Key Insights

- Following the collapse of FTX, Solana’s asset value was one of the most impacted, as its market capitalization dropped by 70%; however, network health remained stable.

- Integrations unrelated to FTX are underway to reinforce Solana DeFi and are positioned to prop up and service additional demand.

- The NFT landscape of Solana is still developing aggressively, and GameFi is nearing reality.

- Rumors that Solana development was faltering post FTX and that a mass exodus of core devs was underway were false.

- The staking and decentralization of the network remained stable and actually improved its position after the FTX and Hetzner incidents.

- Solana will continue to release several initiatives, including network upgrades, Neon EVM, Firedancer, Solana Mobile Stack (SMS), and community efforts, to name a few.

Primer on Solana

Solana is a public, open-source blockchain that aims to deliver scalability and support smart contracts without sacrificing decentralization and security. It accomplishes this through a novel timestamp mechanism called Proof-of-History (PoH). Using PoH, the network can order and batch transactions before they’re processed through a Proof-of-Stake (PoS) mechanism. Additional design goals include sub-second settlement times, low transaction costs, and support for all LLVM-compatible smart contract languages, including Rust, C, C++, and eventually Move.

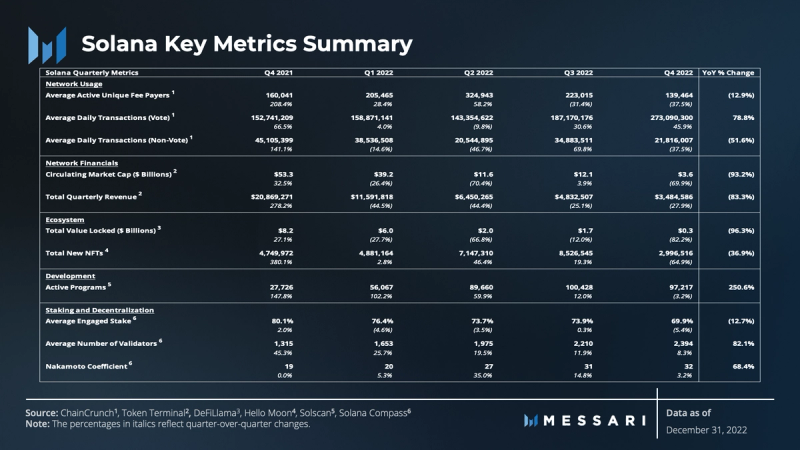

Key Metrics

The Fourth Quarter Narrative

Despite Solana’s strengths demonstrated through Q3 and its resilience against the challenges throughout 2022, the fourth quarter was a rollercoaster for the network. Q4 brought one of the final twists of the year with the collapse of FTX and the contagion that followed. However, not all was lost.

Overshadowed by the FTX chaos, Q4 reflected that Solana’s network and ecosystem remain strong. Solana’s mission toward adoption remains intact, as evidenced by continued development, further integrations with partners like Instagram and Facebook, and ecosystem expansion into GameFi and DePIN (Decentralized Physical Infrastructure Networks). Advancements in network functionality also continued, along with a myriad of other potential catalysts for growth.

As a follow-up to the State of Solana Q3 2022 report, this report will dive into the quantitative performance over the quarter and the qualitative evidence that Solana is continuing to overcome challenges and progress through adverse market conditions.

Subsequent events will be covered in the State of Solana Q1 2023 report.

Performance Analysis

Financial and Network Overview

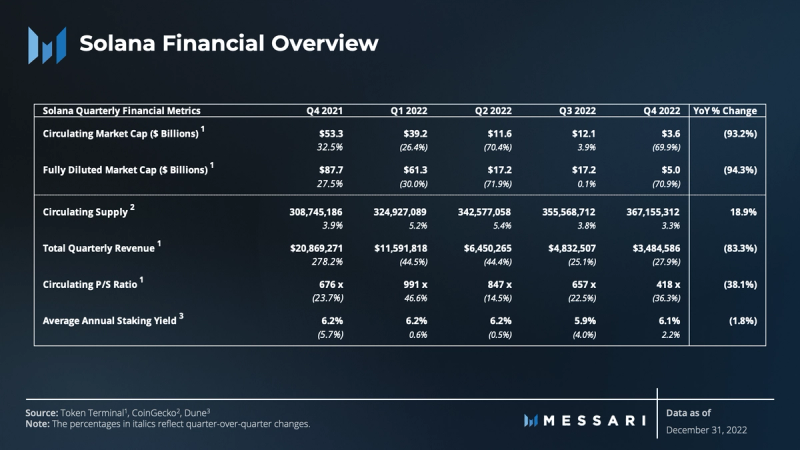

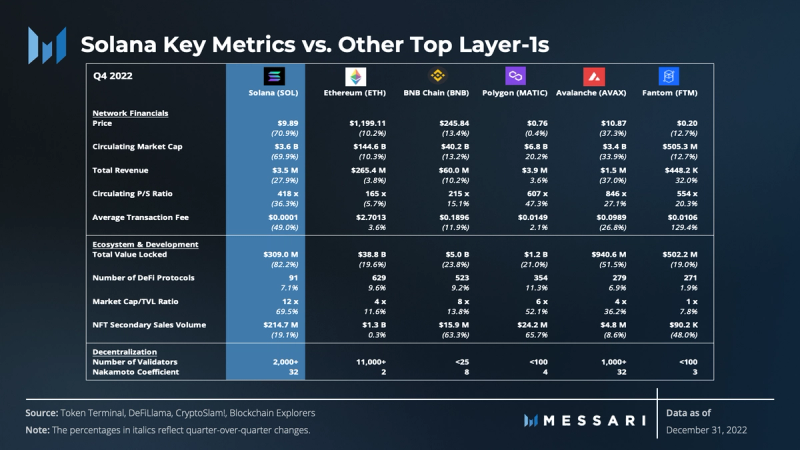

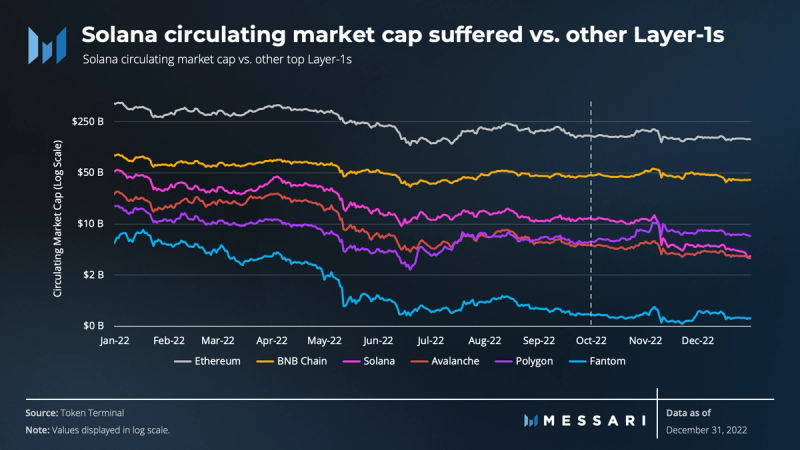

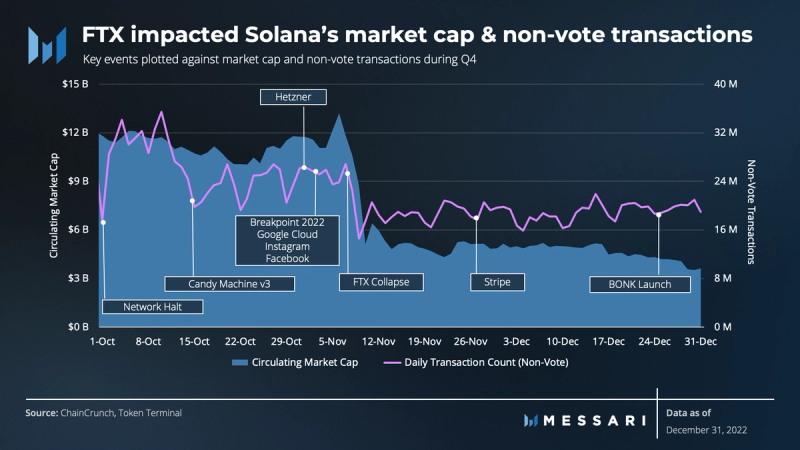

In the fourth quarter, a persistent bear market paired with the collapse of FTX had a significant negative impact. FTX was a significant investor in Solana. It was integral to Solana DeFi, especially in developing its leading DEX, Serum. As a result, Solana was one of the most impacted networks as its market capitalization dropped by 70%, plummeting from $12.1 billion to $3.6 billion.

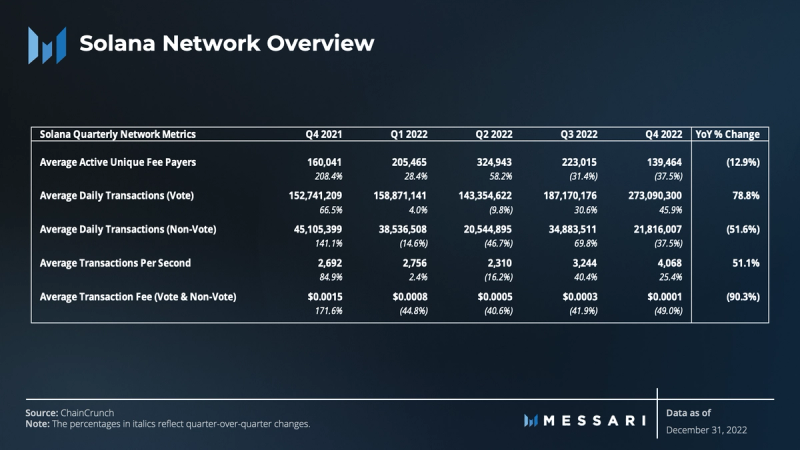

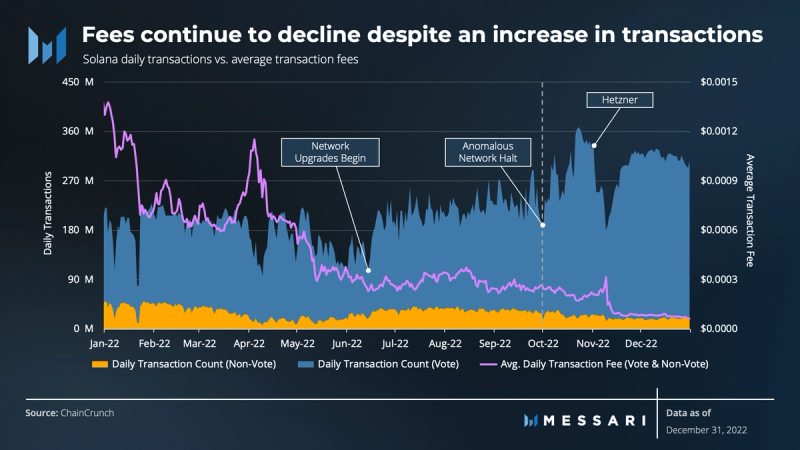

While market conditions have put downward pressure on user activity, average daily transactions in the aggregate and transactions per second (TPS) still increased because network performance improved.

Despite the increase in total transactions, average transaction fees continued to decline (49%). After the fourth consecutive quarter of declines, average transaction fees fell by 90.3% year-over-year (YoY). Revenue also continued to decline (27.9%) during Q4. Similarly, total quarterly revenue declined by 83.3% YoY. That said, it did not decline by as much as transaction fees, suggesting revenue was partially supported by growing transaction activity.

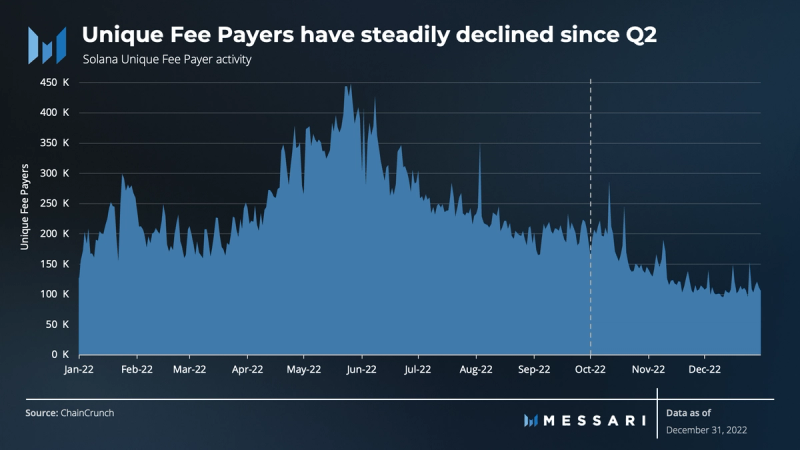

The daily Unique Fee Payers metric consists of the number of unique accounts that pay for at least one transaction per day. The daily average of Unique Fee Payers has been steadily declining since the end of Q2. This user base settled at a foundational level by the end of Q3 as it reached a longer-term average. However, post-FTX market sentiment likely continued to push user activity down through Q4 (37.5%), ending down 12.9% YoY.

The Unique Fee Payers metric can be a somewhat limited way to measure user activity on Solana, as it does not account for transactions authorized by several users but paid for by a single account. The Unique Signers metric might gauge absolute user activity more accurately.

Nonetheless, the trend of Unique Signers closely mirrored Unique Fee Payers over the quarter and the year.

Transactions on Solana can be divided into consensus (vote) and non-consensus (non-vote). Non-vote transactions are analogous to EVM transaction counts. They represent the actual economic activity on the network.

Transaction activity and performance of the network were volatile during 2022, at times for different reasons. During the first two quarters, network performance suffered from the spamming that arose from Gulfstream, Solana’s alternative to the mempool for pending transactions. At the end of Q3 and the first day of Q4, there was a network halt due to an anomalous consensus bug. Finally, the Hetzner change in terms of service sent a wave of transaction volatility in early November.

The “outage” narrative is changing, though, as the aforementioned factors previously causing poor performance have stabilized since the end of the second quarter. Network uptime since April 2022 has been consistently high, with over 99% uptime each month. TPS, as a quarterly average, also reached all-time highs in Q4 thanks to several network upgrades. During the year and through Q4, Solana continued to roll out upgrades related to QUIC, stake-weighted Quality of Service (QoS), and local fee markets.

QUIC

Solana replaced its old data transfer protocol, the user datagram protocol (UDP), with QUIC. Although QUIC shares some similarities with UDP, it allows for greater control over data flow. QUIC enables validators to exercise more discretion in sending and receiving transaction data to and from slot leaders. In other words, validators can more easily filter out the spammy transaction data that damaged the chain in times past.

Local Fee Markets

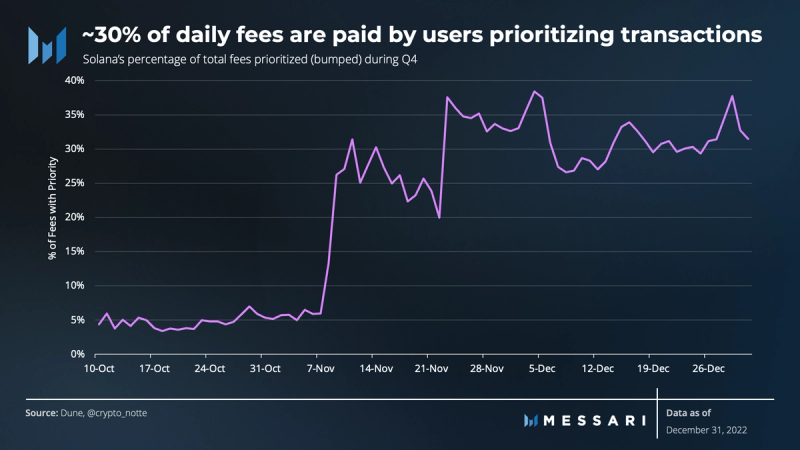

Solana accounts have hard-capped compute limits. Once reached, the ensuing transactions cannot modify that account’s state during a given block. Local fee markets allow users to send priority fees to validators to express an urgency to modify a specific account’s state before it has reached its compute limit in the current block.

The result is less spam (as it can be outbid) and more efficient blockspace markets.

On average, more than 30% of daily fees are paid by users prioritizing their transactions. As more wallets natively integrate priority fees, this average will likely increase.

Further, Solana local fee markets are working in times of high network activity. Base fees have remained steady, but priority fees are spiking in the more active areas of the network.

Stake-Weighted Quality of Service (QOS)

Instead of validators indiscriminately accepting and transmitting transactions, stake-weighting guarantees that a validator always has a right to transmit transaction packets to the leader. For example, a validator with 0.1% of stake can always transmit 0.1% of transaction packets to the leader. The previous indiscriminate approach left validators vulnerable to transmitting packets less than their stake weight. It would thereby push out smaller validators, leading to greater centralization.

Collectively, these three upgrades have brought performance stability to the network. Still, there was a QoQ decline (37.5%) in non-vote transactions (economic activity) and finished down 33.3% YoY, all likely due to market sentiment.

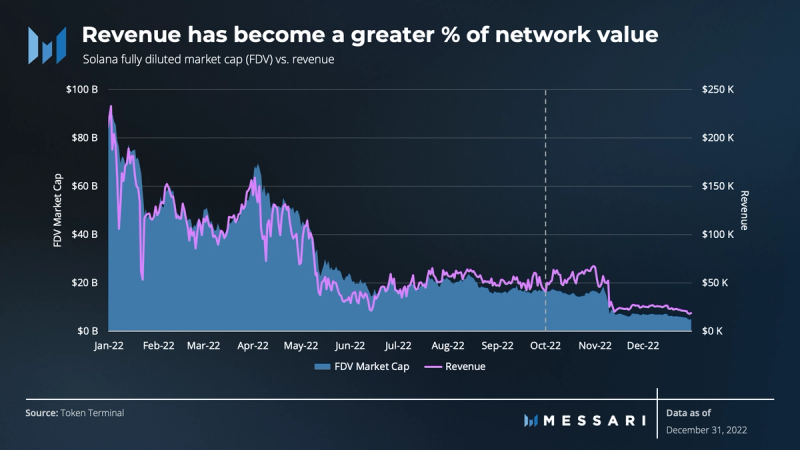

The presence of fee payers and stability in daily transactions drives revenue and value accrual to the network. Ideally, more users and transactions, albeit with lower fees, drive revenue and represent the fundamental value accrual.

To that end, there continues to be a correlation between revenue and network value, given that the volatility and trend of daily revenue are generally accompanied by movements in network value.

As seen in 2021 and throughout Q1 and Q2 of 2022, degraded network performance decreased network transaction activity and reduced the network’s continued revenue flow. This put downward pressure on network value during that time. However, the network upgrades brought more stability. The 49% decline in transaction fees combined with the 28% decline in revenue suggests that fundamentals like network stability, users, and transaction activity are becoming a more significant portion of Solana’s network value.

From a valuation perspective, the relationship between network value and revenue is also in line with the direction of the P/S ratio. The P/S ratio has fallen from 991x to 418x since Q1, suggesting that the network is undervalued compared to historical levels.

It is, however, essential to remember that blockchain assets are an unprecedented asset class that may also necessitate the application of unique valuation techniques. Therefore, traditional financial metrics such as revenue and P/S ratios may not be the most suitable when assessing these metrics.

Ecosystem and Development Overview

The factors that drive Solana’s fundamental activity come to light by evaluating its ecosystem, developer engagement, and growth strategy.

DeFi

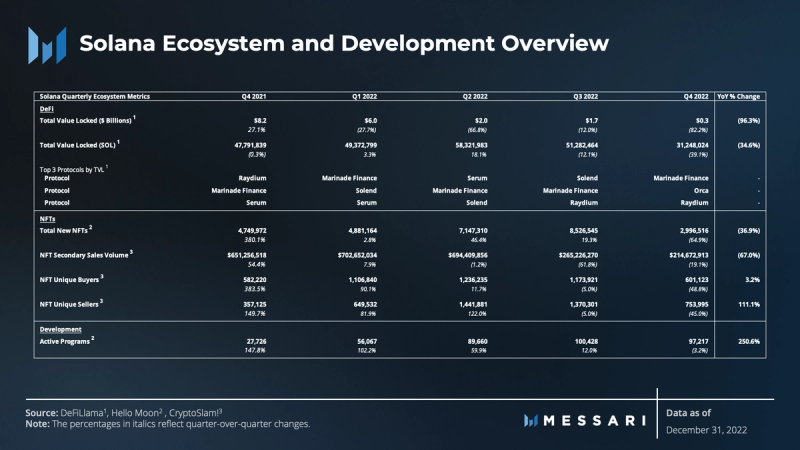

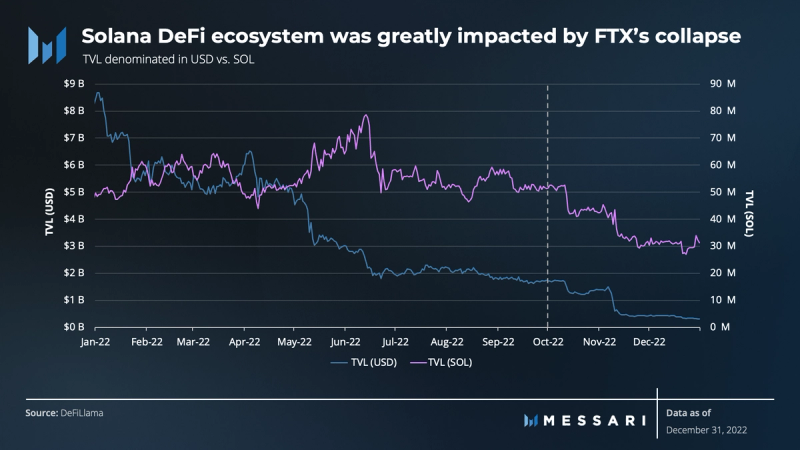

Solana DeFi was greatly impacted by the Mango Markets exploit in October and the collapse of FTX in November. Total Value Locked (TVL) suffered a massive decline due to the removal of Alameda’s on-chain operations.

Mango Markets Highlights

On October 11, Avraham Eisenberg, a cryptocurrency trader, executed a series of trades to artificially inflate the price of the Mango (MNGO) token. The trader profited from the increase, borrowing $116 million against the unrealized profits and withdrawing these funds from Mango Markets. This exploit was a classic example of cross-market manipulation that led to the eventual arrest of the trader.

FTX Collapse Highlights

- By the end of Q4, Solana TVL declined 26% in SOL terms post FTX/Alameda collapse, with SOL itself down 67% against USD.

- A community fork (OpenBook) of Serum had to be deployed, as FTX/Alameda held the upgrade keys to the original Serum contracts. The fork quickly garnered over $50 million in order book depth on the SOL/USDC pair.

- Sollet-wrapped tokens “backed” by FTX saw significant price decreases and began trading at steep discounts to the value of their intended collateral backing.

- The so-called “Solend whale” was liquidated, leaving the protocol with ~$6.5 million in bad debt. The DAO passed a vote to use the Solend treasury to make depositors whole.

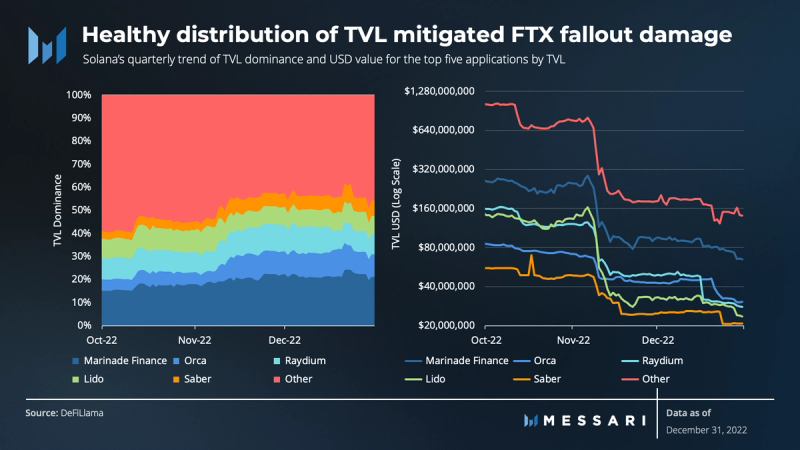

Nonetheless, a healthy distribution of TVL across applications has consistently existed on Solana, which may have mitigated further damage to the overall DeFi ecosystem. Currently, ~50% of TVL is locked across most of the long-tail DeFi protocols on the network.

Despite the difficult conditions, integrations unrelated to FTX are underway throughout Solana DeFi and are positioned to prop up and service additional demand.

Spot DEXs

OpenBook and Ellipsis Labs are two new decentralized exchanges gaining traction.

OpenBook is a community-run version of Serum V3 that was created in response to potential security issues with Serum’s upgrade keys.

Ellipsis Labs’ Phoenix order book builds upon Serum’s central-limit-order-book (CLOB) concept. It has design decisions that increase efficiency, such as removing the time-consuming process of entering DEX order books and setting the best bid and ask prices from the DEX design.

Derivatives and Structured Products

Plenty of teams are building in the derivatives, options, and structured products space, including Drift, Zeta Markets, Mango Markets, Friktion, 01, and Cega. Teams are tackling key problems such as sourcing liquidity, new asset support, cross-margin, and user onboarding.

Hxro network core protocols also went live during Q4. Hxro is an on-chain derivatives primitive that provides the underlying plumbing to support and facilitate any derivatives application built on Solana.

Liquid Staking Derivatives (LSDs)

Liquid staking became more prevalent across crypto during Q4. On Solana, Jito Labs’ JitoSOL experienced traction and generated headlines. Currently, Marinade and Lido are still leaps ahead in terms of market share, but that could change if higher yields for JitoSOL persist.

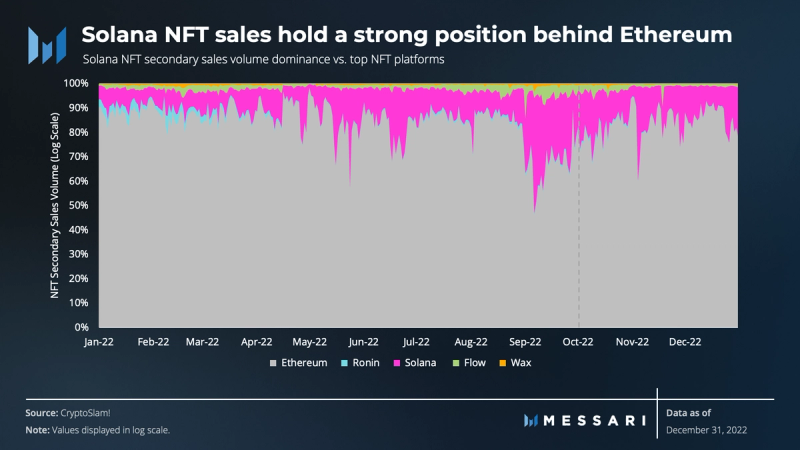

NFTs

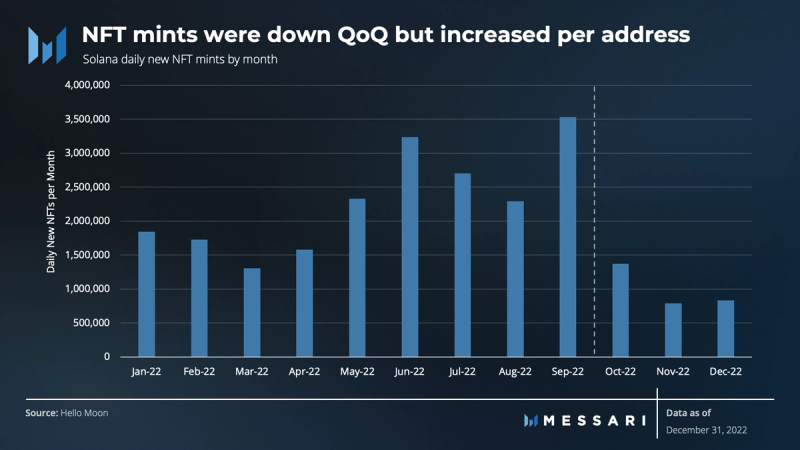

Solana’s NFT ecosystem also experienced a downturn, though not as drastic as DeFi, much like it did for most other networks. The total number of daily new NFTs decreased QoQ for the first time, down 65%. However, this decline came after a significant surge in Q3. Though minting was down QoQ, average NFT mints per address increased, signaling that power users are emerging.

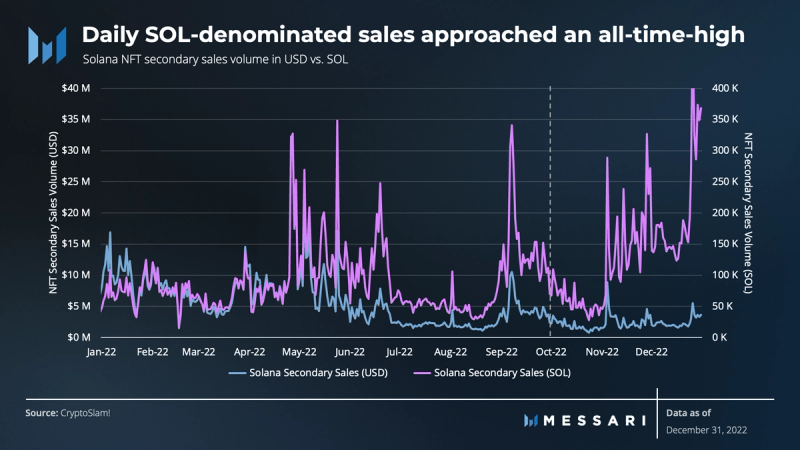

Despite the decline in new NFTs amidst the FTX fiasco, NFT sales activity remained relatively resilient. Daily SOL-denominated sales volume hit an all-time high in December as holders and traders rushed to adjust their NFTs’ valuations to cratering SOL prices.

Nonetheless, the NFT landscape of Solana is still developing aggressively.

In addition to the continued optimization of Metaplex’s Digital Asset Standard, Metaplex moved forward with several key initiatives during Q4, including:

- Developing compression for NFTs.

- Launching no-code solutions for less technical creators.

- Enhancing its popular, open-source minting solutions such as Candy Machine (V3).

- Enabling creators to enforce royalties.

The royalties debate has dominated the narrative in the world of NFTs. At first, aggregator adoption favored evading royalties whenever possible.

In addition to Metaplex, leading platforms Magic Eden and Cardinal have also announced a form of creator royalty protection at the protocol level. The debate has shifted, with several designs enabling creators to ban marketplaces that don’t enforce royalties. Time will tell which design wins in the long run.

Beyond the leading NFT platforms, Instagram and Facebook integrated support for Solana NFTs and went live during Q4.

Solana’s strategy and position in the NFT sector remain strong, maintaining its position as the second-largest network in terms of secondary sales volume behind Ethereum.

GameFi

As the crypto space positions itself to support GameFi, Solana Ventures leads the way. Its $150 million fund to boost the network’s gaming ecosystem has attracted additional investment funds (notably, Magic Eden’s Magic Ventures) and has sparked gaming traction. Developments like these have placed GameFi on the cusp of catalyzing a wave of activity across the crypto space, with Solana being positioned to grow its GameFi ecosystem.

Over 1,100 gamers attended the Solana Foundation Games Day in Lisbon, which took place the day before Breakpoint. They played dozens of complete (or nearly complete) games in the Solana ecosystem. There are currently 15 live and playable games, with 37 expected to launch by March 2023.

Some highly anticipated games include Star Atlas, ev.io, BR1: Infinite, Aurory, and Legends of Elumia. Aurory’s open alpha and Elumia’s public beta went live during Q4.

Frontier Use Cases

A notable expansion of additional use cases continued to pop up across the Solana ecosystem during Q4, including:

- Orbis – Enabled Solana developers to use their SDK to integrate social experiences in their applications.

- Aleph.im Network – Released Solana’s first fully open-source, decentralized indexer.

- Hivemapper – A decentralized mapping network launched and experienced initial traction.

- Homebase – Announced bringing real estate on-chain with Solana.

- Helium – Officially migrating to Solana Q1 2023.

- Bonk – Solana’s first viral meme coin.

The payments sector also continued to emerge. In early November, sportswear company ASICS teamed up with STEPN to introduce and distribute a custom running shoe dubbed the UI Collection. The shoes were sold through the end of Breakpoint and were only available to purchase with USDC via Solana Pay. Over five days, the UI Collection sold out and generated over $600,000 in sales with instant settlement and no credit card fees.

Despite the issues the Solana ecosystem has faced, there is still promise for the future. As new apps reinvigorate usage and Solana’s technology continues to develop, the downward trend of value accrual may reverse course as a result.

Developer Activity

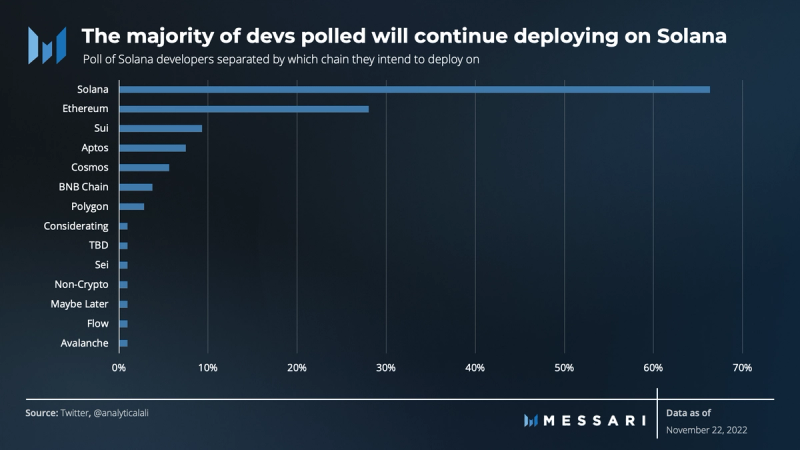

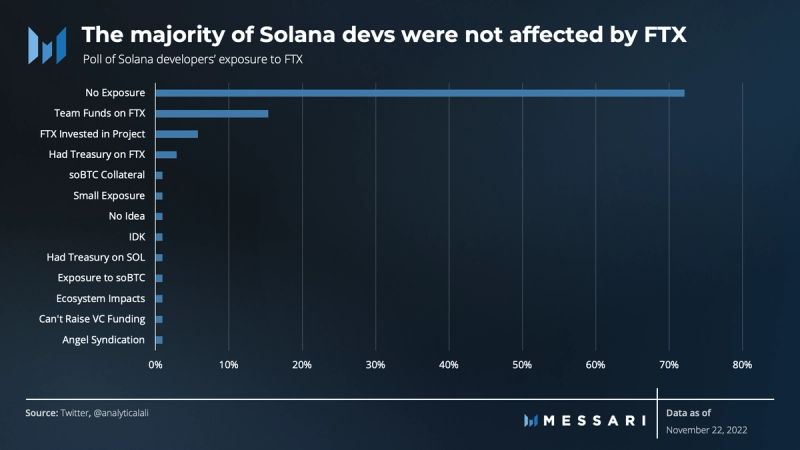

During Q4 and after the FTX implosion, Twitter was fraught with rumors that Solana development was faltering and that a mass exodus of Solana core devs was underway. The rumors were false and were primarily sparked by a data issue via Token Terminal.

Further, a Q4 survey was conducted to test this narrative. While surveys like these aren’t rigorous enough for academic research, they do offer directional data for a better understanding of reality. There were two main takeaways:

1. A material number of developers are deploying on other chains, especially Ethereum, but most (66%) devs polled are sticking exclusively with Solana.

2. 72% of developers reported that their team wasn’t affected by FTX.

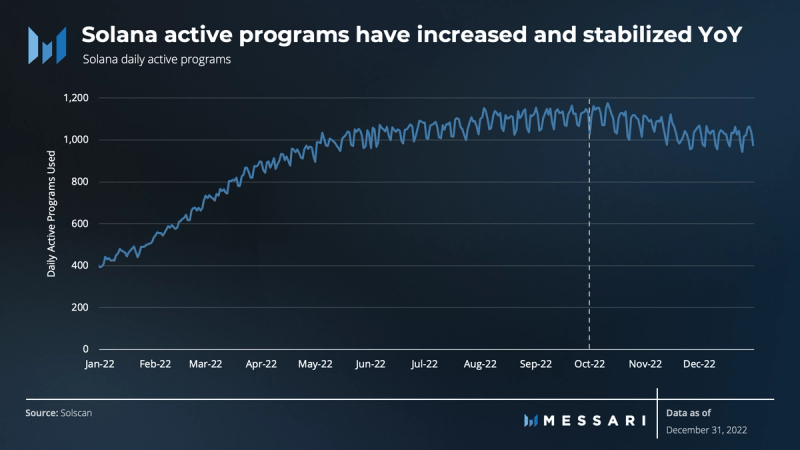

Active programs in a given period are another indicator of ecosystem development. As more applications have launched and grown their user base, the number of active programs has increased and stabilized.

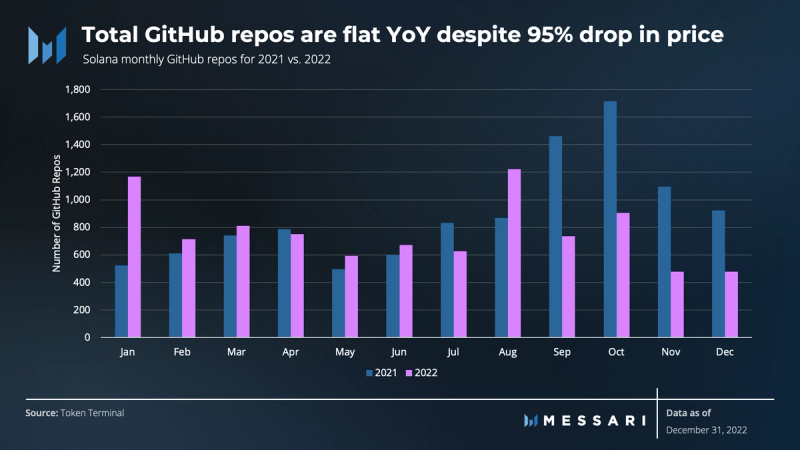

In previous reports, core developer involvement was also measured by data sources tracking the events in the Solana Lab’s GitHub repository.

However, the current data sources on developer data are imperfect. Not all commits are created equal, which can result in an incomplete picture of core developer activity.

Despite an incomplete picture, evidence still suggests that the number of GitHub developer repos has been steady YoY despite SOL prices dropping 95% over the same period.

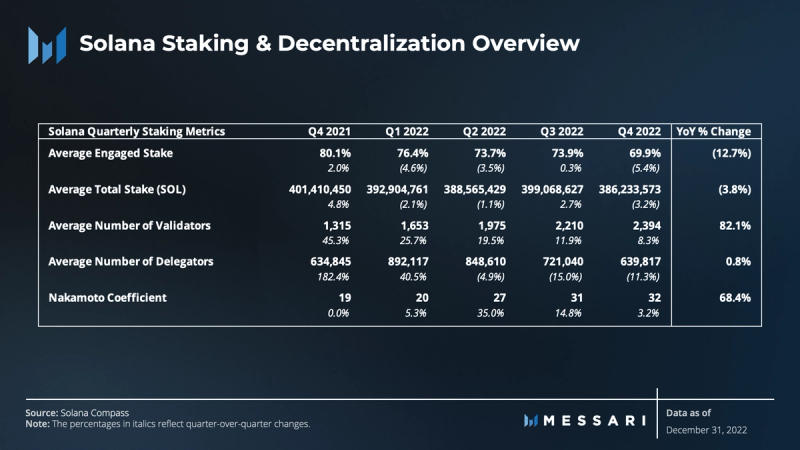

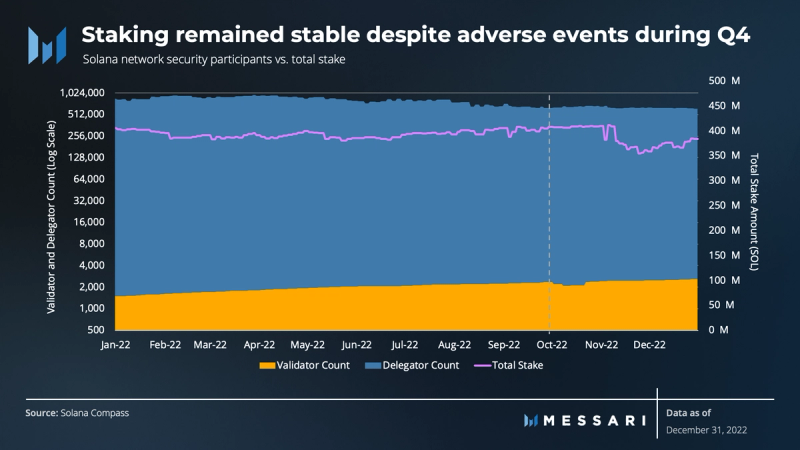

Staking and Decentralization Overview

The narrative also shifted regarding the health of Solana network infrastructure. There were fears that network security participants would flee for one reason or another.

During Q4, the Twitter community speculated that Alameda Research’s control of 13% of the total supply would lead to massive selling pressure. However, the tokens are locked and subject to chapter 11 bankruptcy. In other words, they may only be unlocked once the liquidation process is complete, which could take a substantial amount of time.

Ultimately, the staking and decentralization of the network remained relatively stable despite adverse events. The average engaged stake on Solana has held strong at ~75% over the last year.

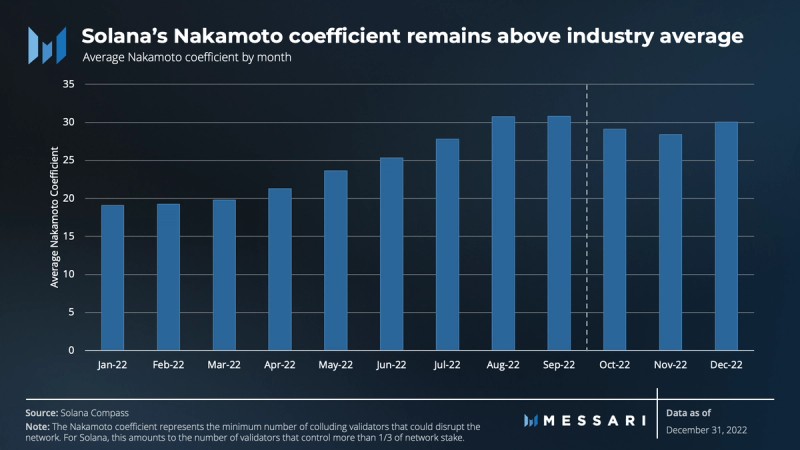

Solana’s Nakamoto coefficient of 32 remains above the industry average compared to other Layer-1 networks.

Although a high Nakamoto coefficient and growing validator set are beneficial, they don’t guarantee freedom from centralization risks. Metrics such as geographic diversity, data center ownership, and entity control over validators may also ensure more comprehensive network health.

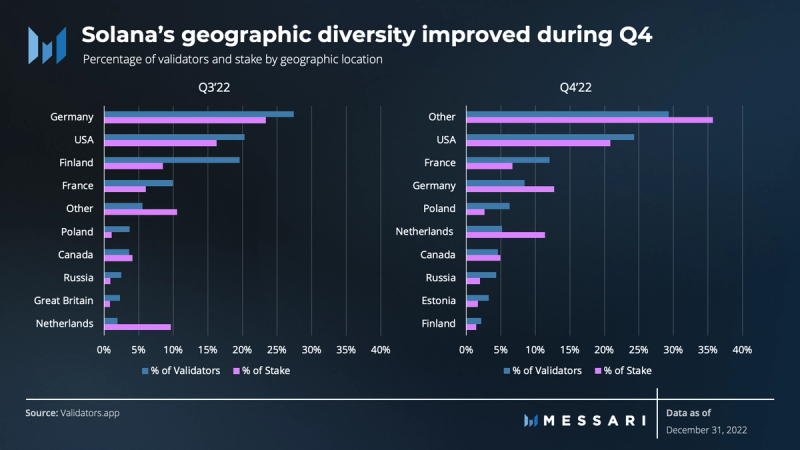

Solana aims to address the issue of geographical concentration that is typical for Layer-1 networks. Too many validators in the same location could jeopardize the health of a network due to geopolitical risks, regulations, and acts of nature, among other reasons.

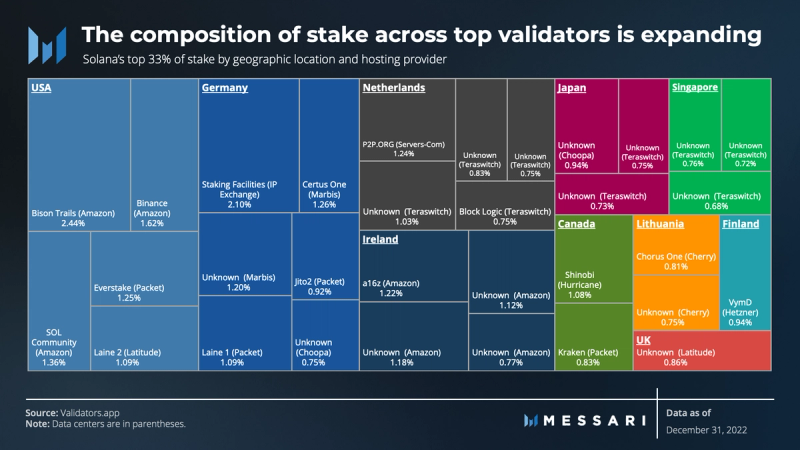

As of December 31, validators and stake were distributed across more than 35 geographic locations around the globe and more than 130 unique data centers.

While distributed globally, ~25% of Solana validators and ~20% of the total stake were located in the U.S. The “other” locations comprise ~30% of total validators and stake and include more than 25 different countries.

Datacenter concentration is another decentralization concern. Private data centers like AWS running validators could give their owners disproportionate power over the network. As of December 31, the total stake on Solana has been distributed such that no single data center is in the range of hosting 33.3%. The “other” category that makes up just over 30% of total stake consists of more than 125 unique data centers.

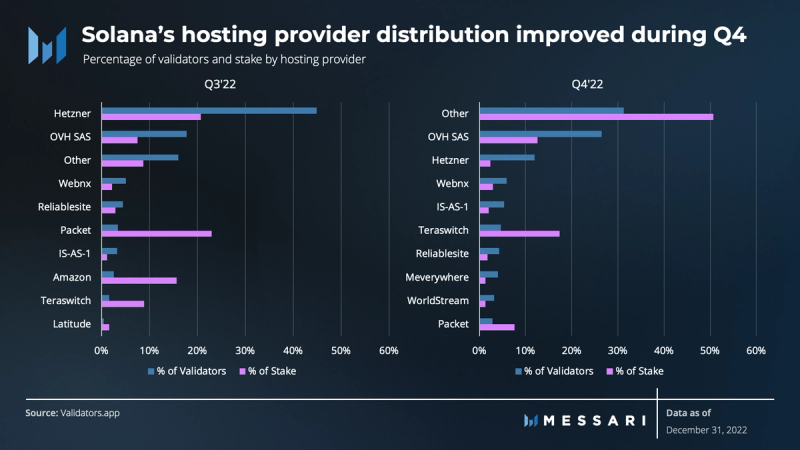

At the end of September, the Solana network had a concentration of validators and stake in Germany and the U.S. with Hetzner, a German web-hosting company. Hetzner hosted over 40% of the network’s validators and over 20% of the stake. This relationship caused the network to be heavily concentrated in Germany, with a particular focus on one data center.

In early November, Hetzner removed support for Solana-related activities and stated that its policy forbids the use of its servers for crypto-related activities. Fortunately, the concentration was not enough to interrupt the network. Still, the event exemplifies the potential risks of too great a network concentration in a single geographic location and data center.

When evaluating the top 32 validators that comprise the Nakamoto coefficient, a slightly different story unfolds compared to the apparent concentration in Germany, Hetzner, or even OVH SAS post-Hetzner migration.

More than half of validators controlling more than 33% of the network stake are hosted by Amazon and Teraswitch. Further, a third of this stake is staked in the U.S. Evaluating the composition of this stake across the top validators is essential, even if there aren’t enough to collude against the network. In this case, the network could be in jeopardy if this group of stake made its way to a more concentrated geographic area like the U.S. or a few data centers such as Amazon or Teraswitch.

Ultimately, the decentralization and health of the Solana network remain well intact and in a better position after validators and stake migrated from Hetzner to dozens of other geographic locations and data centers.

Competitive Analysis

Solana has witnessed high growth since its inception through Q3 2022, but it has since dropped in its position as one of the top 10 most valuable Layer-1 networks. Here, we evaluate Solana’s progress versus the top five Layer-1s by TVL and those with the largest number of DeFi protocols.

Solana’s valuation dropped significantly at the onset of FTX’s undoing. The peer group was also impacted, but not as significantly, and, in particular, Polygon.

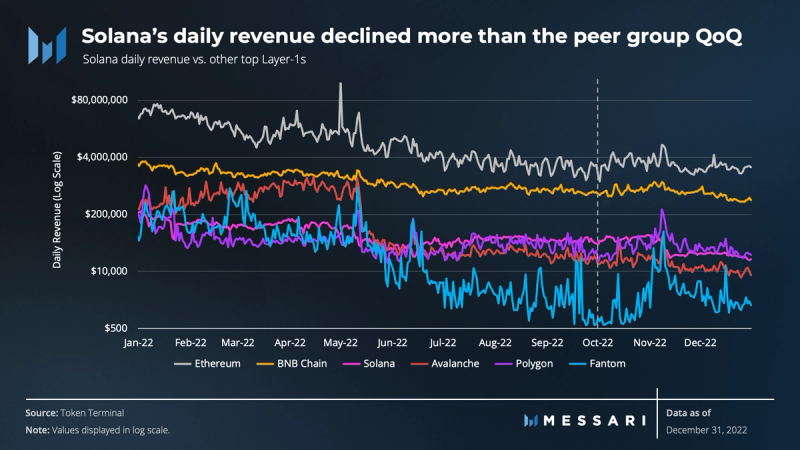

Similarly, Solana’s daily revenue trended downward, even though total daily transactions increased. Therefore, the decline in revenue was attributed to the decline in transaction fees. The rest of the peer group (minus Polygon and Fantom) experienced only modest declines throughout the quarter.

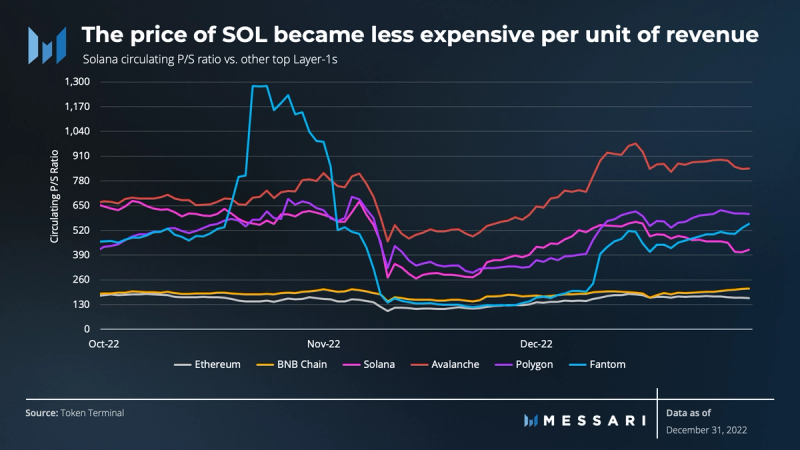

Over the quarter, Solana’s P/S ratio decreased compared to the peer group. The change in P/S gauges a protocol’s revenue and gives a sense of the amount and cost of transactions processed by the protocol. Because Solana’s value change was more significant than its revenue, SOL became less expensive per unit of revenue.

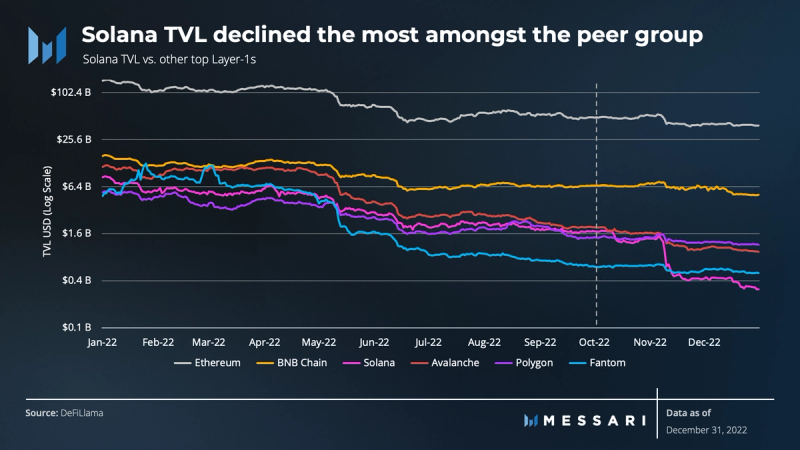

Although Q4 affected the crypto DeFi market, Solana’s TVL declined the most. Declines in TVL are generally evaluated in USD, so the native asset’s decline in value represents the shift in TVL versus the actual utilization of the native asset in DeFi. While TVL in USD was down a staggering 82%, the amount locked denominated in SOL declined by less (39%).

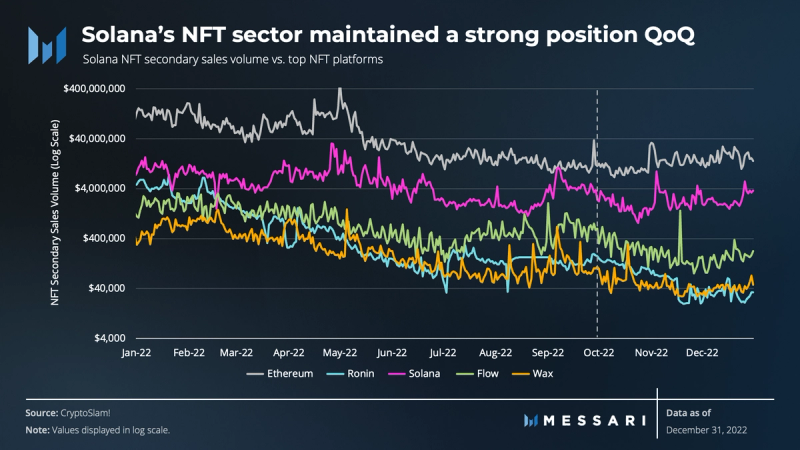

Several developments across Solana’s NFT sector allowed it to maintain a strong position relative to a peer group of the top five L1s (including Solana) by all-time secondary NFT sales volume.

Though Ethereum still dominates the secondary NFT market, Solana continues to hold a strong position behind Ethereum and is well ahead of the rest of the peer group.

Qualitative Analysis

Key Events, Catalysts, and Strategies for Ecosystem Growth

With the bear market continuing and the FTX catastrophe unfolding, Solana’s expansion strategies and network upgrades appeared to be overshadowed throughout Q4. As highlighted in this report, network upgrades continued to improve functionality. The NFT landscape of Solana continued to progress with integrations, including those with Instagram and Facebook. GameFi and fringe use cases, especially in DePIN, continued to march toward catalyzing a new wave of activity. Aside from these ecosystem developments, other aspects of the Solana strategy have been running in the background. While not mutually exclusive, Q4’s strategic elements can be generalized into three areas:

- Technical Developments — Integrate, decentralize, and improve efficiency and functionality.

- User access and experience — Captivate users with greater user access and experience.

- Community — Acquire developers and drive adoption through community building.

Technical Developments

In early November, Google Cloud expanded its involvement with Solana. They started running a block-producing validator and announced the addition of Solana data to BigQuery. Additionally, Google Cloud plans on introducing Blockchain Node Engine to Solana in 2023, so users can run nodes on the cloud. Google Cloud also plans to begin accepting crypto payments.

In a live demo, Jump Crypto showcased Firedancer, the team’s upcoming validator client. The demonstration achieved 1.2 million TPS utilizing synthetic transactions that closely mimicked those of a Solana validator. Implementations such as Firedancer and client diversity can make the network less susceptible to downtime.

The Jito Foundation released Jito-Solana, a third-party validator client enhanced with maximum extractable value (MEV) features. This new validator software brings several benefits, notably providing network validators and stakers with MEV profits, reducing spam, and improving the network’s efficiency.

Squads Protocol, a multi-signature standard on Solana, brought Account Abstraction (AA) to Solana to enhance UX and security regarding the custody of digital assets.

Solana’s Neon EVM was set to go live on Mainnet in December but was postponed due to the filing process involving third parties. The Neon EVM will allow Ethereum-based applications to build on Solana without changing their codebase. Once live in 2023, development activity on the network may experience an increase.

User Access and Experience

Helium Mobile and Solana Mobile partnered to bring the first cryptocarrier to Saga phones in the U.S. Their goal is to enable users to connect seamlessly to the Helium 5G network and partner networks nationwide.

Ledger also announced that it will update Ledger Live to support Solana Mobile Stack (SMS). The update will enable Solana Mobile users to connect their Seed Vault with Ledger Nano hardware wallets.

Payments platform Stripe debuted its fiat-to-crypto payments onramp with 11 of the 16 initial projects supported built on Solana.

Community

In addition to ongoing efforts related to Solana University, Solana Foundations Hacker House events were organized and scheduled for 2023 as well as the Solana Sandstorm Hackathon by Lamport DAO and Helius Labs.

Developer platform Buildspace announced Solana Core, a six-week program designed to enhance Solana development knowledge, while Thirdweb brought its full-stack Web3 development kit and network of 60,000 builders to Solana.

Most notably, the bear market did not slow the attendance of Solana’s annual Breakpoint conference in Lisbon, Portugal. The multi-venue event saw packed rooms, with 50% more attendees than in 2021.

Ecosystem Challenges

During the quarter, the ecosystem experienced a series of challenging events. This report has already mentioned the anomalous network halt, rebuilding of DeFi, Mango Markets exploit, and Hetzner’s terms of service.

However, the elephant in the room was the impact stemming from the FTX implosion. Concerns about Solana’s exposure were prevalent, prompting the Solana Foundation to share details about its exposure to FTX following the exchange’s bankruptcy filing.

According to the statement, the Foundation held ~$1 million in cash or cash equivalents on FTX.com, which is less than 1% of the group’s USD holdings. The Foundation also disclosed that it held ~3.24 million FTX Trading LTD common stock shares, ~3.43 million FTT tokens, and ~134.54 million SRM tokens. The Foundation is unaware of how these and other FTX/Alameda assets will be settled following the Chapter 11 proceedings.

The Road Ahead

Much of the road ahead continues to reflect what the Solana ecosystem has been outwardly working on for several quarters. These developments include continued network upgrades, Neon EVM, Firedancer, Solana Mobile Stack (SMS), and community building, to name a few.

Developers rallied behind the list of initiatives highlighted in a thread put out by Solana Labs Co-founder Anatoly Yakovenko in October. The initiatives include:

Asynchronous Block Production

Asynchronous block production decreases the work slot leaders must do to pack blocks. Without this feature, the slot leader (block producer) is currently performing two critical tasks:

- Execute all incoming pending transactions and ensure that signatures are valid and all accounts have correct paying balances for fees.

- Pack these pending transactions into a block, collect the transaction fees, and send the block out to other validators for consensus and confirmation.

Asynchronous block production means the block producer only needs to do step 2. It assumes optimistically that all signatures are valid and therefore skips the first step. Therefore, it sends the block directly to the validators that will validate the proposed block. Fee-paying accounts that submit invalid signatures are still debited a transaction fee to mitigate spamming the network.

The main benefit of asynchronous block production is that a block producer can dedicate resources to packing the highest priority fee and most parallelizable transactions into a single block. More efficient priority fee consumption and tighter-packed blocks result in more fees collected by the block producer and faster confirmations for the user.

Diet Clients / Light Clients

“Diet” or light clients sample nodes for small transaction units instead of downloading the full blockchain state. They rely on the assumption that the set of nodes they sample is honest. If the honesty assumption holds, light clients allow users to contribute to network security by ensuring honest nodes aren’t eclipsed by a dishonest majority.

Multiple Leaders per Slot

Typically, one validator does the work of validating each slot or block. Said validator becomes the “slot leader” for roughly 400 milliseconds. Multiple Leaders is a design change that would increase bandwidth for block production so multiple validators can occupy the leader slot.

Each leader would propose their own stream of transactions (effectively, a tree list of transactions), with the final order becoming the combination of these streams. The resulting competition from multiple leaders would increase efficiency in the MEV market.

Formal Verification

Formal verification utilizes Rust-based code verifiers such as Kani and Prusti to verify programs in the Solana-program-library and other important, widely used libraries like those found in Anchor.

The end goal of formal verification would be to improve the security of Solana programs. Code verifiers would be able to automatically check for issues or errors within a given program. Making strict use of them — especially on core contracts — should improve the security of those contracts.

Additional Smart Contract Languages

Solana is rolling out support for the smart contract language Move. This language is designed to be platform-agnostic and, once fully implemented, may attract developers to Solana’s library of LLVM-compatible smart contract languages.

Closing Summary

Despite the FTX chaos, Q4 reflected that the network and ecosystem remain resilient. Advancements in network functionality continued, along with several other potential catalysts for growth. Solana’s mission toward adoption remains intact, as evidenced by continued development, further integrations with partners like Instagram and Facebook, and ecosystem expansion into the world of NFTs, GameFi, and DePIN. Solana continues to work to attract new users as it seeks out new partners and expands into more ecosystems.

Solana DeFi imploded, and it will be a challenge to rebuild. Nevertheless, integrations unrelated to FTX are underway throughout Solana DeFi and are set to bring in additional demand.

The staking and decentralization of the network remained relatively stable despite adverse events. Solana’s network health remains well intact and is in a better position after validators and stake migrated from Hetzner to dozens of other geographic locations and data centers.

Much lies ahead for the Solana network and ecosystem. Solana will continue to release a multitude of initiatives, including network upgrades, ecosystem developments, and community efforts, to name a few. After a tumultuous year fraught with one challenge after another, light appears to be at the end of the tunnel heading into 2023.