Key Insights

- stETH deposits accounted for 36% of the value supplied on Ethereum V2 in Q4, driven by stETH rewards outpacing ETH borrow rates.

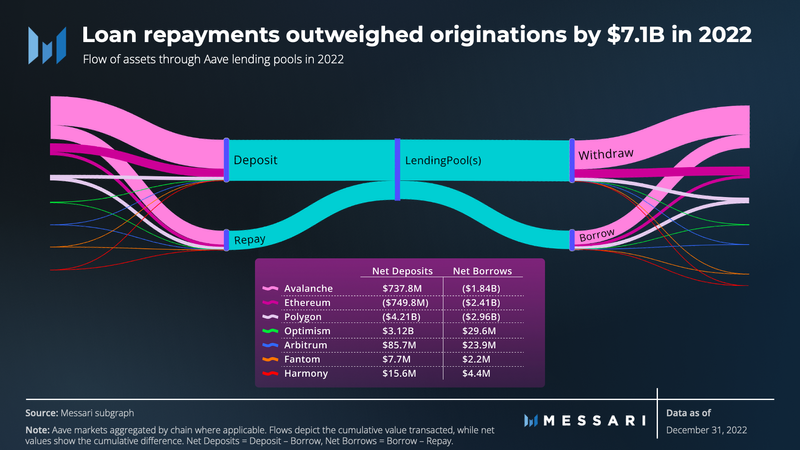

- In 2022, loan repayments outweighed originations by $7.1 billion, and withdrawals exceeded deposits by $1.0 billion.

- Users claimed $68 million worth of AAVE (3.5% of total supply) in rewards and incentives, with 76% of the value and 62% of the tokens claimed in H1 2022.

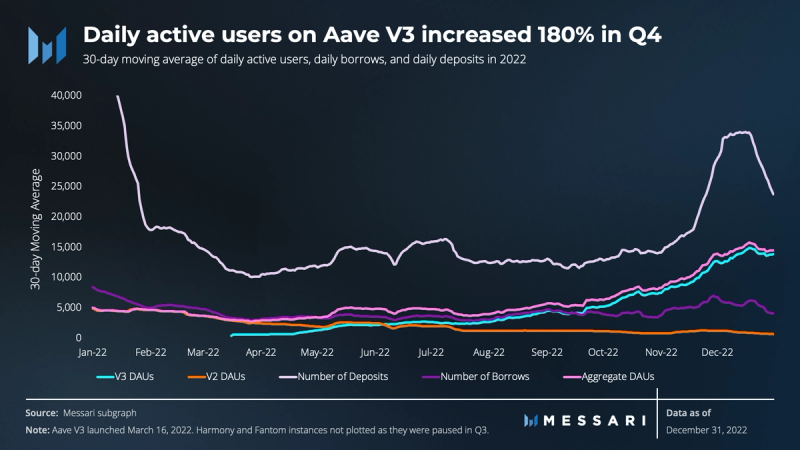

- Daily active users increased 180% on Aave V3, QoQ. Continued growth is expected as V3 was recently deployed to Ethereum, the protocol’s first and largest market.

- Token swap with Balancer makes Aave DAO the 17th largest holder of BAL. The strategic partnership with Balancer was further solidified through the staked aToken primitive.

Primer on Aave

Aave is a decentralized money market protocol that facilitates the depositing and borrowing of various crypto assets. The protocol has two main versions (Aave V2 and V3) and is deployed across various Layer-1 (L1) chains and Layer-2 (L2) networks, with the majority of activity on Ethereum. Aside from the core permissionless lending business, the protocol has introduced various complementary products such as a stablecoin (GHO), an open social protocol (Lens Protocol), and a permissioned instance of the core Aave protocol (Aave Arc).

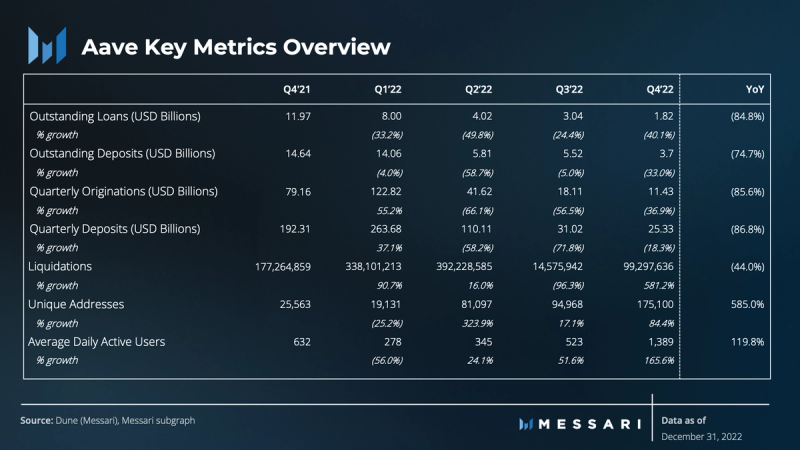

Key Metrics

Performance Analysis

Asset Flows

In 2022, withdrawals on Aave exceeded deposits by $1.0 billion, and loan repayments outweighed originations by $7.1 billion, as prices dropped and the system deleveraged. A significant portion of transactions, accounting for 71% of the total value, occurred on the Avalanche network, fueled by incentives disbursed by Ava Labs. Incentives such as these often push net borrowing costs lower than the interest paid to depositors, which enables users to improve returns with minimal risk by re-collateralizing borrowed funds.

This trend was also seen on Optimism, which launched its liquidity mining campaign in August and ended in November. In the first three days of the campaign, outstanding loans skyrocketed from $5 million to $1.4 billion, but declined 90% in the four days prior to the end of the campaign, dropping from $914 million to $90 million. These incentives, funded by the deployments base layer, not only helped generate revenue for Aave’s treasury, but also reinforced Aave’s market-leading rank as the primary beneficiary of such initiatives.

Daily Usage

While asset flows in 2022 were sub-optimal, the financial woes only tell part of the story. Daily active users (DAUs) gradually increased since the March 2022 release of Aave V3, ultimately resulting in a 180% DAU growth in Q4. Among the V3 instances, Optimism and Polygon DAUs experienced the highest increase, with growth rates of 274% and 209%, respectively. Usage on Arbitrum and Avalanche also experienced substantial growth, with increases of 113% and 46%, respectively. Despite a lack of incentives seen in previous quarters, the fact that DAUs increased across all deployments characterized organic growth; this is a testament to the protocol’s resilience amidst the challenging market conditions of 2022.

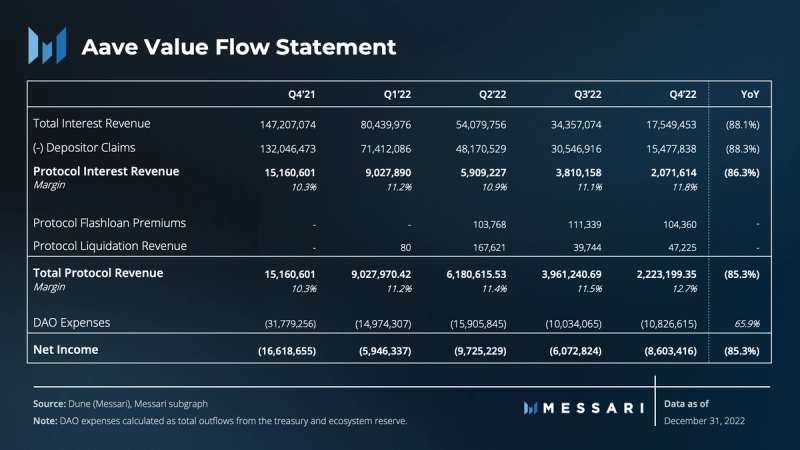

Revenue

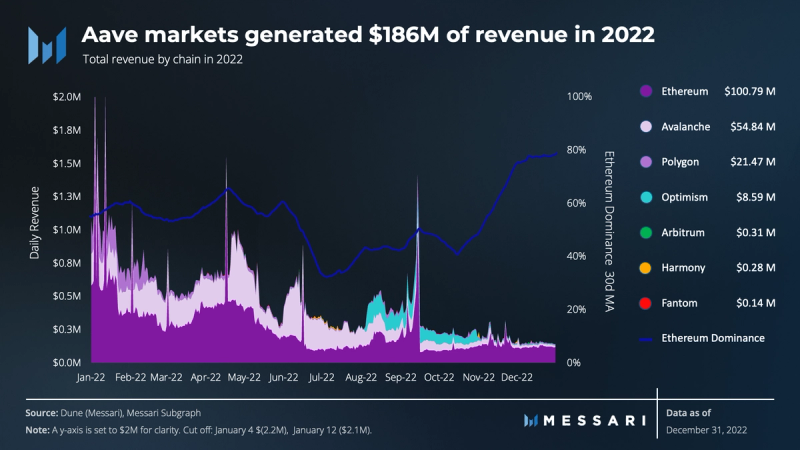

In 2022, Aave generated $186 million in revenue, with $21 million retained for the community treasury. The majority of the value, 56%, was captured on Ethereum. On a quarterly basis, the Ethereum share of revenue was largest in Q4 at 65% dominance, a significant increase from its low of 46% in Q3. This low was driven by incentivized usage on Avalanche and Optimism, which maintained stablecoin utilization rates above 65%. Simultaneously, revenues from Ethereum bottomed following a massive deleveraging in Q2 that stemmed from the collapse of centralized lenders. As incentives tapered off, loans were repaid on the respective chains and Ethereum’s share of revenue continued to grow. By December, Ethereum’s dominance grew to 78%, even higher than before V3 launched, as revenues on Ethereum remained stable and other chains continued to bleed. Despite the higher gas fees, Ethereum has proven to be the home base for Aave users and is expected to remain the primary source of revenue for Aave.

Rewards and Incentives

In 2022, users claimed 555,963 AAVE ($68 million at the time of claim), or 3.5% of the total supply from the ecosystem reserve. Notably, only 24% of the USD value and 38% of the tokens were claimed in H2 2022.

193,370 AAVE were disbursed as part of a liquidity incentive program that ended in May 2022. The Safety Module, separate from the incentive program, acts as a user-funded insurance fund for the protocol. If protocol insolvency occurs, 30% of the funds can be slashed to cover the debt. As a reward, stakers in the Safety Module proportionally received a share of AAVE tokens, with 362,593 AAVE distributed in 2022. The amount of staked AAVE in the Safety Module decreased 19% over the year to 2.4 million tokens. Despite this decrease, the insurance power of the funds increased from 2.6% to 3.2% of the outstanding loan balance.

Stablecoins

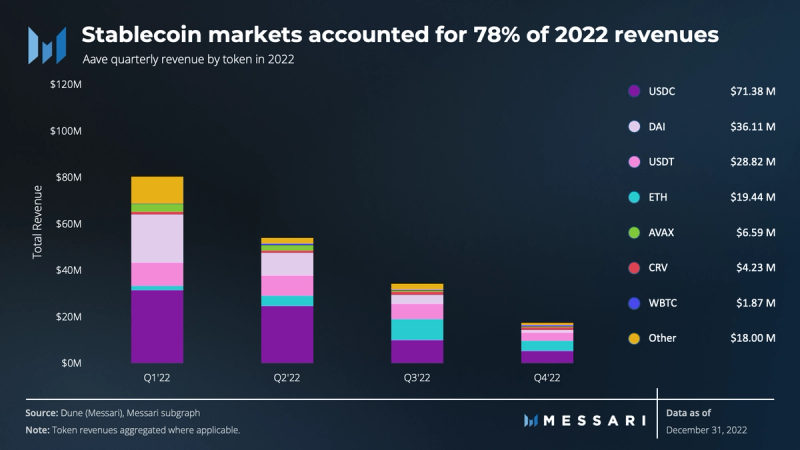

Stablecoin markets generated $145 million in 2022, accounting for 78% of the revenues. However, the share of revenues derived from stablecoins dropped throughout the year, from 86% in Q1 to 60% in Q4 as demand for USD-denominated debt contracted with falling prices. The difference was almost entirely made up by increased revenue share from ETH, which climbed from 2% in Q1 to 24% in Q4 as the leveraged stETH-ETH strategy gained traction throughout the year.

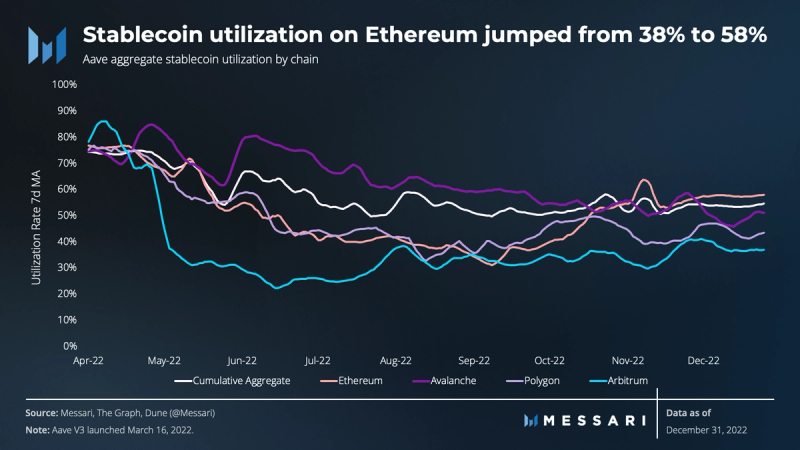

Stablecoin utilization remained relatively flat in Q4. Ethereum V2, an exception, increased from 38%-58%. This increase was primarily driven by two factors: first, traders seeking to short USDT in the wake of the FTX collapse, given that FTX and Alameda were significant market makers for the stablecoin. The USDT utilization rate briefly peaked at 94% on November 9, before leveling off to 72% by the end of the year. Second, a single trader’s decision to collateralize $64 million of USDC in an attempt to short CRV also contributed to the increased stablecoin utilization on Ethereum.

In terms of borrowing, V3 on Arbitrum offered the most favorable stablecoin rates in Q4, with an average utilization of 36%. On a monthly basis, however, Optimism experienced the lowest rates in November and December, as users unwinded recursive liquidity mining positions without withdrawing their deposits. The utilization rate on Optimism dropped from 69% in October to an average of 23% in November and December.

stETH-ETH Analysis

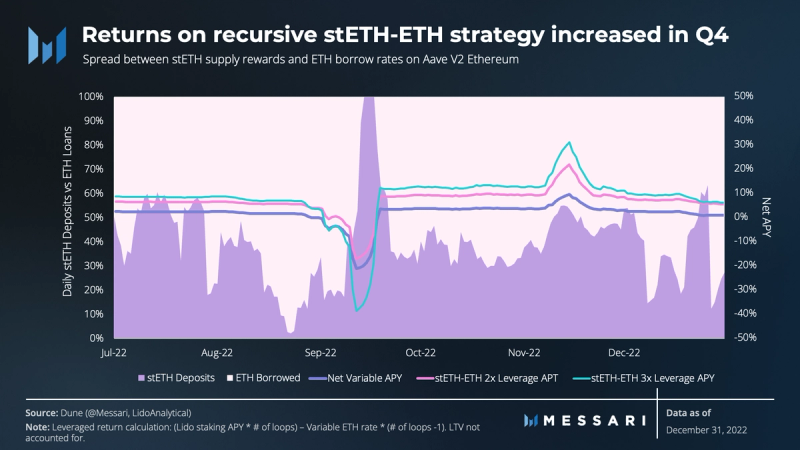

The transition to proof-of-stake (PoS) on Ethereum led to the emergence of liquid staking derivatives (LSDs), allowing investors to earn validator rewards without directly running a node or locking Ether. Lido Finance’s Staked Ethereum (stETH), backed 1:1 with ETH staked on the Beacon Chain, accrues rewards daily through rebasing. stETH has become the most popular choice of collateral on Aave V2 Ethereum because its rewards rates are often higher than the ETH borrow rates. This effectively led to stETH being viewed as self-repaying collateral, amassing a 36% share of the value supplied on Ethereum.

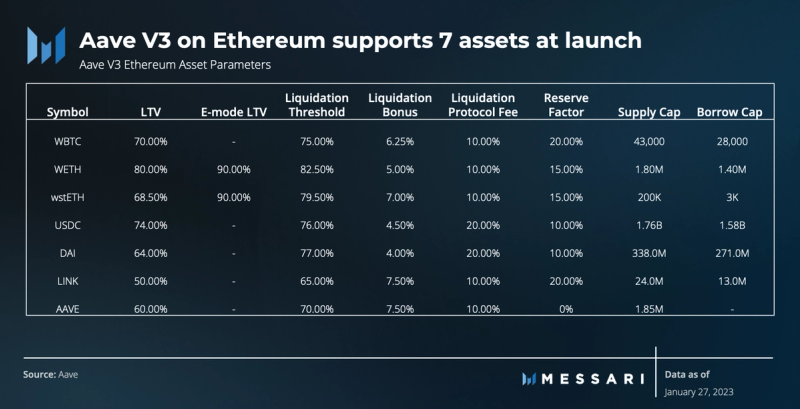

In Q4 2022, investors who collateralized stETH and borrowed ETH achieved a net variable APY of 3.1%, excluding LTV assumptions. By doing this recursively, yields improved, with an average APY of 9% for one “loop” and 12% for two. The launch of Aave V3 on Ethereum further optimized this strategy through the Efficiency Mode (E-mode) feature. This enables higher loan-to-value and liquidation thresholds for borrowers who use similar assets as collateral. Through E-mode, the LTV for stETH collateral increased from 72% on V2 to 90% on V3. Notably, V3 migrates stETH to Lido’s wstETH, which is an upgrade that bakes the staking rewards into price instead of rebasing.

This recursive strategy, although a significant contributor to Aave’s revenue in 2022, carries risk. In V2, stETH’s price parity with ETH and depth of available liquidity are crucial to prevent cascading liquidations and potential insolvencies. V3 reduces this risk through the implementation of supply / borrow caps and additional risk parameters. The initial supply and borrow caps for wstETH were set at 200,000 and 3,000 wstETH, respectively.

Treasury

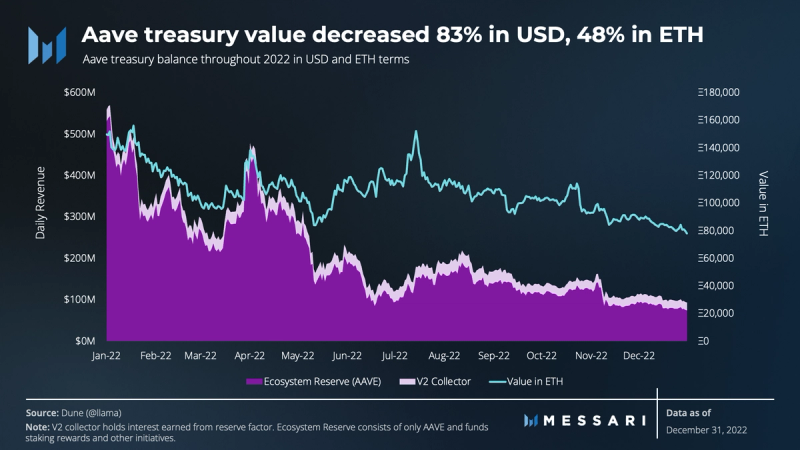

Aave’s treasury consists of a V2 collector contract, which holds the protocol’s share of interest payments, and an ecosystem reserve, which solely holds AAVE tokens and is used for staking rewards and other initiatives such as grants, incentives, and partnerships. In 2022, the treasury value fell 48% in ETH terms and 83% in USD terms, from $559 million to $93 million. $457 million of the loss in value came from the ecosystem reserve, which distributed 29% of the tokens (590,113 AAVE), combined with falling prices.

As interest revenue accrues and staking rewards are disbursed, the treasury composition becomes more diverse. At the beginning of the year, the treasury composition consisted of 95% AAVE and 5% various tokens. By the end of the year, the treasury comprised 75% AAVE with a notable 646% increase in ETH.

The treasury also made a significant acquisition of 300,000 BAL tokens, cementing its place as one of the largest holders of BAL. The longstanding partnership between Aave and Balancer was solidified with the launch of the Staked aTokens Primitive, allowing Balancer liquidity providers to use LP tokens as collateral. This mutually beneficial partnership provides composability for Balancer liquidity providers while boosting the total value locked (TVL) on Aave. Moreover, the newly acquired BAL tokens are expected to play a critical role in GHO, Aave’s overcollateralized stablecoin. By directing BAL incentives to aToken pools, Aave will be able to bootstrap liquidity for GHO without exhausting treasury reserves.

Qualitative Analysis

All Systems GHO for Aave V3 on Ethereum

Over the holiday season, anticipation remained high for the launch of V3 on Ethereum, the protocol’s first and largest market. Following in-depth discussions, the community voted in favor of a conservative, guarded launch proposed by community partner Chaos Labs, which supports seven assets: WBTC, WETH, wsETH, USDC, DAI, LINK, and AAVE.

A less-publicized, but still high-impact, feature of V3 on Ethereum is the implementation of a liquidation protocol fee. In V2, users are incentivized to liquidate underwater positions in return for a portion of the collateral known as a liquidation bonus. Whereas in V3, a share of the liquidation bonus is diverted to the protocol reserves, generally between 10-20%.

The V3 deployment on Ethereum also set the stage for the launch of GHO and will serve as the stablecoin’s first facilitator. Unlike other stablecoin debt, GHO will allow Aave to retain all interest revenue, as it will not need to split it with depositors. With 78% ($145 million) of Aave’s interest revenue in 2022 generated from stablecoins, the launch of GHO is expected to significantly boost the company’s bottom line, even if it only captures a fraction of the demand. Additionally, Lens Protocol, a decentralized social protocol and complementary business line developed by Aave, has seen significant growth in usage and recently passed 100,000 profiles minted. On top of allowing developers to create social applications with unique monetization models, Lens aims to further increase the efficiency of the Aave ecosystem by bridging the gap between overcollateralized and undercollateralized lending through trusted reputation and identity systems. GHO is expected to serve as the main currency on Lens, fueling organic demand and providing Aave with a means to offer loans against future cash flows.

Treasury Repays Excess CRV Debt

In November, an attempted short of CRV led to the protocol incurring $1.7 million of bad debt. The saga began when a trader deposited $39 million USDC into Aave to borrow CRV, which they would then sell back to USDC in an attempt to short it. They began to short CRV for a week, driving the price of CRV down from $0.625 to $0.464. On November 22, the trader ramped up efforts by borrowing and dumping 55 million CRV, worth ~$34 million, causing the price to drop further. This posed a threat to Aave borrowers using CRV as collateral as they moved closer to crossing the liquidation threshold. One of the users collateralizing CRV was the founder of Curve Finance, and speculation suggests the short was aimed at liquidating his position. To avoid this scenario, he deposited an additional 20 million CRV tokens.

The trader’s actions ultimately resulted in a short squeeze of the CRV price, causing his position to be liquidated with the assistance of CRV liquidity injected by the Curve founder. However, the injection wasn’t enough, and due to the lack of CRV liquidity, the position was closed over the course of an hour through 385 individual mini-liquidation transactions. This left Aave with 2.7 million CRV, roughly $1.7 million at the time, in bad debt. This incident highlights the importance of adequate liquidity in the market, as it can significantly impact the protocol’s ability to handle liquidation events and potentially result in financial losses. As previously mentioned, V3 reduces this risk with the implementation of supply and borrow caps.

In January, the DAO voted in favor of repaying the excess CRV debt with aUSDC from the treasury, of which $280,000 was subsidized by Gauntlet’s insolvency fund. This path, chosen over utilizing the Safety Module, highlights a commitment to protecting investor funds. As of February 2, bad debt on Ethereum V2 stands at $400,000 (0.01% of TVL) according to the Risk DAO dashboard.

Governance

Partnerships

The DAO executed three partnership proposals in Q4. The first proposal extended the partnership with Llama for twelve months relating to treasury management and analytics services, with an approved budget of $1.5 million paid in 70% USDC and 30% Aave. The second proposal approved a twelve-month partnership, with a $500,000 budget, for Chaos Labs to build out risk simulation tools to help optimize and protect Aave V3 markets. As a show of commitment, Chaos Labs delayed payment streams to begin six months following the execution of the proposal. The final proposal renewed the partnership with Gauntlet for continued risk management, including interest rate parameter recommendations. The $2 million fee covers twelve months of services and includes a $600,000 insolvency fund, refundable to the DAO in the event Gauntlet’s parameter optimizations incur insolvencies during the engagement.

Level 2 Governance Requirements Updated

In October, the Dao voted to update the governance Level 2 requirements, which control any changes that could directly affect the dynamics of the voting power or the logic of the voting itself. This includes changes such as the upgradeability of the AAVE / stkAAVE tokens, the permissions on the Governance V2 smart contract itself, and the upgradeability of the AAVE/ETH Balancer ABPT and stkABPT. BDG Labs’ justification for the proposal indicated the voting participation requirements in place were too strict, potentially blocking progress and community contribution. Additionally, BDG Labs found that a minimum of 36% of the AAVE supply was unable to vote in governance decisions due to being held in contracts that do not have the functionality to cast votes, such as AAVE deposited into lending pools (aAAVE) and the AAVE / ETH Balancer pool.

The implementation of the proposal required innovation in itself as it still had to pass the current Level 2 requirement of 3.2 million (20% of total supply) votes in order to change them. At the time, the ecosystem reserve held 1.7 million AAVE, and because it does not affect the dynamics of voting, it is controlled by the governance on Level 1. Therefore, a path forward was realized by executing the following chain of events:

- A Level 2 proposal was created to change Level 2 parameters.

- A Level 1 proposal (voting boost) was executed to upgrade the AAVE ecosystem reserve, allowing for a one-time vote on the previous Level 2 proposal.

- The ecosystem reserve contributed 1.5 million YES votes to the Level 2 proposal.

- The rest of the Aave community pulled together 1.7 million YES votes.

- The vote passed with 100% approval and reached the quorum requirement with 3,208,113 votes, meaning 0.25% of the votes made all the difference needed.

Upon execution of the Level 2 proposal, the quorum for the Level 2 Executor changed from 20%-6.5% (1.04 million AAVE), the vote differential changed from 15%-6.5%, proposition power required for Level 2 proposal changed from 2%-1.25%, and a delay of 7,200 blocks (~1 day) was added between proposal creation and vote start.

Closing Summary

Despite the challenging economic conditions of 2022 that contributed to declining yields and a reduction in demand for leverage, the Aave community persevered and successfully delivered an upgraded version of the protocol. This expanded Aave’s reach from four chains to seven, resulting in a significant increase in DAUs. The emergence of liquid staking derivatives was a major contributor to protocol revenues and proved to be a seemingly superior collateral asset. This, combined with the recent launch of V3 on Ethereum and the highly anticipated launch of the GHO stablecoin, positions the Aave ecosystem for an exciting 2023.