In this new roundup we will look at a strategy called ‘bias’ that analyzes the recurring behaviors of a specific market. The strategy identifies time slots, or days of the week for example, when it is more convenient to buy or sell a specific underlying asset.

Specifically, this type of strategy exploits information from all the recurring behaviors that occur over a set period. Depending on the duration of a trade, three different macro-categories of bias strategies can be distinguished:

- Intraday

- Weekly

- Monthly or ‘Seasonal’

In the specific case of this article, the analysis focuses on a rather fast time horizon, the intraday one, and we are going to test the idea on the second most capitalized cryptocurrency in the world: Ethereum.

Testing the Bias trading strategy on Ethereum (ETH)

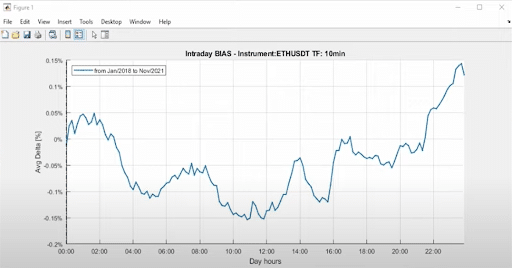

We proceed with a test on the Unger Academy® software, the Bias Finder , which will allow in a very simple way to evaluate the average historical price trend of Ethereum. Figure 1 shows this trend over the period from 2018 to 2021.

, which will allow in a very simple way to evaluate the average historical price trend of Ethereum. Figure 1 shows this trend over the period from 2018 to 2021.

It can be seen almost at a glance how in the initial hours of the session, which starts at midnight (GTC), there is a bearish trend that is promptly recovered in the late morning hours, around 11:00 AM, and lasts until the final hours of the session in a sort of harmonious cycle of declines and rises that follows one another day after day.

Clearly, the trend analyzed is only an average result, so it does not amount to a guarantee that every day of the year Ethereum moves following this trend. However, the truth remains that the sum of the movements recorded on ETH led to these results, so it is worth investigating based on the time frames uncovered by the software.

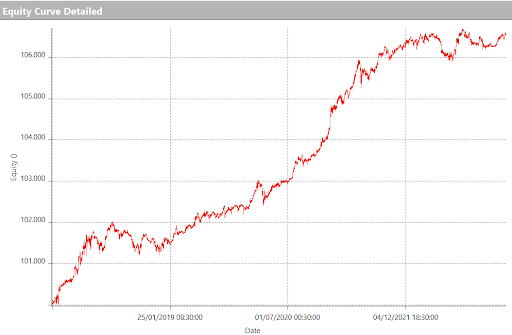

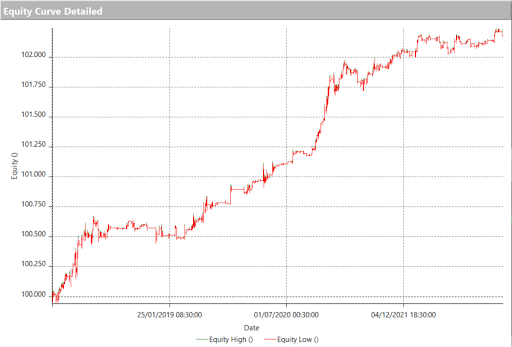

Specifically, using this information to build an automated strategy, one can see in the following figures how buying daily at 11:00 AM and closing the trade a quarter of an hour before the session closes, at 11:45 PM, immediately yields an excellent profit curve (Figure 2).

Backtesting the strategy

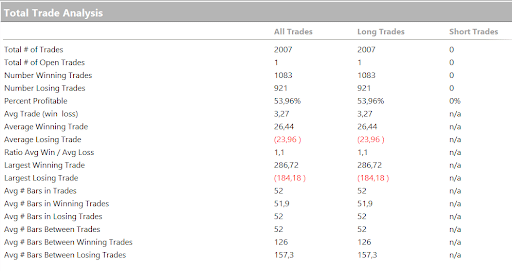

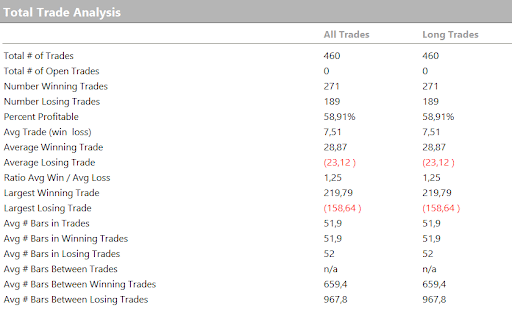

The size used for one trade in this backtest is $1000. The backtest starts in 2017 and ends in the early days of the year 2023.

The sore point of this strategy concerns the average trade, which barely touches $3.27 (or 0.327% of the position’s countervalue). Certainly not a figure that allows for safe trading with this system in the real market, because the commission costs and slippage (i.e., the difference between theoretical and actual price) that a trader would have to pay, could be quantified at around $2 (0.2% of the position’s countervalue) hence remaining with a meager 0.127% (3.27-2=1.27$) as the net average trade.

In any case, this result is interesting in that it must be remembered that the system, as designed, stays in the market only a few hours and makes a trade every day of the backtest. In short, a bit like staying in the market 12 hours on and 12 hours off, continuously, every day of the year. It becomes more understandable that it is not possible to aspire to extremely large average trades, but one can always try to improve the value by adding a condition that limits the number of trades in the history and make the strategy more effective and selective.

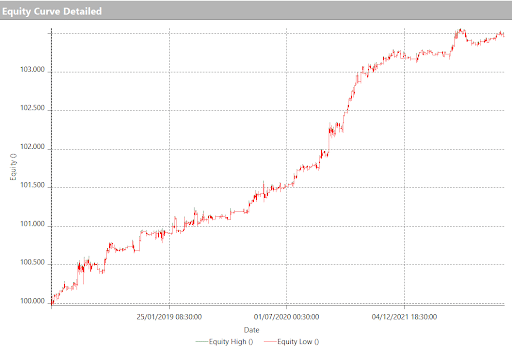

In the figures below we see how adding a condition, found within a list of proprietary patterns, improves results. Indeed, by isolating the trade on days when today’s session high is at least 0.75% higher than the previous session high, the strategy goes from an average trade of $3.27 to $7.50 (0.75% of the position).

This condition identifies an additional confirmation situation in addition to the hourly signal in which the trend of the current session is bullish, at least compared to the previous day. One will proceed to open the long trade (buy trade) only if by 11:00 AM today, the market is showing strength compared to the day before. A kind of further confirmation on the short-term trend of the market.

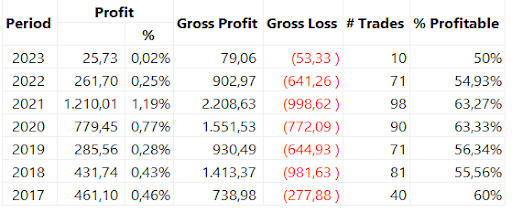

The profit curve also takes a more graceful shape, with good results in all years of the backtest, including 2022, a year that we know has been very difficult for ETH and all crypto in general. Moreover, 2022 was left out of the initial backtest run by the software. Hence, even the ‘out of sample’ period, the portion of time not considered in the backtest, was more than positive, and this only corroborates the basic idea of the system.

Refine the strategy

However, the strategy could be further refined, or slightly modified, for example by adding a stop-loss (point of maximum loss acceptable by the system), or a take-profit (point of maximum profit beyond which to cash out the gain) or another condition suitable to further limiting the number of trades. This is meant to be just an initial idea to show what are the tangible advantages in operating with an automated strategy compared to a more traditional ‘buy-and-hold’.

On the other hand, it must be acknowledged that 5-6 years of backtesting may not be enough to make a definitive judgment on the strategy, especially since it is biased, which is usually a strategy that may harbor more pitfalls than more classic types of entry such as ‘trend-following‘. What is certain is that the more than 450 trades obtained during the backtest period represent a reliable statistical sample.

As further counter-evidence on the work done, we now proceed to use this same strategy also on the main cryptocurrency market, Bitcoin, where good results continue to be obtained, in the wake of what we have seen on Ethereum (Figure 7).

This additional test adds effectiveness to the work done on ETH and gives the strategy even more robustness.

Cryptocurrencies are certainly a young market, still immature, but beginning to mature over time. Strategies away from the more traditional ones, such as precisely bias, are beginning to show comforting signs even on these financial products, an indication that perhaps these markets could be used in a well-diversified portfolio context.

Until next time!

Andrea Unger