Key Insights

- The launch of the Range-Bound Stability (RBS) system can provide the stability OHM needs to gain acceptance as the crypto-native reserve currency.

- Olympus DAO has big plans to expand the supply of OHM sustainably, but the protocol’s rebase rate (staking rate) is suppressing the development and adoption of new projects.

- The DAO is currently discussing the best way to transition the staking rate from 7.35% to 0%, with options ranging from a wait-and-see approach to killing staking emissions all at once.

Introduction

Olympus has long sought to establish OHM as crypto’s decentralized reserve currency with autonomous and dynamic monetary policy governed by Olympus DAO, OHM’s central bank. Recently, Olympus has pivoted away from its ultra-inflationary bootstrapping tactics to double down on the stability, sustainable growth, and adoption of OHM.

A few months ago, Olympus introduced a Range-Bound Stability (RBS) mechanism through OIP 123 and launched a lending market pilot program with OIP 127. Olympus is now considering designating Lending Algorithmic Market Operations Controllers (AMOs) as a key focus area in 2023 per OIP 130. Going forward, Olympus has an ambitious project list for the rest of the year.

Despite an ambitious 2023 roadmap, Olympus’ overall goal of the widespread adoption of OHM as a reserve currency has suffered at the expense of the fixed 7.35% rebase rate (staking rate). This risk-free rate gradually dilutes the liquid backing per OHM, while limiting the functioning abilities of projects focused on OHM utility. A thread was recently shared on the Olympus Discord to create a plan to bring Olympus’ once astronomical staking rate down from 7.35% to 0%.

Understanding OHM

Stability

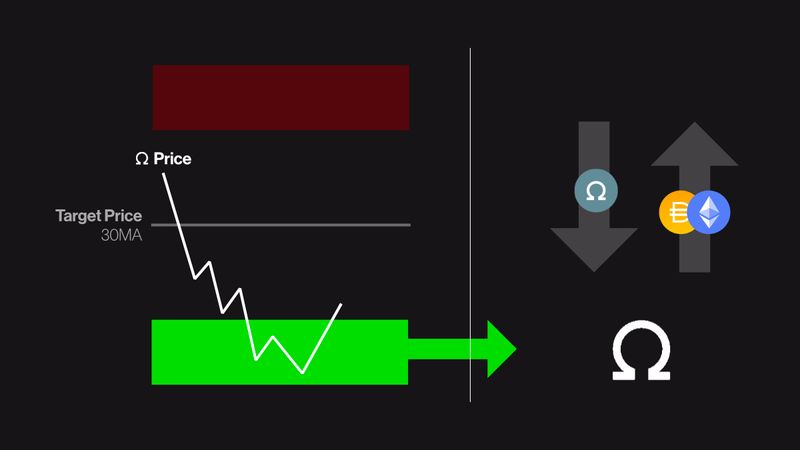

In November 2022, OIP 123 introduced a Range-Bound Stability (RBS) system to mitigate OHM’s price volatility relative to a specific reserve asset held in Olympus’ treasury contracts. The stability of OHM as a reserve currency is fundamental to both Olympus’ vision and product roadmap.

The RBS system works by guiding market participants with economic incentives. RBS allows Olympus DAO to define some parameters to smoothen the market price of OHM, including a dynamic target price and the range in which OHM should float relative to the target price.

When the market price of OHM begins to fall outside of the dynamic range, the protocol auctions off reserve assets at a discount, taking OHM out of circulation. Should the price continue to fall, the protocol will uses a predetermined portion of the treasury to place market orders for OHM above the current market price, creating an attractive arbitrage for traders.

Source: Olympus DAO

When the market price of OHM climbs outside of the range, the protocol auctions off newly-minted OHM at a discount to increase the circulating supply. If the price continues to climb, the protocol provides a discounted, fixed exchange rate to issue a capped amount of OHM. This enables traders to easily mint and sell OHM for a profit.

Source: Olympus DAO

The RBS parameters are tuned to target OHM’s 30-day moving average, with reserves defined as all of the DAI in the treasury contracts. With third-party market participants incentivized to serve as agents of the treasury, OHM’s RBS mechanism seems to check the “Stability” box.

Sustainable Growth

OHM has historically been issued through staking emissions and the sale of Reserve and Liquidity Bonds. For Olympus to achieve sustainable growth, the supply of OHM must scale according to demand. Unfortunately, OHM’s current staking rate of 7.35% fails to account for the market’s actual demand. As a result, it has resulted in the slow dilution of OHM’s liquid backing. As it stands, staking emissions are ultimately what’s dampening the effectiveness of RBS ever since OIP 125 adjusted the price target as the higher number between the 30-day moving average and the liquid backing per OHM.

In an effort to sustainably expand the supply of OHM, the DAO has decided to transition away from staking emissions in favor of OHM bonds. By selling future OHM at a discount, OHM bonds will introduce a crypto-native yield curve for a crypto-native reserve currency. OHM bond markets will enable the DAO to minimize and regulate bond yields, which would maximize the protocol’s benefit of OHM emissions.

Adoption

Olympus DAO has a lot in the pipeline regarding the adoption of OHM, with OIP 130 being the most recent initiative. The proposal aims to promote OHM as a borrowable asset by designating Olympus’ lending algorithmic market operations controllers (AMOs) project as one of the key focus areas in 2023.

Lending AMOs enable the protocol to mint and remove OHM directly to and from whitelisted lending markets. Protocols can only add newly minted OHM to the circulating supply once a user has deposited the necessary collateral and borrowed it. In other words, lending AMOs can further expand the supply of OHM without diluting its liquid backing. Additionally, lending AMOs can further diversify OHM’s backing by adding claims on various collateral assets into the mix.

By dictating the supply of borrowable OHM in lending markets, Olympus’ lending AMOs empower the protocol to provide the stable and predictable rates that borrowers desire. This stability could, in turn, drive borrowing demand for OHM. Furthermore, lending AMOs will allow users to hedge or short OHM, instilling natural market dynamics. The proposal also highlights the potential for lending AMOs to create an additional revenue stream for the DAO via lending interest. However, all of these advantages are contingent on the market’s desire to borrow OHM in the first place.

While OHM’s deep liquidity and Range-Bound Stability mechanism make it a desirable collateral asset, the market has yet to show meaningful demand for OHM credit. Of the ~70,000 OHM minted through the Lending Markets Pilot Program, only 23% is currently utilized on Silo, and 0% is utilized on Euler.

In Olympus’ defense, the program was intended to test rates and gauge market demand. Silo’s base borrow rate for OHM is 0% and 12.6% at kink, while Euler’s base borrow rate is 5% and 20% at kink. These rates suggest that borrowers are currently demanding a ~4% spread between the borrowing rate and OHM’s risk-free rebase rate of 7.35%.

Unlike staking ETH in the Ethereum network, staking OHM doesn’t directly contribute to Olympus’ security. Therefore, users borrowing and staking OHM simply introduce more staking emissions without adding value to the protocol. It’s in Olympus’ best interest to set rates at a level that discourages excessive amounts of leveraged staking. At the same time, the rates should encourage the productive use of OHM, making it difficult for OHM to compete with the lower borrow rates for dollar-pegged stablecoins.

Reducing Olympus’ Staking Rate

On Feb. 27, 2023, abipup, a DAO contributor, created a thread on the Olympus Discord addressing the undesired consequences of the staking rate. The thread highlights that staking and the existence of gOHM, a wrapped representation of staked OHM, complicate key projects such as OHM bonds, on-chain governance, LP farming, and lending AMOs. The post presents three potential options to reduce the staking rate from 7.35% to 0% in an effort to increase OHM’s productivity.

Option 1

The first option suggests issuing a one-time six-month OHM bond at a fixed rate of 7.33%. Once the bond market closes, the DAO can either gradually or immediately reduce the staking rate to zero. This option offers an alternative for OHM stakers searching for simple yield since they can simply unstake their OHM and purchase the bond.

Several community members have embraced this approach. They’ve emphasized that it’s time to “rip off the band-aid” while highlighting that it won’t be difficult for Ohmies to beat the staking rate of 0%.

On the other hand, this transition would complicate things for Olympus’ Flexible Loans project and external protocols, like Alchemix, that have built products that rely on gOHM’s yield-bearing properties. Abruptly ending the staking emissions could damage Olympus DAO’s reputation as the central bank for a crypto-native reserve currency.

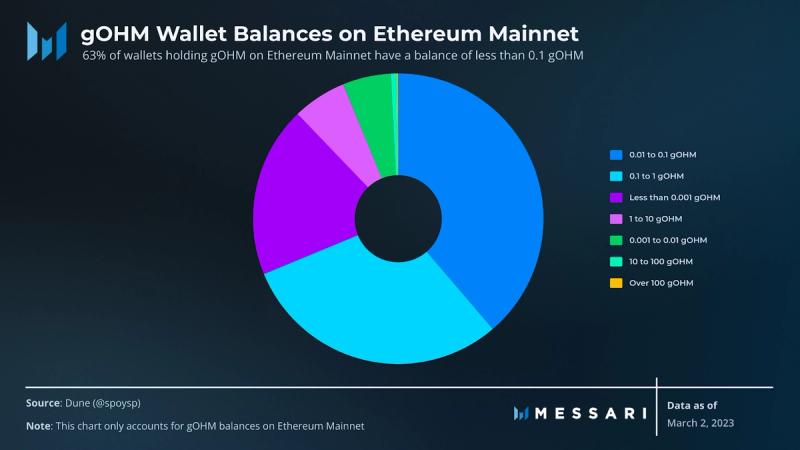

Furthermore, the transition would require users to manually unstake and purchase an OHM bond. While this option does force active stakers to actively use their OHM to search for better yield opportunities, it may be a tough sell considering Ethereum’s gas fees could potentially dissuade the ~63% of holders on mainnet that hold less than 0.1 gOHM from participating.

Option 2

The second option proposes waiting until the broader lending projects, including leverage, LP farming, and OHM bond vaults, are implemented to reassess lowering OHM’s staking rate. This approach acknowledges that killing the staking rate before alternative yield opportunities arise could be detrimental to the protocol. It also allows Olympus’ partners plenty of time to explore alternative yield paths.

This option fails to address the short- and medium-term issues caused by staking, which could potentially cost the protocol millions of dollars in OHM emissions. 0xFelix highlights that it’s unlikely projects will be developed and adopted with such a high staking rate. As such, increasing the monetary velocity should be a top priority if Olympus plans to establish OHM as a reserve currency.

Option 3

The third option combines the previous two options. It advises the DAO to take a step-by-step approach and gradually reduce the staking rate as projects are completed. The proposal recommends waiting until the lending AMO pilot is finished, then reducing the staking rate to 2.33%, and later reducing the rate to 0% once the remaining lending-related projects are completed.

This option gives partners time to adjust to the changes, removes some of the protocol costs via lowered emissions, and incentivizes active stakers to seek better yield opportunities. However, it fails to completely solve any of the issues caused by the fixed staking rate. DAO contributor sh4dow voiced concerns that gradually reducing the staking rate will make it difficult to calculate long-term OHM bond rates. abipup summarized the issues with Option 3 by stating that it “kicks the can down the road.”

Although Option 3 dampens the problems caused by OHM’s staking emissions without solving them, it does provide a slightly better user experience by staggering the reduction.

What’s Next?

Killing staking emissions will undoubtedly bring OHM closer to its goal of becoming the crypto-native reserve currency, but the transition won’t be easy. The Olympus community appears to be heavily divided on which plan to move forward with. Right now, most Ohmies seem to favor Option 3.

Given that the proposal is still in its ideation phase, adjustments will be made as new ideas arise. While the path to 0% staking emissions will be challenging for Olympus DAO, it won’t be the first time a DAO has pivoted away from the rebase model. Creating a crypto-native reserve currency was never going to be a small task.