Key Insights

- Goldfinch is facing its first two credit events in 2023, including a technical default and a pending write-down. In response, the community treasury has stepped in to allocate funds to offset the loan in default, while Warbler Labs plans to cover losses in the other.

- Goldfinch’s “DeFi For The World” initiative aims to simplify the UX of digital wallets, eliminating the need for usernames, passwords, or private keys.

- As of September 30, FIDU was trading at 81c on Curve, representing a 52% implied yield for holders if the loans are fully repaid on time.

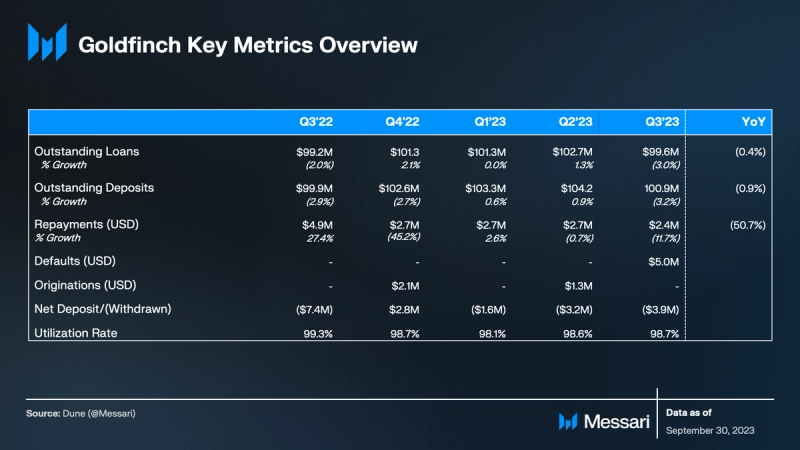

- Goldfinch’s outstanding loan balance decreased by 1.8% YTD, with one new origination of a 90-day callable loan to Fazz, marking Goldfinch’s first callable loan.

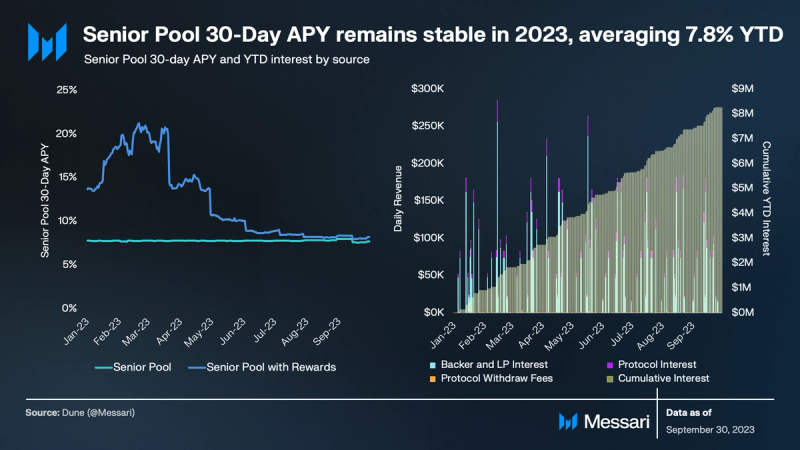

- The Senior Pool APY has remained flat YTD, averaging 7.8% throughout the third quarter.

- Warbler Labs recently introduced a visionary blueprint for Goldfinch, aiming to evolve it into a decentralized operating system for lending.

Primer on Goldfinch

Goldfinch is an open-source credit protocol built on Ethereum. It was launched in January 2021 to enable decentralized lending focused on emerging credit markets. The protocol’s business model is to originate loans using collateralized real-world assets (RWA), insulating them from crypto volatility. The protocol enforces Compliance standards such as know your customer (KYC), anti-money laundering (AML), and onchain reputations using Goldfinch’s novel soul-bound Unique Identity (UID) which incentivizes users to maintain credibility and accountability.

The participants in Goldfinch include Liquidity Providers (LPs), Backers, and Borrowers. The lending pool either aggregates USDC deposited by LPs and Backers in two tranches (senior/junior) or more recently has created pools that are “unitranche” and are only Backers. LPs represent a second-loss reserve depositing into a Senior Pool (Sr. tranche), whereas Backers represent a first-loss reserve (Jr. tranche). Backers perform due diligence on prospective Borrowers and inherit more risk than LPs. Borrowers on Goldfinch are financial institutions (e.g., asset managers or fintech lenders) that submit term sheets for loan approval before accessing any liquidity. They then extend loans to businesses.

Key Metrics

Performance Analysis

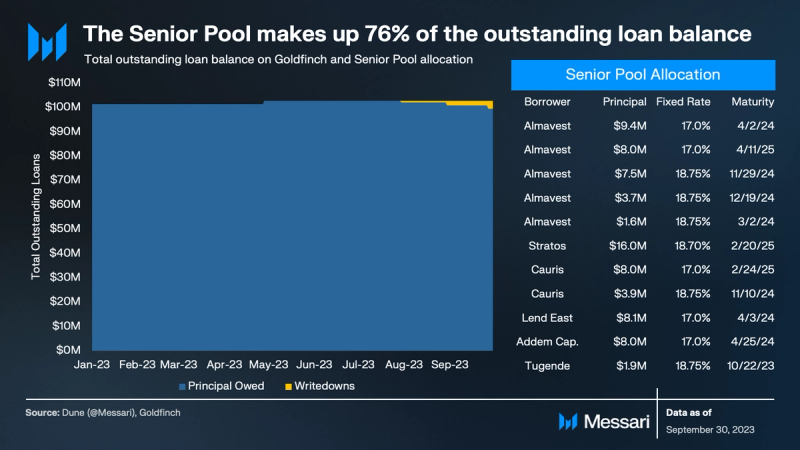

In 2023, Goldfinch’s outstanding loan balance has slightly dipped by 1.8%, standing at $99.6 million as of September 30. Of this balane, 76% is attributed to the Senior Pool, which carries a weighted fixed interest rate of 12.4%, factoring in the designated allocations for Backers and the Protocol.

The single loan origination this year was in April, when Goldfinch’s backers collectively raised $1.35 million to issue a 90-day callable loan to Fazz, a fintech company based in Singapore and backed by Tiger Global. This marked Goldfinch’s first venture into callable loans, which allow the lender to demand full repayment and receive it at the end of that quarter. Such loans offer lenders added protection against changes in market conditions and potential credit risks.

The Tugende loan posed challenges for the Senior Pool in Q3. It led to a phased write-down of $3.1 million from the original $5 million, triggered by a technical default in July. In September, Warbler Labs provided an update, revealing that they and Tugende had agreed in principle to a restructuring plan. The plan centered on the potential for a significant recovery for the Goldfinch Senior Pool. Following discussions and a Snapshot vote in October, the community implemented a response plan. Since its implementation, the plan has since provided relief and brought the loan current on its interest obligations.

The 30-day annual percentage yield (APY) for the Senior pool is denominated in USDC and based on the actual interest payments received. The Base APY for the Senior pool remained consistent. It averaged 7.6% through Q3, largely due to no material change in the portfolio’s loan balance. Meanwhile, the APY when including GFI rewards dropped notably from 17.6% in Q1 to 8.3% in Q3. This significant reduction was a result of GIP-43, in which the community voted to reallocate 1.2 million GFI from the Senior Pool LP liquidity mining rewards allocation to the Backer Rewards allocation.

In Q1 2022, Goldfinch governance enacted GIP-01, introducing the FIDU-USDC Curve pool into the Goldfinch ecosystem. This initiative was designed to enhance liquidity and offer Senior pool LPs a streamlined, fee-free avenue for transitioning in and out of FIDU. Simultaneously, the initiative would alleviate potential withdrawal pressures on the Senior Pool. During this period, the Senior Pool maintained a balanced stance, with 60% of LP funds being utilized and the remaining 40% kept idle for immediate withdrawal.

However, the equilibrium was disrupted following the Terra/LUNA collapse in Q2 2022. Despite the portfolio’s consistent performance and a 0% loss rate, the broader market uncertainty drove investors to prioritize the “first come, first serve” withdrawal system. This trend significantly increased liquidity demands, depleting the Senior Pool’s idle USDC and pushing the Senior Pool’s utilization rates close to 100%. In response, Goldfinch introduced a bi-weekly withdrawal system in Q4. This system mandates LPs to submit their FIDU for a withdrawal request, with bi-weekly pro-rata distributions allocated as Borrower payments are received.

For LPs considering liquidating their FIDU positions, they have two avenues: either enter the structured withdrawal queue to exchange FIDU for USDC at the programmatic “share price” or directly swap FIDU for USDC on Curve. This share price reflects the Senior Pool’s Net Asset Value (NAV), encompassing the principal owed, interest accrued, and any loan write-downs. By the end of September, the NAV saw a 2% uptick YTD, inclusive of $3.1 million Tugende loan write-down.

LPs lending to Goldfinch can anticipate an annual yield of roughly 8%, with a principal-weighted time to maturity of 13 months. As these maturity dates approach, the discount to NAV on Curve has expanded, shifting from 15% in Q1 to 34% by Q3. This trend presents a unique opportunity for investors willing to underwrite the default risks and liquidity premium. With the FIDU price on Goldfinch trading at $1.13 as of September 30, and the price on Curve at $0.81, buyers could earn a 52% yield if all the remaining loans are paid in full with interest.

Qualitative Analysis

DeFi For The World

Despite the blockchain landscape approaching a decade of innovation, the intricate nature of managing digital assets has continued to be a significant hurdle for mainstream adoption. Recognizing this challenge, Goldfinch introduced DeFi For The World, an initiative designed to streamline the user experience in the digital asset realm. This project aims to eliminate the intricacies associated with traditional wallets, doing away with the need for usernames, passwords, and private keys.

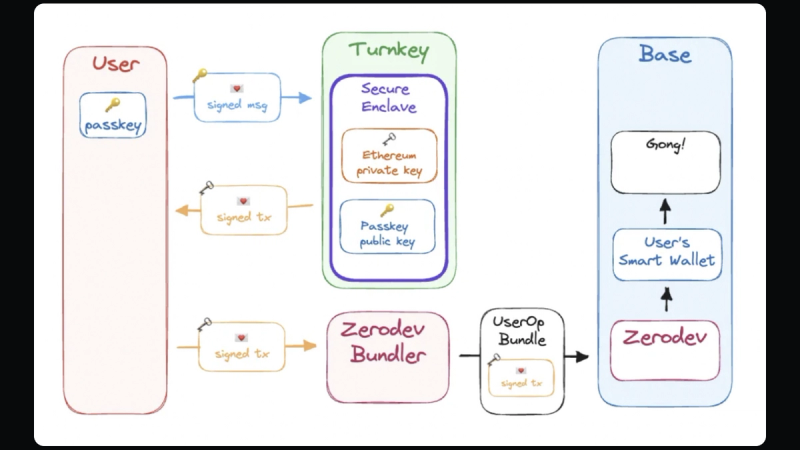

Source: DeFi For The World

For authentication, Goldfinch adopted the use of Passkeys. This feature was recently brought into the limelight by tech giants Apple and Google. Essentially, Passkeys are innovative tools that provide account security without the traditional password. They often incorporate biometric features, like Apple’s Face ID, for enhanced security. While functioning within an on-device secure enclave, akin to a hardware wallet, Passkeys utilize a private/public key mechanism for various actions. This design ensures the Passkey remains confined to the device, with only its signed messages being public, bolstering security and minimizing phishing threats.

While Passkeys were a leap forward in user experience, they presented a technical challenge: their inability to sign Ethereum transactions due to differing cryptographic languages. To address this, Goldfinch collaborated with Turnkey to leverage their expertise in cloud-based secure enclaves, which was instrumental in transforming the Passkey signature into a format compatible with Ethereum. This ensured that transaction initiation remained exclusive to the Passkey. This collaboration successfully overcame the signature challenge, resulting in the ability to execute Ethereum-ready transactions..

Yet, creating a signed transaction was only half the battle. The next step was its onchain submission, which demanded gas. Here, two pivotal advancements proved invaluable: Account Abstraction and Layer-2 networks. Account Abstraction, also known as Smart Wallets, introduced flexibility in transaction signing methods and facilitated gas sponsorship. On the other hand, Layer-2 networks, fortified by the security of Ethereum Mainnet, promised swifter and cost-effective transactions. By synergizing Account Abstraction and partnering with Coinbase’s Layer-2 network, Base, Goldfinch has positioned itself at the forefront of simplifying blockchain interactions for users worldwide.

Navigating Loan Defaults and Restructuring

In 2023, Goldfinch has faced challenges with its first two credit events. One deal entered a technical default, while the other is anticipated to undergo a 35% write-down.

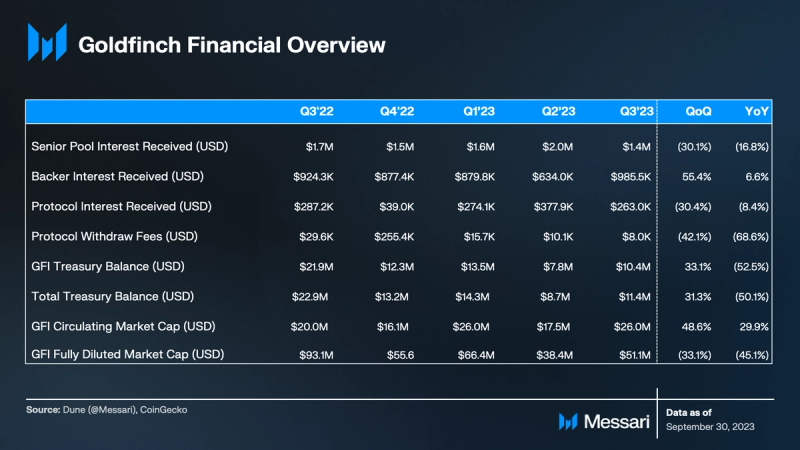

The first setback occurred in July with a $5 million loan extended in 2021 to Tugende Kenya, a motorcycle taxi financing enterprise. Since this loan was originated before the introduction of tranched pools, it was entirely funded by the Senior Pool capital. The initial fallout was a 3.95% reduction in the NAV of the Senior Pool. However, in September, Warbler Labs disclosed that Tugende had agreed in principle to a confidential restructuring plan, potentially reducing the Senior Pool’s NAV write-down from 3.95% to just 0.79%.

Further bolstering the situation, the community approved GIP-52, leading to an allocation of $1 million from the Goldfinch treasury to mitigate a portion of the loan. To date, $825,000 of this allocation has been executed. As a result of this action, the NAV of the Senior Pool’s FIDU shares saw an uplift of 4.5%, rising from $1.14 to $1.19.

Another challenge arose on October 7 when Warbler Labs shared an update of a likely $7 million write-down on a $20 million loan granted the previous year to Stratos, a U.S.-based credit fund. Stratos had diversified this loan into three investments: $13 million in Threecolts, $5 million in REZI, and $2 million in POKT. REZI, operating in the real-estate tech sector, ceased its interest payments, while the investment in POKT, associated with the Pocket Network, was nearly a total loss. Notably, Warbler Labs stated intentions to cover all losses related to these investments for the Senior Pool and Backers.

The Goldfinch community’s decisions to backstop these losses underscore tits commitment to minimizing LPs’ losses. Beyond that, these events highlight the inherent risks of tokenizing real-world assets (RWA). This is especially true for private credit in regions that lack comprehensive credit scoring systems or where traditional financial safeguards are absent.

Despite these challenges, Goldfinch remains forward-looking and recognizes the transformative potential of tokenized real-world assets, which allow for efficiency, transparency, and cost-effectiveness that surpass legacy systems. Taking proactive steps to shape the industry’s future, Goldfinch joined hands with industry leaders like Circle, RWA.xyz, Coinbase, Aave, and Centrifuge to form the Tokenized Asset Coalition. Through its focus on development, education, and advocacy, the coalition is dedicated to advancing the pivotal onchain infrastructure. Doing so ensures that Goldfinch aligns with the evolving needs of all stakeholders in the tokenized RWA ecosystem.

Goldfinch Blueprint: A New Private Credit Operating System

The current financial landscape is characterized by high inflation, escalating interest rates, and tighter credit conditions. As maturities come due and traditional financing avenues become less accessible, borrowers, both new and seasoned, are compelled to explore alternative lending solutions.

For private credit investors, this evolving landscape presents a dual opportunity. Firstly, traditional bank financing has been pulling back over the past decade due to regulations that place capital constraints on large banks. Post-SVB crisis, similar regulations have been proposed in Congress for regional banks. These regulatory changes open the door for private credit providers as a form of “capital of last resort.” Moreover, the outflow of deposits from said regional banks creates a dearth of supply in the financing market.

Secondly, from the demand side, the retreat of the collateralized loan obligations (CLO) market — traditionally the largest issuer of such debt — has led to private lenders refinancing debt more frequently. Recent months have witnessed over $10 billion in private credit refinancings, as highlighted by Bloomberg. Notable deals include those for companies like Cole Haan, Hyland Software, and Finastra, which secured the largest private debt deal ever at $5.3 billion. Adding to this momentum, Blackstone is actively seeking to raise over $10 billion across two private credit funds.

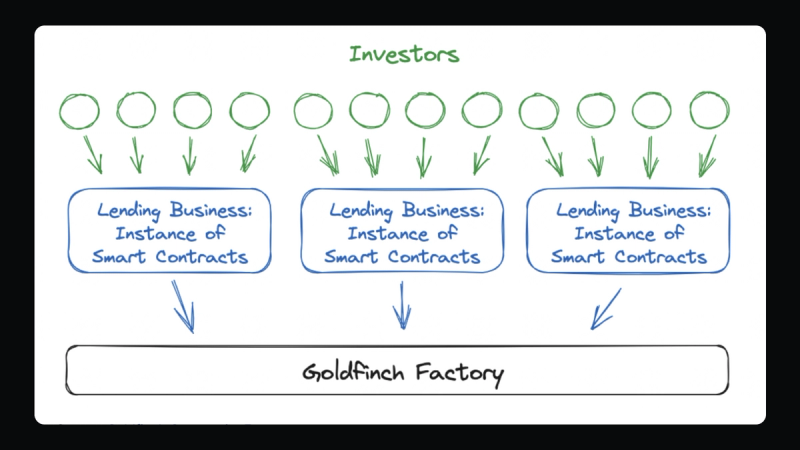

Warbler Labs, recognizing the shifting tides, recently rolled out an ambitious blueprint for Goldfinch. The primary goal is to harness the platform’s robust smart contract foundation to better cater to investors’ growing appetite for the expansive $1.4 trillion global private credit market. The strategy is threefold and aims to transform Goldfinch into a trusted lending “operating system” that supports a multitude of centralized, branded lending businesses — all built upon a unified decentralized infrastructure.

Source: Goldfinch Community Forum

Warbler Labs intends to pioneer this transformation by launching its own lending business on the Goldfinch protocol, a unique robo-advisor focused exclusively on private credit transactions. Platforms that allow retail investors to invest in private credit are rare, and automated rebalancing of a private credit portfolio does not currently exist. However, Warbler Labs is already in the process of securing regulatory approval from the SEC to be recognized as an “internet advisor.” This new venture promises direct-to-consumer private credit solutions, automated rebalancing (meaning all investors need to do is fund their Goldfinch account and select a strategy–Warbler does the rest), and a dedicated Warbler credit team overseeing deal sourcing and monitoring. While doing all of this, Warbler stays true to the transparent and self-custody principles of DeFi by leveraging the simplified account management infrastructure highlighted in the “DeFi For The World” initiative.

The next phase is about expansion and attracting other lending businesses to the Goldfinch platform. Recognizing that many lending businesses operate on tight margins, the proposed approach involves a shift in the fee structure to one that doesn’t directly erode these margins. Instead of the traditional protocol interest fee, individual lending businesses would have control over an underwriting fee and an AUM fee, akin to those charged by private equity firms. To make Goldfinch a more attractive proposition, the new structure is designed to provide a compelling, cost-saving infrastructure. To ensure the protocol’s revenue stream remains balanced, a “fee switch” has been proposed. This would channel a portion of these fees back to the Goldfinch treasury. As a strategic move to incentivize early businesses, this fee would initially be set to zero, allowing them to build on the platform without immediate costs. Once a robust network is established, the community has the potential to introduce fees.

The vision culminates in the creation of a vibrant ecosystem of onchain lenders. By tapping into the collective expertise of the Goldfinch community in marketing, origination, and tool development, the aim is to establish a vast, interoperable network of loans across various industries and lending entities, all unified under the Goldfinch standard.

Closing Summary

Goldfinch’s journey this year has been marked by both innovation and formidable challenges. The “DeFi For The World” initiative stands as a testament to the protocol’s dedication to democratizing digital asset management, with a focus on simplifying the user experience. Yet, financial hurdles emerged. With a single loan origination, Goldfinch experienced the onset of its first-ever credit events including a technical default and an impending write-down. The community’s swift responses, underscored by the treasury’s allocation and Warbler Labs’ pledge to backstop losses, showed the resilience and adaptability of the Goldfinch community.

The gap between the FIDU NAV and its price on CURVE widened, expanding from 15% in Q1 to 34% in Q3. The resulting FIDU market discount could attract more long-term investors willing to navigate the associated risks.

Furthermore, Warbler Labs’ visionary blueprint for Goldfinch aims to reshape the protocol into a decentralized lending operating system, catering to the vast global private credit market. As a pioneer in tokenized private credit, Goldfinch is not only primed to enhance its future strategies, but it also stands as a seminal case study for the broader RWA sector.