Key Insights

- Cardano’s stablecoin value was up 16% QoQ and 461% YTD. Native stablecoins like iUSD started this momentum, but in Q3, bridged versions of USDT and USDC were introduced by Wanchain.

- Cardano’s TVL was flat QoQ but was up 198% YTD. Cardano’s TVL ranking among all networks increased from 34th at the beginning of 2023 to 15th.

- Project Catalyst Fund10 was completed, funding 192 projects from the Cardano Treasury from a fund pool of 50 million ADA.

- The Voltaire governance phase continued to build momentum with the launch of SanchoNet and Intersect. SanchoNet is a testnet for onchain governance, and Intersect is a Cardano member-based organization.

- Mithril launched with nearly 100 SPOs participating in signing certificates. Mithril is a stake-based signature scheme and protocol that improves the speed and efficiency of node syncing times.

Primer on Cardano

Cardano is a Proof-of-Stake (PoS) Layer-1 smart contract network launched in 2017. Cardano aims to provide security, scalability, and sustainability to decentralized applications and systems building on top of the blockchain. In addition to the community of developers, node operators, and projects, Cardano is supported by multiple entities: Input Output Global (IOG), dcSpark, MLabs, The Cardano Foundation, EMURGO, and more. They work together to support the network’s development, adoption, and finances while Cardano moves toward the age of Voltaire.

Cardano has taken a unique approach to development when compared to other smart contract networks. The Ouroboros consensus model allows for delegation of stake, the extended unspent transaction output (eUTXO) accounting model enables native token transfers, scalability, and decentralization, and smart contracts were enabled by the Alonzo hard fork in 2021.

With a dedicated community of users and developers, Cardano has demonstrated staying power. Post-Alonzo, Cardano began to compete in more traditional crypto markets, such as DeFi and NFTs, while remaining focused on its core goals. For a full primer on Cardano, refer to our Initiation of Coverage report.

Key Metrics

Financial Analysis

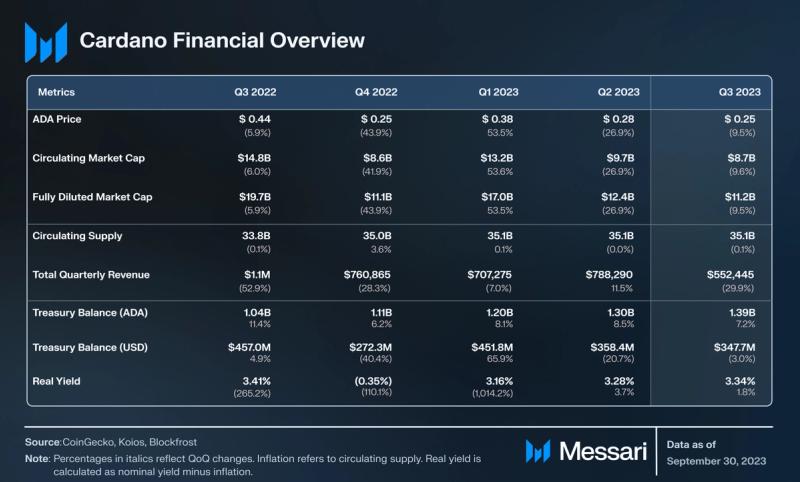

Q3’23 featured a largely quiet, sideways trading overall crypto market. The one major exception was a large selloff in mid-August. ADA’s price declined for the second consecutive quarter, down 9.5% QoQ to $0.25. This was generally in line with the overall crypto market, which fell 9.2% QoQ.

ADA is the native asset of Cardano. It has three primary use cases: (1) settling network fees, (2) being used to register a stake pool to participate in network consensus as a pool operator, and (3) staking as a pool operator or delegator to help secure the network and earn token rewards.

Revenue (USD) declined 29.9% QoQ. Revenue is driven by transaction fees, which are mostly affected by users’ urgency to transact. Q3’s transaction fees are explored further in the Network Analysis.

Cardano’s Treasury balance grew 7.2% QoQ to 1.39 billion ADA. The 90 million ADA increase was generally in line with growth from previous quarters. Due to ADA price depreciation, the treasury’s value in USD terms decreased 3.0% QoQ from $358 million to $348 million. Currently, 20% of all transaction fees go to the treasury, which can be changed via governance if needed.

The nominal staking yield on Cardano is generally 3.3% for ADA delegators, although it can vary by stake pool. Real yield is calculated as nominal yield minus inflation to account for any value dilution due to inflation. In Q3, real yield was 3.34%. Any reference to inflation in this report refers to ADA’s circulating supply rather than its total supply, since ADA’s supply is capped at 45 billion. In each epoch, 0.3% of ADA reserves (i.e., the ADA not in circulation) are distributed as stake pool operator (SPO) rewards. This “inflation” trends towards zero as the reserves deplete and the circulating supply approaches 45 billion.

Network Analysis

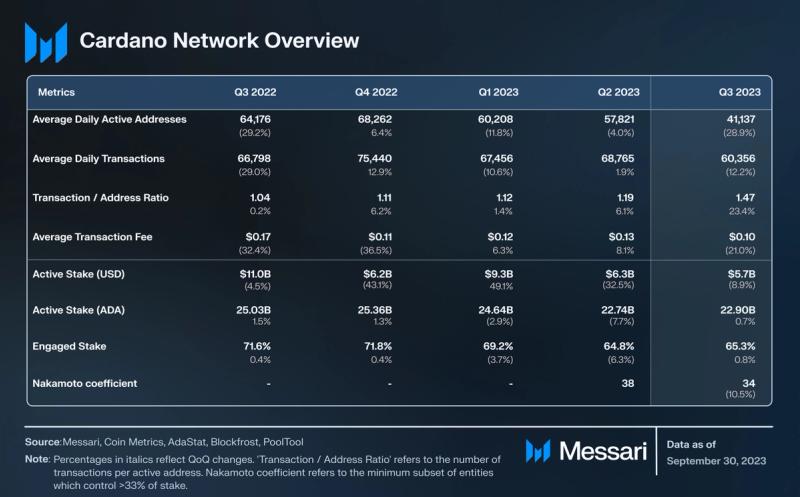

The average transaction fee (USD) decreased 21.0% QoQ from $0.13 to $0.10. The average transaction fee (ADA), on the other hand, only decreased by 2.8% QoQ. The disparity indicates that ADA’s price action was almost completely responsible for the decrease denominated in USD. Each transaction on the network is accompanied by a fee for processing actions and storage costs. Fees are calculated by a minimum payable fee in addition to transaction size.

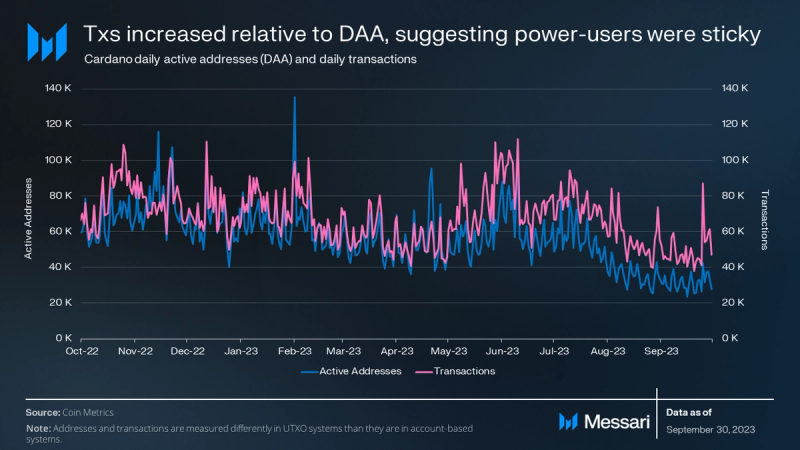

Various growing niches on Cardano, such as DeFi, have not been enough to increase overall activity metrics. Daily active addresses declined for the third consecutive quarter, down 28.9% QoQ to 41,100. Average daily transactions also decreased but by a smaller margin of 12.2% QoQ.

The movement in transactions and active addresses are typically correlated, but they have deviated in recent quarters. The ratio of transactions to active addresses has grown steadily over the past year, suggesting that while some users are not regularly active, those present are power users. In Q3, the Transaction / Active Address ratio of 1.47 was up 23.4% QoQ and 41.3% YoY.

Note that Cardano uses a variant of the unspent transaction output (UTXO) accounting model, like Bitcoin. Some activity metrics, such as those involving addresses and transfers, are fundamentally different from those on networks with account-based accounting models (e.g., Ethereum, Solana).

Cardano’s average blockchain load decreased from just over 50% in Q2 to roughly 40% in Q3. The average daily load in Q3 peaked at 75.8% on July 11. A 100% load would mean that all blocks are full (currently 90 kb per block), and a 0% load would mean that all blocks are empty. Smaller transactions, created by more efficient coin selection algorithms, would help increase Cardano’s TPS and bandwidth in the event of a 100% blockchain load.New development languages and toolkits, such as Aiken, have also improved efficiency in terms of both execution speed and memory.

Staking

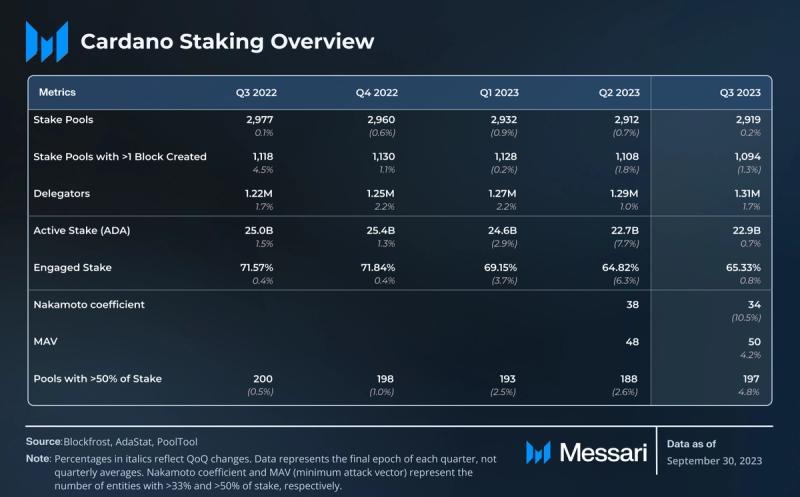

The number of stake pools and delegators did not change significantly in Q3. Stake pools are run by various entities, such as individuals (public or anonymous) or organizations (crypto-native or other). Regardless of the entity in charge, many stake pool operators (SPOs) operate several pools due to the current incentives limiting the maximum size of a pool. Accounting for multi-pools, there were 2,036 unique SPOs (1,862 single-pool operators and 174 multi-pool operators) in Q3. However, the real number of SPOs may be slightly lower, since not all SPOs identify their pools in ways that can be linked.

Stake and delegator distribution were largely unbalanced across total pools in Q3. Of the 22.9 billion total staked ADA, the top 197 pools (6.7% of pools) accounted for over 50%. While the top 197 pools would technically make the minimum attack vector (MAV), there are actually only 50 entities, as many of the top pools are run by multi-pool operators. Another measure of decentralization, the Nakamoto coefficient, ended the quarter at 34.

While 50 (MAV) and 34 (Nakamoto coefficient) are low numbers relative to the total number of pools and delegators, they’re considerably higher than many other networks. The Edinburgh Decentralization Index (EDI) offers a new framework to measure decentralization. In addition, a beta feature in the Lace wallet enabled users to stake ADA across multiple pools, which would grant delegators more flexibility over their distribution of stake.

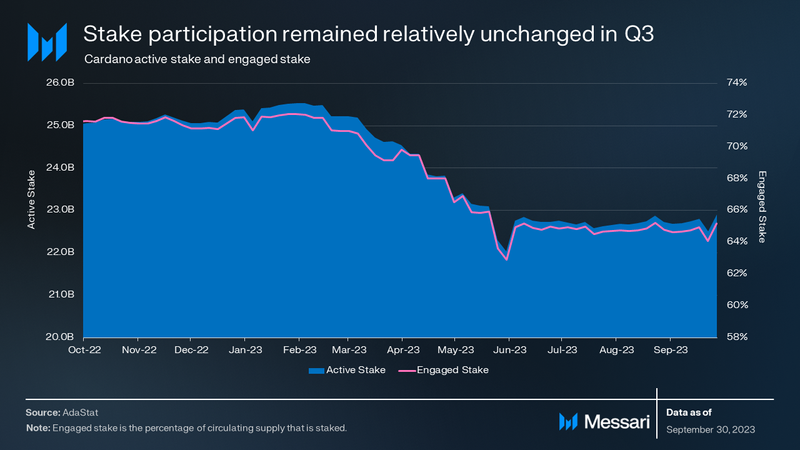

Active stake grew slightly, up 0.7% QoQ to 22.9 billion ADA. Also, engaged stake grew 0.8% QoQ to 65.3%.

Since 2022, there has been a community discussion over changing two vital variables related to staking:

- K parameter: The level at which a staking pool becomes saturated and experiences diminishing rewards.

- Min pool fee: The flat amount paid to a pool before rewards are split among delegators. It is done automatically so there is no risk of delegators not being paid.

After a long and nuanced discussion, SPOs have decided to not yet make any changes to the K parameter. The Parameter Committee determined the results were inconclusive. In general, the majority of SPOs voted to raise the K parameter to 1,000, which would change the optimal pool size from 70 million ADA to 35 million ADA. However, the SPOs that control a majority of the stake voted to keep the K parameter at its current value of 500. Changing the minimum pool fee on the other hand was more conclusive; it is currently the recommendation of the Parameter Committee in PCP-01.

Mithril

In July, Mithril went live on mainnet in beta and produced its first snapshot. Nearly 100 stake pools have contributed to signing Mithril certificates already. Mithril is a stake-based multisignature scheme that is intended to help the Cardano network to scale. It offers a lightweight, efficient experience and a secure alternative for users and applications to access all or parts of the state of the chain. Its users do not require access to the full current state yet receive a similar level of trust. As such, Cardano’s network becomes more efficient, streamlined, and capable of supporting a wider range of applications and use cases.

Mithril will enable applications such as

- “Light” wallets with no additional trust assumptions

- Fast bootstrapping of full nodes

- Efficient voting systems

Since its deployment on mainnet in July, Mithril signers have been deployed by about 80 SPOs, totaling over 1.5 billion ADA in stake, and adoption keeps growing. Improvements to the download and extraction process reduced the time to bootstrap a Cardano node to under 20 minutes on a consumer-grade laptop.

Mithril is both a novel cryptography scheme and a network of signing nodes deployed alongside the Cardano network. Mithril signers are lightweight processes run by SPOs alongside block producers which produce stake-based signatures sent to aggregators. Mithril clients can download and verify certified snapshots from untrusted so-called aggregators. They can then use those snapshots to resolve chain synchronization, state bootstrapping, and chain validation.

SanchoNet

SanchoNet was launched in Q3 in the node V8.2.1 pre-release, marking a milestone for onchain governance. SanchoNet is a testnet for Cardano’s onchain governance, as defined by CIP-1694 guidelines and as a core initiative of the Voltaire roadmap phase.

Voltaire will take the final steps toward self-sustainability via onchain voting. After completion, the community will control parameter changes, hard forks, and the treasury withdrawals rather than IOG, Cardano Foundation, and EMURGO — which combined hold all seven governance (genesis) keys.

The infrastructure required for a successful onchain voting platform does not yet exist. To meet this need, SanchoNet serves as a sandbox to test and build out not only processes but also tools. Developers can use the testnet to launch new infrastructure (e.g., wallets and vote explorers), SPOs can test voting/proposing to find pain points, and a new user role — delegate representatives (DReps) — can be hashed out.

SanchoNet is championed by Intersect — a member-based organization for the Cardano ecosystem — among other community members, SPOs, and teams. Intersect launched with the aim of bringing all ADA holders together behind a shared vision to enable a more resilient, secure, transparent, and innovative Cardano ecosystem. Intersect is heavily aligned with Voltaire and bottom-up coordination: true decentralization.

Ecosystem Analysis

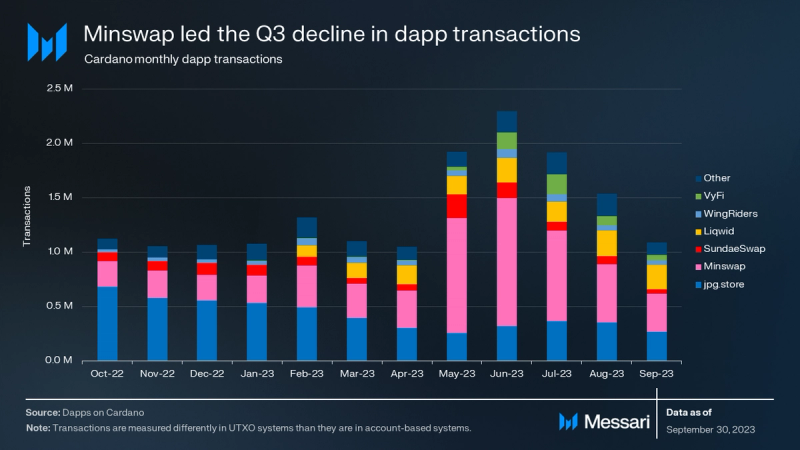

Average daily dapp transactions decreased 14.7% QoQ. However, this Q3 decrease was not enough to offset previous consecutive quarters of increases. Dapp transactions still finished the quarter up 40.0% YTD. NFT transaction activity declined for the third consecutive quarter, down 3.0% in Q3. Despite this, NFT trading volume increased 19.8% QoQ, displaying the average growth in value of Cardano NFTs. NFT innovation continues to be driven by projects such as Book.io, Paima, and Empowa.

As of the end of Q3, there are 144 projects building on Cardano and thousands of tokens, with the top 10 tokens having a combined market cap of over $400 million.

Minswap, an automated market maker (AMM), was the most popular Cardano dapp by transactions in Q3 for the second quarter in a row. Minswap remained the most-used dapp despite its 33.5% QoQ decline in transactions. Minswap’s in-development Stableswap feature may help the protocol drive even more activity by providing minimal slippage and more efficient trading.

DeFi

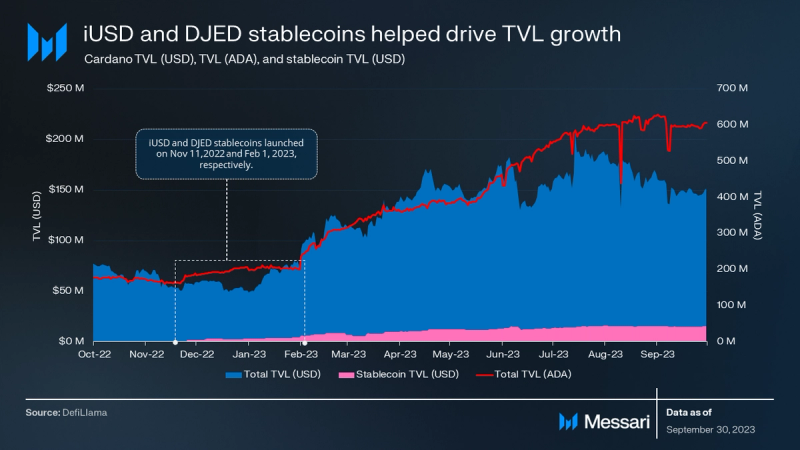

TVL (QoQ) was steady, declining 0.1% QoQ. Cardano’s TVL ranking among all networks increased from 21st to 15th during Q3 (starting at 34th at the beginning of the year). This shows that while TVL did not grow in absolute USD terms, it grew relative to other ecosystems. TVL (USD) staying flat despite ADA’s nearly 10% QoQ price decline suggests growth and asset diversification.

The launch of two new stablecoins, iUSD and DJED, in the past year proved to be a major catalyst for overall TVL. The total stablecoin market cap grew 16.3% QoQ from $13.5 million to $15.7 million. Relative to other networks, Cardano’s stablecoin market cap moved up from 54th to 32nd in 2023. Stable assets are ideal for pairing in liquidity pools, borrowing and lending, creating leverage, and providing quick escapes from volatility – which is quite common in the crypto market.

Indigo and Djed are the two main stablecoin issuers on Cardano. They issue the overcollateralized tokens iUSD and DJED, respectively. Indigo and Djed further contribute to TVL by offering other tokens as well, such as Indigo’s synthetic asset iETH and Djed’s reserve token SHEN. Between the overcollateralization of the stablecoins themselves and the other assets created, protocol TVL is several times higher than the stablecoin market cap in the case of both issuers.

Wanchain — an L1 PoS EVM blockchain and a decentralized blockchain interoperability solution — has made USDT and USDC available on Cardano through its various bridges. Wanchain’s bridges are secured by Wanchain validators, connecting Cardano to Wanchain, Bitcoin, Ethereum, TRON, and more. Bridged versions of Bitcoin and USDT/USDC (the largest stablecoins by market cap in all of crypto) have created a massive liquidity opportunity for Cardano DeFi.

Smart token standards such as CIP-68 or CPS-0003 could open the door for built-in compliance, allowing USDC to be natively available on Cardano as well. USDA and USDM are two additional Cardano-native stablecoins. Mehen’s USDM and Anzens’ USDA stablecoins are both in development, preparing for Cardano mainnet.

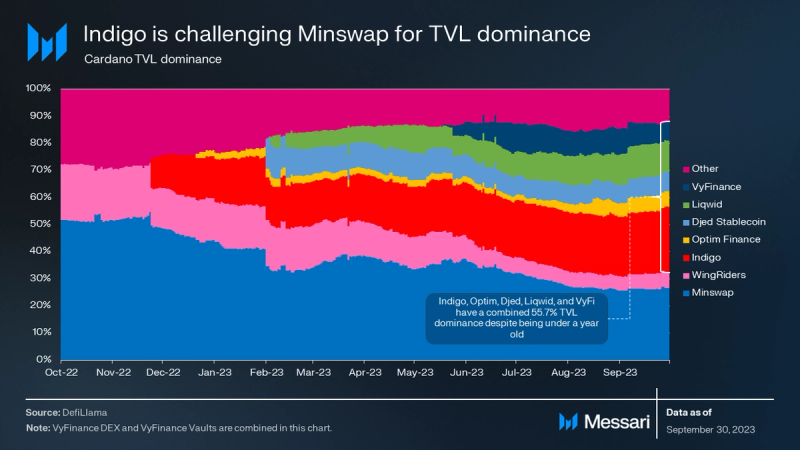

Much of the 2023 TVL growth was driven by newer protocols. As of the end of Q3, 55.7% of TVL has come from protocols launched within the last year. Synthetic asset-issuer Indigo is the oldest and largest of these new protocols, ending the quarter challenging Minswap for overall TVL dominance. Indigo’s $36.8 million in TVL was not far behind Minswap’s $40.2 million.

TVL and DeFi ecosystem growth has come with growing pains, specifically for DEXs. Cardano’s novel eUTXO mechanism brought new DeFi paradigms with it, such as batching and transaction chaining. Many DEXs are exploring new or improved solutions, such as MuesliSwap working on transaction chaining. Transaction chaining, already implemented on protocols such as Optim Fi, should be an improvement over MuesliSwap’s contested batching process.

Sidechains

Cardano has a handful of sidechains — some live in production and some still in development. Some of these networks include Milkomeda C1, Wanchain, Midnight, and World Mobile.

Milkomeda C1 launched in early 2022 as Cardano’s first sidechain. It initially brought EVM compatibility to the Cardano ecosystem, but in early September, it brought EVM compatibility directly to Cardano wallets. Milkomeda C1 is primarily maintained by dcSpark. Most of Milkomeda’s activity comes in the form of games built with Paima Engine — a framework for rollups focused on creating onchain games and autonomous worlds. Unlike all other current rollups (including Ethereum rollups which use centralized sequencers), Paima-built rollups are true rollups with decentralized sequencing/proving, like Fuel V1.

IOG launched a toolkit for building custom sidechains for Cardano, including a technical specification for developing sidechains on Cardano, a chain follower. The toolkit was showcased alongside a proof-of-concept EVM testnet.

Midnight is Cardano’s upcoming data-protection-focused sidechain. By leveraging zero-knowledge cryptography, Midnight aims to bridge the principles of DeFi with the requirements of TradFi. It will enable users to have selective data disclosure while meeting regulatory needs. The users will also be able to choose which data they wish to reveal publicly or keep private. Unlike Milkomeda, Midnight will have its own token: DUST. The upcoming launch of the initial devnet will include up to 100 development teams, with applications open in October.

Hydra

In Q3, Hydra V0.12.0 was released. Hydra is a family of scaling protocols, mostly L2s based on state channels. Hydra Head, the first solution from the set, is an offchain mini ledger that works between a small group of participants, not unlike other popular state channels such as Lightning. Hydra leverages the eUTXO model for a more efficient and flexible transfer from L1 to L2 and back, allowing for the isomorphic transfer of data. Hydra for Payments is an open-source toolkit for implementing payment solutions that will leverage Hydra Head.

The first Head on the Cardano mainnet, also known as a channel, was opened in a limited form in March 2023. As of writing, the protocol can be considered to be in a “public beta.” Until the protocol is more thoroughly tested, the quantity of ADA committed is limited for user safety. Builders from various teams are actively working on improvements to Hydra Head. Early applications include gaming, auctions, and P2P payments. All in all, Hydra Head is a flexible protocol, with several proposed topologies.

Project Catalyst

Project Catalyst is a decentralized fund for innovative projects in the Cardano ecosystem, supported by the ADA treasury. Through all 10 funding rounds, Catalyst has funded 1,344 proposals. Fund10, the most recent fund, ended in September 2023 with 192 funded proposals. dcSpark was the top-funded team with 6.26 million ADA ($1.6 million) in funding; its top-funded proposals were related to Paima Engine.

Participation and vote-selling (i.e., paying another user for their vote) are two points of focus in decentralized governance that affect nearly all groups and initiatives. The community has continued to explore different ways to improve its governance process. These include assessing proposals, distributing funds, increasing participation, and formalizing vote-selling.

Over its two-week voting period, Catalyst Fund10 received just under 410,000 votes, an increase of over 45,000 more than in the previous fund. The increase brought the total number of votes cast across Catalyst’s lifetime to more than 2 million. Fund10 saw 60,000 wallets registered with a total voting count of 4.5 billion ADA. However, only 7,900 of those wallets actually voted to confirm a proposal, 50% of which only voted on 10 or fewer of the over 1,000 total proposals.

The relatively low participation rate (in terms of both users and ADA) had some community members suggesting different models and incentives. Due to Project Catalyst’s linear token-based voting (i.e., 1 token equals 1 vote), the top 1.5% of wallets controlled 56% of the voting power. Certain voting schemes, such as quadratic, conviction, and reputation-based voting, may be worth exploring. Other schemes, such as holographic, are likely counterproductive in addressing vote-selling — should the community deem it to be an issue and not an opportunity for both yield and added transparency.

Optim Finance formalized vote-selling in Fund10 with its liquidity bonds — a vehicle to borrow and lend ADA delegation and, by extension, voting power. Optim’s model enables borrowers to pay a premium to gain additional voting power from lenders. Thus, a user can pay a relatively small premium to borrow many votes for a single epoch to vote for or against Catalyst proposals. Vote-selling already happens, so making it a transparent process would only strengthen governance in the long term.

Cardano addresses have separate keys for payment and staking, enabling native liquid staking. In other words, users can deposit ADA on protocols (i.e., the protocol contract owns the payment key) without having to relinquish control of the stake key. This process is handled differently by various protocols:

- Indigo keeps the lender’s stake key attached to their own deposits, retaining voting rights for the lender.

- Minswap attaches its own stake key to the lender’s deposits, transferring voting rights to the protocol.

- Optim attaches the borrower’s stake key to the lender’s deposits, transferring voting rights to the borrower.

Development and Growth

Notable events in Q3 include:

- The IOG Academy, an initiative presented by IOG Education, provided open courses and technical guides to development with Marlowe, Haskell, and Plutus.

- The Cardano Foundation and Emurgo continued to run developer education programs.

- Community-run projects for education and developer tools, such as Gimbalabs and Genius Academy, continued to produce content and host events.

- IOG continued to facilitate Working Groups to assist and support Cardano ecosystem developers, while member-based organization Intersect established several new committees.

Closing Summary

Interoperability and core infrastructure both accelerated in Q3. Wanchain connected Cardano to top networks and assets, Milkomeda made EVM contracts accessible directly from Cardano wallets, and development continued on other sidechains such as Midnight. As for infrastructure, Hydra state channels saw new use cases and an update; Mithril launched on mainnet pushing towards greater decentralization; and the SanchoNet onchain governance testnet was launched.

DeFi is positioned to be an early beneficiary of the new infrastructure and connections to other ecosystems. The new liquidity from both native and bridged assets has already proven to boost activity and TVL in 2023. New use cases for that liquidity may be enabled soon from infrastructure such as Hydra or some of the many DeFi projects recently funded by Project Catalyst.