Key Insights

- In 2022, veBAL faced many challenges, and the coordination game still needs stewardship if it is to sustainably work.

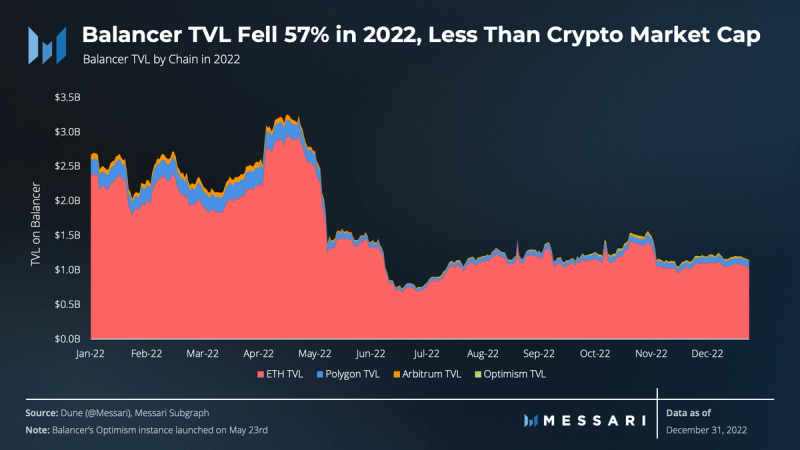

- Total Value Locked (TVL) on Balancer fell 57% in 2022, faring significantly better than the crypto market and leading peers, likely due to Balancer’s unique product offering and incentive rewards.

- Trading revenues for Liquidity Providers (LPs) continue to fall with market prices and activity. Balancer is in a unique position to offer differentiated revenue streams via boosted pools and incentive rewards.

- The Balancer DAO must continue to be mindful of the treasury, as they had a net outflow in the last two quarters.

Primer on Balancer

Balancer is a decentralized finance (DeFi) automated market making protocol using novel self-balancing weighted pools. The protocol allows anyone to create a pool of assets with predefined weights in the pool. Balancer strives to be a platform for DAOs and other protocols to build tools that provide useful liquidity to its end users and products. The protocol is managed by the Balancer DAO community and currently supports Ethereum, Polygon, Arbitrum, and Optimism (managed by Beethoven X). Since launching V2 in August 2021, Balancer’s product line has expanded to include several types of unique liquidity pool constructions.

Key Metrics

Performance Analysis

Liquidity Provider Perspective

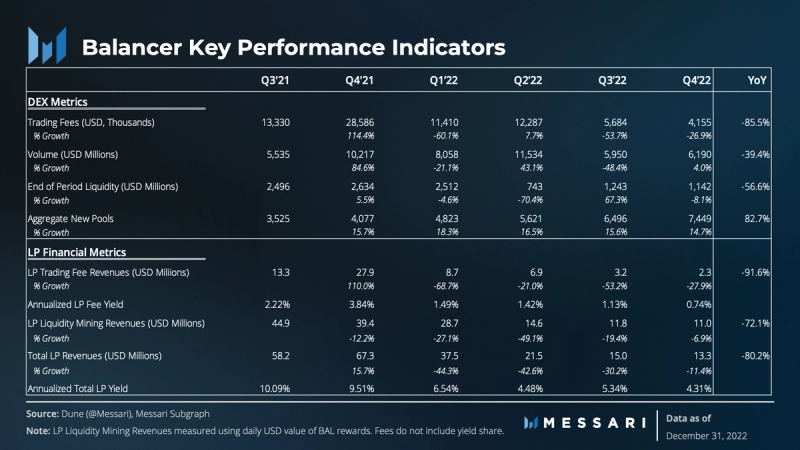

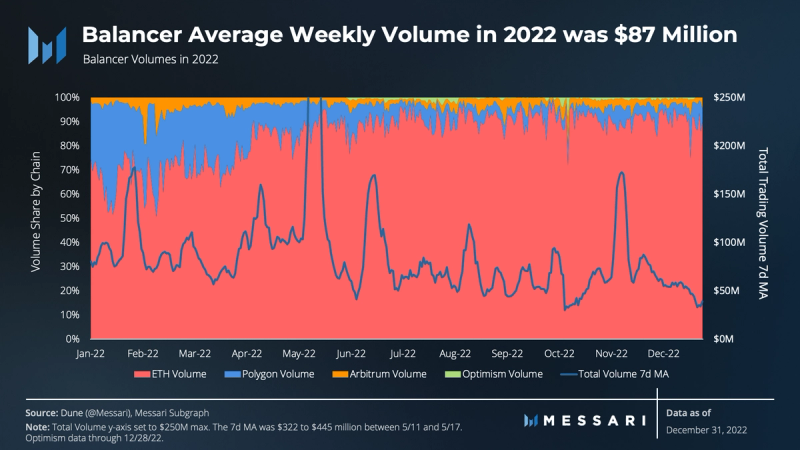

Volumes were roughly flat on the quarter, bolstered by the volatility in November around the FTX collapse. Balancer volumes on Polygon and Arbitrum increased in Q4, increasing 5% from Q3. Balancer’s decentralized exchange (DEX) volume market share increased from 3.6% in Q3 to 4.1% in Q4. It began the year with a 2.1% volume share in Q1.

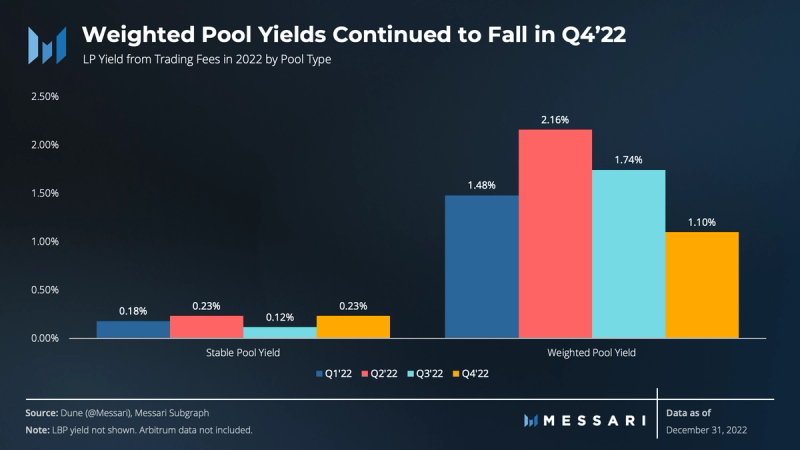

Margins on Balancer, the amount of fees paid per unit of volume traded, declined again in Q4. Stable pools typically charge lower fees (0.04% or lower) than weighted pools (typically 0.1% to 1%), making them a lower margin product. The reason for stable pools’ growing dominance of volume on Balancer is likely a combination of:

- Boosted pools are unique to Balancer. They are made up of linear pools that manage the utilization of the stablecoin between the native coin for trading and a yield-bearing receipt of the token (lent on Aave or staked). Rebalancing of the linear pools increases volumes. Many new pools in Q4 used bb-a-USD as the stablecoin pair instead of simply a stablecoin.

- In Q3, staBAL3 was 32% of volumes and bb-a-USD was 30%. In Q4, the share shifted dramatically to 13% staBAL3 and 49% bb-a-USD. StaBAL3 has a 0.005% fee while bb-a-USD has a 0.001% fee.

- In Q4, the veBAL Wars came to the fore as veBAL liquid derivatives competed for liquidity using Balancer stable pools. The primary competitors were Aura and Tetu, whose stable pools comprise BAL/wETH 80/20 BPTs and auraBAL or tetuBAL. Incentives to these pools drive volume and activity.

- Stablecoins’ share of market cap has grown as prices of other assets have dramatically fallen.

The stable pools’ growing dominance is not a phenomenon unique to Balancer, and it’s an issue all DEXs should consider. Balancer might have the clearest strategy to face the issue with their unique boosted pool strategy and precedent for the DAO to receive a share of revenues earned from yield.

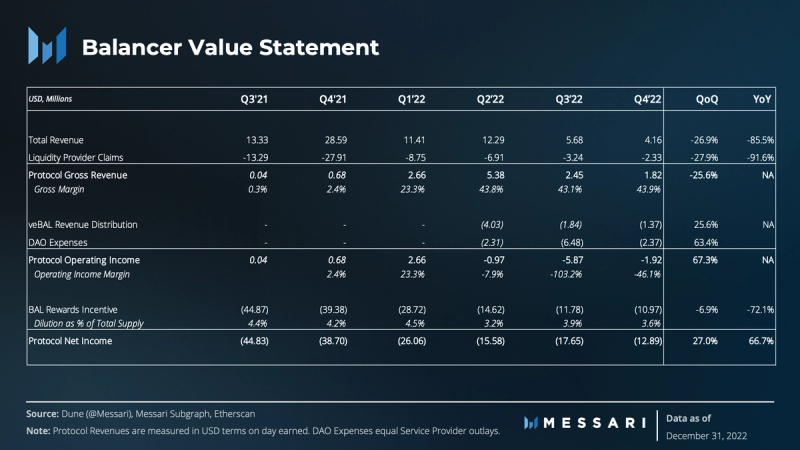

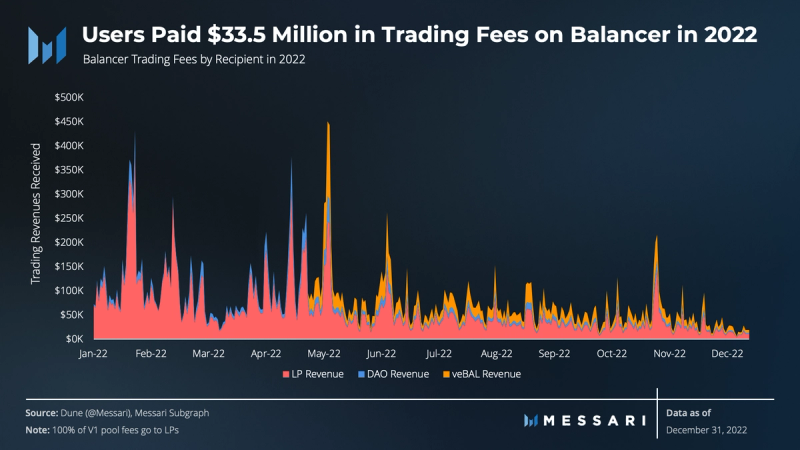

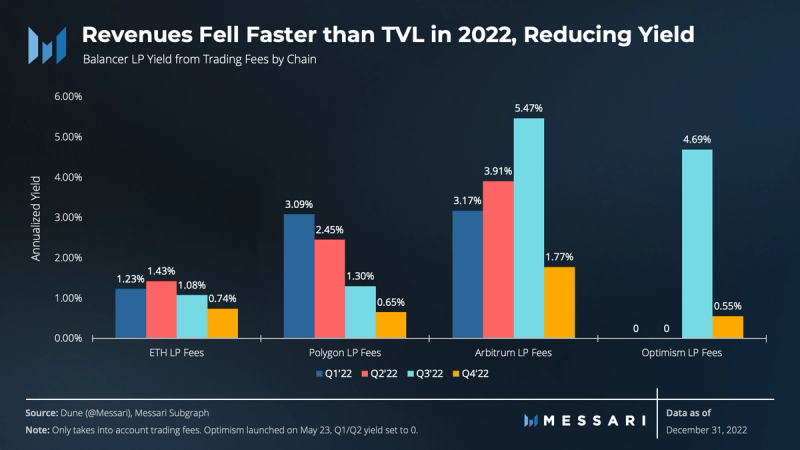

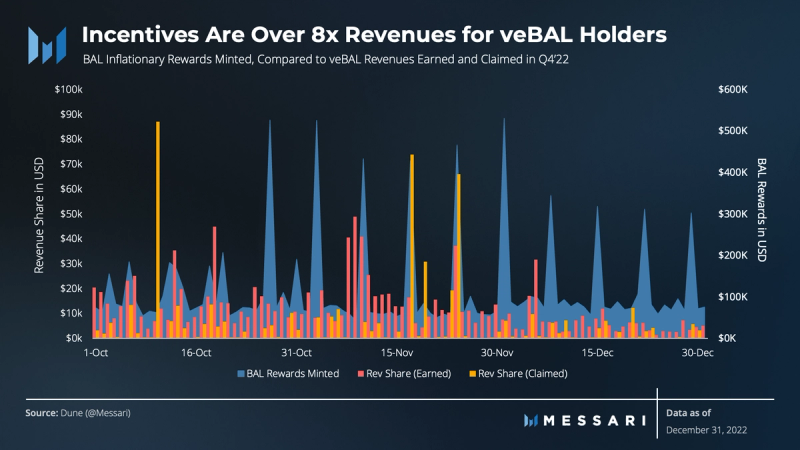

In Q4, on average per day, LPs earned $27,779 in trading fees, veBAL lockers were paid $16,232, and the DAO received $5,411. The primary variables for revenue are token prices and DEX trading activity. The fall in both led to a declining trend for Balancer across 2022, from over $108,000 in daily fees in Q1 to $49,000 in Q4.

Across chains, yield fell from 1.13% to 0.74% as BAL rewards increased the stickiness of TVL but could not incentivize trading activity. This measure does not consider yield generated from boosted pools, which would increase LP yield numbers. While volumes were +/- 6% across instances, TVL changes were more drastic. On Ethereum, TVL fell by 10%, but on Polygon, Arbitrum, and Optimism TVL increased 42%, 71%, and 20%, respectively, from September 30 to December 31. Much of the sticky TVL on Layer 2s is thanks to external incentives, primarily from Lido and Rocket Pool whose pools make up roughly 50% of the TVL on Arbitrum and Optimism with nearly 10% APRs. Unsustainable Q3 numbers after the initial launch largely accounted for the fall in Optimism yield.

Despite the fall in activity, stable pool yields climbed from Q3 to Q4. Volumes in stable pools were fairly flat over the quarter while stable pool TVL on Ethereum and Polygon fell 36% from $517 million to $350 million. Weighted pools, however, saw a slight decrease in volumes and only a 16% decrease in TVL (on Ethereum and Polygon). Most of Balancer’s boosted pools are stable pools, including bb-a-USD and b-steth-stable (wstETH/wETH). Therefore, total LP yields will be greater than just trading fees.

Trader Perspective

TVL on Balancer likely benefited from Boosted Pools, attracting stablecoin liquidity from BAL inflationary incentives. In 2022, TVL fell less on Balancer than it did on competitors Uniswap (-61%), Sushiswap (-90%), and Curve (-84%). In Q4, TVL increased on all of Balancer’s L2 instances but decreased on Ethereum.

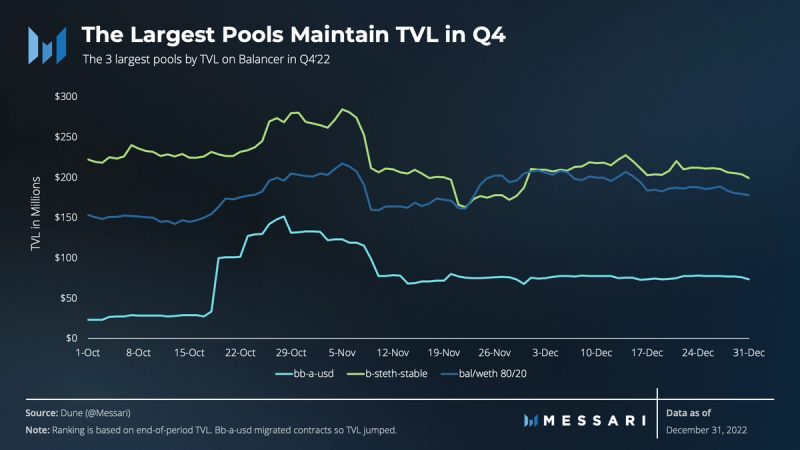

The three largest pools on Balancer now account for 40% of TVL on Balancer at $460 million, up from 33% at the start of Q3 and 39% at the start of Q4. The b-steth-stable pool, made up of stETH/ETH, received more than 50% of bribes on Hidden Hand in Q4 (~$2.8 million) to incentivize veBAL voters and increase liquidity. The bb-a-USD stable pool sports higher yields than most because of the increased capital efficiency of using Aave lending pools. The BAL/wETH 80/20 pool has maintained TVL, likely due to higher fees earned, along with the ability to lock the Balancer Pool Tokens in exchange for voting power and a share of revenues.

Featured Pool Analysis

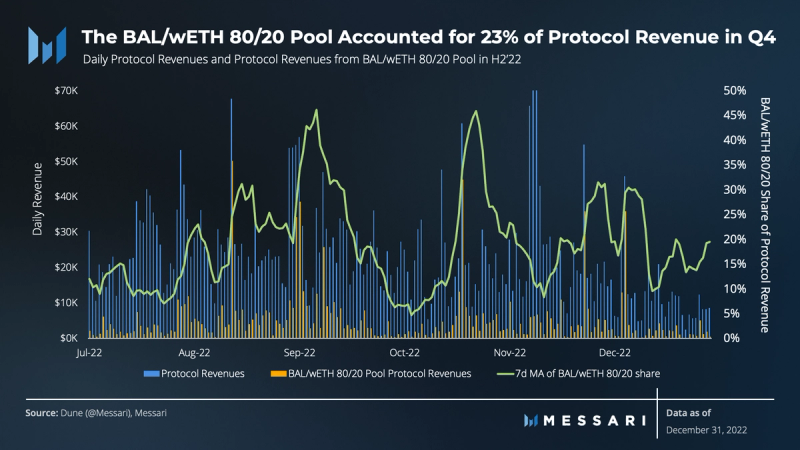

To get veBAL for governance rights and to direct BAL incentive rewards, users must create a Balancer Pool Token (BPT) by depositing into the BAL/wETH 80/20 pool and lock the BPT. That opportunity has helped make this Balancer’s second-largest pool by TVL. Interestingly, the pool has also become a key driver of protocol revenues. The veBAL pool’s share of protocol revenues has risen from 15% in Q2’22 to 22% in Q3’22 and 23% in Q4’22.

veBAL

Revenues for veBAL holders fell again in Q4, but this did not lead to less BAL locked as veBAL. Differing economic incentives can lead to a depressed yield for veBAL lockers, whether lockers are playing for price appreciation of the BPT or willing to accept a lower yield in exchange for control of BAL incentives. Conversely, a lower yield for veBAL holders implies a higher multiple on BAL, making incentives more valuable to LPs.

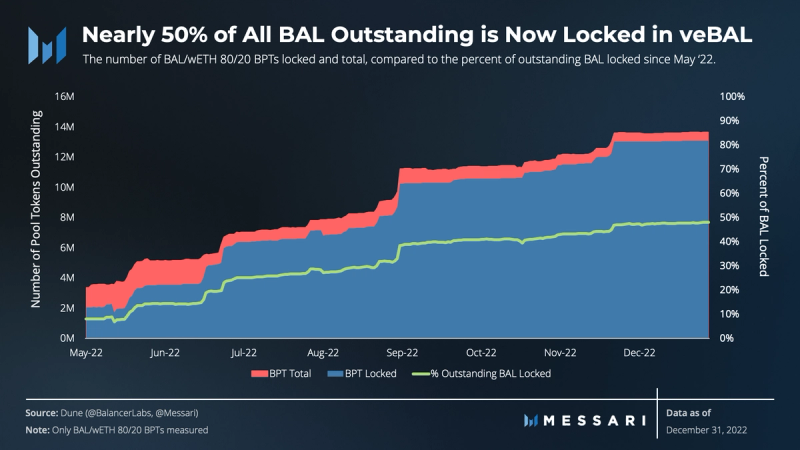

96% of all Balancer Pool Tokens for the 80/20 BAL/wETH pool are locked as veBAL. As of December 31, this accounts for 48% of all outstanding BAL tokens (54 million current supply). A higher portion of BAL locked as veBAL makes BAL price more sensitive to changes in yield. At the same required yield, more BAL locked as veBAL leads to a higher price for BAL.

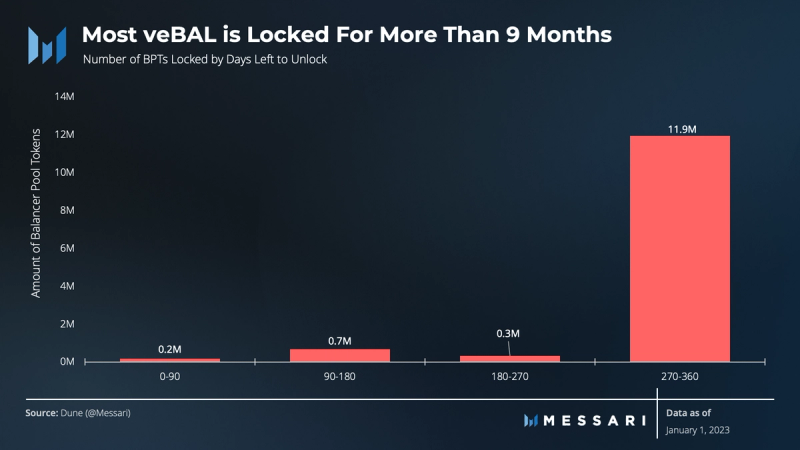

To optimize the voting power of locked BPTs for veBAL, holders must lock for longer time periods (up to one year). Presently, the number of BPTs locked as veBAL is expected to minimally change, as over 90% of veBAL is locked for more than nine months.

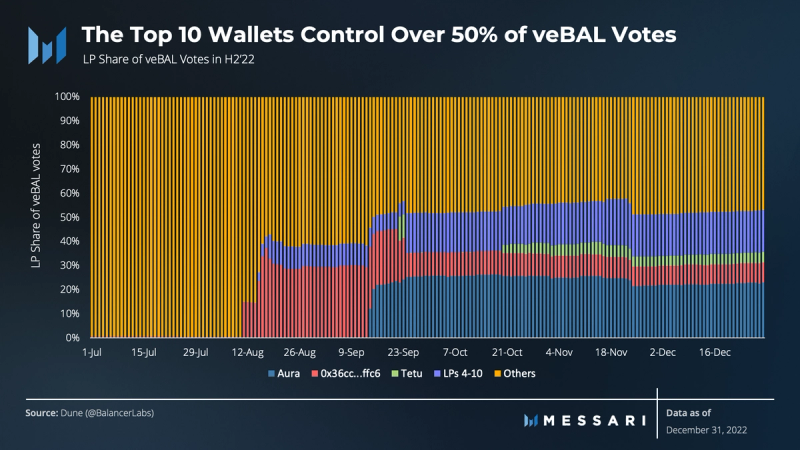

Notably, veBAL holdings remain relatively concentrated in top holders. A significant source of the concentration is Aura, one of the protocols that offers a liquid wrapper for veBAL. In November, Aura passed a proposal that will increase Aura’s voting power in governance votes (but not gauge votes) by making it a voting block instead of individual voters. Previously, holders of vlAura could vote in governance with their share of voting power. After the change, all Aura voting power will be used on the decision that gets the most votes from vlAura holders. This consolidates and increases Aura’s voting power in governance.

BAL will likely always trade at a multiple to earnings for veBAL lockers. Currently, BAL is trading at 11x annualized LP revenues from Q4. A high multiple is both good and bad for Balancer. On the one hand, incentives (BAL inflationary rewards) are very valuable to LPs, which should lead to greater stickiness of TVL. On the other, it creates a greater incentive for rational economic players to allocate BAL to themselves rather than to revenue-generating pools.

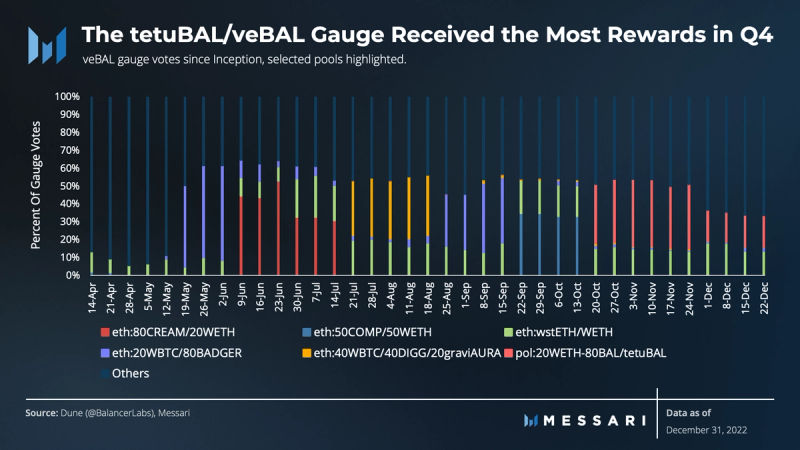

Tetu is a Polygon-native protocol that also offers a veBAL liquid wrapper. To increase liquidity for its wrapper, Tetu created a pool on Balancer for BAL/wETH 80/20 BPTs and tetuBAL tokens. This pool became a key piece in the DAO discussions this quarter, given its smallholder base but large share of inflation rewards. As part of the Peace Treaty, the largest voter has agreed to accept a 17.5% gauge limit on this pool.

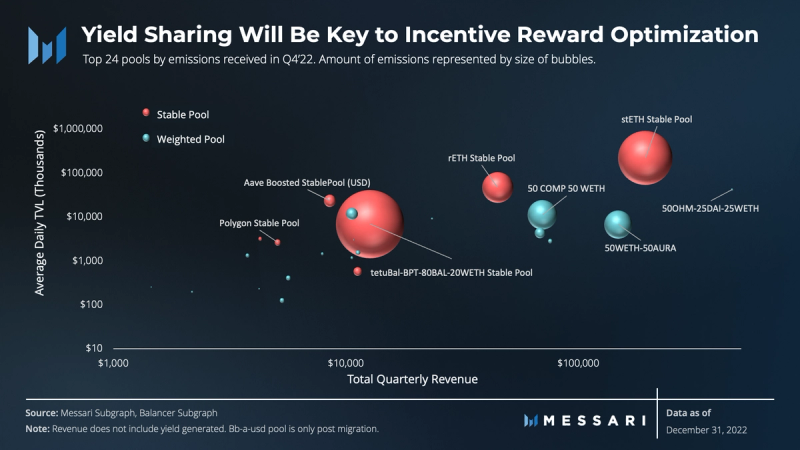

From the perspective of a veBAL holder, rewards are most efficiently allocated when they go to pools that earn a lot of revenue per unit of TVL. In the above chart, that would be the bottom right quadrant. At the moment, the above measure does not include revenue from yield, which is important as a majority of BAL rewards in Q4 went to stable pools (likely aided by the New Gauge Framework implemented in Q2). Clearly, the tetuBAL-BPT stable pool is the outlier here, receiving the most rewards in Q4 (nearly $2.6 million). Aside from that pool, the largest recipients of BAL all brought in at least $45,000 of trading revenues for Balancer in Q4.

Treasury

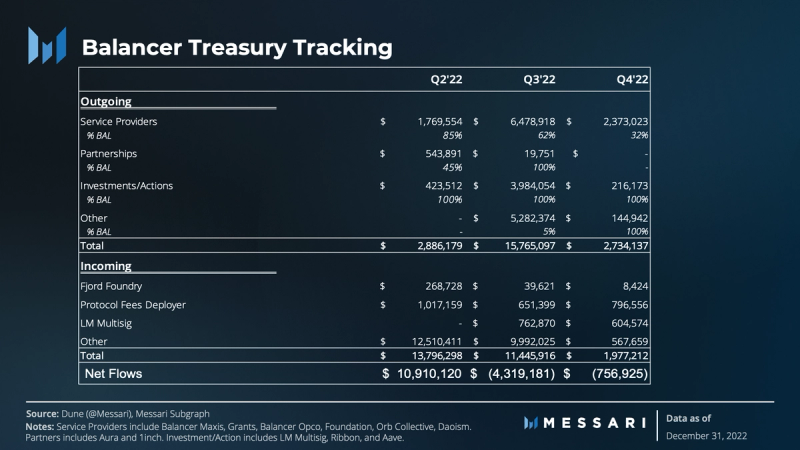

Tracking the Balancer treasury wallet informs on burn-rate for the DAO. The treasury is primarily funded from protocol revenues and from the partnership with Fjord Foundry (formerly Copper). Fjord powers Liquidity Bootstrapping Pools that are more common in times of ample liquidity (bull markets). Other income to the treasury is from swaps with other DAOs, refunds from investments like in Fei Protocol, and returns from earlier allocations to Balancer Labs. The largest cost for the DAO is Service Providers, though the DAO also allocated funds to partnerships and investments.

Qualitative Analysis

In Defense of veTokenomics

Many have touted that Satoshi’s breakthrough was not in technology or blockchain, but game theory and coordination. Over a decade later, Balancer announced it would be implementing vote-escrow tokenomics to align token holders and protocol users (liquidity providers).

Since that announcement, many have seen the experiment as a case study proving the failure of this mechanism, especially following the drama in Q4 between the DAO and Humpy the veBAL whale.

Capitalism is an economic game where holders of capital have the sovereign right to allocate it as they see fit. It creates the opportunity for positive sum investment and benefits from the wisdom of the crowd, if the average allocation enables productivity gains beyond the cost of capital. Crypto uniquely enables capitalism in digital economies. The purpose is the opportunity to benefit from the collective and increase the pace of productivity gains.

Most other DEXs have no such design. The existing models of business that give capital to allocate to smart or efficient builders or allocators to make those decisions can also work, as they have for many years in our existing system. Build a product and charge fees for it. A tried and true mechanism.

Alternatively, veTokenomics is an attempt at a different mechanism. Instead of taxing users to reward the capital allocators, inflation taxes passive holders in exchange for the efforts of active participants to grow the pie by efficiently allocating them as incentives; free-riders pay in the form of inflation while active participants have the opportunity to benefit. Further, using crypto and innovations like quadratic voting (if sybil resistance is successfully enforced), the benefit could be a more efficient form of capitalism that reduces the impact of unequal wealth distribution caused by compounding.

One of the known issues with veTokenomics is that it is incredibly difficult to align token lockers, who control the allocation of inflation rewards, with protocol revenues. Part of this could be an issue of intention: veTokenomics was originally created as a bootstrapping mechanism for pool creators to incentivize them to use a certain DEX to create liquidity for their token.

Since its inception, Balancer has been fighting to keep lockers aligned. From the New Gauge Framework to limit the ability to manipulate small pools to finally the Peace Treaty in Q4, there is no easy way for the DAO to maintain alignment.

This highlights a unique pain point for crypto and decentralization. In order to get “over the hump” to a point where it would be prohibitively expensive to take advantage of the system, the protocol could benefit from having more centralized controls. Balancer has placed an emphasis on decentralizing, leaving minimal points of control including a 6-of-11 multisig to implement approved proposals (with a new TimeLock Authorizer for security) and a 5-member Governance Council tasked with creating Snapshot votes for well-defined proposals. As such, it was required to “cut a deal” that is likely less beneficial to the DAO in the near term than being able to censor a member would have been.

Decentralization for many protocols is a process. Perhaps for veTokenomics, it is a process that should go slowly until the market cap of the protocol is to a point where amassing a large position is prohibitively expensive. Or the control should not be decentralized until there is strong sybil resistance and effective quadratic voting to similarly weaken whales. Whales could otherwise use the incentive structure in a manner that does not benefit the DAO as a whole.

It has been a strong and valid criticism to say it is extremely difficult to bootstrap effective vote-escrow tokenomics. At a small market cap, large players can very easily use the system without giving anything back to it. By accepting a lower yield because their income is in the form of BAL incentives, they deter new lockers from partaking in a now overvalued system. Once in the grips of the whale, it could be very difficult to reverse course.

However, if the protocol can reach escape velocity, the design can be extremely effective. A higher token price typically means lower yield for lockers but stronger incentives for LPs. However, higher yields for lockers should coincide with a lower BAL multiple and thus weaker LP incentives. A key variable is the percent of outstanding BAL locked.

Thus far, the criticisms of veTokenomics have been validated. There are large and adept players who are not properly incentivized to promote protocol revenues or liquidity growth. Fortunately for Balancer, the DAO was able to reach an agreement with these players. New tools such as Digital Identifiers (DIDs) and other sybil resistance mechanisms can likely help prevent similar issues in the future. Balancer’s innovations with boosted pools and its partnership with Aave will provide real opportunities to reward lockers and benefit from the protocol’s tokenomics.

In 2021, veTokenomics was the hottest idea on the block. In 2022, it fell on its face and looked like a huge mistake for all those who implemented it. As we turn to 2023, DAOs will be challenged to adapt to the failures and lessons learned from the experience thus far.

Boosted Pools, GHO, and the 2023 Outlook

Generalized Boosted Pools is a unique innovation that Balancer offers liquidity providers. Boosted pools offer LPs the opportunity to simultaneously earn from both trading fees and interest, for any ERC-4626 compatible wrapped token. Work is being done to enable these pools to utilize any available Aave lending pool as well.

Boosted pools are important for Balancer’s future for two reasons:

- They are a differentiated offering for LPs that should generate higher yields.

- They create a significantly more direct connection between liquidity incentives and protocol revenues.

For pool creators and DAOs looking to bootstrap liquidity of a token, instead of creating a pool of TKN/stablecoin, they can use the bb-a-USD pool or a specific stablecoin linear pool like bb-a-USDC to reward LPs with both trading fees and lending yield on the stablecoin leg. Using ETH as a pair enables similar efficiency, if pool creators use the b-stETH-stable as the ETH leg (a linear pool of wETH and wstETH).

The protocol collects 50% of revenues earned from yield-bearing pools. In July, Balancer voted to create added incentives for veBAL voters to allocate rewards to “core pools,” which are pools with interest-bearing tokens. The innovation gives the DAO the opportunity to be significantly more efficient with inflation rewards spending, as the expected impact on protocol revenues from increased liquidity will be much more predictable.

In November, Aave passed a proposal to enable some liquidity pool tokens (LPTs) to be allowed as collateral on the lending platform. The proposal also approved a direct integration with Balancer as a tool to bootstrap GHO, Aave’s proposed stablecoin. The opportunity shows the depth of the Balancer-Aave partnership along with great promise for revenues to Balancer once launched.

Aave will create a liquidity pool on Balancer for its GHO stablecoin with other stablecoins (likely the bb-a-USD boosted pool). Using BAL in the treasury from treasury swaps, Aave will create a veBAL position and vote to incentivize liquidity in its newly created pool. On its lending platform, Aave will accept the Balancer Pool Token (BPT) for the pool they created as collateral, in exchange for GHO. In doing so, they can create an incentive for users to borrow GHO and other stablecoins from their platform to create BPTs and receive BAL rewards. The flywheel is mutually beneficial and an exciting launch to watch in the first half of 2023.

Managed Pools is another innovation expected to launch in 2023. Managed Pools are a long-time coming for Balancer and should enable pool creators to use Balancer to create positive-carry index funds. In other words, pool creators can create a pool of tokens at fixed weights where users can deposit assets and earn revenues for holding them there from trading fees instead of paying a management fee.

In August 2021, Fernando shared his vision that the value of Balancer is what is built on top of it. Generalized boosted pools, GHO, and Managed Pools are all examples for that vision coming to fruition. The responsibility remains on builder execution and DAO voters, who wield significant influence in the future of the protocol and DAO because of their control over the significant incentives that Balancer’s tokenomics offers.

Closing Summary

Balancer continues to innovate and create solutions for others to build upon, with generalized boosted pools and managed pools on the horizon along with a growing partnership with Aave. The protocol maintained its TVL in 2022 better than all leading peers, likely due to its unique product offering as well as its vote-escrow tokenomic design. However, the design creates a difficult battle in the DAO as incentive allocation can serve various purposes. A united DAO would likely help focus investments and streamline the outcome of the experiment, but reaching that stage is difficult. The protocol and DAO look forward to promising product releases and partnerships in 2023.