Key Insights

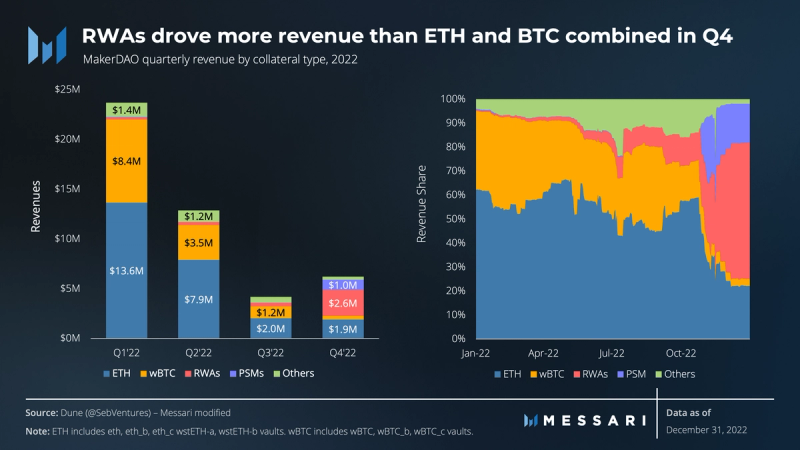

- MakerDAO took big strides in transitioning the protocol to a real world asset (RWA) lender, becoming the largest decentralized off-chain lender in Q4 with over $600 million in loans. Revenue from RWA loans accounted for 57% of daily expected revenues at year-end.

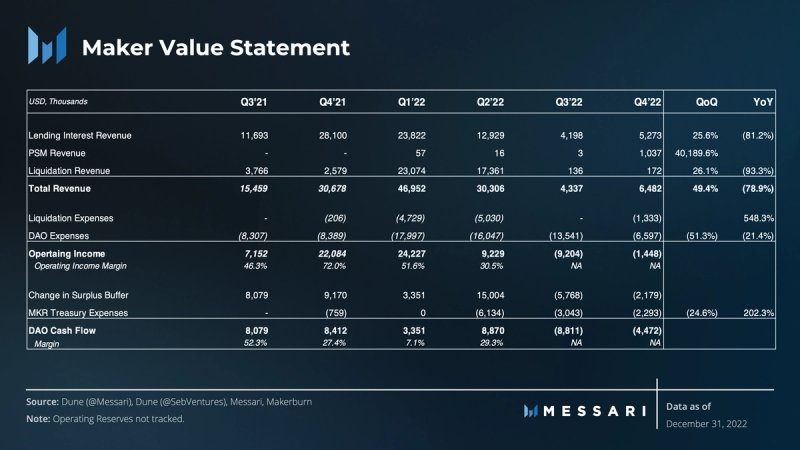

- The increase in revenue from RWA loans and DAO spending cuts of nearly 50% quarter-over-quarter (QoQ) brought MakerDAO close to profitability, shrinking the quarterly loss to $1.4 million.

- DAI outstanding fell 21% to 5 billion, while the total value deposited in the protocol fell 13% to just under $7 billion. Volumes also fell 60% in the quarter as centralized stablecoins gain share and DAI is repurposed to a savings vehicle.

- The DAO increased the DAI Savings Rate to 1% in December, the first meaningful increase since 2020, on the back of RWA and peg stability module (PSM) yield opportunities.

Primer on Maker

Maker is a peer-to-contract lending platform that enables overcollateralized loans by locking collateral in a smart contract and minting DAI, a stablecoin pegged to the U.S. dollar. MakerDAO determines which collateral types are accepted as well as their collateralization ratios and stability fees. Maker maintains DAI’s stability through a dynamic system of collateralized debt positions, autonomous feedback mechanisms, and incentives for external actors. DAI also uses Peg Stability Modules that allow for 1:1 swap of DAI with three approved stablecoins: USDC, USDP, and GUSD. Once generated, DAI can be freely sent to others, used as payments for goods and services, or held as long-term savings.

Key Metrics

Performance Analysis

Maker Protocol

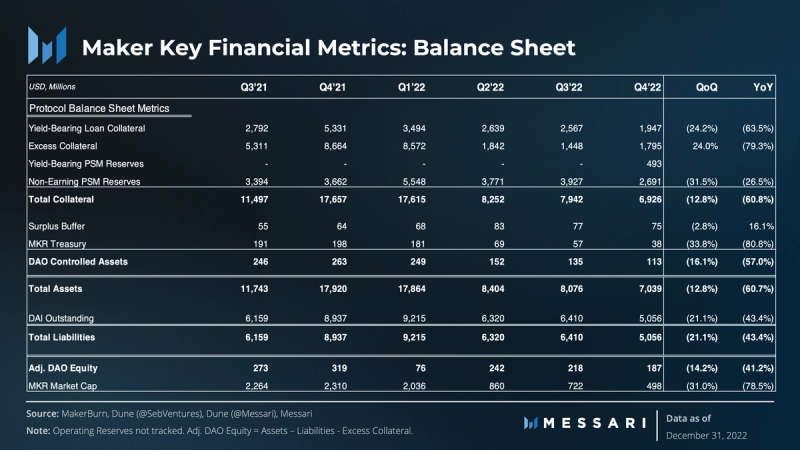

Maker’s collateral ratio improved in Q4, as total DAI outstanding fell faster than total collateral, ending the year at 1.37. Removing non-earnings PSM reserves ($2.7 billion), the collateral ratio rises to a healthy 1.79. The roll-out and execution of MakerDAO’s RWA and PSM investment strategy are demonstrated through the change in the asset mix. Non-earning PSM reserves were down 31.6% QoQ. Roughly half of this $1.2 billion reduction in the PSM is attributable to the $500 million launch of the new RWA, RWA007, which loans DAI to the borrower that is then swapped for USDC from the PSM to move the dollars off-chain (see visual in Qualitative Analysis section). Yield-bearing PSM reserves are also a new line item that represents a large growth opportunity for MakerDAO.

The biggest change in yield-bearing collateral by percentage was certainly RWAs, which grew 367% QoQ and was led by the $500 million Monetalis Clydesdale vault. However, the largest number change was actually the fall in G-UNI collateral. Covered in depth in Q2, G-UNI are wrapped Uni V3 LP tokens for USDC / DAI pools. The reduction appears to be primarily due to MakerDAO’s lowering the debt ceiling. Nearly $600 million, or 73%, of the $817 million reduction in TVL occurred on two separate occasions, October 13 and November 23, and over $1.3 billion was pulled from the Yearn Deployer. in Borrows against ETH (including stETH) and BTC each dropped 33% in Q4.

Maker accrued over $6 million in interest revenue in Q4. For the first time, non-crypto loan revenue accounted for the majority of the protocol’s quarterly revenues. RWA revenues accrue to an off-chain legal entity, so these revenues are not accounted for in some methods that measure on-chain earnings. The other notable increase is in the PSMs, with over $1 million in Q4. In October, MakerDAO approved a proposal from Gemini to earn interest (1.25% at inception) on GUSD in the PSM, as long as the balance at month end was above $100 million. We estimate these earnings similarly to RWA assets, by multiplying the asset base times the interest rate. PSM revenues are the only non-DAI revenue the DAO currently earns.

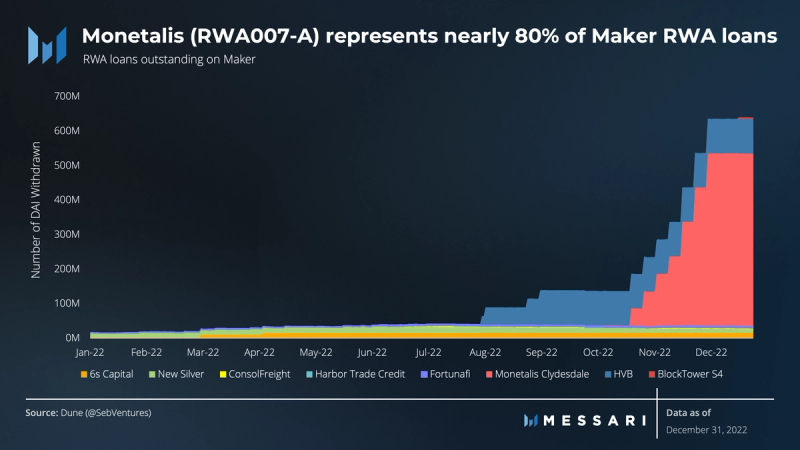

The biggest story of the quarter for MakerDAO was the launch of RWA007-A Monetalis Clydesdale. Within two months of launch, the entire credit line was withdrawn and invested. Maker’s second largest RWA vault, Huntingdon Valley Bank, had no change in its 100 million DAI loan in the quarter (the maximum that RWA has been allocated). MakerDAO also agreed to and launched RWA013-A BlockTower S4, which withdrew 5 million of its 70 million initial DAI debt ceiling on December 23. MakerDAO is now the largest off-chain loan provider, surpassing peers Goldfinch, Maple, and TrueFi in 2022.

In terms of on-chain lending, Maker ceded significant market share in wBTC lending to Aave and Compound. Maker’s share of wBTC deposits fell from 47% on October 1 to 23% at year-end. While there were also withdrawals from Aave and Compound, none to the degree of withdrawals from Maker. For wETH and wstETH, Maker’s share was relatively flat QoQ, while Compound’s share again fell, from 11% to 8%.

DAI Stablecoin

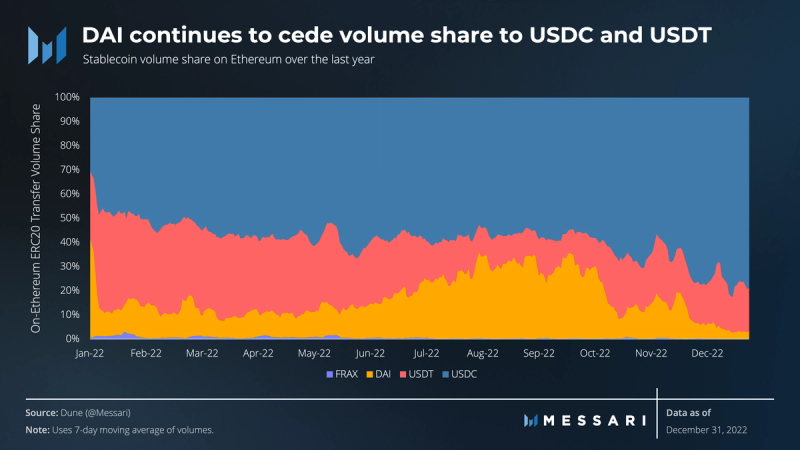

After gaining share last quarter on the back of centralization risks and USDC supply falling 13%, USDC supply increased by 2%, while DAI and FRAX supply on Ethereum fell 21% and 25%, respectively, in Q4. The diverging supply changes drove DAI’s market share from 8% to 6.3%.

Users of DAI continued to prefer to hold them in Externally Owned Accounts (EOAs), with the share of outstanding DAI in EOAs increasing from 50% to 60% over the quarter. Over 600 million DAI came off of decentralized exchanges (DEXs), largely due to the unwind of the G-UNI LP tokens, which took over 500 million DAI off of Uniswap. In Q4, DAI on lending protocols also fell dramatically (410 million), falling 64% on Aave, 29% on Compound, and 88% on Euler.

The reduction of DAI on DEXs and lending protocols is likely related to the fall in activity in DAI, as DAI volume fell 40% in Q4. Fees on Uniswap fell 21% QoQ, but in the two largest DAI / USDC pools fees fell 30%. The collapse of FTX and pursuant market volumes actually led to an increase in centralized stablecoins USDT and USDC, which had a 44% and a 16% increase in volume, respectively.

Qualitative Analysis

Real World Assets Update

MakerDAO continues to seek out new RWA investments, with its focus now mostly on cash-like, short-term opportunities. Two entities have emerged as MakerDAO’s primary RWA arrangers facilitating these investments, Monetalis and BlockTower Credit. Each entity had one vault officially launch this quarter (Monetalis Clydesdale and BlockTower / Centrifuge) and have another in the works (Monetalis Redwood Friesian and BlockTower-MIP90).

- The Monetalis Clydesdale vault invests USDC from the PSM into 0-1 Year and 1-3 Year U.S. treasuries, having re-allocated capital originally planned for medium-term corporate bonds to more short-term treasuries. Its entire 500 million DAI debt ceiling was drawn down in several portions throughout the quarter.

- BlockTower Credit’s 150 million DAI debt ceiling vault funds senior secured, real-world credit assets tokenized via Centrifuge Tinlake. BlockTower Credit is also providing $70 million of junior capital. It went live in December and so far 54 million DAI has been drawn down.

- The Monetalis Redwood Friesian vault seeks to invest up to 225 million USDC from the PSM into investment-grade residential mortgage-backed securities through Redwood’s Sequoia securitization platform. The proposal, which passed a ratification poll at the end of November, estimates an expected yield of 100 bps higher than the 3 Year U.S. Treasury rate.

- BlockTower Credit proposed to launch a 600 million DAI debt ceiling vault to invest in 70% AAA-rated structured credit and 30% money market funds. However, the proposal received some pushback. With the heightened focus on short-term, cash-like investments, BlockTower Credit commented recently that they are open to restructuring the investment to more closely reflect the Monetalis Clydesdale structure.

The set of Endgame Plan MIPs that passed in November (see more below) caused restructuring and offboarding of Core Units that dealt with RWA onboarding. The changes, which delegate ACREinvest summarizes well, have stalled RWA developments. A recent ratification poll passed, approving the Strategic Finance Core Unit’s updated mandate and budget to pick up RWA onboarding work.

Monetizing the PSMs

In Q3’22, Coinbase and Gemini made proposals that would give Maker yield on the USDC and GUSD in its Peg Stability Module (PSM).

Gemini proposed an incentives program to increase the adoption of GUSD within the PSM. The program pays Maker a 1.25% yield on all GUSD in the PSM, with the condition that its average monthly balance on the last day of the month is above 100 million. The proposal passed and in October the GUSD PSM debt ceiling was increased to 500 million and the tout (fee for swapping out of the PSM) was set at 20 bps to create outflow friction. Gemini made payments for the months of November and December, totaling over $1 million DAI.

Gemini halted withdrawals from its Earn program in the wake of the FTX and Genesis collapses, which caused some community members to question if Maker should continue the partnership. Almost 90% of the total GUSD supply is in the PSM. However, Gemini has stressed to the community that GUSD is unaffected by the Gemini Earn issues, and other community members are not worried. At the end of the year, Gemini announced that they plan to increase the reward to 1.5% in the new year. In January, MakerDAO held a vote over whether to adjust the debt ceiling given the concerns. At the end of the voting period, Gemini investor ParaFi delegated just enough MKR to keep the debt ceiling the same. Meanwhile, a concurrent vote was passed to decrease the tout to zero, which would theoretically allow the vault to unwind more naturally.

Coinbase’s proposal from last quarter passed a ratification poll in October, but has taken longer to be implemented, as both sides are figuring out the best technical solution. Unlike Gemini’s program that keeps GUSD in the PSM, Coinbase’s proposal involves custodying the USDC. There have been talks of implementing the program using either an off-chain structure with a legal entity (potentially using Monetalis as the arranger) or a smart contracts system. The Strategic Finance Core Unit believes the off-chain solution should be implemented while the smart contracts are finalized. However, several clauses in the proposed off-chain legal structure (including Coinbase’s ability to veto Maker’s USDC withdrawal requests and the introduction of Monetalis as the arranger) have faced pushback and will require further ironing out before the exact implementation is voted on.

A new PSM proposal this quarter came from Yearn, a DeFi yield aggregator. The proposal that passed a ratification poll in January seeks to onboard 100 million USDC from the PSM into a bespoke Yearn vault, which would earn an estimated 2% yield. MakerDAO community members are excited about diversifying the PSM into decentralized yield opportunities but are considerate of the risks.

In January, a new PSM partnership proposal came in from Paxos. Paxos is looking to incentivize usage of their stablecoin Pax Dollar (USDP) in a similar manner as Gemini. It is offering 45% of the effective federal funds rate on the amount of USDP in the PSM as long as the USDP PSM debt ceiling is at or above 1.5 billion USDP. Discussions are in the early stages.

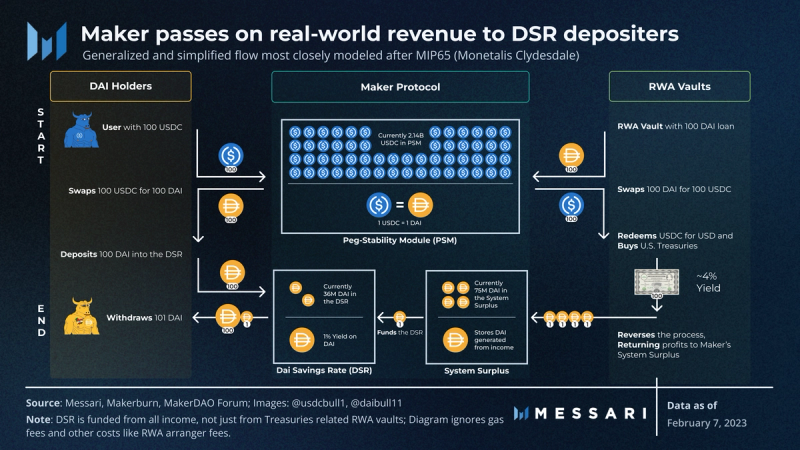

Return of the DAI Savings Rate (DSR)

The Dai Savings Rate (DSR) allows depositors to earn yield on DAI. It was first introduced in 2018 but was disabled in response to the Black Thursday crash in 2020, which de-pegged DAI and added bad debt to MakerDAO. It remained effectively disabled (was increased to 0.01% in Q1’21) until an executive vote in mid-December 2022 raised it to 1%.

The increase in DSR is enabled by MakerDAO’s stickier revenues from growing exposure to real-world rates through RWA vaults and PSM partnerships. The higher interest rate on DAI aims to increase DAI demand, which will allow MakerDAO to continue deploying more funds into these real-world, cash-like investments. However, some community members believe that MakerDAO hasn’t yet built up a big enough surplus and that there could be potential duration mismatches.

Turning on the DSR is imperative for the success of Maker’s transition from a primarily crypto-backed lender to a decentralized bank. Since 2020, DAI supply was supported largely by leverage demand on crypto-native assets; users wanted to borrow dollars against their tokens. Maker facilitated this transaction and DAI proliferated in the ecosystem. More recently, leverage demands have waned and competitors like Aave are launching their own stablecoin to facilitate cheap borrowing. Instead, MakerDAO has pivoted to focusing on lending to RWAs. This is enabled because of the demand for DAI in exchange for stablecoins (namely USDC). MakerDAO can facilitate loans that off-chain entities can turn into dollars by using USDC in the PSM. Like any bank, users can deposit USDC for DAI and receive a return on their savings by depositing the DAI into the DSR (like a savings account). By returning a yield to DAI holders, MakerDAO can drive demand for DAI in exchange for stablecoins. Like a bank, Maker will borrow liquid assets (savings) and lend out the duration curve, collecting the spread in interest rates from the maturity mismatch.

The strategy carries a real risk, as Maker needs to offer a rate higher than other native stablecoins. For example, if Circle can offer a native interest rate, it could likely offer a much higher rate than MakerDAO for the same risk. Likely, Circle is currently receiving over 4% yields on the collateral it holds to back USDC, given the rate of overnight lending markets. These are the most liquid and risk-less markets for non-bank entities. It is how savings accounts today offer greater than 3% yields. If Circle can pass some of these earnings to USDC holders, Maker will have to offer a higher yield in the DSR to retain capital. In the meantime, being the intermediary between the centralized stablecoin issuers and on-chain savers can be a lucrative business.

Following the increase, DAI in the DSR has increased from around 1 million to 36 million. But almost 31 million of that comes from one wallet. Because of Ethereum gas fees, a 1% DSR is not attractive enough for retail participation. Most DSR deposits will instead come from protocols. To this end, Maker Growth Core Unit posted a proposal on Compound’s forum to re-integrate Compound v2 with the DSR. OlympusDAO recently voted to deposit 77 million DAI from its treasury into the DSR. In the longer term, a DSR vault on L2s will enable more direct retail participation.

Endgame Plan Progress

MakerDAO’s Endgame Plan, which you can catch up on at the end of last quarter’s report, has continued to evolve this quarter with a formal governance vote on an initial set of Endgame pre-launch proposals, several teams announcing their creation of Clusters, and drafts of the Endgame Constitution and Scope Frameworks.

At the end of October 2022, a ratification poll passed for a set of Endgame Prelaunch proposals. The set includes frameworks for SubDAO Clusters, modifying existing Core Unit mandates related to collateral onboarding to smooth the transition to the Endgame, and activating a Protocol-Owned Vault, which Maker will use to accumulate liquid staked ETH derivatives, eventually turning into Maker’s own synthetic liquid staking ETH. On-chain sleuthing indicated that the vote was largely pushed through by Rune himself.

Clusters are teams voted on by SubDAO token holders to carry out the core work of the SubDAO. Several have begun to form this quarter. Two RWA-related Clusters are seeking to be voted into Protector SubDAOs: the Viridian Cluster with Monetalis as their primary arranger and the Spring Cluster with BlockTower Credit as their primary arranger and Centrifuge as the infrastructure service provider. The Crimson Cluster is seeking to be voted into a Creator SubDAO and provide innovative frontend and lending services.

Rune and other contributors have continued to flesh out the Endgame Plan, focusing this quarter mainly on creating the Constitution and Scope Frameworks. The Constitution is intended to be a high-level guiding document for MakerDAO, with Scope Frameworks providing more specific rules and principles for core Maker initiatives such as protocol engineering, decentralized collateral, growth, infrastructure, and more.

The Endgame is tentatively expected to launch in mid-2024. Major focus areas for 2023 include creating the pregame smart contracts, much of which can be taken from existing Maker smart contracts, creating the SubDAO front ends, fostering a community of Clusters and SubDAO members on a new forum, and revising the Constitution and Scope Frameworks.

Closing Summary

While markets were in flux most of Q4, MakerDAO continued to execute its strategy of becoming the first decentralized bank. Maker offers a savings rate via the DSR and turns stablecoin deposits in the PSM into interest-bearing loans. While the protocol is giving ground in crypto-loans, it has emerged as the most dominant player in off-chain lending. Combined with progress on the endgame plan, MakerDAO’s revenue sources suggest the DAO will look very different from the crypto-lending protocol of previous years. Diversifying the income stream in a bear market has so far been a great success, with plans for continued expansion in motion.