Key Insights

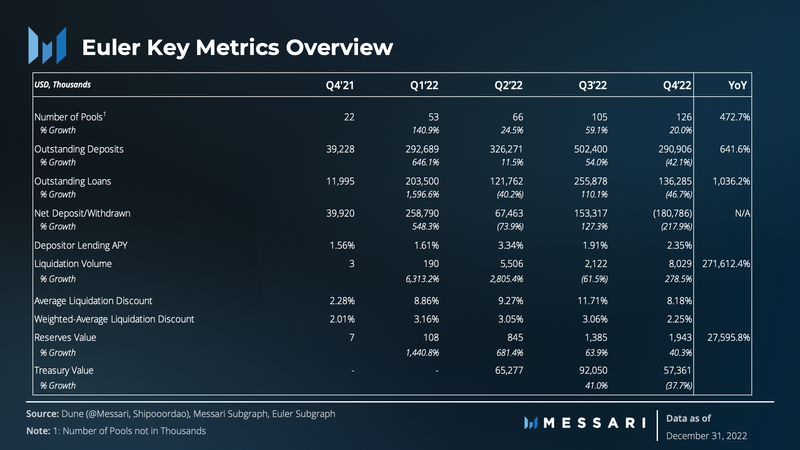

- Euler achieved impressive activity growth in its first year, even in the face of a tough bear market. It now supports 126 pools, 6,000 unique users, and over 10,000 transactions in Q4’22 alone.

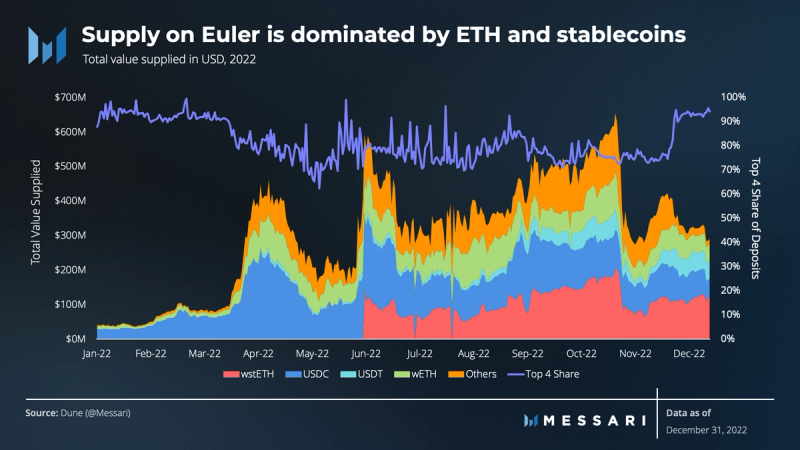

- The protocol ended the year with $290 million of deposits and $136 million of borrows. Despite the permissionless ability to add right-tail assets that have a Uni V3 TWAP oracle, more than 90% of supply is in stablecoins and ETH derivatives.

- Euler’s unique liquidation mechanism is significantly better for large borrowers compared to peers. The weighted-average discount on liquidations was 2.25% in the fourth quarter.

- Reserves increased 40% in each of the last two quarters of 2022, ending the year at $1.9 million. The treasury also benefited from diversification in June and sits at $57 million at year-end.

- The DAO passed eIP 18 ahead of the Merge, moving many assets to Chainlink oracles from Uni V3 TWAP oracle. Work is underway on Eulerswap, an Euler-native AMM, as part of a better price oracle solution.

Primer on Euler

Euler Finance (pronounced “Oiler”) is a permissionless lending protocol built on Ethereum, empowering users to lend and borrow ERC-20 tokens. Euler Finance is governed by EulerDAO, which uses EUL (ERC-20 token) to govern the protocol. Euler differentiates itself from other lending protocols in a number of ways, including permissionless token listing with a Uni V3 TWAP oracle, two-sided risk-adjusted borrowing capacities, improved liquidation efficiency through gradual Dutch auctions, and more. Euler introduces a risk framework for classifying assets into three tiers — isolation tier, cross tier, collateral tier — which dictate whether an asset can be used as collateral or as a lending and borrowing asset.

Key Metrics

Performance Analysis

Overview

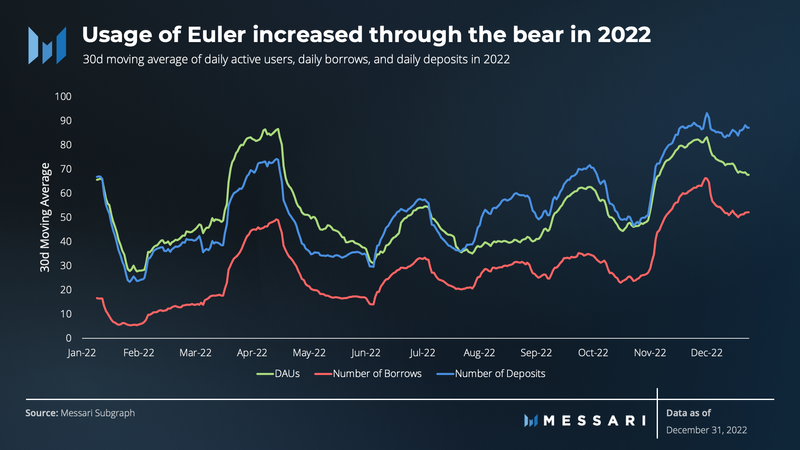

The 2022 bear market had little impact on Euler’s usage metrics. Pool count, average daily active users, unique users, daily number of borrows, and daily number of deposits all increased consistently over the year. The protocol went live on Ethereum Mainnet in December 2021. Although these metrics could be reflective of Euler only being live on Ethereum Mainnet since December 2021, they still show that Euler grew consistently over a tumultuous year.

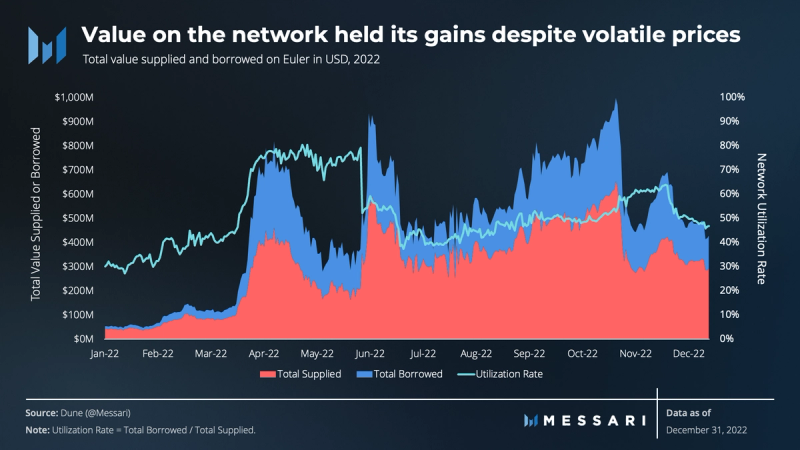

Euler was very successful in its first full year at attracting and retaining deposits and borrowing demand. Using value deposited in Compound, Aave, and Euler as a proxy, Euler launched in December 2021 and entered the year with 0.1% market share. In November 2022, it reached a peak of 6.8% share, closing the year at 4.3%. The acceleration in March and continued success were certainly due in part to the ongoing EUL rewards program which increases deposit yields on some pools and reduces borrowing costs on many. Euler’s network utilization rate was also higher than its peers for most of the year, likely reflecting delta-neutral borrowing to mine rewards.

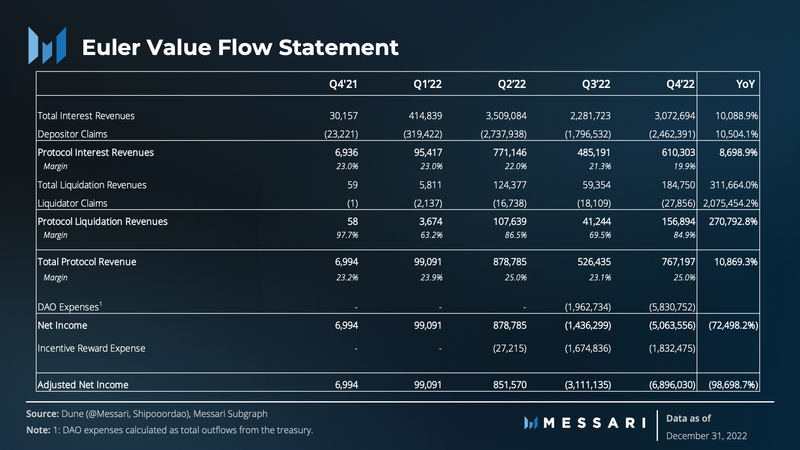

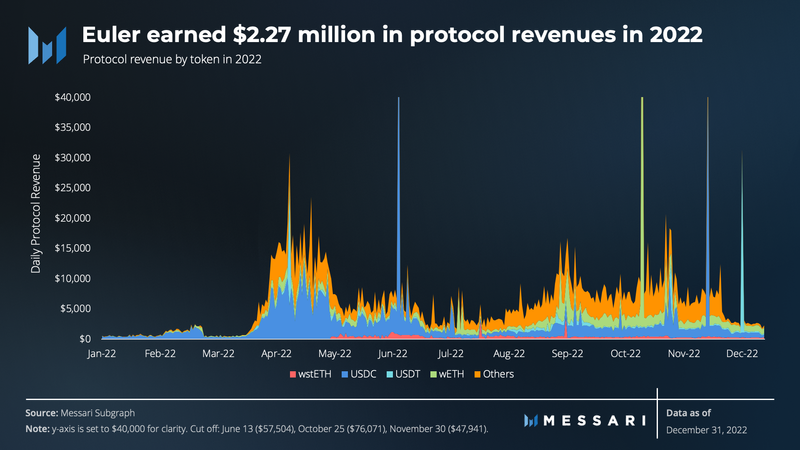

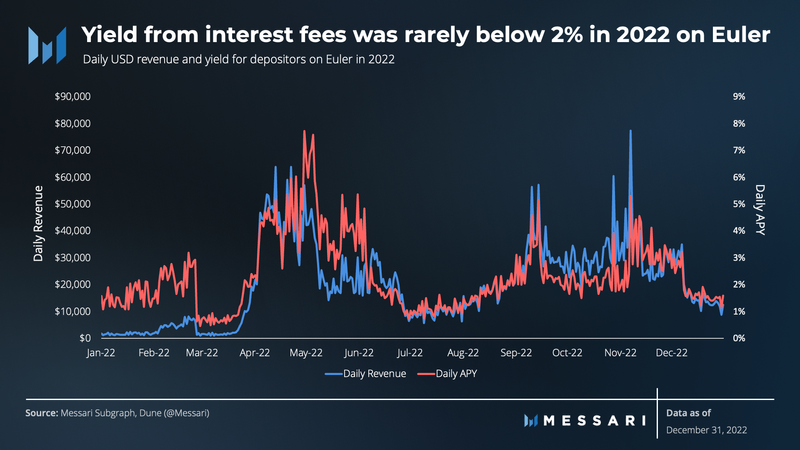

In the last nine months of 2022, Euler averaged $8,000 per day in protocol revenues (also serving as reserves). The protocol earns fees in the form of reserves from both a share of interest and payments and a share of liquidations. About 14% of reserves generated in 2022 were from liquidations, with the three largest earning days all having over $2 million of liquidations. Euler collects reserves from liquidations denominated in the borrowed asset, thereby creating a stronger buffer against future liquidations of borrows in that asset.

Borrower Perspective

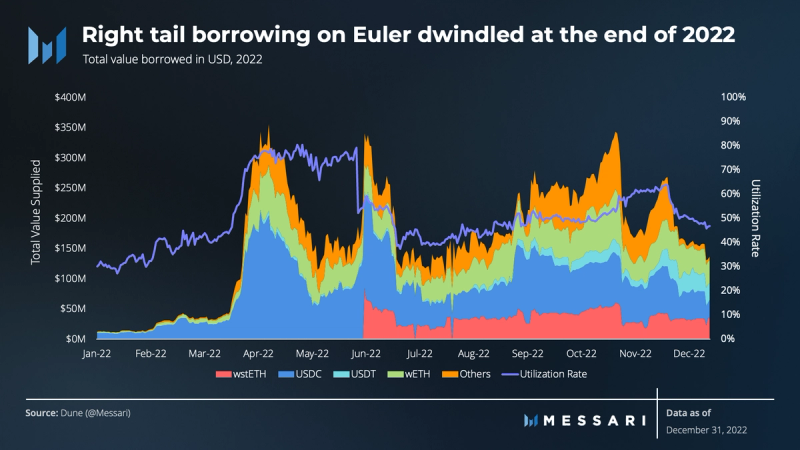

From the start of Q3 to the end of Q4, total value supplied on Euler was almost exactly flat at $290 million. But the end-of-period numbers hide the drama in between, which included over $350 million of withdrawals from Euler’s wETH and wstETH pools during the FTX collapse. The protocol ended November 5 with around $315 million in deposits in those two pools, indicating a complete turnover of deposits in just three days. On November 9, the two pools had $110 million in remaining deposits.

In November, EulerDAO voted to update EUL distribution to reduce incentives and widen distribution. The change included fixed rewards for USDC, UDST, and wETH depositors as well as USDC, USDT, wETH, and wstETH borrowers. Despite its solutions for the right tail of assets, value on Euler was dominated by ETH and stablecoins, ending the year at more than 90% deposit share.

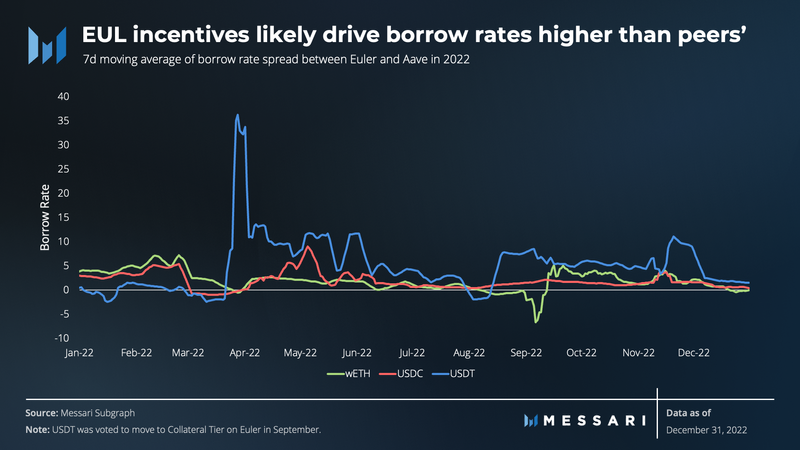

Euler has gauges where tokenholders can vote to allocate EUL rewards to borrowers of various assets. These rewards reduce the borrowing cost on loans, leading the natural interest rate (which ignores the reward from incentives) to trade a positive spread to peers (using Aave as an example).

Perhaps because of the smaller asset base, borrowers on Euler need to worry more about large changes in their borrow rate. Compared to Aave, the standard deviation of borrow rates across wETH, USDC, and USDT was high on Euler in Q4. The higher rate does impact this metric, but even as a percent of the average rate in the quarter, Euler rates showed more volatility. USDC standard deviation as a percentage of the average rate was 38% (1.34 stdev) on Euler in Q4 versus 13% (0.28 stdev) on Aave. Higher borrow rate volatility makes it more difficult for users to plan or execute levered investment strategies.

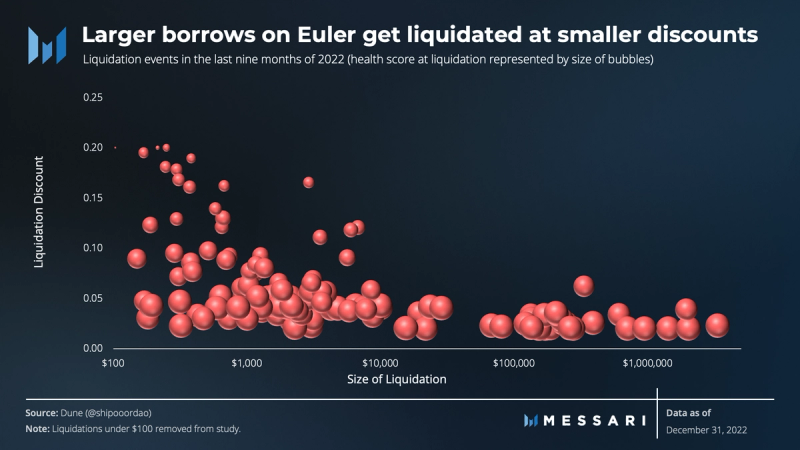

Liquidations on Euler utilize a unique mechanism. They create a gradual Dutch auction for liquidators to bid for collateral assets instead of simply giving them at a fixed discount to the fastest or highest gas-paying liquidator. The liquidation discount is capped at 20%.

This approach results in cheaper liquidations for larger borrowers. In the last nine months of 2022, liquidations over $10,000 were executed at an average discount rate of 2.77%, while liquidations smaller than $10,000 but over $100 were liquidated at a 7.54% average discount. The protocol charges the liquidator a 2% liquidation surcharge, which is included in the discount rate, or amount returned to the borrower who is being liquidated.

Euler liquidators are accepting a mere 0.77% return on large liquidations. Given many protocols are charging closer to 5% for all liquidations, the auction-based metric gives a first look at market-based liquidation pricing at different loan sizes.

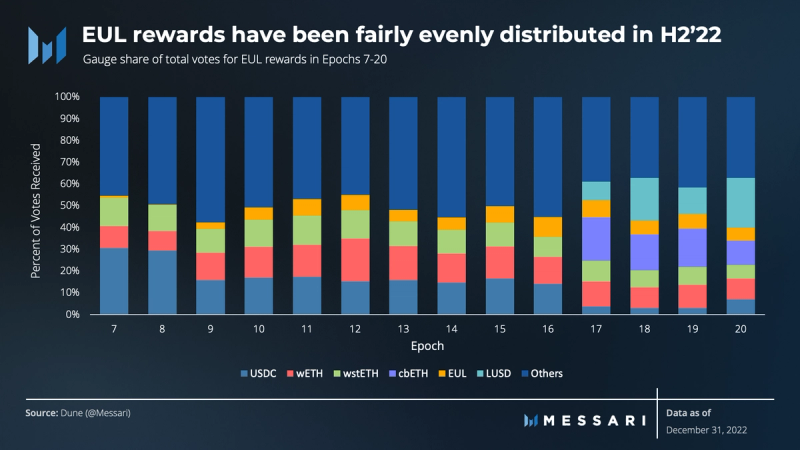

No tokens received more than 25% of the EUL rewards vote since Epoch 8, which ended on July 5. Each epoch is roughly 15 days, during which EUL holders can vote to allocate rewards. The share of votes going to USDC, USDT, wETH, and wstETH fell from 60% in Epoch 8 to only 24% in Epoch 20 as more gauges were listed. eIP 24 also created dedicated rewards for the Big Four assets (USDC, USDT, wETH, and wstETH), empowering voters to send rewards to other pools.

Lender Perspective

Euler saw rapid adoption in its first full year, with total borrowing growing from $12 million at the end of 2021 to $136 million at the end of 2022. On September 30, 30% of the borrow value ($75 million) on Euler came from outside of the Big Four. As the market turned further risk-off in Q4, borrowing demand in those assets contracted more than in centralized stablecoins and ETH-related tokens, both of which ended the year with 96% of borrow value on Euler.

Some notable Q4 shifts had several metrics experience significant drops:

- DAI supply ($81 million to $5 million) and DAI borrow demand ($47 million to $1.7 million).

- FTT supply ($10 million to $0) and borrowing ($5 million to $0)

- LDO supply ($8 million to $1.4 million) and LDO borrowing ($3.2 million to $500,000).

- wBTC supply ($41 million to $5.6 million) and wBTC borrowing ($22 million to $1.9 million).

Yield for lenders peaked in Q2 of 2022, potentially driven by demand stemming from the ability to short tokens on the platform. The borrow side is rewarded with EUL tokens on Euler, pushing demand and therefore depositor APYs up, which were generally higher than peers. Lending yields also spiked in September around The Merge, both for shorts and as a way to play an ETH POW fork.

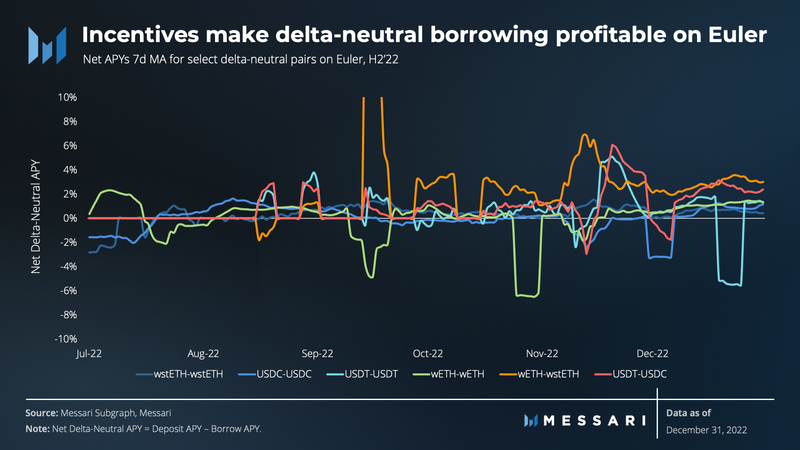

Euler offers EUL holders the opportunity to vote in gauges to direct EUL rewards to borrowers of assets on Euler. On November 13, the rewards distribution was updated to include 5,000 EUL to lenders of USDC, USDT, and wETH per epoch, along with 8,000 EUL to borrowers of USDC, USDT, wETH, and wstETH, and another 8,000 EUL to be allocated by gauge voters for a six-epoch trial.

The rewards bring down borrowing costs and increase lending returns. Depending on the interest rate, users could potentially farm rewards without taking any (or small) price risk. For example, for most of Q4, users could deposit $1 of USDT and borrow $0.80 USDC and earn nearly 2%. Given the leverage on this position, that is a 10% yield on stablecoins with cushion for small price volatility.

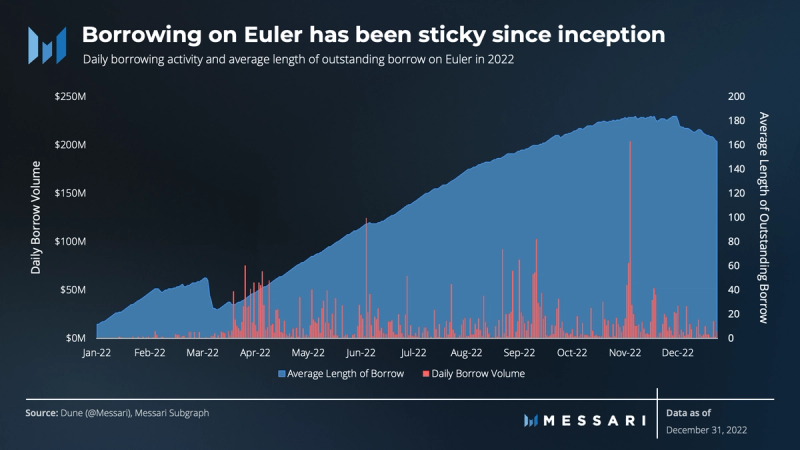

The average length of borrows on Euler increased throughout the year. Having long-term borrowers is a good indication for depositors as it means yields should be more reliable. Over $715 million of borrows were initiated on Euler in 2022, with Q3 being the most active quarter at nearly $256 million of borrows initiated.

Qualitative Analysis

Decentralized, Manipulation-Resistant Oracles and Eulerswap

On September 5, Michael Bentley, founder of Euler, posted eIP 18: Move all asset price oracles to Chainlink where available ahead of the Merge.

Euler enables the permissionless creation of lending markets for tokens with a Uniswap V3 wETH liquidity pool; all that is required is a Uni V3 TWAP oracle. Much of the reason for using the Uni V3 TWAP oracle is the resilience to manipulation that it provided, as Michael’s own research shows. Essentially, arbitrage and maximal extractable value (MEV) create an expensive uncertainty for manipulators who want to move the price on one block and profit from it on the next.

However, the move to Proof-of-Stake (PoS) on Ethereum changed the game for TWAP oracle manipulation. Post-Merge, the block builder is known before the block is created. With Proof-of-Work (PoW), the block was won by the miner who solved the hash function the fastest. With PoS, validators can now know when they will be the block builder ahead of time, reducing the uncertainty and cost of manipulating a price in block n-1 and then profiting from it in block n. Further, the likelihood of being the validator for two consecutive blocks is higher because of stake weighting.

Euler still uses Uniswap V3 TWAP oracles to allow the permissionless creation of lending pools. However, there is now a typical change by EulerDAO from the TWAP oracle to Chainlink after a lending pool grows or moves to a higher tier on Euler. This process has become so common that beginning in Q1, it will be handled in a monthly meeting to avoid spamming the forum.

Spot price oracles have other risk factors including price spikes and flash loan manipulations. Using Chainlink also creates a new vector for risk/manipulation. In his post, Michael referred to the Chainlink solution as a short-term fix.

In the medium- and longer-term, Euler is working on Eulerswap (final name TBD). In June, the Ethereum Foundation released research on using a median-price oracle as a solution to potential TWAP manipulations. Early indications from the core team at Euler show this implementation is likely to be used on Eulerswap. The Euler team plans to release its whitepaper and more details in the first half of 2023.

LSD Lending and Borrowing

With the expected release of the Ethereum Shanghai upgrade in Q1’23, liquid staking derivatives (LSDs) have come to the forefront as a critical asset. There are currently three main players in the space: Lido with stETH, Coinbase with cbETH, and Rocket Pool with rETH.

The largest collateral asset on both Euler and Aave is currently Lido’s stETH (a wrapped version). However, Euler is the only protocol to allow users to borrow the LSD. At the end of 2022, it was the second largest asset by USD value borrowed, behind only wETH.

On November 17, the EulerDAO voted to move cbETH to the Collateral Tier. From December 6, the value of cbETH deposited on Euler grew from $142,000 to over $36 million as of January 21, 2023. In the same time frame, borrows went from zero to over $6 million.

The DAO is currently voting on whether to promote rETH to the Collateral Tier as well. Rocket Pool is in the process of getting a Chainlink oracle set up to meet the last requirement for safe listing on Euler. The DAO plans to be conservative at first, as rETH has a worse liquidity profile than other LSDs, though it is growing fast.

Supply and Borrow Caps

EulerDAO has consistently operated with a risk-first perspective to lending. This commitment can be seen in the dual-sided adjusted risk factors that take both the collateral risk and the loan asset risk into account, as well as the risk tiering system.

In December, Euler’s founder raised a new idea for discussion around implementing supply and borrow caps on Euler. Likely due to the CRV manipulation on Aave in 2022, lending protocol DAOs are realizing the importance of available liquidity to inform their risk systems. At the same time, they are having to consider the difficulty of manually managing these risks on all assets or opting for a service provider. Instead, EulerDAO is ideating on automated solutions.

The leading suggestion at the moment is from Tyler Loewen, who uses the framework of “How many liquidations can the market absorb before bad debt is accumulated?” His solution has two implications:

- A velocity solution that limits the speed with which risks could build up on Euler, giving the DAO time to be proactive.

- A liquidity-informed hard cap that limits the deposit capacity on the protocol.

The second solution uses a liquidity oracle to inform a risk parameter of how much outstanding liquidity there is on DEXs (although some oracles could measure liquidity elsewhere as well).

Tyler’s solution would do well to limit a situation where there is more of an asset available to borrow on Euler than there is to transact on exchanges. However, it may be a bit naive in ignoring a reflexive relationship between liquidations and available liquidity that should inform a multiple of the available liquidity to the amount available to borrow. For example, if there is $100 of liquidity, and liquidations begin, will there be 1x amount available to liquidate? Or 3x? How about 0.6x? The discussion is still in the idea stage, with more research yet to be done.

Efficiency Mode (e-Mode)

Introduced by Aave’s V3, efficiency mode for lending protocols empowers DAOs to specify loan-to-value (LTV) ratios for specific asset pairs. Typically, on lending protocols, assets receive a collateral factor which determines how much users can borrow against them. Using e-mode, DAOs can specify that certain pairs can have greater leverage than allowed by the typical collateral ratio.

The original request for comment on EulerDAO is to enable e-mode for USDC/USDT and wETH/wstETH pairs. These are liquid, highly correlated pairs of assets that should have a lower risk profile when used as collateral to borrow from one another. The proposal is still more conservative than the current e-mode implementation on Aave for these pairs, but it enables borrowers on Euler to get more efficient borrowing on these liquid and correlated pairs.

There certainly is increased risk when you allow higher LTV ratios. If something goes awry with Tether or Circle, it would be more painful for the protocol and borrowers than without e-mode. The probabilities likely favor taking the risk, given the increased usage it would enable for lenders and borrowers.

Closing Summary

Euler’s first full year came in a very tough market for crypto and DeFi, but the protocol emerged as a key player in the space. Activity on Euler grew through the year, partially aided by incentives but also by the innovations in risk tiering and cheaper liquidations for large borrowers. Despite the protocol’s unique ability to support right-tail assets, most of the value on Euler is in stablecoins or ETH derivatives. With a diversified treasury and growing user protection in the form of reserves, Euler has a solid foundation to continue to fund research and innovation, with the release of Eulerswap in H1’23 first on the roadmap.