Key Insights

- Comdex is a Cosmos-based ecosystem that includes a DeFi focused Layer-1 blockchain and a close-ended Software-as-a-Service (SaaS) platform for commodity trading and settlement.

- The Comdex chain recently had the launch of its first three applications: cSwap, a hybrid orderbook-automated market maker (AMM) decentralized exchange (DEX), Harbor, a collateralized debt position (CDP) protocol (with its own native stablecoin, CMST), and Commodo, a decentralized money market protocol.

- As Comdex progresses along in its roadmap, it plans to expand the Comdex chain ecosystem by releasing a wide range of applications (money markets, perpetuals, synthetics, trade financing, etc.) and by attracting external developers.

- While Comdex faces stiff competition in its standalone DeFi offerings, its foundation with underserved commodity traders offers a unique and promising avenue for growth.

Introduction

From dYdX to Delphi Labs, many of crypto’s best and brightest are waking up to the possibilities and technical advantages of the Cosmos ecosystem. But despite the recent excitement, the ecosystem is underwhelming in its current state. Its decentralized finance (DeFi) offerings in particular, especially after Terra’s implosion, are paltry, fragmented and underdeveloped, holding a mere $1.1 billion.

Back in 2018, Comdex set out to use Cosmos and its ecosystem to streamline and digitize commodity trading. However, the lack of DeFi primitives in Cosmos constrained Comdex’s design space and made it difficult to build a comprehensive offering. As a result, Comdex shifted its focus to creating the building blocks for Cosmos DeFi through its own Layer-1 blockchain.

Comdex’s modular approach enables developers to spin up applications that allow users to collateralize, create and exchange tokens. All three of the live applications on the Comdex chain were released over the past two months, so it’s still too early to measure outcomes. However, in the near term, Comdex is bringing one of the most complete and composable DeFi experiences to Cosmos. Looking further out, Comdex is laying the foundation to fulfill its initial purpose: to serve as a conduit between traditional markets and DeFi.

Background

Comdex was founded in 2018. The Comdex team opted to use Cosmos (application-specific blockchains) in order to fulfill scalability and privacy requirements for its Enterprise Trading Platform. The Enterprise Trading Platform went live in 2019.

In 2020, due to regulatory hurdles associated with cross-border fiat payments rails (e.g., in-person KYC/AML) and the lack of native primitives on Cosmos, the Comdex team shifted its focus to building out the Comdex chain. In Q4 2021, Comdex launched its mainnet and released the chain’s native token, CMDX.

The rollout of the Comdex ecosystem began in 2022. So far there have been a number of notable milestones:

- The launch of its validator arm Zenscape

- Mainnet for hybrid orderbook-AMM DEX cSwap

- Mainnet for CDP protocol Harbor

- Introduced over-collateralized stablecoin Composite (CMST)

- Airdropped native governance token HARBOR

- Mainnet for decentralized money market protocol Commodo

Comdex Ecosystem

Source: DCentral Austin

In its current state, Comdex is best understood as an ecosystem. One part of the ecosystem is services, such as Zenscape and the Enterprise Trading Platform. The other part of the ecosystem is the applications built on the Comdex chain.

Comdex Chain

The Comdex chain is a Tendermint-based, IBC-enabled, layer-1 blockchain built on top of the Cosmos SDK with CosmWasm-integration.

Comdex offers permissionless entry into its validator set and also has its own Validator Delegation Program. The program runs in six month cycles, where Comdex delegates up to 3 million CMDX per validator based on strategic value and setup strength.

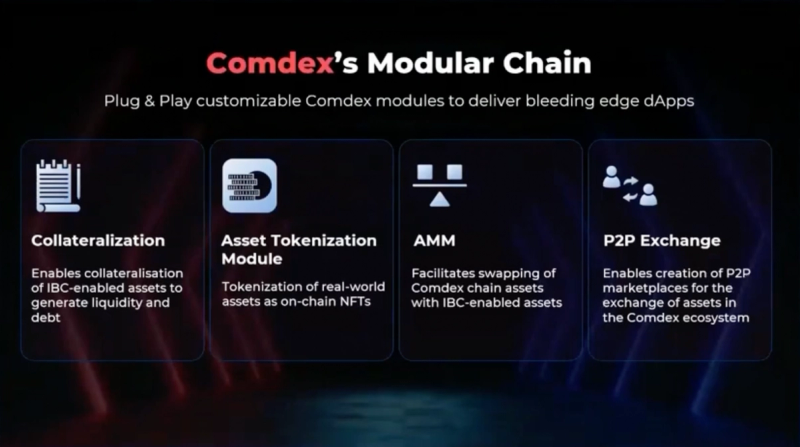

As for building on the chain, developers are required to whitelist new applications and assets through governance. They can then build their applications using 13 customizable, plug-and-play modules. These modules, broadly, fit into one of the four following categories.

Source: Persistence Blog

As of now, there are three live applications on the chain, cSwap, Harbor Protocol and Commodo. All three projects were developed by the Comdex team.

Harbor Protocol and Composite Stablecoin (CMST)

At a high level, the Harbor Protocol will function like Maker. It will enable overcollateralized loans by allowing users to lock governance-approved IBC assets as collateral in smart contracts (“vaults”). By doing so, users will mint Composite (CMST), an IBC-enabled stablecoin pegged to the U.S. dollar.

As of now, there are four live vaults. One live vault is the USDC “Stable Mint” vault. This module allows users to directly swap USDC for CMST, rather than having to borrow CMST. This setup ensures peg stability by maintaining a reserve to directly swap CMST for USDC (given sufficient stablecoin liquidity). The other three live vaults allow users to mint CMST against ATOM. Each vault has different parameters, flowing down from the minimum collateralization ratio. The more aggressive (lower) the ratio (i.e., ATOM-A at 140%), the more stringent the parameters (stability fee and debt ceiling).

Harbor earns revenue through stability fees (interest on CMST), drawdown fees, and liquidation fees. Once fees collected are above a certain threshold, they are used to buy back and burn HARBOR tokens from the supply through “surplus auctions.”

Commodo

Commodo is Comdex’s most recent release. Similar to Aave, Commodo is an IBC-native decentralized, collateralized lending and borrowing platform for digital assets. It’s primarily designed to provide passive yield to IBC asset holders.

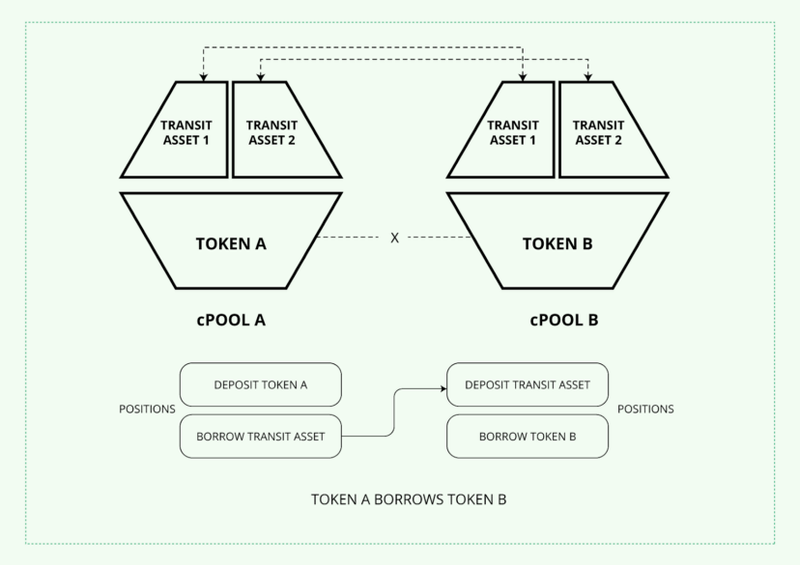

Commodo aims to solve two recurring pain points in DeFi lending and borrowing: fragmented liquidity and shared pool security. The platform’s innovation is the concept of isolated money markets, cPools, using two preset bridged assets: (1) ATOM and (2) CMST, Comdex’s overcollateralized stablecoin. Liquidity is provided by pooling digital assets with the two preset bridged assets, ATOM and CMST. This creates money market modules like OSMO-CMST-ATOM and ETH-CMST-ATOM. In this way, Commodo can offer a single lending pair for each individual token, concentrating liquidity rather than fragmenting it across multiple pools.

From a security perspective, since all transactions are routed through the same bridge assets (CMST or ATOM), only these assets require trust. If a paired token is compromised, only the pool for that token will be affected, limiting risks to a single lending pool.

Commodo doesn’t have its own governance token. Rather, platform upgrades and development proposals that occur through the Comdex governance process will be controlled by $CMDX token holders and stakers. Value will accrue back to CMDX holders as the premium difference between lending and borrowing rates is used to buy back the CMDX token.

Commodo just launched on January 7th, so listings are still relatively sparse. As of now, users can borrow and lend CMDX, CMST, and ATOM.

cSwap

cSwap is Comdex’s hybrid orderbook-AMM. It enables traders to swap between IBC-enabled assets. Liquidity providers (LPs) can passively manage liquidity by depositing assets into liquidity pools and earn trading fees (paid in CMDX). cSwap’s AMM determines pricing algorithmically through a constant product market maker (CPMM). However, LPs can also provide liquidity using limit orders. Similarly, users can place trades through market orders (executed at the best available price) or limit orders (only executed at a specified price).

In addition to assets, cSwap’s trading pairs also need to be whitelisted through Comdex governance. Another parameter determined by governance are “internal” liquidity rewards (25% of CMDX supply is allocated for “Rewards”).

cSwap’s liquidity mining rewards system uses two types of liquidity incentives, external and internal. External liquidity incentives work just like those of other AMM-DEXs. They allow any individual or group to incentivize liquidity pool(s) of their choice. The internal rewards system, however, introduces the concept of “metapools” to abate mercenary farming. cSwap calls this the Master Pool – Child Pool Rewards System, where LPs are required to provide liquidity to a “master pool” in order to maximize internal (i.e., native token) rewards. Master pool liquidity provision effectively serves as collateral, disincentivizing LPs from instantly selling rewards.

As of now, cSwap has fourteen live pools, covering most of the major Cosmos ecosystem tokens, with a CMDX/ATOM master pool.

Enterprise Trading Platform

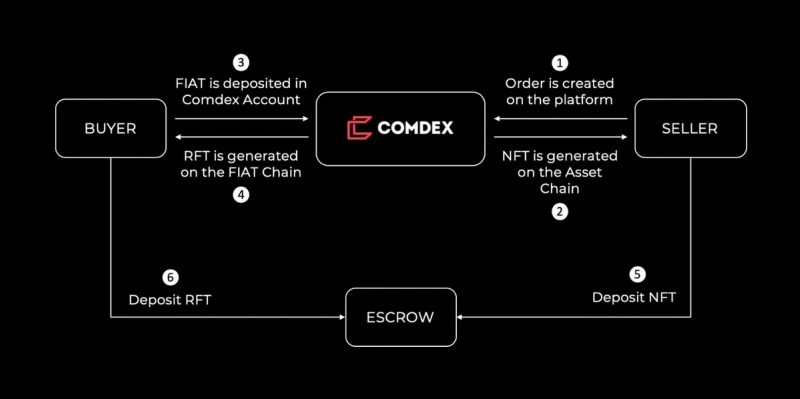

The Enterprise Trading Platform facilitates cross-border trading lifecycles (end-to-end) for physical commodities. It does so on a permissioned blockchain (Persistence SDK), as a closed-ended SaaS application without any cryptocurrency at the interface layer. Instead it conducts settlement by minting and exchanging NFTs that represent physical commodities and fiat deposits (“RFTs”) on the Persistence blockchain. To split the intensive storage and transaction requirements, commodity NFTs and fiat deposit RFTs are stored on separate chains (“‘Asset” and “Fiat”) while transfers are IBC transactions routed through the “Hub” chain.

How the Comdex Enterprise Trading Platform Works Source: Persistence Blog

The Enterprise Trading Platform aims to replace the archaic methods of communication, settlement and record-keeping that pervade the commodities trade. Leveraging the blockchain brings speedier settlement, more transparency and immutability (more trust) to the process.

However, new regulations (i.e., Singapore’s Payment Services Act, 2019), external dependencies (i.e., fiat deposits), fragmentation (i.e., lack of trade financing) and the closed nature of the platform have hindered growth, and leaving a lot to be desired in terms of offerings. Around its launch, in 2019, the rest of the Cosmos ecosystem also lacked comprehensive, easy-to-use, interoperable solutions (stablecoins, money markets, synthetics, etc.). The Comdex team developed the Comdex Chain and its attendant ecosystem to help fill some of these gaps.

Zenscape

Zenscape is Comdex’s validator arm. It primarily exists to increase Comdex’s participation and visibility in the Cosmos ecosystem by validating various chains.

Zenscape (in coordination with Comdex) has also made several infrastructure support services available for ecosystem stakeholders.

- IBC Relayers: Setting up, running & maintaining the IBC relayers to make sure the communication between the chains is reliable and users are able to transfer their assets between chains.

- Tendermint-Based Chain Snapshots: Isolating, tracking, and analyzing pruned snapshots of Tendermint-based chains.

- Public Remote Procedure Call (RPC): Providing public RPC/REST endpoints, ensuring high availability for Cosmos Hub and other ecosystem projects.

CMDX Token

CMDX is the native token for the Comdex blockchain. The token serves five functions in the ecosystem:

- Usage – Gas fees to use the network (i.e., its dApps) are paid in CMDX.

- Staking – CMDX holders can delegate their tokens to validators to run and secure the network. In return, they’ll earn gas fees and staking rewards (issued in CMDX).

- Governance – CMDX holders govern protocol decisions

- Collateralization – CMDX will be able to be collateralized across the Comdex ecosystem.

- Rewards for liquidity provision – CMDX tokens are distributed as rewards to liquidity providers on the network

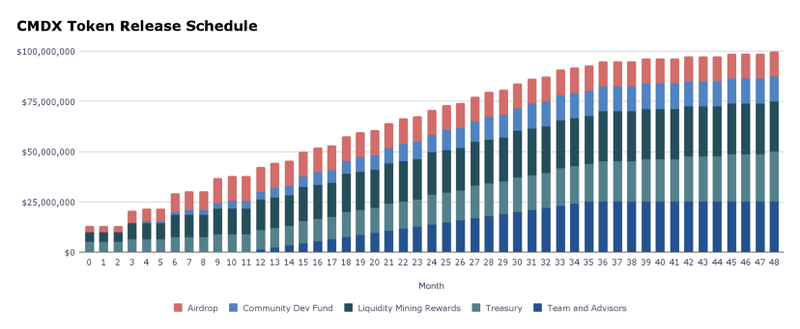

Token Distribution and Economics

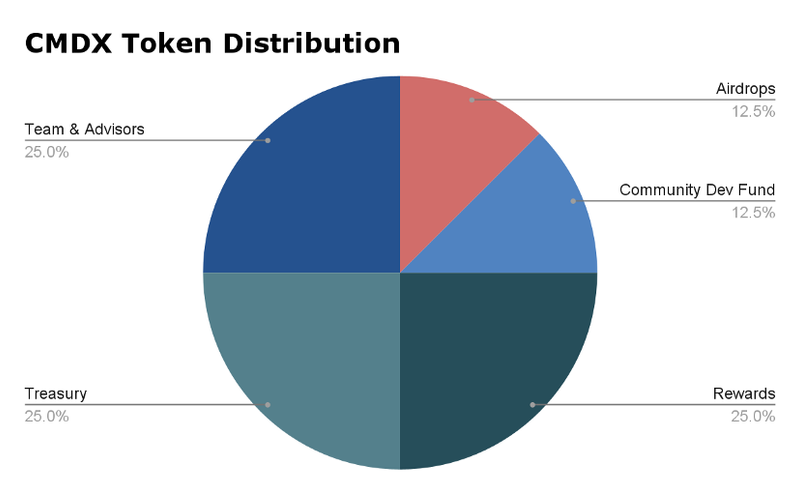

The supply of CMDX is inflationary (30% in the first year and a 25% reduction in inflation every subsequent year) with a maximum supply of 200 million CMDX. 100 million CMDX minted at genesis, and the remaining CMDX will be unlocked over the following four years (three years remaining as of this writing).

- Airdrops: 12.5% (12.5 million CMDX)

- Issued to ATOM, LUNA, OSMO, and XPRT holders and stakers. At listing, 2.5 million CMDX was unlocked, and then 2.5 million CMDX unlocks every three months until the total amount (12.5 million CMDX) is distributed.

- Community Development Fund: 12.5% (12.5 million CMDX)

- Used to incentivize developers to build on the Comdex protocol.

- Rewards: 25% (25 million CMDX)

- Used to incentivize certain value-add functions across the ecosystem — in particular, liquidity provision on cSwap. Spread across a 36 month period.

- Treasury: 25% (25 million CMDX)

- Team and Advisors: 25% (25 million CMDX)

In addition to CMDX, certain dApps will have their own native tokens as well. So far Harbor has launched and started the airdrop for its own governance token, HARBOR.

Traction

Comdex Chain

While the Comdex Chain was launched in November 2021, its first application (Harbor Protocol) went live a year later. This means there isn’t much in the way of activity so far, but we can still look at a few key metrics.

As of this writing, there are 80 active validators that have produced a cumulative 5.4 million blocks. Together, they stake roughly 96 million CMDX, about 70% of the token’s circulating supply. Additionally, Comdex’s Nakamoto coefficient is one of the highest in the Cosmos ecosystem at 13.

Enterprise Trading Application

According to Comdex, the Enterprise Trading Application hason-boarded18 organizations and facilitated $160 million in trade volumes. For the most part, these organizations have been small and medium-sized enterprises (SMEs) based out of Southeast Asia.

As mentioned earlier, for a number of reasons, Comdex shifted its attention and resources away from the Enterprise Trading Application to develop the Comdex Chain and its ecosystem. So it’s unlikely that the Enterprise Trading App has seen much recent growth, since the only work done on the application has been around maintenance and feature-specific development.

Ecosystem

Zenscape currently validates 10 Cosmos chains. Notable chains include Osmosis, Umee and Akash.

The Harbor Protocol, launched about six weeks ago as of this writing. So far about $700,000 of its CMST stablecoin has been minted. 92% of CMST has been minted through the USDC “Stable Mint” vault, while the more recently deployed ATOM vaults have contributed roughly 8% of CMST supply.

cSwap went live around the same time and has had similarly light activity. However activity has picked up since Comdex governance approved a proposal to incentivize liquidity across pools. As of this writing, its 14 pools have $698,000 in total liquidity.

Commodo, as mentioned, launched a few days ago. As of now, it has $100,000 in deposits.

However, there is a rewards program in place for those who provide liquidity to the CMDX-ATOM master pool on cSwap. In return for doing so, they will be able to borrow CMDX or ATOM at subsidized rates, which could create a virtuous flywheel for cSwap liquidity (LP -> borrow -> LP borrowed tokens).

Partnerships

Comdex has also recently announced a number of partnerships with other projects. Some partnerships include:

- White Whale: Has deployed its arbitrage infrastructure and flash loan vaults on the Comdex chain, enabling faster and more efficient liquidations and making it easier for users to take flash loans on Commodo.

- Skip Protocol: Plans to integrate its frontrunning-resistant MEV protocol, protecting users against sandwich attacks while increasing staking rewards by “recapturing” MEV (via payment for prioritization).

- Stride: To create liquid staking derivatives for CMDX (StCMDX) and CMST (StCMST).

- Crescent: Has listed CMDX and CMST on its DEX with incentivized pools. Comdex plans to allow LPs to use positions as collateral in Habor.

Roadmap

The Comdex roadmap can be divided into two sections. The first is building on existing infrastructure and applications. The second is releasing new primitives.

The roadmap items that fit cleanly into the former primarily center around the Harbor Protocol, Commodo, cSwap and Zenscape. Harbor governance will likely whitelist additional collateralized debt position (CDP) vaults, which will allow users to mint the CMST stablecoin using many different IBC-assets. Similarly, there will likely be additional trading pairs and assets added to cSwap and Commodo, respectively, and an increase in liquidity as provision and borrowing are incentivized. Finally Zenscape is currently developing Telegram alert bots, for governance proposals and chain upgrades, and wallet tracking analytics platform.

Beyond building out a complete DeFi suite, Comdex’s end goal is to attract real world commercial and financial activity. The ShipFi application on the roadmap has particularly strong synergies with the Enterprise Trading App as it will facilitate the creation and exchange of commodity trade finance debt. This application will round out the Enterprise Trading App’s offerings for SMEs and again open up a fairly inaccessible market for retail lenders.

Zooming out, these roadmap items start painting a more complete picture of how this ecosystem will work. The first phase (ongoing) is the deployment of a DeFi ecosystem. The second phase will be the ecosystem’s integration with the Enterprise Trading Application.

Bug Bounty

While Comdex has been audited by Oak Security, they also plan to launch a bug bounty program to keep current with the evolving nature of the project and make sure new applications aren’t vulnerable to exploits.

Competitive Landscape and Outlook

Given Comdex’s breadth, its competitive landscape is best understood from different angles.

Cosmos DeFi

The first angle is a broad look at Cosmos DeFi. When it comes to a multi-faceted DeFi base layer, Comdex is the one of the most comprehensive offerings since Terra. The closest competitors in this realm are most likely Canto, Kava, and Cronos.

These three protocols are also Cosmos-based Proof-of-Stake blockchains that offer a DEX and lending market. By most metrics, Cronos is the largest of the three, however all four projects (including Comdex) have notable differences. For example, Comdex offers the only DEX with an orderbook (native limit orders), while Canto’s DEX protocol is immutable.

Another key difference is in the overcollateralized currencies. Cronos doesn’t offer a native stablecoin of its own, and Canto’s NOTE is not actually a stablecoin. Rather, it is a unit of account around the dollar whose stability is maintained by varying lending rates. While Kava’s stablecoin USDX is overcollateralized, its market price has been greater than or equal to $1.00 for only 52 days over the past two years.

Given that these chains have had a head start on Comdex, Comdex’s success will depend on both seamless execution and its unique “real-world” offerings. In addition, Comdex faces competitors for each of its verticals — especially stablecoins and DEXs. While a single, complete DeFi experience does confer benefits, such as reducing dependencies – from IBC, of course, and around composability (i.e., relying on other projects to integrate assets) – this isn’t as big of a selling point in Cosmos, since IBC exists to make moving between blockchains seamless.

Stablecoins

While Kava’s USDX is the largest Cosmos-native stablecoin as of now, native USDC (by Circle) coming to Cosmos in early 2023 could put serious pressure on all Cosmos-native stablecoins. The main drawback with USDC is its centralization and lack of censorship resistance; however, its reliable backing and impeccable track record are attractive for users going “risk-off.”

DEXs

Osmosis is the largest, most popular AMM on Cosmos. In addition to its first mover advantage as the first IBC-enabled DEX, it offers several unique features, including flexibility around the liquidity pool (i.e., market maker functions) and superfluid staking. While these network effects make Osmosis a stiff competitor, Comdex has a pathway to differentiation (e.g., native limit orders and synthetics).

While a broader analysis is out of scope, it’s worth noting that Comdex’s competition really extends to all Layer-1 blockchains with DeFi capabilities. Given the saturation, it’s fair to conclude that competition is quite stiff. Thus, Comdex will seek to differentiate itself through its focus on commodities and commodity trading.

Real-World Assets and Financing

For starters, commodities in crypto is an interesting choice. It brings the very tangible and physical to the abstract and virtual. This, however, may be a powerful strategy of accessing the commodities and trade financing markets can be very difficult, but it has plenty of potential to act as a hedge to high-beta cryptoassets.

As it turns out, there’s no need to speculate on feasibility and traction since synthetics have been around for some time. For example, Synthetix’s offerings have worked fairly well since launching in 2018, but the protocol has lagged behind in terms of user adoption, volumes, and revenues. This puts a question mark around how compelling synthetic assets actually are in crypto – or at least have been so far. That’s not to say that Comdex can’t outperform Synthetix, as Terra’s synthetics offering Mirror did back in 2021. However, projects like Cosmos-based DeFi Layer-1 Sei are also coming to fill the gap left by Mirror.

To truly differentiate itself within Cosmos and across all of crypto, the most promising avenue for Comdex appears to be connecting the commodity trade with DeFi primitives and capital. In particular, Comdex should seek to target SMEs in areas with underdeveloped financial infrastructure (i.e., South and Southeast Asia). Other DeFi firms (i.e., Goldfinch in the undercollateralized lending space) have found success with this strategy, and Comdex has already laid much of the groundwork with its Enterprise Trading Platform. Beyond trade financing (via ShipFi, Commodo, etc.) and settlement (via CMST), Comdex can continue to expand to other verticals such as futures (via cAssets). Onboarding even a small chunk of this $17 trillion market would make it one of the largest applications in DeFi.

Closing Remarks

Comdex is entering a saturated and competitive market, but it is doing so with a unique foundation. With strong execution, the protocol has a promising path to leverage its background and the open, democratizing ethos of DeFi to onboard the many underserved participants of the global commodity trade.