dropping 18% and 23%, respectively.

Operational Performance

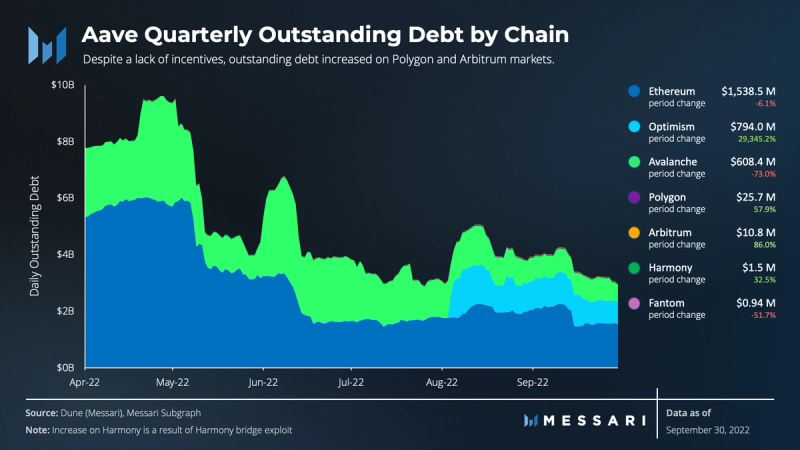

Repayment of outstanding debt on Avalanche contributed the most to the decline in cumulative debt balance. By the end of the quarter, outstanding debt on Avalanche totaled $608 million, a decrease of 73% or $1.65 billion when compared to Q2. This resulted from the unwinding of recursive borrowing strategies used to farm liquidity mining incentives from Avalanche Rush. At the end of Q2, 87% of Aave’s Avalanche deposits were stablecoins with a utilization rate of 75%. However, by the end of Q3, utilization fell to 51% as $1.8 billion in stablecoin deposits were withdrawn from the Avalanche market.

On the other hand, Aave’s Optimism market saw outstanding debt increase from $2.7 million to $794 million over the quarter. This steep increase was due to the launch of Optimism’s 90-day liquidity mining program and resulted in the same recursive stablecoin borrowing strategies seen on Avalanche. Within the first 24 hours of the program, the total value of stablecoin deposits on Aave’s Optimism deployment jumped from $32 million to $884 million and stablecoin utilization increased from 15% to 85%. At the end of the quarter, stablecoins accounted for 85% of deposits on Aave’s Optimism deployment. Once OP incentives expire in November, stablecoin deposits are likely to fall by roughly $550 million as the stablecoin share of deposits falls in-line with other non-incentivized markets.

On Aave’s Ethereum market, outstanding debt only decreased by 6%. However, the value was supported by a 26% increase in the quarter-end price of ETH. In addition to the contraction in stablecoin demand, Celsius repaid $238 million in outstanding debt from July 1-August 4. At the time, this repayment equaled roughly 15% of all debt on the Ethereum market and cleared the remaining debt for the well-known Celsius wallet.

Despite a lack of liquidity mining, Aave V3 markets on Polygon and Arbitrum experienced organic growth in Q3, as both had increased quarter-end deposit and debt balances. On the Arbitrum market revenue from WBTC was the biggest contributor to performance due to increased utilization from 9% to 18% as token supply increased by 94%. On the Polygon market WMATIC had a similar effect as WMATIC utilization increased from 36% to 41% while token supply increased by 82%. In both cases, revenue was supported by users borrowing and selling the assets in hope of repurchasing them at a lower price to repay the debt and profit the difference, aka “shorting.”

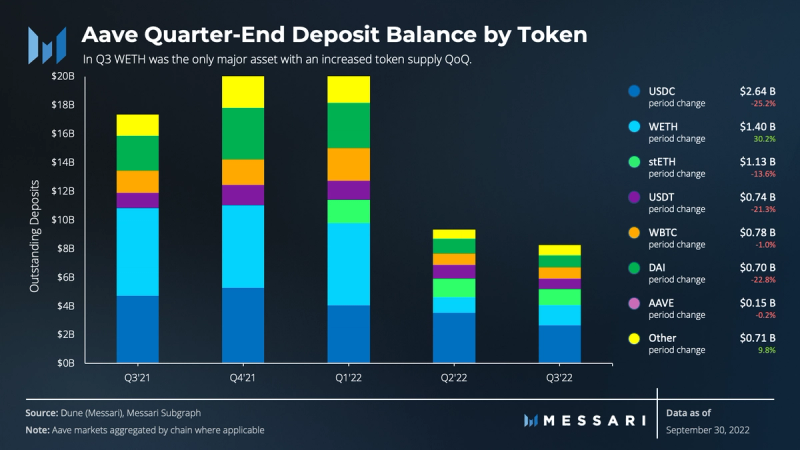

Between the unwinding of leverage strategies and rotation of capital between markets, outstanding deposits fell 12% in Q3. USDC supply decreased by $891 million and accounted for 81% of the overall decline. This decline resulted from a $1.2 billion decrease in USDC supply on the Avalanche market partially offset by increases on Optimism, Polygon, and Arbitrum markets. WETH supply grew 4% on a token basis and is the only major asset to have a net inflow in spite of a 30,000 WETH withdrawal from Celsius. In total, the Celsius wallet withdrew $605 million of assets from Aave’s Ethereum market including 17% of the WBTC supply ($118 million) and 31% of the stETH supply ($410 million). While stETH token supply never recovered following the withdrawal, WBTC token supply partially recovered and ended the quarter with a 3% decline. At the end of the quarter, only 617 stkAAVE remained in the Celsius wallet on the Aave V2 Ethereum market.

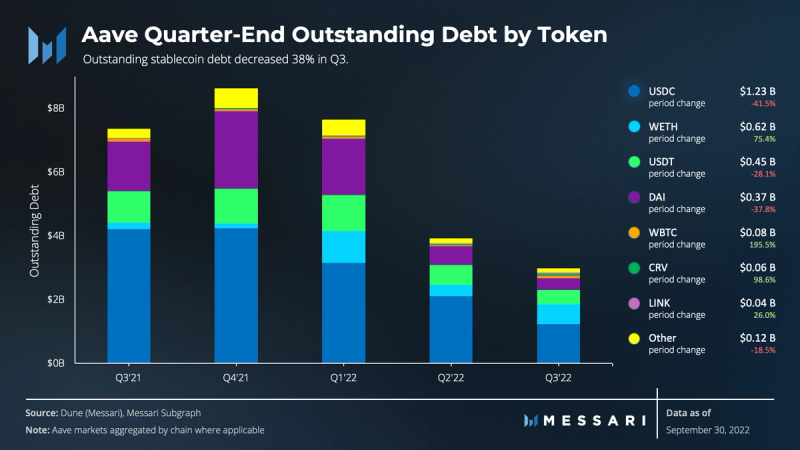

On the originations side, stablecoin debt fell 38% in the quarter. When compared to Q2, net of Celsius repaying $193 million USDC and $45 million DAI, the decrease was proportionally consistent (28%-32%) across the three major stablecoins (USDC,USDT, and DAI). For the remaining smaller cap stablecoins, the cumulative debt balance fell 32%. However, the balance was not proportionally shared across the assets.

Debt denominated in Synthetix USD (sUSD) and Binance USD (bUSD) increased 41% and 60%, respectively. The increase in sUSD is the result of a 75% supply cap increase from $20 million to $35 million, while the increase in bUSD debt is likely the result of a 20% overall market cap increase from $17.6 billion to $21.1 billion. Simultaneously, Fei and Frax balances dropped 92% and 60%, respectively, due to external factors. In August, TribeDao, the team behind Fei, announced their dissolution and 1Fei:1Dai redemption plan. The resulting liquidity shrink of Fei posed a liquidation risk for Aave, which led to a freeze of the Fei market and $6.2 million of repayment in the quarter. In September, Frax Finance launched their own borrowing and lending market, FraxLend, which led to a $14.4 million reduction of Frax debt on Aave.

With support from increased quarter end prices, the debt balance for non-pegged assets increased 56% as users sought to profit from the broader market declines by “shorting” these assets.

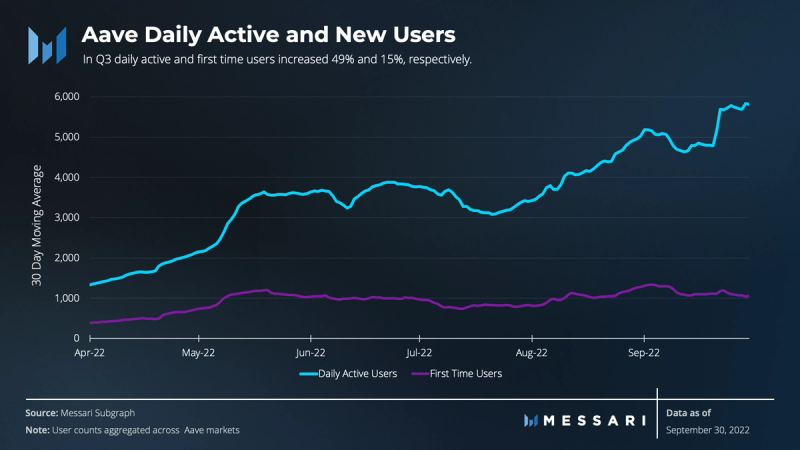

Supported by Aave V3 usage, overall user activity increased in Q3. The Optimism market led the way as daily active users (DAU) increased from 204 to 1,318 users. Following Optimism, the largest increases were on Arbitrum and Polygon. DAU on Arbitrum increased from 518 to 988, while Polygon active users increased from 670 to 1,051. All other markets experienced a decrease in DAU.

The Merge

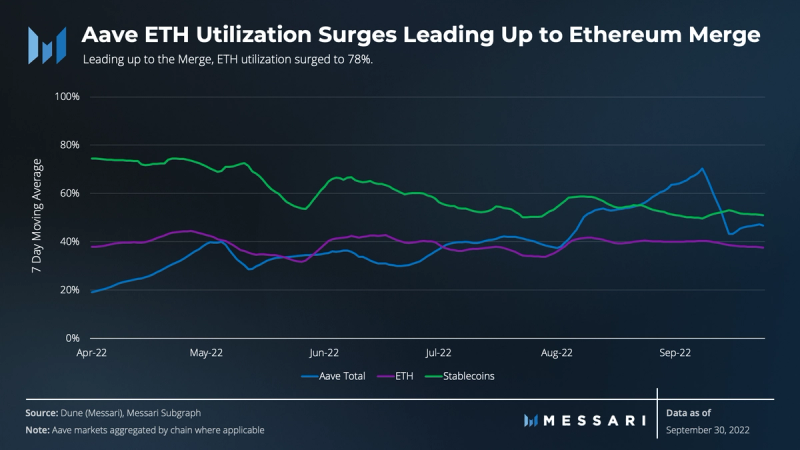

Leading up to the Ethereum Merge, borrow demand for ETH surged as an ETH Proof-of-Work (ETHPoW) airdrop encouraged speculators to hold ETH in their wallets. This combined with an on-going recursive stETH/ETH strategy pushed the utilization rate of WETH to 78% before Aave Governance executed a proposal to pause ETH borrowing. Abnormally high utilization paired with incentive to withdraw ETH deposits posed an insolvency risk that the quick actions of the Aave community ultimately mitigated.

The pause lasted for 10 days and borrowing was re-enabled on September 18. In the 5 days leading up to the Merge, 33% of ETH deposits were withdrawn from Aave on Ethereum, and supply interest rates reached 70% APY as the utilization rate spiked to 100%. The day following a successful Merge, utilization dropped back down to 46% as more than $550 million of ETH was repaid.

Qualitative Analysis

Aave Freezes Two Markets

In Q3, the Aave community voted to freeze depositing and borrowing on two of its markets, Aave V3 on Harmony and Aave V3 on Fantom. The first freeze in July, followed a $100 million attack on the Ethereum side of the Harmony Horizon ERC20 bridge, causing certain bridged assets on Harmony to have un-backed value. Aave uses Chainlink oracles for price feeds, and those price feeds are for the underlying tokens on Ethereum Mainnet and not the bridged tokens. Because of this distinction, arbitrageurs deposited exploited tokens of a lesser, un-reported “real” value and unexploited, borrowed assets, specifically ONE and LINK. Prior to the freeze, the utilization of LINK and ONE shot up to 100%, and ONE borrowings accounted for roughly 80% of all outstanding debt on Harmony.

With repayment of outstanding debt unlikely and liquidations not happening due to the Chainlink oracle not accounting for the “real” value of the exploited bridged assets, users took to the Aave forum to discuss a path toward retrieving their lent-out assets. At the time of writing, there has been no official word on a solution. However, the Harmony team released a statement outlining a plan to deploy treasury funds toward recovery. At the end of the quarter, deposits on Harmony’s market totaled $3.2 million and outstanding debt totaled $1.5 million.

With the rippling effects of the Harmony attack still fresh, the second freeze was in September. This one came upon execution of a proposal to freeze Aave V3 on Fantom due to a lack of traction and dependence on the Multichain bridge. At the time of the proposal, the Fantom market had $9 million in deposits and $2.4 million in outstanding debt, generating around $30 in daily fees for the Aave treasury. At the end of the quarter, deposits totaled $3.3 million and outstanding debt totaled $940,000. There has been no further discussion in the Aave forum regarding the future of Aave V3 on Fantom.

Aave V3 Ethereum and GHO

In mid-October, Aave Companies provided an update for two of its two largest roadmap objectives: the deployment of Aave V3 on Ethereum Mainnet and the launch of GHO. In March, Aave V3 was launched and deployed to six blockchains. Ethereum was not among the six. Aave V2 on Ethereum is the protocol’s largest market, and for security amongst other reasons the community chose to upgrade the V2 smart contracts over a new deployment. Following a recent forum discussion initiated by community partner Bored Ghost Development, the protocol pivoted as Aave DAO voted in favor of a new deployment.

GHO is the forthcoming overcollateralized ERC20 stablecoin, native to the Aave protocol. The stablecoin introduces the concept of “Facilitators.” Once approved by Aave DAO, they can mint a limited amount of GHO in a trustless manner. The Aave V3 Ethereum market will be the initial Facilitator at launch and will allow users to borrow GHO while earning yield on their deposited collateral. Because GHO is minted upon borrowing and burned upon repayment/liquidation, traditional interest rate models cannot be relied upon. Therefore, rates will be statically chosen by Aave Governance with the benefit of discounted rates for stkAAVE holders.

Another key feature is that the protocol retains 100% of interest revenue from GHO, compared to 10% on other assets. If GHO is able to attract demand from the market, Aave DAO is likely to see a significant increase in adjusted net income. However, it is probable to see revenue increase at a faster rate than net income as AAVE tokens are likely to be distributed from the Ecosystem Reserve to incentivize a V3 liquidity migration and/or demand for GHO. While there is no official deployment date for GHO and Aave V3 on Ethereum, the update stated “the new market is expected to be deployed in the coming weeks.”

Governance and Grant Expenses

In July, Aave Governance executed a proposal to enter a strategic partnership with Balancer, one of the largest DEXs by TVL. As part of the execution, a token swap was performed where the Aave DAO received 200,000 BAL in exchange for 16,907 AAVE from the Ecosystem Reserve. The motivation behind this initial transaction is that Aave DAO can create a veBAL holding by pairing the acquired BAL with sufficient ETH to be deposited into the Balancer V2 BAL:ETH (80:20) pool. Onced locked, Aave could then direct BAL rewards to pools that support Aave’s aTokens, ideally increasing outstanding deposits on Aave and/or AAVE token liquidity. This transaction placed Aave DAO as the 24th largest BAL holder and Balancer DAO as the 83rd largest AAVE holder, furthering synergies between the two governance communities.

Following a successful launch of Aave V3, the Aave community voted to retroactively fund Aave Companies $16.3 million for the development and audit of Aave V3 smart contracts, which introduced new features such as High Efficiency Mode, Isolation Mode, and Portal. Together these features provide additional risk management parameters that allow for increased capital efficiency and a seamless flow of assets between Aave V3 markets on different networks. The payment consisted of $6.3 million in AAVE tokens staked in the Safety Module with one and two year cliffs, $6.6 million in stablecoins, and $3.4 million in higher volatility assets. Since launch, Aave V3 has generated $3.8 million for the Aave treasury equating to a 42% annualized return on investment.

Following risk analysis and technical support from the broader Aave community and partners such as Gauntlet and BDG Labs, five new collateral assets were added to Aave markets. These additions include 1Inch, LUSD, MiMatic, stMatic, and MaticX. Additionally, as part of Gauntlet’s continued parameter recommendations, a total of 12 adjustments in risk parameters were made across 5 Aave V2 assets. These assets include WBTC, CRV, LINK, DAI, and ENJ and were driven by simulations that aim to balance three core metrics: insolvencies, liquidations, and borrow usage. In a September forum post Gauntlet outlined their progress and anticipated timeline for integrating V3 markets into their simulation platform.

The grants program was extended in May with a total Q2 and Q3 budget of $3 million for grants, around $2.5 million for general marketing, and $350,000 for operations. Since inception in May 2021, Aave Grants Dao has disbursed $5.5 million with an acceptance rate of 19% across 1,000+ applications. In Q3, grant funding decreased 36% from $1.1 million to $698,000 with applications and integrations being the most awarded category. Notable grants include Flexible Voting and Shippooor. Flexible Voting will allow AAVE token holders to deposit their tokens into Aave while still participating in governance votes. Shippooor is building an analytics dashboard that will allow users to measure changes in the health factor of a position against changes in market prices.

Closing Summary

Despite the market’s wavering appetite for leverage, the Aave community continues to broaden its reach as the leading decentralized lending protocol. For the third consecutive quarter, first time users and DAUs increased. Financial performance declined alongside peers, which led to a higher focus on risk management and protocol optimizations. Q4 looks bright as the team prepares to launch its native stablecoin GHO and deploy the more efficient Aave V3 market to the Ethereum Mainnet. Both objectives are likely to improve cash flows for the Aave treasury, although token incentives may be needed to bootstrap adoption.