How are you doing, anon? It’s been a tough year. Risk assets have had a rough go of it in 2022. Stocks are down ~20% year to date, while Bitcoin and Ethereum are down ~60%. Yet since July, crypto prices are up in the face of a steeply declining macro backdrop. Rejoice!

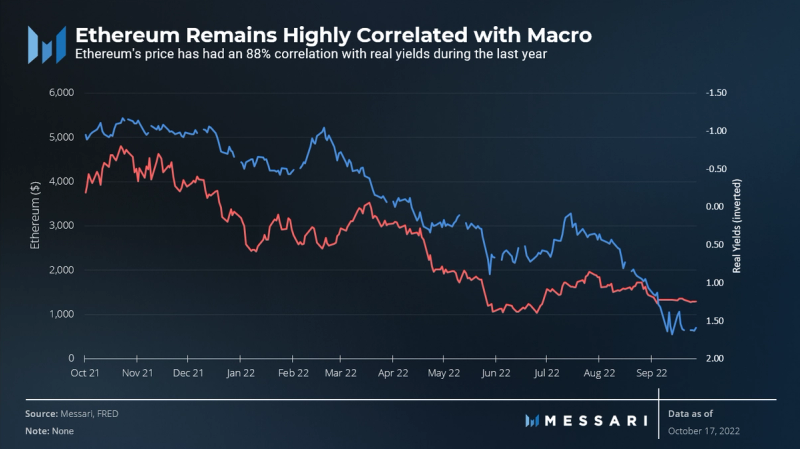

Still, even the most ardent crypto supporter would agree it will be challenging for the asset class to have sustained momentum against the specter of a global recession. Crypto has continued to have a strong correlation to the broader macro environment, particularly if we look at baseline alternatives like real yields (interest rates adjusted for inflation).

With that in mind let’s take a tour around the macro landscape to see where we stand today and where we may be headed for the rest of 2022.

Company Earnings

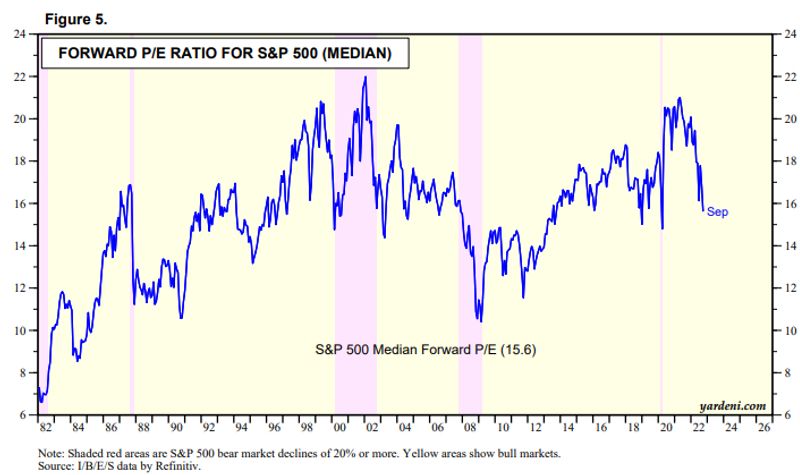

Investors understand monetary policy is tightening, but they are closely watching how companies are responding to these changes. When buying a stock, you are technically buying its earnings into perpetuity. The aggregate of these earnings across companies can help tell us if the market is over- or under-valued. Historically, the S&P 500 is roughly valued at around 15x on a price-to-earnings (P/E) basis. Looking at extremes, the dotcom cycle had the S&P 500 peaking in September 1999 at ~22x for forward earnings and ~30x for trailing earnings. Valuations on a P/E basis are now in line with the median over the last 40 years.

Source: Ed Yardeni

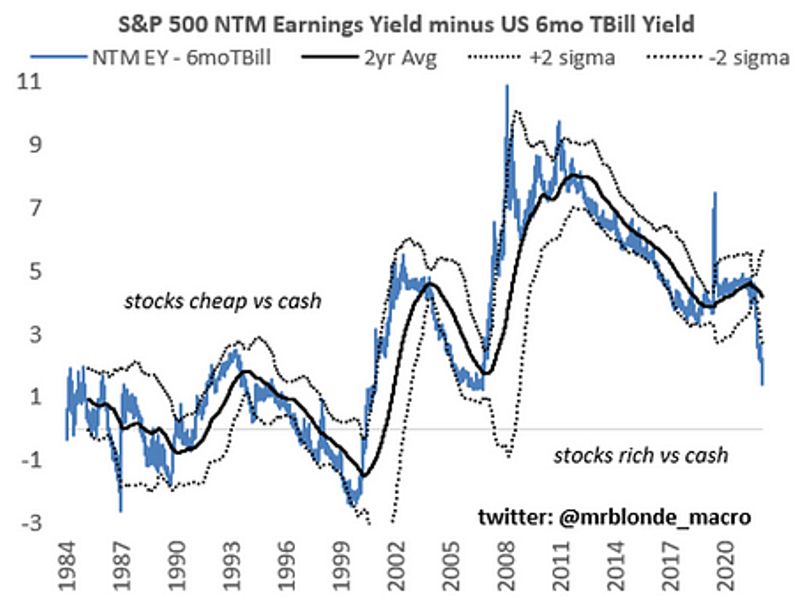

Does that mean it’s time to sound the all-clear and start moving into risk assets? Not quite. With yields rising sharply, comparing stocks to cash doesn’t give investors a very attractive choice. Risk assets, whether they be equities or crypto, are going to have a tough time competing with what will likely soon be ~5% risk-free yields from US treasuries. Risk assets are still historically expensive when compared to bonds.

Source: Mr. Blonde

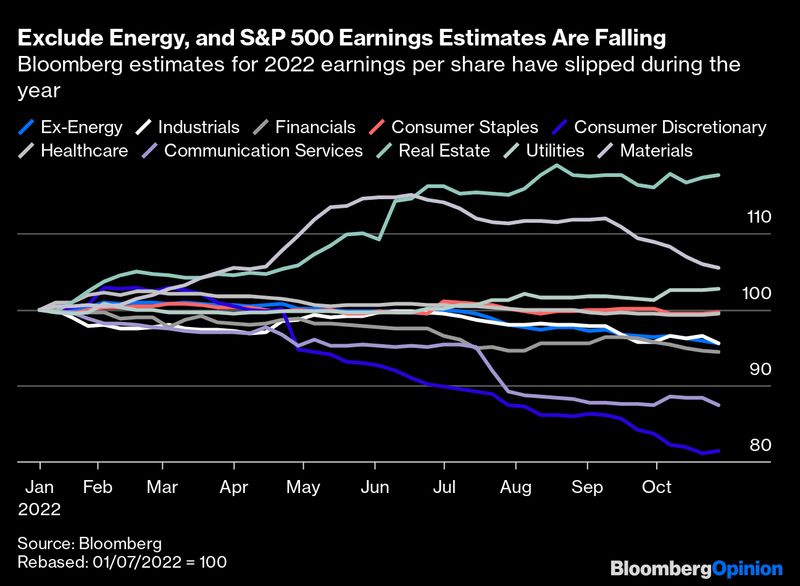

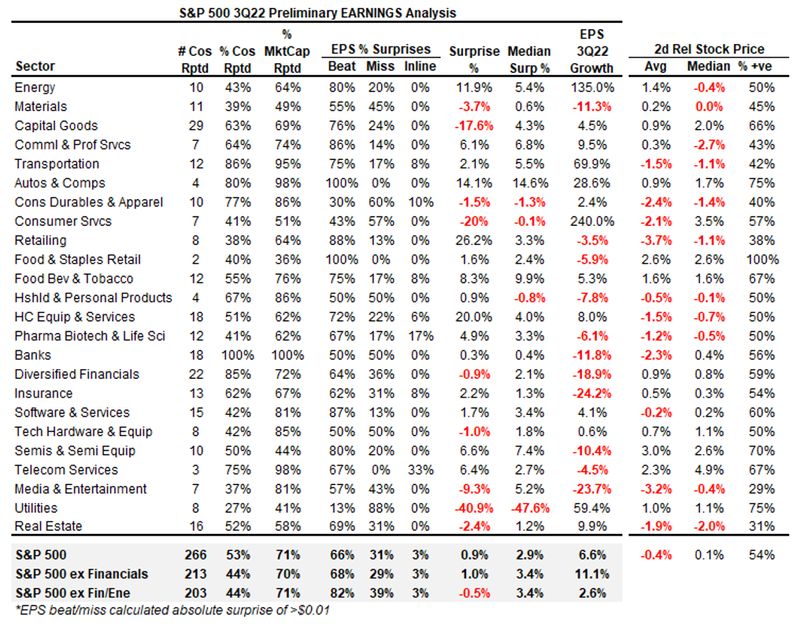

Stocks may continue to get cheaper based on the slowdown in company earnings. Earnings season is nearly complete with over half of companies in the S&P 500 reporting.

We’ve had some big misses in tech with Meta and Google both whiffing on their consensus estimates by wide margins. Even favorable numbers by stalwarts such as Amazon were hampered by a poor forward outlook.

A handful of tech stocks make up almost a quarter of the biggest stock index in the world, so their direction continues to swing sentiment. Exclude energy, and the forward guidance across sectors was fairly bleak in Q3.

The energy sector has shouldered a furious rally on the back of rising oil and natural gas prices. Earnings per share for this cohort are up over 100% since Q3 2021. Other staples such as transportation and utilities also came along for the ride. This is classic “risk-off” behavior as investors move into assets they know will have demand regardless of the broader economic picture.

Source: Mr. Blonde

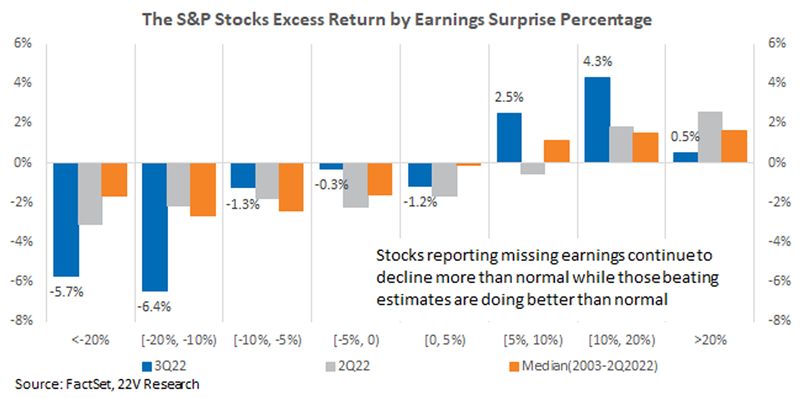

Interest rates are a key pillar for investors when determining where to allocate capital. It’s challenging to consider ETH at ~4.0-5.0% yields when treasuries are yielding a commensurate amount. The Federal Reserve (Fed) is preaching data dependence as it evaluates the path of interest rates. That means every major data release and company earnings report is under that much more of a microscope.

The market is certainly listening. Companies that miss earnings expectations are getting punished even more than usual. The average drop for a miss is 5% — the worst figure in a decade.

The market is hanging on every statement by the Fed. We have seen ~2% drops, or billions of dollars in value, erased based on a few simple words. The press conference by Fed Chair Jerome Powell on November 2 was clear evidence of this.

Source: Bloomberg

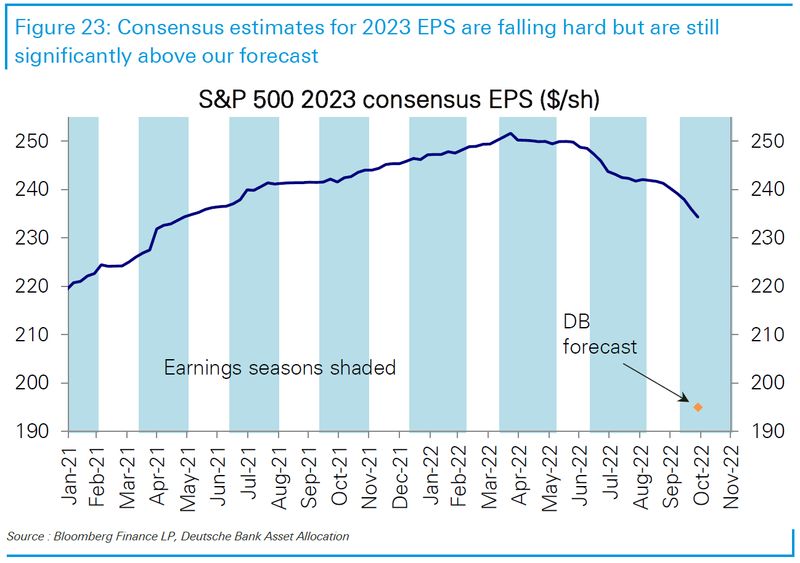

Despite the challenging earnings backdrop, the market is still pricing in a “soft landing” for equities. Essentially, the market believes that U.S. company earnings will not materially suffer in 2023 despite rising interest rates and high inflation. The average estimates for earnings per share in 2023 are back to the level analysts estimated before this recent inflationary spike. Some sell-side firms like Deutsche Bank have materially different forecasts, almost 20% lower than the current estimates.

Sentiment and Positioning

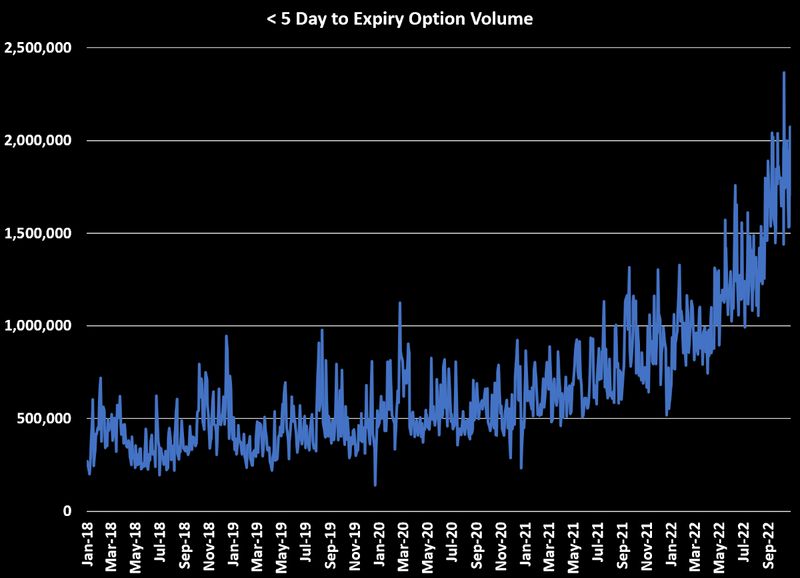

So companies are starting to feel the pain of inflation, but how are traders allocating for the next leg up or down? Positioning in aggregate is net short, but that hasn’t stopped speculators. Speculation continues to run rampant with short-dated call option buying accelerating. The GameStop saga may have materially changed investor attitudes.

Source: Bloomberg

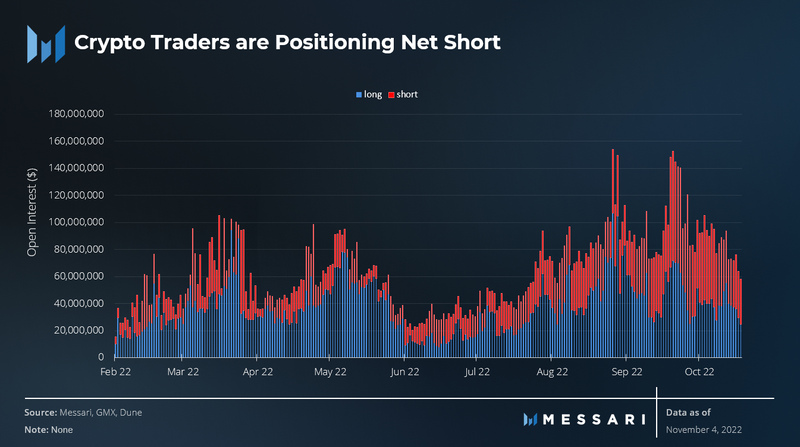

Crypto traders are also increasingly positioning net short. By evaluating trading data on GMX, we find a strong basis on bets to the downside.

Inflation

At the end of the day, inflation is where the buck stops. The Fed will continue to tighten until we see the whites of the eyes of inflation. Powell has made that clear.

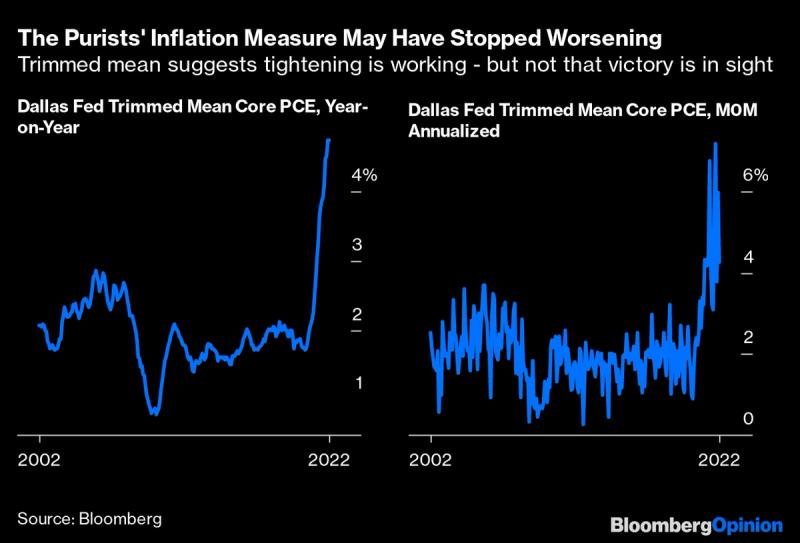

Whatever flavor of CPI you are into, be it core, headline, trimmed mean, or otherwise, the numbers are still unacceptably high. Headline inflation is still above 8%. Even after stripping out the more volatile components (food, energy, used cars, etc.), we still have inflation well over 4%.

While we are starting to see some of the components begin to come down, such as housing, the biggest issue is the continued rise of wages. The Fed is continually reminded of the wage-price spiral of the 1970s. Accelerating wages are a major red flag for this regime, and wage growth and job growth both remain extremely strong.

Wages are up over 5% year over year. Job openings (measured by JOLTS)continue to expand, and individuals still feel comfortable enough to leave their jobs at record levels (measured by QUITS). Despite economists expecting a decline, job openings rose from ~400,000 to 10.7 million on the last business day of September. For inflation to slow, the Fed has said through multiple channels it wants to see the labor market slow down. There is no evidence of this yet.

Looking at the actual underlying inflation in the economy outside of employment, we do see some encouraging signs. The prices paid component of inflation (PPI) is in a free fall. This is a strong leading indicator of inflation going forward. Companies are continuing to pay less for goods, which should eventually filter through to consumer prices.

Source: Bloomberg

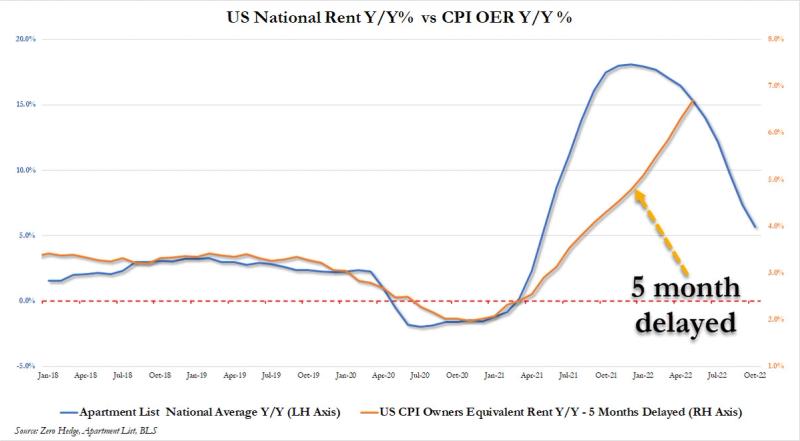

PPI is important to see where we are going, but the headline numbers you see on TV will continue to be high. Housing is the biggest component of CPI (via owners’ equivalent rent or “OER”). Unfortunately, this piece of the puzzle operates on a serious lag of at least 3-6 months. So while inflation may be coming down, it will take some time to see it in the headline numbers.

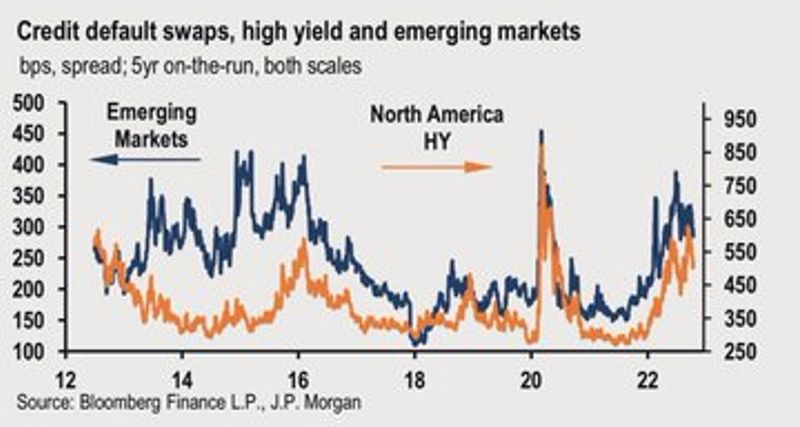

The Fed will likely err on the side of overtightening rather than undertightening — it has been very clear in its communications. Credit is the key data point the Fed uses to understand if it’s moving too fast on hiking interest rates in its fight against inflation. Currently, all signs point to no. Credit default swaps, or the price of default risk on companies, remain well within normal levels.

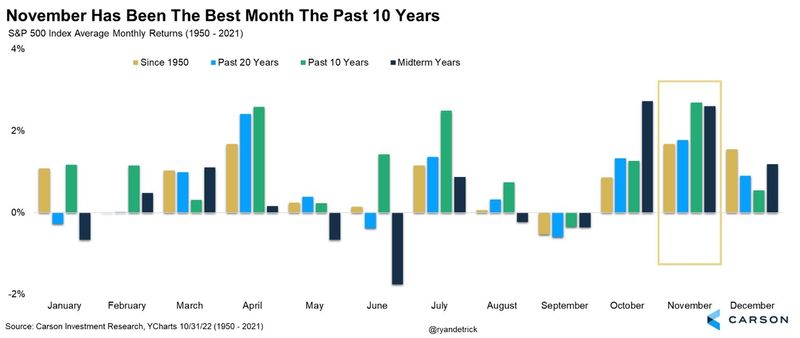

Election Season

Despite broader market turbulence, one of the key pillars for the bull case has been that sitting politicians will help the market along with favorable policies due to upcoming elections. Historically, this has proven true as November tends to be a strong month for markets.

Not only has November been good to investors, but forward-looking estimates have been particularly strong after midterm elections. This is especially true when there is a divided Senate/House which we are projected to have based on current polling.

Outside the U.S.

Meanwhile, the European Central Bank (ECB) recently committed to its second consecutive 75 bps hike. It was too late to help control prices. Inflation was up 10.7% year over year. Core inflation was 5%.

The European region is pushing on a string with energy driving the bus. Energy prices rose 6.5% from September and 41.9% year over year. Germany is bearing the brunt of the pain with inflation rising 11.6% in October. With winter approaching, this is not an encouraging recipe.

Source:Bloomberg

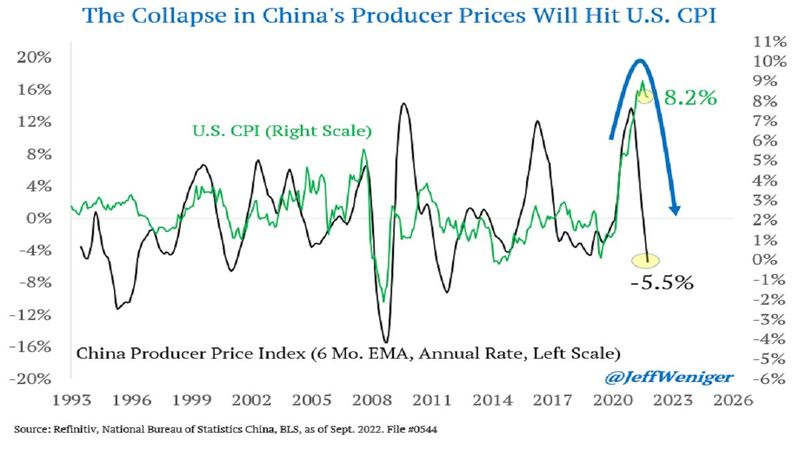

In China, prices are collapsing in part due to economic shutdowns driven by the zero-covid policy. As an importer of a material amount of goods from China, lower prices are a good thing for the U.S. inflation picture.

Wrapping Up

Geopolitical tactics — in the form of strategic realignments, on-shoring, re-shoring, de-globalization, and persistent supply chain adjustments — are virtually guaranteed to define the macro outlook for the next decade. In the near term, monetary policy will remain restrictive for the rest of 2022.

Yet, markets are forward-looking; will we see more accommodative policies in 2023? Perhaps.

Regardless of the macro picture, there is the possibility for crypto to forge its own path and move away from the correlation it continues to exhibit with equities. Today, 41% of institutional investors hold crypto, and an additional 15% plan to hold digital assets in their portfolios within the next few years. The biggest impediment to broader adoption continues to be regulatory clarity.

If we have clear regulations, we will see flows into crypto. Macro finally won’t matter. Unfortunately, in the near term, we have to continue reading the tea leaves with Mr. Powell until that day comes.