Key Insights

- The Staked aTokens proposal represents a critical puzzle piece in the long-term strategies of Aave and Balancer, allowing Balancer liquidity providers (LPs) to borrow against their liquidity pool tokens as collateral.

- If approved, the proposal lays the foundation for a go-to-market strategy for GHO that avoids using Aave-native incentives. The strategy leverages Aave-held veBAL to incentivize Balancer LP collateral while using Aave’s ability to control GHO borrow rates to bootstrap GHO liquidity.

- If GHO is successful, the stage would be set for Aave and Balancer to experience significant total value locked (TVL) growth, creating a legit stablecoin contender built on capital-efficient liquidity from two DeFi giants.

Introduction

Aave and Balancer have a long-standing relationship, dating back to January 2021. Each protocol has since evolved. Aave continues to execute on its roadmap, planning to release an overcollateralized stablecoin, GHO. Balancer is doubling down on its ambition as a baseplate protocol, using vetokenomics to align LP incentives with protocol growth. Though each path is unique, the mutual benefits of Balancer integration have never been clearer.

The latest Aave proposal, Staked aTokens: A New Aave Primitive Exploring Vote-Escrow Economies, is the next step in this partnership. If approved, the proposal would lay the foundation for a cross-chain go-to-market strategy for GHO that avoids using Aave-native incentives. The strategy would leverage Aave-held veBAL to incentivize Balancer Boosted Pools while using Aave’s ability to control GHO borrow rates to attract lenders and bootstrap GHO liquidity. To contextualize the proposal and its implications, we’ll observe each protocol’s roadmap and how it binds them closer together.

Balancer: The Liquidity Stack

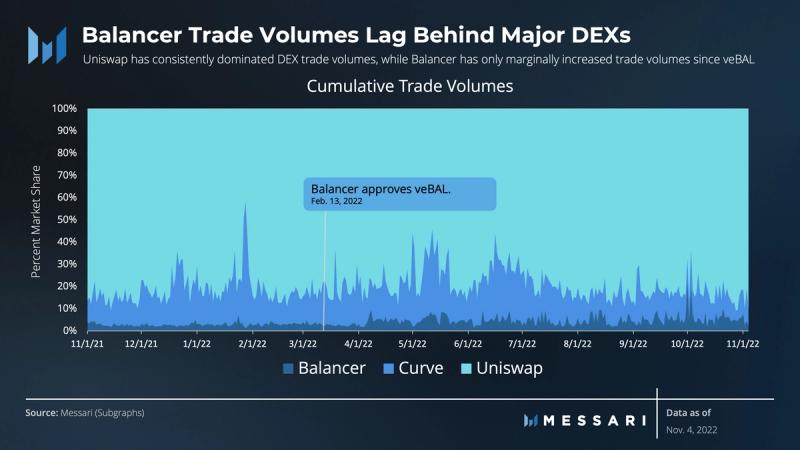

Balancer competes for TVL and volume with decentralized exchange (DEX) giants Uniswap and Curve. In a move to attract liquidity and grow partnerships, Balancer introduced a vote escrow (ve) tokenomics framework. The new tokenomics allows LPs of the 80 BAL / 20 ETH pool to stake their Balancer Pool Tokens (BPT) to earn veBAL. veBAL holders can direct BAL emissions to LPs or themselves and accrue a portion of protocol revenue. While veBAL tokenomics has dramatically affected Balancer operations, the protocol is still waiting for liquidity, TVL, and volumes to catch up with Uniswap and Curve.

While not without growing pains, in the eight months since launching veBAL, Balancer has sprouted an entire ecosystem of applications and markets on top of its base layer. The veBAL ecosystem comprises a marketplace of liquid locker providers and bribing markets. However, new use cases and composability for Balancer Pool Tokens (BPTs) are lacking. A deeper Aave integration would be the start, providing leveraged LP opportunities with the added benefit of socializing boosted yield from veBAL emissions.

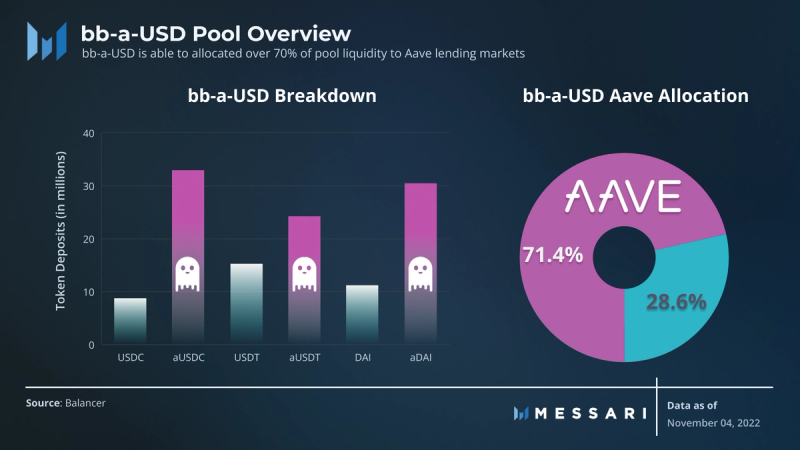

Boosted Pools are the most relevant innovation on Balancer for Aave. These pools increase capital efficiency for depositors by sending idle tokens to lending markets (currently only Aave) to accrue interest. Boosted Pools can be compared to Balancer’s staBAL3-USD pool, an equal-weighted DAI/USDC/USDT pool. If there were no trading volume in the staBAL3-USD pool, it would earn zero yield. By comparison, Balancer’s bb-a-USD meta pool comprises three Boosted Pools (bb-a-USDC, bb-a-USDT, and bb-a-DAI) and would still generate yield in the result of zero trading volume as over 70% of the pool’s assets are yield-bearing aTokens. Boosted Pools additionally provide greater swap efficiency as they’re composed of Phantom BPTs, which abstract away the costs of minting and burning LP tokens.

bb-a-USD is the third largest pool on Balancer with over $122 million TVL. As LPs continue to search for new ways to increase yield, boosted pools offer a unique, risk-averse solution. If only there were a way to leverage BB-A-USD positions…

Aave: All Systems GHO

Messari previously published a comprehensive overview of the GHO proposal, but the Aave roadmap extends far beyond the proposal itself. Unlike other lending markets, Aave has direct control of the borrowing rate for GHO. Since Aave mints GHO, there are no depositors, eliminating interest rates based on utilization. Thus, Aave controls a powerful mechanism to drive collateral to the protocol. Aave can influence GHO supply and the nature of collateral that backs GHO by adjusting GHO borrow rates across its portfolio of supported collateral assets. Aave can even affect Safety Module collateral by adjusting the GHO borrow rate discount provided to Safety Module stakers.

Aave V3 introduced a separate array of features that increased capital efficiency and security and introduced cross-chain functionality to Aave by introducing:

- High-Efficiency Mode (E-mode): maximizes capital efficiency for collateral and borrowed assets with correlated prices enabling up to a 97% loan-to-value ratio.

- Portal: allows users to bridge aTokens by burning and minting aTokens cross-chain.

Marc Zeller, Integration Lead at Aave, recently doubled down on the protocol’s wallet, social, and fintech ambitions. Aave wants to position GHO as a “center of gravity” for the Aave app ecosystem — an integrated currency for the financial and social ecosystem of Aave and Lens.

Staked aTokens: A New Aave Primitive

The latest proposal from Aave Companies, the official development lab overseeing the Aave Protocol, outlines a new aToken primitive to the Aave DAO. Staked aTokens are targeted specifically at ve protocols that allow LPs to receive rewards from gauges. The Staked aTokens concept marries the ideas explored in the previous sections, allowing liquidity providers to use liquidity positions as collateral in the Aave protocol. While Staked aTokens are protocol agnostic, the proposal approves Balancer as the first Staked aToken integration.

The technical implementation of the proposal involves the deployment of BalancerVeRouter to integrate Aave with Balancer’s VotingEscrow smart contract and allows Aave to participate in veBAL gauge voting and revenue claims. BPT assets supplied to the Aave protocol would be staked at liquidity gauges by the contracts. Aave could then pair and stake treasury-held BAL to vote for BAL liquidity emissions and boost aBPT yield.

Source: Aave Governance Forum.

The contract could additionally siphon a percentage of rewards to the Aave treasury and further bolster Aave’s governance power in Balancer. Some community members, specifically Llama, have suggested in similar proposals that Aave move up the risk curve to integrate Aura, a veBAL liquid locker, to boost yield further. While the Aave Companies team received the idea, it was dismissed until further risk analyses and audits could be conducted.

The proposal received overwhelmingly positive support from the forum and in a signaling off-chain vote. The proposal received endorsements from SolarCurve, a core contributor to Balancer, and influential delegates from Flipside and Stablenode. If successful, future proposals will select a final list of BPT assets to be included, implement the allowlist, and deploy the treasury-held BAL and ETH to the veBAL contract. The Aave Treasury currently holds 20,996 BAL, representing around 1.48% of the total veBAL supply. Once deployed, it is estimated this veBAL would control the distribution of 1,986.5 BAL per week.

All things considered, it would be foolish to assume that adding LP positions as collateral does not introduce significant risk. Paul Lei of Gauntlet took the first step of publicly addressing the security risks of the Aave proposal, including the significant impacts of LP liquidations on liquidity. Gauntlet’s initial conclusions suggest that even in perfect conditions LP collateral should be lower than any associated collateral factors.

What Comes Next?

The integration gives Aave a few distinct advantages as it looks to bootstrap GHO liquidity. Aave’s ability to leverage its BAL holdings allows it to incentivize bb-a-USD aToken leverage at essentially zero cost. Further, using veBAL and Aave’s ability to set the GHO borrow rate below the bb-a-USD interest rate, Aave can drive demand for bb-aUSD leverage, GHO collateral, and bb-a-USD/GHO liquidity simultaneously. In short, Aave can incentivize the aToken lending market through veBAL and allowing LPs the opportunity to lever their positions.

The potential for the flywheel is overwhelming when the aforementioned E-mode is factored in. Suppose Aave enabled E-mode for GHO loans against bb-a-USD Pools (i.e., up to a 97% LTV). In that case, the leverage opportunity could allow Aave to incentivize GHO liquidity and avoid liquidity mining campaigns altogether. Aave’s ability to mint native GHO on multiple chains, combined with Balancer’s cross-chain presence, would only lend to the strategy’s scalability.

Marc Zeller has continuously expressed Aave’s view of Balancer as a critical partner, outlining specifically the importance of Aave gaining veBAL influence as a critical strategy for both the safety module (which currently consists of both Aave Balancer Pool Token (ABPT) and stkAAVE) and GHO. The sentiment was further reflected in the Aave Companies’ ambitions to purchase 112,000 veBAL for 1 million DAI from Tribe DAO as part of the Fei Unwind.

As shown by Maker DAO and Curve with the original stablecoin Tri-Pool, a deep and efficient liquidity base not only creates heightened swap efficiency but also plays a significant role in maintaining stablecoin pegs during volatility.

Since Aave Safety Module stakers receive a discounted borrow rate for GHO, bb-a-USD/GHO tokenholders could also be integrated into the Safety Module, allowing GHO LPs to receive both safety incentives and discounted borrow rates.

The downstream social ambitions for GHO as the fundamental stablecoin of the Lens ecosystem become interesting as well. Imagine an Aave x Lens integration that allows a creator to take advantage of these DeFi legos. Users could interact with a one-click contract to take out a capital-efficient GHO loan against their stablecoin savings to fund a new creative project. Aave V3’s potential will continue to grow as the protocol allows its users to mint their GHO on Arbitrum, Polygon, or even StarkNet.

The Balancer x Aave partnership lays a formidable foundation for GHO liquidity. If the two protocols can successfully execute the roadmap, GHO appears well-positioned for traction and success, and each protocol should expect a notable increase in TVL.