Key Insights

- Q4 experienced a significant 146% increase in interest revenue compared to Q3, driven by the Binance Launchpad and Launchpool events and accruing interest on stablecoins borrowed by the BSC Token Hub exploiter.

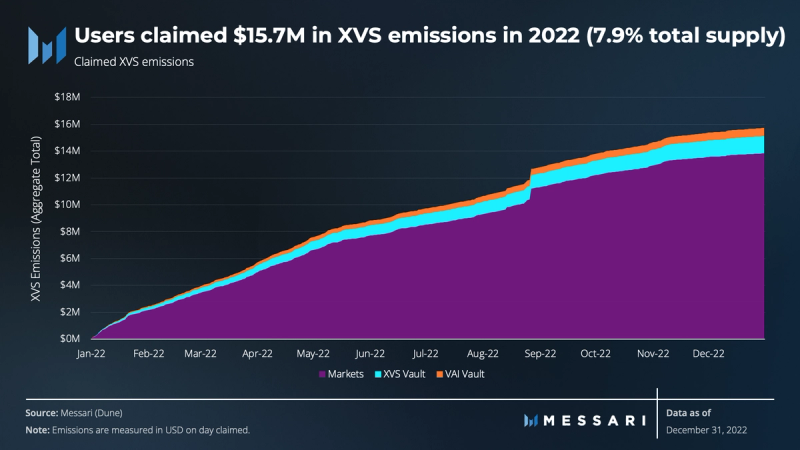

- Users claimed a total of 2.3 million XVS tokens emitted by the protocol in 2022, equal to 7.9% of the total supply and $15.7 million at the time of claim.

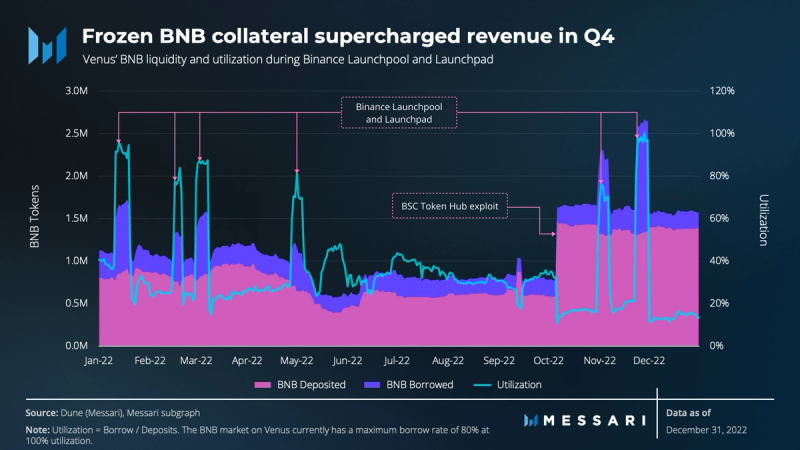

- The October BSC Token Hub exploit resulted in a 150% increase in BNB liquidity on Venus.

- In 2022, the CAKE market averaged a 65% utilization rate and generated $2.2 million in interest revenue, as users sought to profit from PancakeSwap’s “Syrup Pools.”

Primer on Venus

Venus is a decentralized money market protocol on the BNB Chain that facilitates depositing and borrowing of various crypto assets. The interest rates for these assets are set algorithmically using an interest rate model that triggers updates based on the proportion of deposited assets lent. This is known as the utilization ratio. The protocol is managed by the Venus DAO community and governed by the XVS token. Users can stake the governance token in a vault to participate in governance and receive a portion of the protocol revenue.

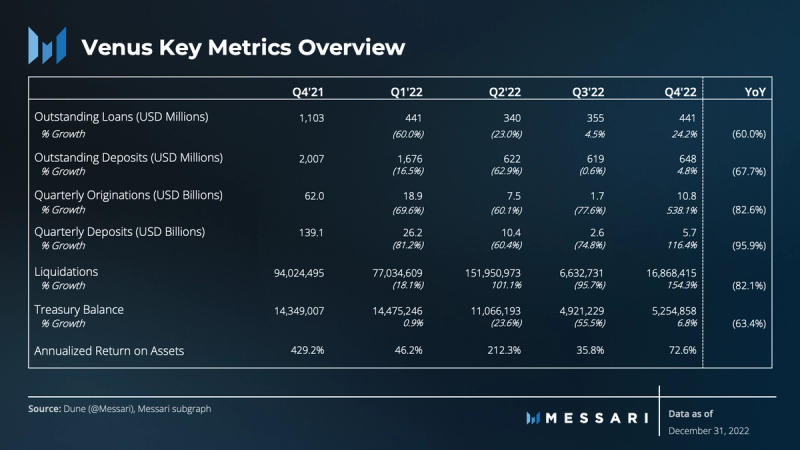

Key Metrics

Performance Analysis

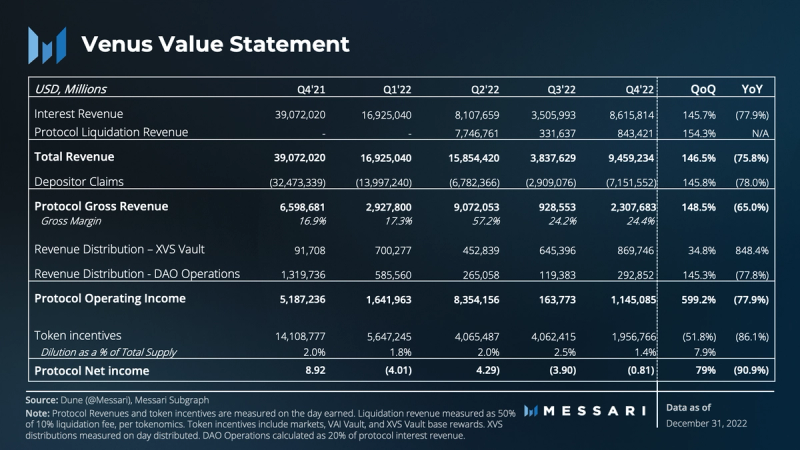

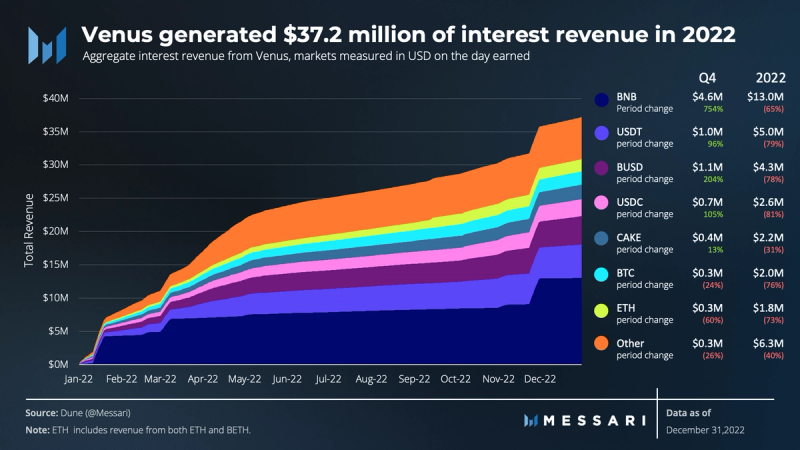

In 2022, Venus markets generated $37.2 million in interest revenue. Of this amount, 35% came from BNB, 34% came from stablecoins, and the remaining 31% came from other non-pegged assets.

Q4 experienced a significant 246% increase in interest revenue compared to Q3. The increase was driven by the successful launch of the Binance Launchpad and Launchpool events, which attracted significant investment from large investors (whales). During these events, large amounts of stablecoins are deposited, and the maximum amount of BNB is borrowed. By holding BNB, users are able to receive tokens from new projects. These events have not taken place since Q2 and have historically been a major contributor to Venus’s revenue. Additionally, accruing interest on stablecoins borrowed by the BSC Token Hub exploiter contributed to the Q4 revenue increase.

Protocols often encourage liquidity and usage through token incentives. In 2022, users claimed a total of 2.3 million XVS tokens, equal to 7.9% of the total supply and $15.7 million at the time of claim. Of this amount, suppliers and borrowers of Venus markets claimed $13.8 million, stakers in the XVS Vault claimed $1.3 million, and stakers in the VAI vault claimed $614,000.

In November, Venus Governance executed proposal VIP-78 to reduce XVS emissions to the markets by 50% to reduce sell pressure during the down market. Furthermore, Venus’ v3 Tokenomics upgrade, which passed in a Snapshot Vote in September, included language around curtailing emissions. The initial proposal on the community forum advocated for a reduction of 10 million tokens, bringing the total supply to 19.7 million and reducing the remaining emissions schedule from four to two years. However, the Snapshot proposal delayed any curtailment until a second discussion could take place to better evaluate the impact of a reduction as the primary focus of the time was on rolling out the feature-packed Venus v4 protocol upgrade. Secondary discussions will involve finding the optimal reduction amount and the potential use of tokens for other ventures.

Further curtailing emissions and reducing the total supply should make each XVS more valuable, However, it will need to be supplemented with other incentives to keep users from redeploying liquidity elsewhere. The introduction of Venus Prime Soulbound tokens will allow users to access variable boosted yields, effectively beginning this process. Read more about Venus Prime here.

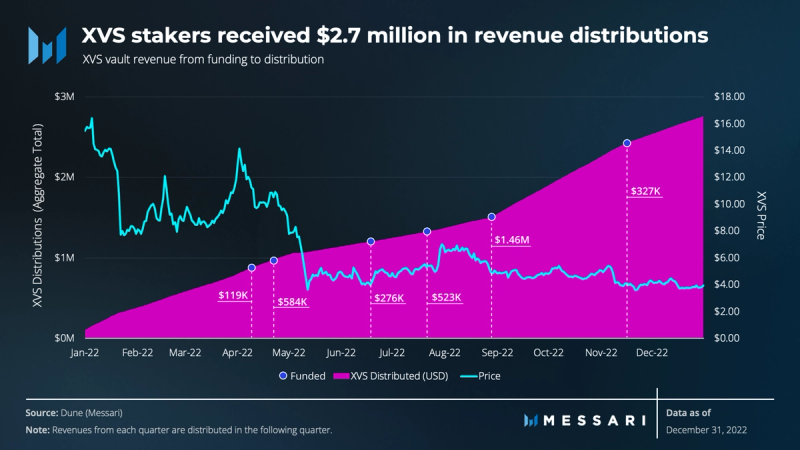

On top of the $1.3 million in base rewards, XVS stakers received an additional $2.8 million in XVS tokens from protocol revenue distributions in 2022. In Q4, these distributions increased by 34% in USD terms and 56% in token terms. Interest revenues are collected in the treasury over the quarter, and 20% of these revenues are used to purchase XVS tokens. These are distributed proportionally to stakers. Notably, though, the value of these tokens decreased approximately $620,000 by the time they were distributed, with the vault originally being funded with $3.3 million in XVS tokens.

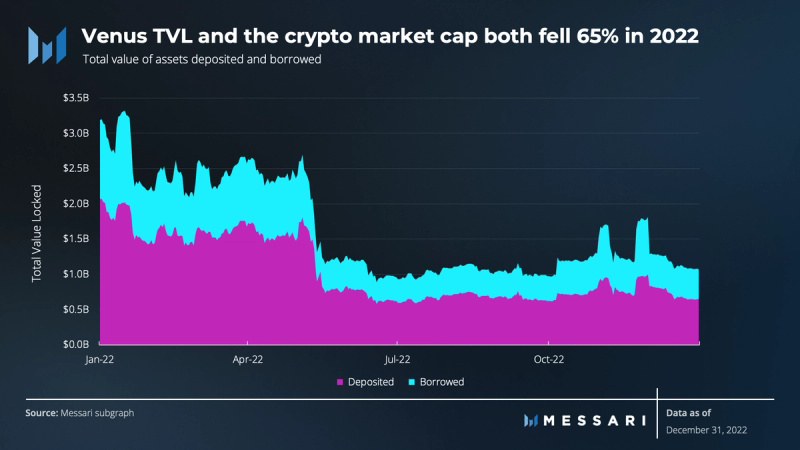

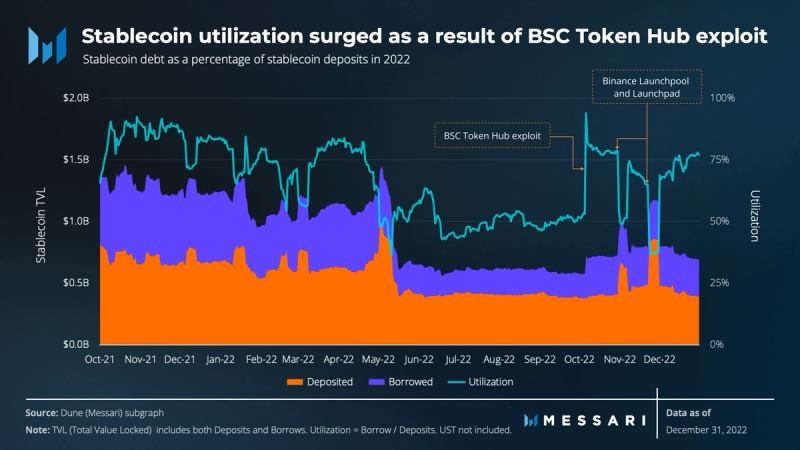

The TVL in Venus markets experienced a drop of 65% in 2022, a trend that mirrored the overall crypto market. The majority of this decline occurred in Q2 due to the LUNA crash and system-wide deleveraging. TVL remained relatively flat thereafter but slightly increased 12% QoQ in Q4 as a result of the BSC Token Hub exploit.

BSC Token Hub Exploit

In October, there was an exploit on the cross-chain bridge, BSC Token Hub. This exploit resulted in a 150% increase in BNB liquidity on Venus within minutes. The flaw in the verification process for proofs allowed the exploiter to trick the bridge into transferring 2 million BNB tokens, worth $568.6 million at the time, to their own wallet.

Of this amount, 900,000 BNB were deposited into Venus to borrow a total of $147.5 million in stablecoins including USDT, USDC, and BUSD. In response to the bug, BNB Chain was briefly paused to mitigate the issue and the remaining assets of the exploiter were subsequently frozen. According to blockchain security firm Certik, the exploiter was able to bridge roughly $110.7 million to other chains before the freeze. Despite the negative consequences of the exploit, the influx of BNB deposits came at a fortuitous time. Binance Launchpool and Launchpad took place for the first time since May, which significantly increased BNB demand. During these events, BNB loans originating from Venus generated $4.1 million in interest revenue, and the exploiters’ BNB deposit made up 71% of all the available liquidity.

Although the exploiters’ BNB position remains healthy, a liquidation could potentially cause cascading negative effects on the BNB price and BNB Chain users. To avoid this, a member of the BNB Core Dev Team initiated a proposal to whitelist BNB Chain as the sole liquidator of the exploiters’ position to safely offload the outsized volume. Venus Governance executed the proposal with 100% approval.

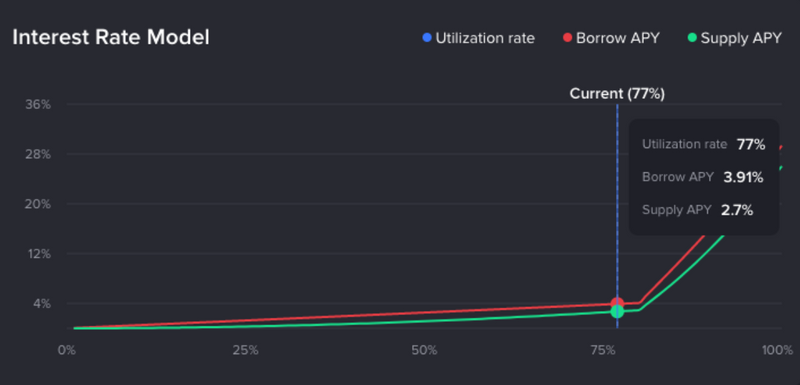

The exploit consequently increased stablecoin utilization to bull market levels, which increased the interest rate for the exploiter and other users. As of January 9, aggregate stablecoin utilization is at 77%, which triggers a borrow rate of 3.91% according to the current interest rate model.

Source: https://app.venus.io/

At 80%, a “jump” rate is initiated and increases the borrow rate exponentially. However, even with increased borrowing rates, it remains unlikely the exploiters’ position will be liquidated in the near future due the large amount of interest revenue received during Launchpad events.

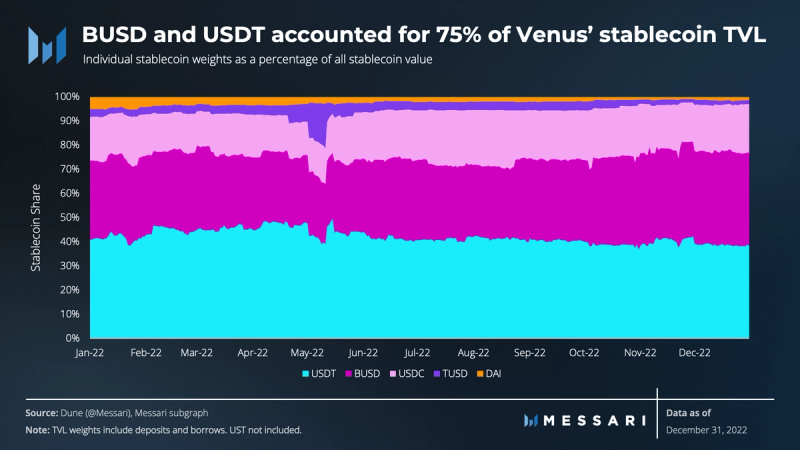

The average TVL of stablecoins on Venus significantly dropped by 49% in 2022, falling from $1.67 billion to $844.7 million. While much of this is due to deleveraging, the average supply of stablecoin deposits dropped 44% in 2022, from $932 million-$518 million. Among the five stablecoins supported by Venus markets (BUSD, USDT, USDC, TUSD, and DAI), DAI saw the steepest decline, with deposits decreasing 82% from $34.5 million-$6 million. This decrease was accompanied by a 43% drop in the market cap of DAI. BUSD deposits, Binance’s native stablecoin, decreased the least at 31%, down from $218.5 million-$149.7 million.

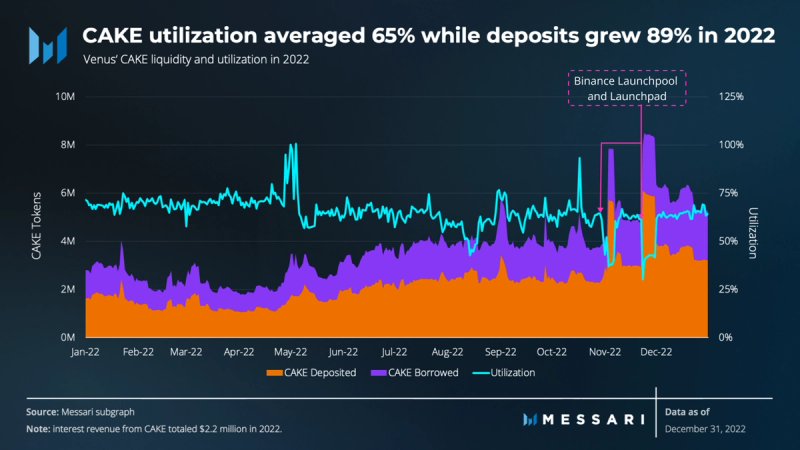

CAKE is the governance token of PancakeSwap and is a key component of their platform’s value. In 2022, the average utilization rate of CAKE on Venus was 65%. Per the interest rate model, when utilization reaches 65%, the borrowing interest rate for CAKE is 29.58%. On PancakeSwap, users can earn additional CAKE rewards by locking their tokens in a “syrup pool” for up to a year at a rate of 49% APR. The average lock time for CAKE on PancakeSwap is currently 42 weeks.

Some users adopt an investment strategy of collateralizing stablecoins and borrowing CAKE to profit from the difference between the two interest rates. This profit is derived from the difference between the CAKE earned from the syrup pool and the interest paid for borrowing. In 2022, the CAKE market on Venus generated $2.2 million and accounted for 6% of interest revenue. The high utilization rate of CAKE on Venus is likely to be maintained as long as this strategy remains profitable (i.e., the APR from staking CAKE in the syrup pool remains higher than the CAKE borrow rate on Venus.

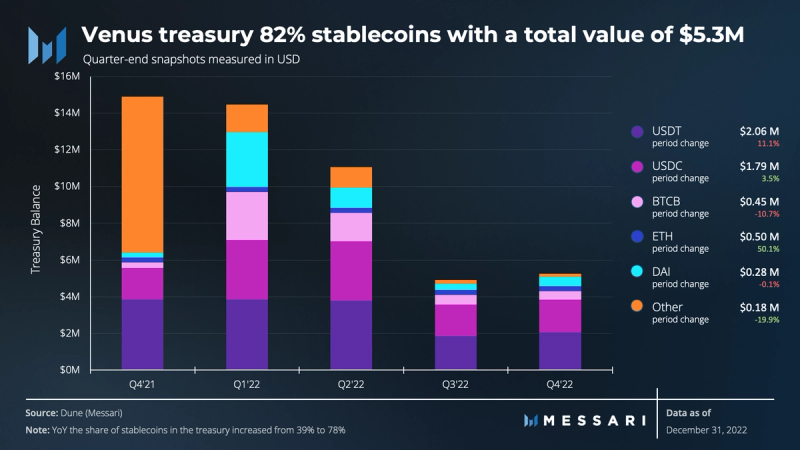

Thanks to the uptick in interest revenue, the DAO treasury increased 7% QoQ, the first increase since it began descending in Q1’22. During that time, it has been consolidated into stablecoins. By holding a significant portion of its assets in stablecoins, the DAO is able to weather market fluctuations and fund ongoing operations and initiatives such as the v4 upgrade. This strategy helps to provide stability and support the long-term success of the Venus protocol.

Qualitative Analysis

In 2022, the Venus community faced challenges such as CeFi contagion, price feed issues, and the BNB bridge exploit, but it was able to end the year on a successful note by reducing emissions by 50% and introducing the Venus v4 upgrade. The emission reduction lowered the sell pressure of XVS and extended the protocol’s runway while also reducing the cost of liquidity.

The Venus v4 upgrade is a comprehensive overhaul that addresses various challenges and enhances the platform’s capabilities. One of its features, the DEX integration, has already been released and enables one-click borrow and repay, eliminating the need for users to switch to a separate application to swap tokens. This streamlines the experience of interacting with borrow/supply markets and vaults and brings Venus closer to owning user relationships. Venus also captures a percentage of the fee volume from PancakeSwap and likely future DEX partnerships for these transactions, providing an additional source of revenue for the protocol.

A stability fee for VAI, another highly anticipated feature, recently passed in on-chain voting and has already been partly implemented. The second part of the implementation (The Floating APY rate) is set to be implemented in early Q1 2023. The stability fee will help keep VAI pegged, providing a more predictable experience for borrowers.

Also included in Venus v4 are two new features that will help users manage the risk of their positions: isolated markets and stable interest rate borrowing. Isolated markets provide an alternative to the cross-margin core pool, allowing for the onboarding of long-tail assets with custom risk management configurations. This helps users diversify risk and better manage the health of their accounts. Stable interest rate borrowing allows users to pay a premium for predictable interest rates, particularly useful during periods of high market volatility when stable loan rates remain fixed and partially reduce the probability of liquidation due to volatility.

One of the most important aspects of Venus v4 is the inclusion of measures to ensure that shortfall risks are covered and managed effectively. When a liquidation does not occur, it can lead to a shortfall caused by various factors such as an oracle issue, high price volatility, or a lack of liquidator participation. To address this, Venus Protocol will maintain a risk fund for each pool that receives 40% of the income generated by that pool in the form of its currency. In the event of a shortfall, the risk fund will be used to recover the bad debt through an auction of the reserve fund.

Venus is also working on issuing bonds as a strategic financing activity to address the existing shortfall and support the risk fund. According to Risk DAO, the existing shortfall is approximately $52 million. The bonds will be issued to strategic institutional investors who can provide both the necessary financing and partnership as Venus navigates the crypto market. While the issuance of bonds is unchartered territory for Venus, it is expected to bring significant benefits regarding risk management and financial stability.

Decentralization is also a key focus of Venus v4, with improvements such as faster interest rate parameter modifications, new role assignment, and fine-grained pausing of specific actions within specific markets. These enhancements aim to improve the efficiency and flexibility of the governance process and provide more precise control over protocol operations. Finally, v4 introduces price feed redundancy, which improves the reliability and resiliency of price feeds by supporting multiple oracles and monitoring for significant deviations between them.

Closing Summary

Venus faced many challenges in 2022, such as the crash of LUNA and the BSC Token Hub exploit. Despite these challenges, Venus was able to maintain its position as the top lending market on BNB Chain. In Q4, the protocol saw increased revenue thanks to demand for BNB during Binance Launchpad and Launchpool events, as well as interest earned on stablecoins borrowed by the BSC Token Hub exploiter.

The Venus community made significant progress in the latter part of the year with the reduction of XVS emissions and the unveiling of the Venus v4 upgrade. The emission reduction helped to lower sell pressure on XVS and extend the protocol’s runway. The Venus v4 upgrade is a comprehensive overhaul that aims to address various challenges and enhance the capabilities of the platform.

The BSC Token Hub exploit currently poses a risk to Venus, the price of BNB, and others on the chain due to the potential for liquidation of the exploiters’ large volume. However, the support of the BNB core dev team as sole liquidator, along with the high interest earned on the exploiters’ BNB position, is expected to keep liquidation at bay for the near future. The Venus v4 upgrade introduces shortfall coverage and bonds as mechanisms for addressing potential insolvencies and refinancing risks. It remains to be seen how effective these features will be in addressing the aforementioned debt. In the meantime, Venus continues to work on its ambitious v4 upgrade, focusing on addressing key challenges and enhancing the platform’s capabilities as it aims for success in the recovering market.