Key Insights

- While usage measured in transactions, volume, and DAUs fell in Q3, transactions and DAUs were up significantly over the last year.

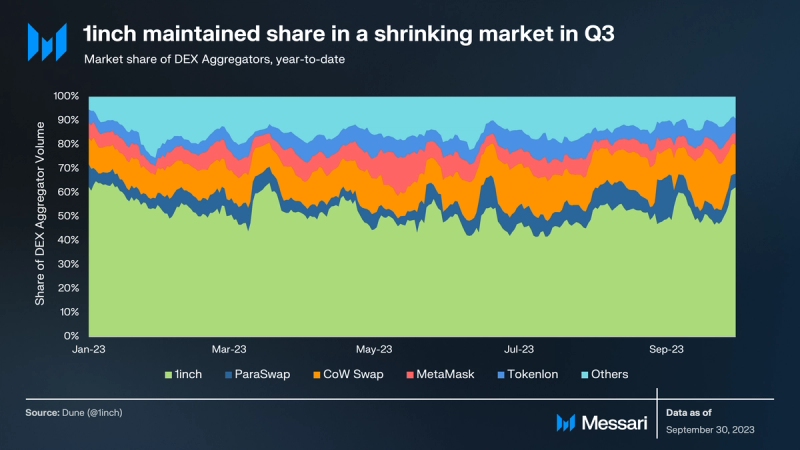

- 1inch maintained its 50% volume market share this quarter among DEX aggregators, though the pie shrunk 20%.

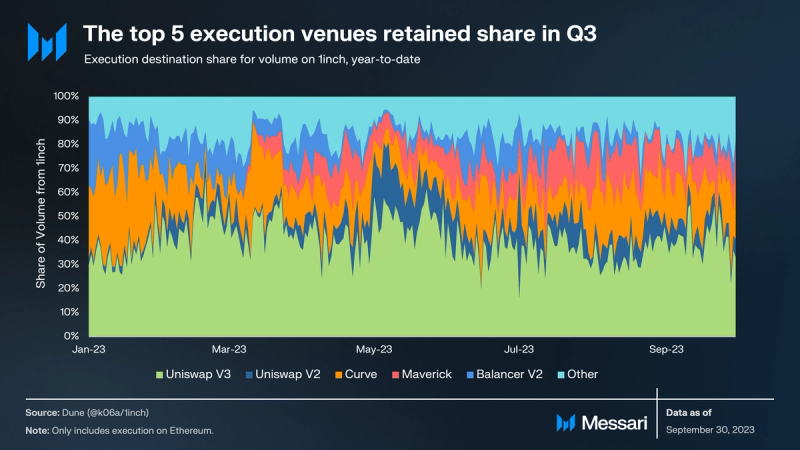

- On Ethereum, the top five execution venues for trades routed through 1inch made up 84% of volumes for the second consecutive quarter.

- 1INCH staking increased only 5% in the quarter, as falling volumes limited resolver earnings and thus APRs for stakers.

Primer on 1inch Network

The 1inch Network is an all-in-one decentralized finance (DeFi) service provider operating on Ethereum, Arbitrum, Optimism, Polygon, zkSync Era, Avalanche, BNB Chain, Gnosis, Fantom, Klaytn, and Aurora. Launched in 2019, 1inch Aggregation Protocol (AP) allows users to route trades across various markets and realize the best available rate compared to any individual decentralized exchange (DEX). In late 2020, the 1inch Liquidity Protocol introduced a native automated market maker (AMM) to the network, which enabled users to provide liquidity and earn passive liquidity mining rewards.

The network’s third product, the 1inch Limit Order Protocol (LOP), was introduced in June 2021 to support conditional limit and stop-loss orders with no fees. In late December 2022, the 1inch Swap Engine enabled Fusion mode, which is partially based on the existing tech, including the 1inch Limit Order Protocol and the 1inch Aggregation Protocol. This new feature empowers DeFi users to place orders with a specified price and time range without paying network fees. All three protocols, and Fusion mode, are governed by the 1inch DAO using the network’s native 1INCH token.

Note: This report includes data from Ethereum, BNB Chain, Polygon, Optimism, Arbitrum, Avalanche, Gnosis Chain, Fantom, and Base. Data from zkSync, Klaytn, and Aurora are currently not included. We are working to improve access to this data.

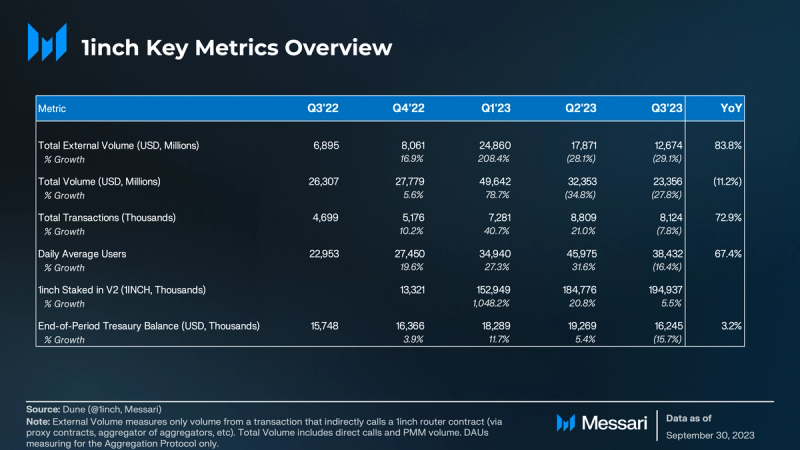

Key Metrics

Performance Analysis

Usage Analysis

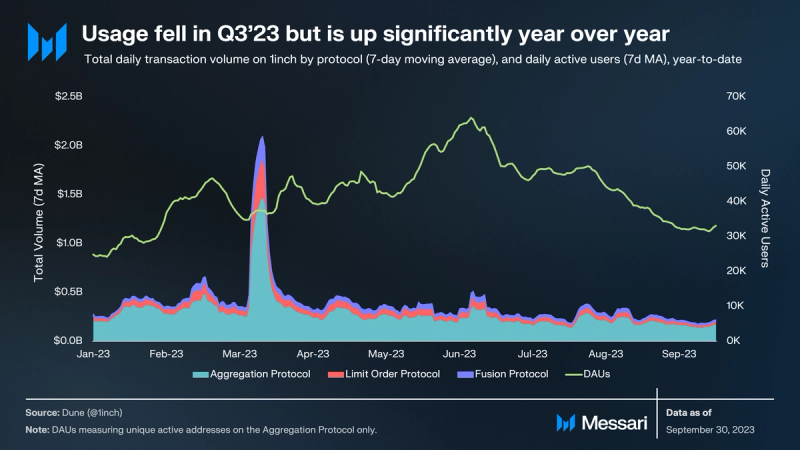

1inch continued to attract strong usage, though daily average unique users (measured by number of addresses) fell to just under 40,000 in Q3. Over 50% of users were on 1inch’s largest two markets by DAUs, Polygon and BNB. Both fell in Q3, though only by 8% and 7.4%, respectively. The biggest decliners in terms of DAUs were Arbitrum and Avalanche, where usage declined 36% and 46% to 5,900 and 2,100 DAUs, respectively. Optimism was the only 1inch instance to see users grow, increasing 14% to over 2,700.

In terms of volume, trading on 1inch continued to normalize after the USDC depeg in Q1. Volume fell in each protocol in Q3, led by the Limit Order Protocol volume falling 37% to $3.3 billion in volume. Volumes via 1inch Fusion fell 29% to $2.7 billion in the quarter, and volume on the Aggregation Protocol fell 25% to $17 billion. Ethereum continued to be the largest 1inch instance by volume, responsible for 72% of the volume in the quarter.

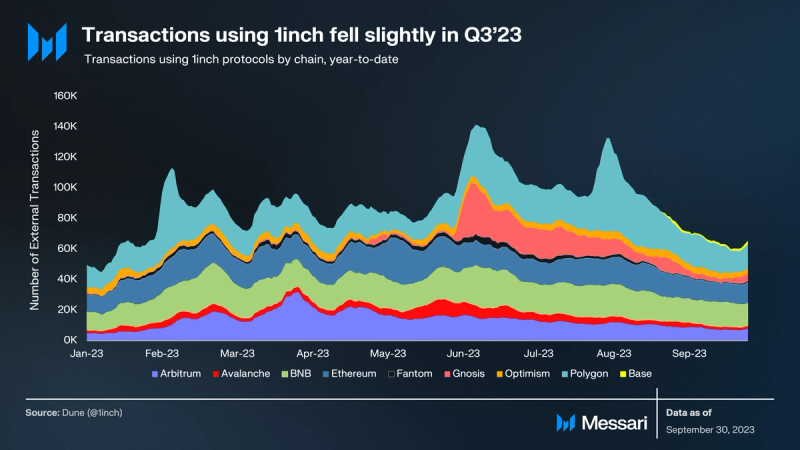

Transaction and volume trends by chain were similar in Q3, with Arbitrum and Avalanche transaction counts falling 39% and 45%, respectively. Activity did grow on Gnosis, Optimism, and Polygon, however. In Q3, Polygon activity accounted for 30% of 1inch transactions, with BNB second at 20%. 1inch also launched on Base in Q3, which executed over 55,000 transactions in the quarter.

The number of external transactions represents the transactions on 1inch that originate from proxy contracts or aggregators rather than those that directly interact with the router contracts. As such, external transactions give a clear picture of the success and usage of 1inch integrations. In Q3, external transactions actually increased by 15%. Polygon posted an impressive 91% increase in the number of daily external transactions on 1inch, averaging over 19,000 per day in Q3. Other L2s had split experiences, with Optimism transactions increasing 45% to 2,600 per day while activity on Arbitrum fell 37% to 5,500 per day.

As the number of transactions increased and volume fell, the average trade size on 1inch fell in Q3. By protocol, the aggregation and limit order protocols average trade size fell 20% and 15%, respectively. 1inch Fusion, on the other hand, saw its average trade size remain flat quarter-over-quarter. Fusion is primarily used for reducing slippage, which generally increases with larger trade values. Thus, it averaged the largest trades by protocol at over $5,700 per trade.

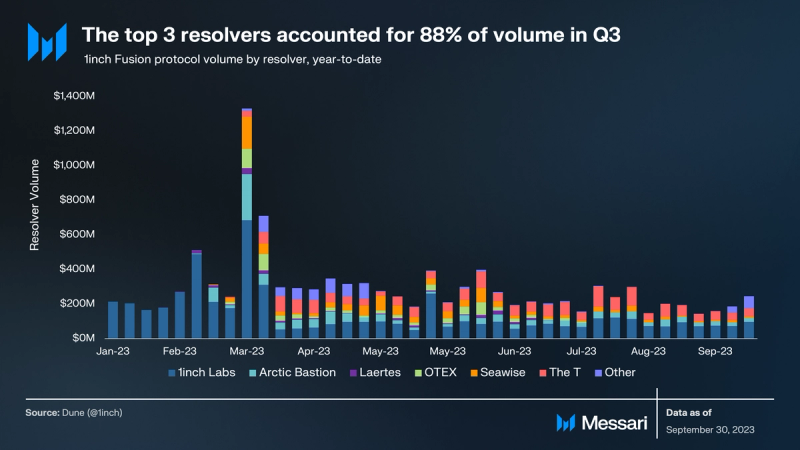

Total trading volume via 1inch Fusion fell 29% to under $3 billion in Q3. The mix of volume by resolvers also concentrated on the three biggest winners thus far: 1inch, Arctic Bastion, and The T. Despite the fall in overall volume, the cumulative volume of those three was roughly flat quarter-over-quarter at $2.3 billion. In Q3, they made up 88% of volume versus only 64% in Q2. The increase in share is primarily a result of Wintermute, The Open DAO, and OTEX all losing their viability as resolvers at different times in the last five months.

In July, the 1inch DAO voted to change how resolvers can participate in executing Fusion volume. The community of users and teams operating resolvers had an important debate about the best way to benefit users and build a sustainable ecosystem. One side argued that increasing the number of resolvers from five to ten would increase competition. The opposing side maintained that the economics of running a resolver do not clearly support enough earnings and thus APR to attract delegation to compete. A possible solution could involve priority fee limits, which make up a large portion of the trade costs for resolvers. However, the power of competition could also drive innovators to find new ways to profit from Fusion volumes and offer stakers APR to get to 10% delegation.

Market Share Analysis

1inch connects with over 40 DEXs to facilitate trade execution on Ethereum alone. The top 5 venues accounted for 84% of 1inch’s volume on Ethereum in both of the last two quarters, down from 87% in Q1. Within that group, Uniswap’s share (including both V2 and V3) fell from 51% in Q2 to 45% in Q3, while Curve and Maverick both increased their share to 18% and 14%, respectively.

In Q3, DEX aggregator volumes fell 20% from Q2 to just under $16 billion. 1inch retained its greater-than 50% market share again this quarter. CoW Swap and ParaSwap both increased share this quarter, rising to 15% and 8%, respectively. MetaMask volume fell the most at -48% QoQ and saw its share shrink to 5%, executing under $1 billion in volume.

Treasury and Staking Analysis

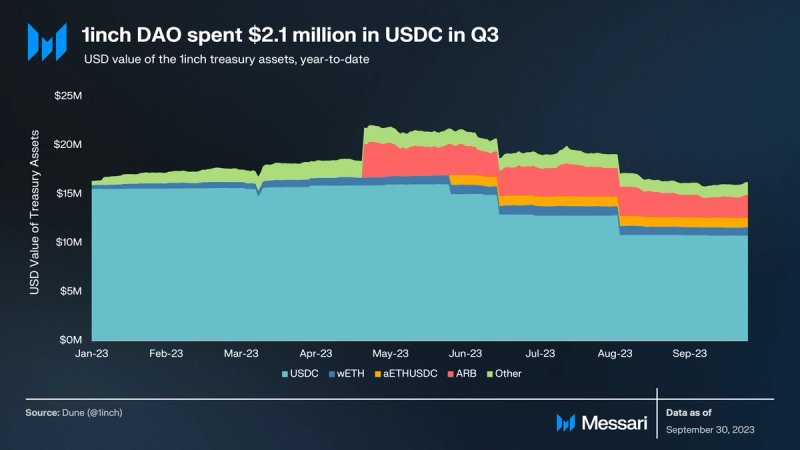

The DAO turned off slippage revenue last quarter and also allocated $1 million USDC as a deposit on Aave to earn interest. The UDSC deposit has accrued by less than 1% in value so far, and there has been no other revenue. The largest expense in Q3 was the Events Grant (1IP-34) proposal that passed to fund 1inch at conferences and events with 1.94 million USDC. Besides USDC, all other asset balances remained unchanged in the quarter, though price changes led to a roughly $1 million loss in USD value, led by a $627,000 mark-to-market loss in ARB.

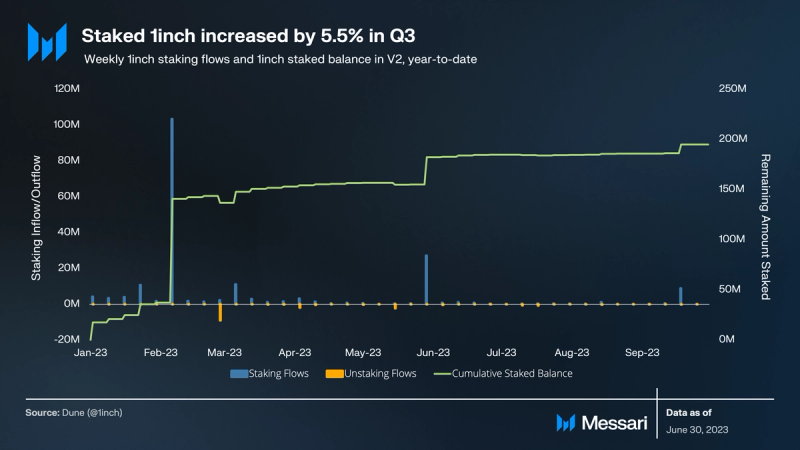

Turnover and staking flows were small in the quarter, with 12.6 million 1INCH staked and 2.4 million 1INCH unstaked. The 194 million 1INCH staked accounted for nearly 20% of the circulating supply. Demand for staking is the accumulation of Unicorn Power, which can then be used to vote on proposals in the 1inch DAO or can be delegated to a resolver to earn. Resolvers are essentially market makers who execute transactions in the 1inch Fusion. Their participation and access to those orders are limited by their total Unicorn Power as they must have delegations of at least 10% of Unicorn Power in the network to participate in fusion transaction execution. Thus, resolvers are incentivized to share their earnings and earn a delegation. Currently, resolvers offer 3.75%-4.8% APRs to delegators.

Qualitative Analysis

Strategy Outlook

Aggregating the actions and updates by the 1inch Network team and funding by the DAO helps bring the long-term strategy outlook into context. Since building the leading DEX aggregator, the 1inch Network team and DAO has remained committed to its defense of its market share. Next, they plan to turn the protocol into infrastructure and build a user-aligned business that drives value to the token. As 1inch continues to roll out updates and strategically allocate funding through its DAO, the team ultimately aims to go directly to the consumer.

Defending a Leading Market Share

1inch is by far the leading DEX aggregator in crypto, today. The Performance Analysis section covers the recent quarter and usage of the protocol.

As 1inch seeks to defend its position, it has continued to add integrations, partnerships, and execution venues. In the third quarter, it added a multitude of new execution venues including SushiSwap V3, Velodrome V2, Carbon DeFi, Pendle, LEVEL Finance, and WOOFi V2 on zkSync Era. It also integrated with new demand sources including Kaikas, a non-custodial digital wallet from Klaytn, South Korea’s leading Web3 ecosystem, and Fox Wallet. Lastly, 1inch expanded to the fastest growing roll-up, Base, launching its Aggregation Router and Limit Order Protocol on the L2.

Beyond adding new products, like the 1inch Fusion, 1inch must keep up with liquidity sources, demand sources, and expansions in order to maintain market share in a competitive product category.

Building a Business

The accrual for the 1INCH token changed dramatically this year with the release of staking V2, the end of swap surplus revenue, and the release of the 1inch Fusion. Though the token still gives voting rights in the DAO, which controls the $16 million treasury, the end of surplus revenue changes the expected growth of that pool of assets. Now, the primary value driver for 1INCH is likely staking and delegating to a resolver in exchange for earnings. 1inch currently runs the largest resolver by volume and offers a roughly 4% APR to delegators.

Through its new resolver model, 1inch has aligned a business for the token and others to build on with a market-leading product for consumers. Resolvers on 1inch are the market makers who have access to execute orders on 1inch Fusion, where users sign intent-based transactions specifying their preferred terms. Resolvers can see the orders and compete to fill them, within the constraints specified by the user. The Dutch-auction-esque process means resolvers only need to bid up to the point where they are willing to accept the trade as well — in other words, the point where they are comfortable with the profit margin. Thus, when transactions occur, both participants’ trade requirements have been met.

For this reason, being a resolver should be a profitable business like any other market making operation where orders are bid upon based on the market maker’s point of profitability. Staking and delegating aligns these businesses with the token, with whom they must share some profits (i.e., an exchange fee, of sorts).

Winning the Consumer

Since building a leading product in the aggregation protocol, 1inch is now in a position to create a best-in-class user experience that can further increase market share.

Since at least 2022, the 1inch team has focused on wallets and self-custody. Last quarter, 1inch DAO voted to fund the completion of the 1inch Hardware Wallet. This quarter also included many updates to their existing wallet apps for both iOS and Android. In July, the 1inch Wallet V1.15 was released for Android with an added check for suspicious domains and wallet addresses. Later in the quarter, V1.16 was released with a new portfolio feature that enables users to track investment performance and control their portfolios directly in the 1inch Wallet. For iOS users, V2.2.0 was released in Q3 with many new features including address book, a new send flow, integration with the newly launched network Base, quick actions in Wallet Picker, and enhanced support for NFT domains.

The wallet functions as the user’s gateway to crypto and likely one of the stickiest ways to win transactions and volumes. Along with its market-leading DEX aggregator, the new 1inch Fusion should be a top choice for users looking to transact more patiently but with more constraints. As a marketplace, 1inch needs both high-powered resolvers competing for the business and users driving volume, providing opportunity for those market makers. For this model to work, 1inch must be able to win the customer.

Closing Summary

1inch completed another quarter as the leading DEX aggregator in crypto, maintaining a 50% share and executing over $20 billion in volume. While volumes fell, the number of daily active wallet addresses continued its climb along with the number of daily transactions, indicating increasing demand for the product. Polygon and Base remained the instances with the most transactions and users, while Ethereum kept its place as the volume king. Volumes via 1inch Fusion fell 29%, and the big three resolvers, 1inch, The T, and Arctic Bastion, increased their share of volume. The 1inch team continued to add new demand integrations, liquidity venues, and chains to maintain and grow their share. Looking forward, the recent wallet updates and the future hardware wallet presented some promising opportunities to win the consumer and drive more usage of the core products.