Key Insights

- Since introducing Chicken Bonds on October 4, there have been over 2,400 bonds created and over $70 million in deposits.

- LUSD supply increased for the second quarter in a row but is still down 79.3% from a year ago.

- Liquity’s stability pool has benefited from users depositing into Chicken Bonds with total value locked (TVL) increasing from $115-$134 million.

- The system collateral ratio decreased from 2.5-2.3 QoQ but remains significantly above the 1.5 ratio required to trigger recovery mode.

- LQTY is down 25% since the inception of Chicken Bonds while ETH is down 12% in the same period. This may be attributed to selling pressure from Chicken Bonds.

Primer on Liquity

Liquity is a non-custodial, immutable, governance-free borrowing protocol. It charges users an issuance fee to take out an interest-free loan in USD stablecoin (LUSD) backed by ETH collateral. Loans can be liquidated if they fall below 110% collateral ratio. Liquidations are supported by a stability pool of deposited LUSD used to pay back the loan in exchange for excess ETH. The protocol has liquidation mechanisms should the stability pool be empty. Liquidators who initiate liquidations also receive 200 LUSD in gas compensation and 0.5% of the liquidated collateral. LUSD is hard-pegged between $1 and $1.10 through arbitrage opportunities and soft-pegged to $1 using a Chainlink oracle. LQTY stakers earn the issuance fee in ETH and a redemption fee in LUSD when arbitrageurs swap LUSD to maintain the peg.

Key Metrics

Performance Analysis

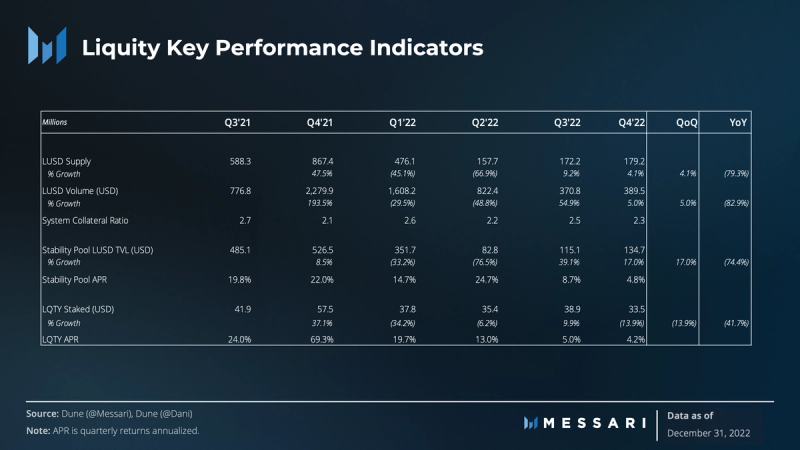

Following a muted Q3 in terms of revenue, Liquity generated $757,000 in revenue in Q4 for an increase of 36.4% QoQ. Revenues YoY are down 93.1%, which is not unique to Liquity and a result of the overall deleveraging of the cryptocurrency ecosystem. Both the stability pool and LQTY staking saw a continuation of their declining APRs, with decreases of 3.9% and 0.8% QoQ, respectively.

LUSD supply increased for the second consecutive quarter by 4.1% to reach a total supply of $179 million, down from its peak of $867 million a year ago. Volumes remained relatively stable QoQ, increasing by 5% to $389 million. LQTY fell 20.8% over the quarter while emissions continue to decline.

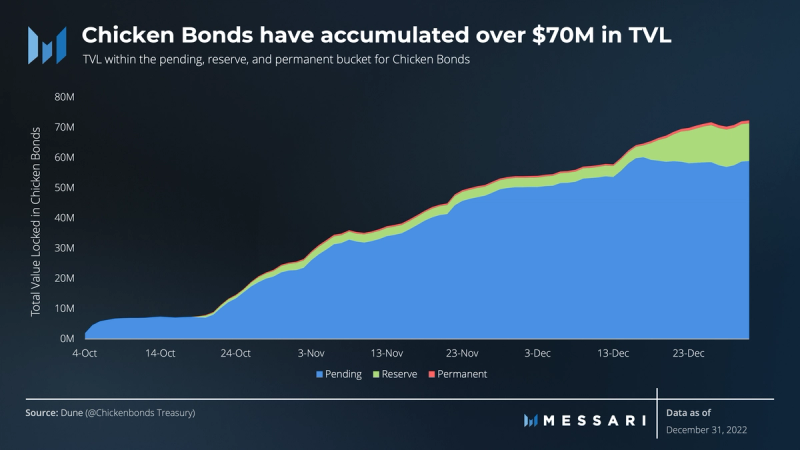

The release of Chicken Bonds, as covered in a previous quarterly, has garnered the attention of many in the decentralized finance (DeFi) space with over $70 million in deposits since its release on October 4. Liquity continues to be one of the most widely adopted decentralized stablecoins currently available to users, and the team continues their efforts to onboard LUSD into more protocols.

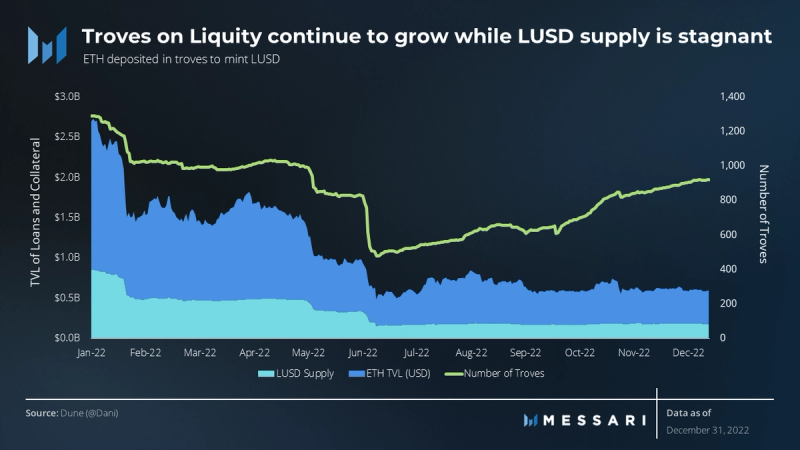

Users opening troves (troves are similar in concept to vaults or CDPs from other platforms) on Liquity continued to increase, rising from a low of 479 troves in June to 922 troves at the end of Q4. Despite this, the LUSD supply only increased by $22.2 million in the same period for an increase of 14.1%. QoQ, the number of troves increased 41.4% and the LUSD supply increased 5.9%. Notably, although Chicken Bonds reached over $70 million in deposits since inception, the LUSD supply only increased by $10 million. This may indicate that most of the investment in Chicken Bonds came from users already within the Liquity ecosystem. However, the increasing number of troves argues otherwise.

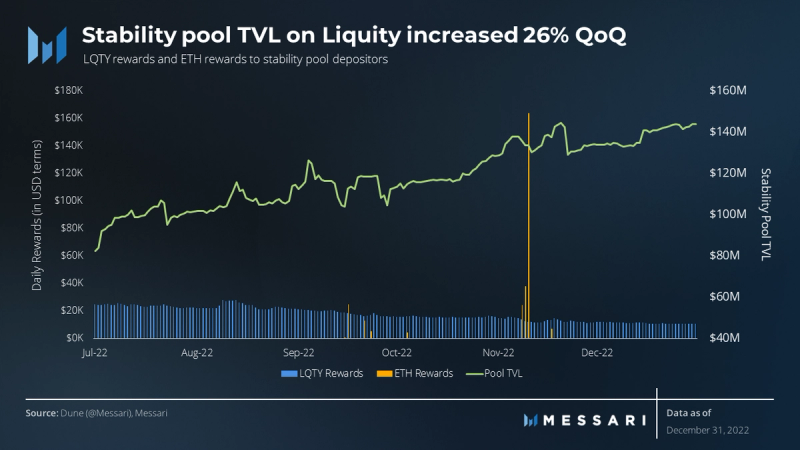

The stability pool continues to grow from its low of $82 million in Q2 to over $134 million by the end of Q4. The stability pool’s 17% QoQ growth can be attributed to the release of Chicken Bonds and the redirecting of a portion of funds from the Pending, Reserve, and Permanent buckets toward the stability pool.

A declining LQTY price and reduced emissions have negatively affected the LQTY rewards. By the end of Q4, LQTY’s circulating supply was 86,581,245 but its maximum supply is set for 100,000,000. Emissions will continue to decline by adhering to the following schedule 32,000,000 * (1–0.5^year).

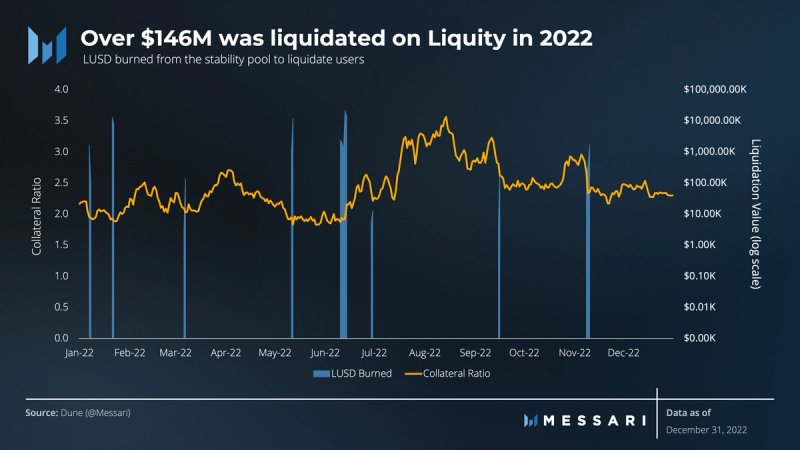

Liquidations in Q4 centered around the FTX fiasco in early November. There were $2.9 million in liquidations resulting in $283,194 of revenues for stability pool depositors. Compared to the $115 million in liquidations after the Terra collapse and 3AC unwind in Q2, these liquidations are miniscule. QoQ there was a 5x increase in liquidations.

The leverage in the system remains healthy with a collateral ratio of 2.3, far above the 1.5 ratio that would trigger recovery mode. To date, the protocol has been able to handle liquidations without major issues.

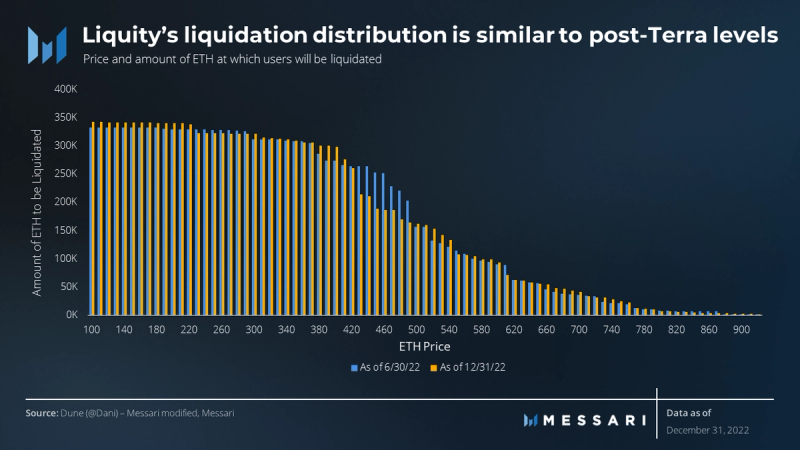

On the back of the FTX collapse, the Liquity liquidation price distribution paints a similar picture as it did following the Terra collapse. Most Liquity troves are not at risk to liquidation until around the $750 level for Ethereum.

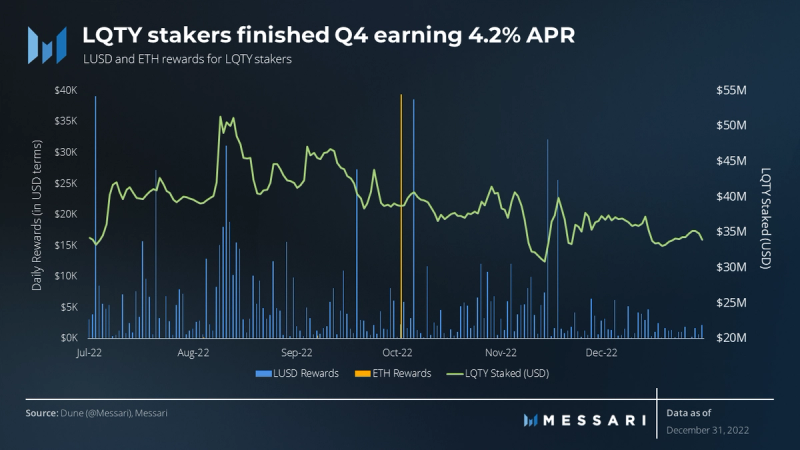

LQTY stakers ended Q4 earning a 4.2% APR, which is 0.8% less than the previous quarter and 65.1% less than the previous year. LQTY stakers enjoyed $39,000 in ETH rewards in the beginning of October, but that aside, ETH rewards were nonexistent for the quarter.

LQTY fell 20.8% over the quarter, which is relatively in line with the rest of the market as the total crypto market cap was down 14.1% over the same period. Notably, Chicken Bond depositors funds are routed through B.Protocol. The strategy here is to sell LQTY and ETH generated for more LUSD. It will be important to monitor the price of LQTY as Chicken Bonds continue to grow to see if there is a strong correlation between the price of LQTY and TVL of Chicken Bonds.

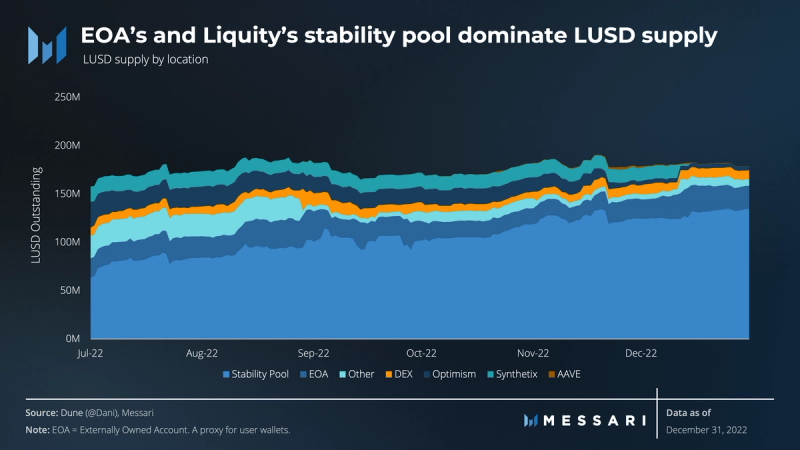

The two main use cases of LUSD continue to be support of the protocol via the stability pool or holding LUSD in an externally owned account (EOA), typically user wallets. Although these two options are perfectly acceptable use cases, by integrating LUSD with more protocols and blockchains, demand for LUSD should increase with the increased token utility.

Efforts to integrate LUSD have undoubtedly been made with the integration of AAVE and deployment on L2s such as Optimism and Arbitrum. Currently, LUSD is available on six different decentralized exchanges (DEXs) and accepted as collateral on six different protocols.

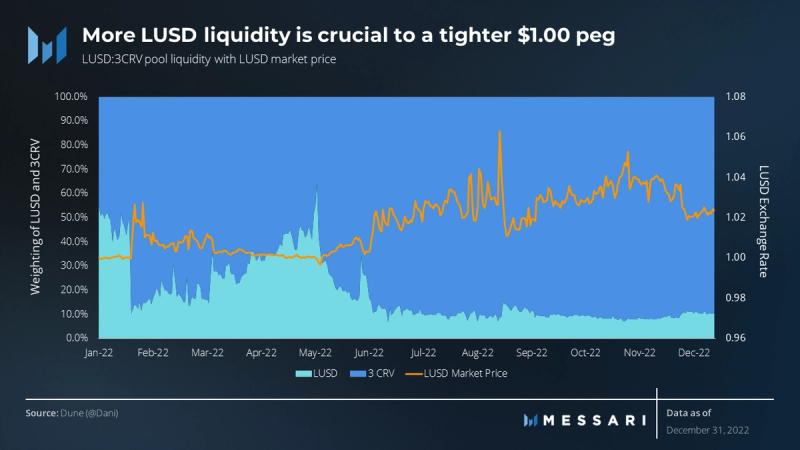

For much of 2022, LUSD traded above its $1.00 price floor as demand remained high for a censorship resistant and decentralized stablecoin. Although by design LUSD can safely remain between $1.00 and $1.10, users generally prefer a stablecoin to maintain a strong peg to $1.00. The peaks in late August and early September can be attributed to the OFAC sanctions on popular cryptocurrency mixer Tornado Cash on August 8 and the succeeding events that transpired with stablecoin issuers utilizing their blacklist functionalities.

Toward the end of Q4, LUSD approached the $1.00 price floor. This may be attributed to a number of possible factors such as, the increased liquidity of LUSD in the LUSD:3CRV pool. As evidenced above, LUSD traded most closely to $1.00 between March 11 and May 10. During this time LUSD made up between 28 and 41% of the liquidity in the LUSD:3CRV pair. By October 4, LUSD was trading above peg at $1.028, while LUSD only made up 9.2% of the pool. On December 31, LUSD dropped to $1.023, with LUSD increasing to 10.31% of the pool.

Where did the LUSD come from that was deposited into this pool? Considering the increase in liquidity was $906,000 over this period and the permanent bucket of Chicken Bonds accrued $960,000 in the same period, it becomes clear that Chicken Bonds have a greater purpose than just offering users a higher yield.

Since the release of Chicken Bonds, there have been 2,374 bonds created by the end of Q4. These bonds account for over $70 million in TVL within the three buckets: pending, reserve, and permanent. The split between the three at the end of the quarter were $58.9 million, $12.7 million and $960,000 respectively. Users who waited enough time for their bond to mature, or “chickened in,” within the reserve bucket benefit from a 5.78x yield amplification. Simply, users would earn 5.78x more yield from having their deposit in the reserve bucket as opposed to depositing into the stability pool directly.

The bonded LUSD (bLUSD), an ERC-20 token minted when a user “chickens in,” is designed such that the floor price can only rise over time. This floor price is what bLUSD can be redeemed for. For example, if a user has 100 bLUSD and the floor price is $1.20, they can redeem their bLUSD for $120.0. Users can also buy bLUSD on the open market via Curve, and in the early days of users “chickening in,” the market price was trading at a 30% premium to what the floor price was. This spread was quickly closed as both the premium for bLUSD fell and the floor price rose. Currently, the bLUSD:LUSD3CRV pool has $16 million in liquidity.

Qualitative Analysis

When Generalized Chicken Bonds?

The introduction of Chicken Bonds in October 2022 generated a meaningful buzz around Liquity. With a generalized version of Chicken Bonds still scheduled for release in H1 2023, many other protocols are considering ways they may be able to utilize Chicken Bonds for their tokens. Beanstalk (BEAN), a credit based algorithmic stablecoin, drafted a plan on how they can implement these bonds in what they call The Coop. Others have speculated on ways to incorporate Chicken Bonds with staked ETH. If Liquity were to charge other protocols a fee to use this bonding mechanism, there could potentially be another way for LQTY stakeholders to extract value.

With this said, the Chicken Bond experiment has only just begun. The Risk DAO has suggested the system may reach a point where bonding may not be profitable. As this bonding mechanism is novel in design, there are still a number of unknowns on how the Chicken Bond protocol will behave in different market conditions. For now, it will be important to monitor the rate at which new bonds are created, the yield amplification offered, and the yield for the bLUSD:LUSD3CRV pool.

DeFi’s Stablecoin

Beyond Chicken Bonds, the Liquity team continues to find new integrations for LUSD. Protocols such as Solidlyeth and Silo Finance both integrated LUSD in November, improving the utility of LUSD within the DeFi ecosystem. In December, Liquity announced an integration with Camelot DEX to bring LUSD to Arbitrum, the fourth largest blockchain by TVL. In the future, Liquity plans to integrate with Aztec Network, a privacy friendly and gas efficient zk-rollup. These integrations are critical for the long-term success of LUSD and prove that Liquity is still working to increase utility for the stablecoin.

Tellor Issue

Following the Ethereum Merge in September, the ETHW fork contained a clone state of Ethereum with Liquity. As The Merge approached, the Liquity team made it clear that the only version of the protocol they would support would be on mainnet. Additionally, Chainlink, Liquity’s primary oracle, also declined to support the ETHW forked instance. As a result, when Liquity was cloned on ETHW the protocol’s fallback logic kicked in and Liquity began to use Tellor as its price oracle. Due to an incorrect implementation of this oracle by the Liquity team, someone on ETHW was able to stake TRB, report a fake ETHW price and mint trillions in LUSD.

Fortunately, the exploit did not occur on mainnet as Liquity was never required to fallback on the Tellor price feed. Liquity was extremely fortunate that the ETHW fork brought this issue to light. Since then, Liquity has made the proper fix to correctly implement the Tellor price feed.

Closing Summary

Liquity had a successful Q4 in 2022, with $757,000 of revenue and an increase in troves and LUSD supply. The release of Chicken Bonds has been popular, with over $70 million in deposits since its introduction. Liquidations in Q4 were centered around the FTX collapse, while the stability pool experienced growth due to the release of Chicken Bonds. LQTY rewards declined due to reduced emissions and a declining price. LUSD continues to be one of the only truly decentralized stablecoins available. The protocol’s APR and LQTY staking APR both declined. It will be important to monitor the continued integrations and the evolution of Chicken Bonds in the following quarter and year.