(Any views expressed in the below are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.)

All day, I dream about powder. Whiteout blizzard conditions are preferred. My favourite days are when the grey clouds blanket the mountain depositing a never-ending stream of fat flakes of dry crisp champagne powder. I know that even while I am fortunate enough to shred freshies, in a few hours, the fields will be replenished, and my snorkel session will begin anew.

To gain sight and perspective, I seek refuge in the trees. Bare birch and pine trees dot the glade. Within this wooded white paradise I can finally see the contours of the snow and read my line clearly.

While trees give me sight during the daily Hokkaido blizzard, central bankers and politicians provide sight whilst I navigate the global capital markets. While no trader can predict the future, we can observe the decision tree facing our clueless overloads and assign probabilities to each outcome. If the probability the market assigns to an event is at odds with our own calculation, a trading opportunity is at hand.

The crypto bull market is in its early stages, and we must not get carried away with our enthusiasm. As sure as Bitcoin blocks are produced every 10 minutes, the current filthy fiat financial system will meet its preordained inglorious end. However certain I am about this eventual outcome, the path to said future is unknown. We must stay vigilant and place our chips accordingly.

Simply put, I have deployed enough capital, meaning sold fiat and bought crypto, for this stage of the cycle. I am preparing for a vicious washout of all the crypto tourists in March of this year. There are various signposts that give me this vision of the future. I shall lay out my reasoning and the inflection points I will observe that will provide me with the confidence to first short the crypto market in big size using Bitcoin puts and then resume selling US Treasury bills (T-bills) and acquiring more Bitcoin and other cryptos.

The Variables

There are three variables, in the form of questions, that collide with each other in March.

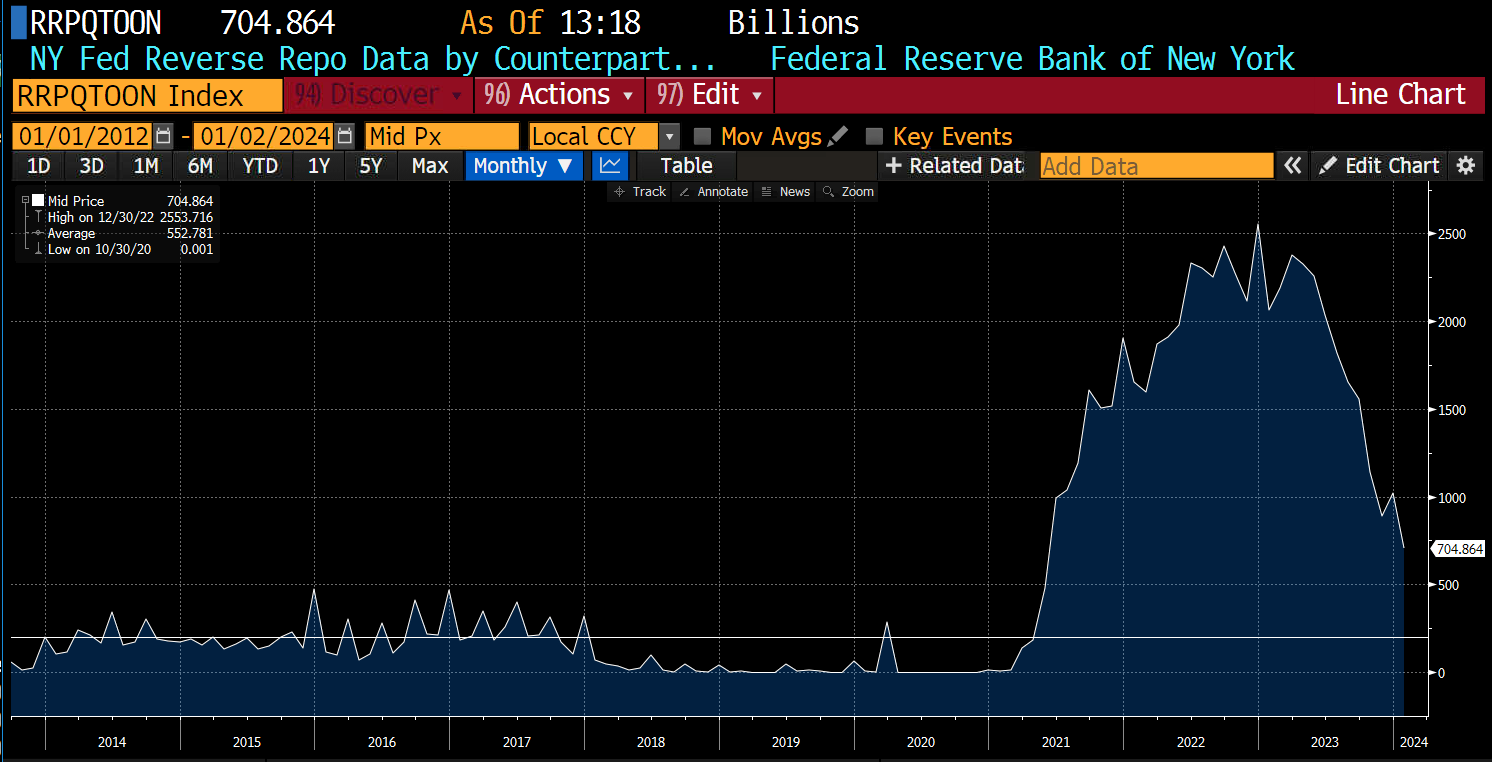

When Will the Reverse Repo Program (RRP) Balance Decline Close to Zero?

Liquidity is being pumped into the system via a decline in the RRP balance. When this number gets close to zero, and I define that as a balance of $200 billion, the market will wonder what is next. There needs to be another source of dollar liquidity supplied to keep the party going.

To understand more about the mechanics of how a declining RRP balance injects liquidity into the system, please read my essay “Bad Gurl”.

This is a chart of the RRP balance for its entire history. The horizontal white line is at $200 billion.

I believe the RRP balance will hit $200 billion in early March. I arrived at this guestimate based on a calculation of the rate of decline in 2023 from a few different starting points.

|

Start Date |

RRP Balance (bn) |

End Date |

RRP Balance (bn) |

Decline Per Day (bn) |

Date to $200 bn |

Notes |

|

6/5/2023 |

$2,131.42 |

12/22/23 |

$772.26 |

$6.80 |

3/15/24 |

Government budget passed, Yellen resumes borrowing |

|

10/31/23 |

$1,137.70 |

12/22/23 |

$772.26 |

$7.03 |

3/12/24 |

Yellen shifts more borrowing into T-bills |

|

9/30/23 |

$1,557.57 |

12/22/23 |

$772.26 |

$9.46 |

2/20/24 |

Start of Q3 |

Will the Bank Term Funding Program (BTFP) Be Renewed?

On March 12th, the broke banks must find the cash to swap with the US Treasuries and other eligible bonds they repo’d with the Fed. Ultimately, this is a call for Bad Gurl Yellen. The market will start getting inquisitive many weeks before about whether or not the banks will continue receiving this lifeline.

The initial BTFP flow was that the banks gave a US Treasury bond that was worth $80 for example, on the open market, but received $100 of cash. When the program finishes, the bank must give back the $100 to then receive the original US Treasury bond. If the cash was given to a fleeing depositor, then absent selling more of its equity or issuing very high-yielding bonds, how will the bank get the cash?

To understand why the BTFP was created and its implications for the pace and amount of fiat debasement, please read my essay “Kaiseki”

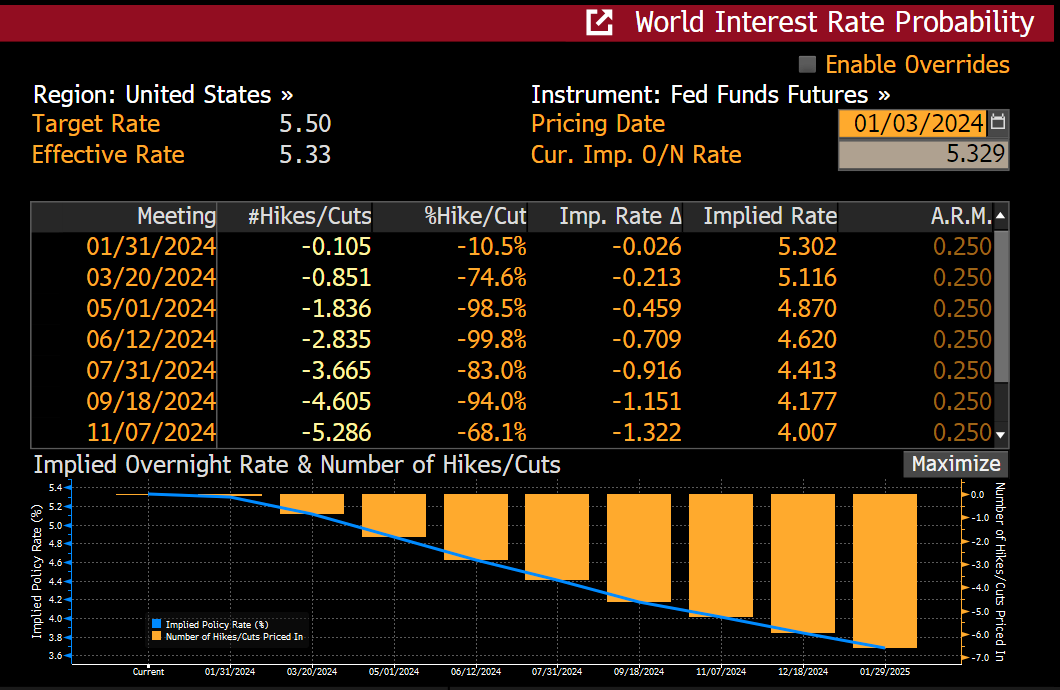

Will the Fed Cut Rates?

The Fed’s March meeting concludes on the 20th of the month. Currently, the market expects the Fed to initiate its first rate cut of at least 0.25% since it started raising rates in March of 2021.

This is a table of Fed Fund Futures implied probability of rate hike at future Fed meetings. As you can see, as of January 3rd, the market is pricing in a 75% chance of a 0.25% rate cut.

These variables are codependent. The sequencing of events matters because it will affect the market’s assumption for the future of how much dollar liquidity will or will not be provided by the Fed and US Treasury Department.

If .. Then

Now we must assign probabilities to the different paths and anticipate the market’s reaction.

Pace of RRP Decline

If the RRP is run down close to zero by early March, the financial markets will start sagging. Remember the surge in US Treasury yields that occurred simultaneously with a dumping stock market? The only reason bonds had such an amazing rally starting from November 1st is the quarterly Treasury refunding documents were published that day. Included inside this now must-read report, was a confirmation that the US Treasury would shift more borrowing to the short end of the yield curve. With more supply and higher yields on T-bills, money market funds (MMF) would be financially incentivised to use cash parked in the RRP to purchase T-bills. The decline in the RRP balance all else being equal adds liquidity to the system; this is what we have witnessed to date and is why the bond and stock markets globally pumped.

The white line is the 10-yr treasury, and the yellow line is the difference between the 10-yr and 2-yr treasury yield. As you can see, yields peaked at the end of October in a bear-steepening fashion, meaning the white and yellow line rose in tandem. The beginning of November kicked off a vicious bond short squeeze, and yields plummeted.

Without any other new sources of dollar liquidity, bonds, stocks, and I believe crypto will also get the stick. I will expand upon this later in the tactical trading section, but I will look to buy a sizable put option position on Bitcoin around this time.

We can’t know the pace of RRP decline if at all, a priori. Therefore, I will watch the rate of change quite closely. I will adjust my trading strategy accordingly if it deviates materially from my forecast. In any case, I loaded up on crypto in the second half of 2023, and I believe now until April is a no-trade zone in terms of the addition of risk.

BTFP

2024 is an election year, and the plebes of Pax Americana are sick and tired of bankster bailouts. Therefore, I believe Yellen, to project an air of confidence in the strength of the American banking system, will not renew the BTFP. However, once a few sufficiently large non-TBTF banks are forced into receivership because their equity falls close to zero, wiping out necessary regulatory capital, Bad Gurl Yellen will hang up her stilettos and put on her knitted slippers, thus transforming into Grandma Yellen. Grandma Yellen will hand out the sweet, sweet sugar of printed money to her wayward banking grandchildren in the form of a renewed BTFP.

The combination of a lack of liquidity gushing from the RRP and the lack of printed money to cover the bond losses on the non-TBTF banks’ balance sheets will decimate the financial markets globally. The market must bring pain upon financial asset holders to force the Fed and Treasury back into the business of printing money. This is a correlation one moment. All assets, including crypto, will fall together as the market hyperventilates at the prospect of the free market working once more and cleansing the system of insolvent banking institutions.

March FOMC Meeting

The BTFP expires on March 12th, and the Fed rate decision is announced on March 20th. There are six trading days between these two crucial decision points. If my forecast is correct, the market will bankrupt a few banks within that period, forcing the Fed into cutting rates and announcing the resumption of the BTFP.

Technically, the US Treasury cannot lend money to banks; that’s the job of the Fed. But suppose the Fed loses money by accepting collateral worth less than the dollars provided. In that case, those losses flow through to the Treasury, and ultimately, the American taxpayer as the Treasury must borrow more to fund losses at the Fed.

Bitcoin initially will decline sharply with the broader financial markets but will rebound before the Fed meeting. That is because Bitcoin is the only neutral reserve hard currency that is not a liability of the banking system and is traded globally. Bitcoin knows that the Fed ALWAYS responds with a liquidity injection when things get bad. It might be called something new to confuse those who get their news from TikTok, but rest assured Bitcoin knows printed money in whatever guise is always printed money. Therefore Bitcoin will rise sharply before and into the Fed’s eventual capitulation to restarting money printer go brrr.

The Other Side

If I’m wrong, the following magic will occur:

- The RRP will decline slowly, and that liquidity will continue to prop up the financial markets late into the second quarter.

- Yellen will communicate that the BTFP will be extended well before March 12th.

- The Fed’s March meeting decision then becomes irrelevant. Whether they cut, hold, or raise, the net effect based on any of those outcomes, combined with all the other ways in which the Fed and Treasury are adding dollar liquidity to the market, remains stimulative.

If the RRP rate of decline is slower than anticipated, I will not put on my put position at the beginning of March. Then, the date Yellen communicates that the BTFP will be renewed, is when I exit the no-trade zone. I will resume selling T-bills for Bitcoin and other cryptos.

Tactical Trading Decisions

Let’s move back to my base case of RRP exhaustion by early March, the BTFP being cancelled on the 12th only to be reinstated by the 20th, and a Fed rate cut. Now I will expand a bit on my trading plan.

Bitcoin Puts

As many of you know, I have a diverse crypto portfolio. My biggest positions are Bitcoin and Ether, representing ~70% of my portfolio. The other shitcoins I own are much less liquid, and in particular, the liquidity of the derivatives on these shitcoins is poor. Therefore, if I want a liquid macro crypto hedge, I must use Bitcoin derivatives. I use the word “hedge”; but this is a trading position. The trade setup I’m describing will take only a fortnight to resolve itself. Because this is a trade I will use options which allows me to know a priori my maximum loss; the premium paid for my puts. A bonus feature is I don’t have to monitor liquidation levels like I would if I traded a perpetual swap or futures contract.

I expect Bitcoin to experience a healthy 20% to 30% correction from whatever level it has attained by early March. The washout could be even more severe if the slate of US-listed spot Bitcoin ETFs has already commenced trading. Imagine if the anticipation of hundreds of billions of fiat flowing into these ETFs at a future date propels Bitcoin above $60,000 and close to its 2021 all-time high of $70,000. I could easily see a 30% to 40% correction due to a dollar liquidity rug pull. This is why I cannot buy Bitcoin until these March decision dates have passed.

I think I’m a decent trader when I’m focused. I will attempt to top-tick the market in late February and then buy a sizable put position. I will buy puts expiring on June 28th. I don’t want the March 29th expiry because I’m entering the position in early March. The high negative theta might overwhelm any delta, gamma, and vega P&L. The longer expiry will be more expensive, but the premium won’t decay as fast because maturity is over a quarter out.

I’ll set my maximum loss, which will be sizable relative to my standard trading position, and then purchase the puts. To get some juicy gearing on these puts, I will choose a strike 20% to 25% out of the money based on the current at-the-money quarterly June futures contract price.

Exiting the Position

Many traders, especially options traders, nail the entry but fumble the exit. Because option payouts are path-dependent, you might call the market right but still lose money if you wait too long to close your position. Every day I hold these puts, I lose money. If my forecasts are correct, the market will start meaningfully correcting around March 12th. Between the 12th and the 20th, I need to attempt to bottom-tick the market and close out my position hopefully in profit. If I get the policy call right, but Bitcoin holds or rises, I must close my put position immediately.

Bull Market Continues

By the end of March, we will be back on schedule. Bad Gurl Yellen and her duck Powell will once again have confirmed there is nothing they won’t do to safeguard the fiat solvency of the Pax Americana financial system. With that brief bit of market turmoil out of the way, crypto can again gush higher amid speculation as to the effect of the impending Bitcoin block reward halving. As such, I shall resume selling T-bills for Bitcoin and other cryptos.

Curve Balls

This essay has focused entirely on the decisions of the two people who run the Pax Americana financial system. All that “democracy” and things are still run by two unelected bureaucrats. In any case, there are other crucial actors in the fiat financial system kabuki theatre.

China

The Taiwan elections could result in one of the pro-China candidates winning, and then Xi Jinping turns on the yuan money printing taps. The gusher of yuan credit into the global markets overwhelms any US banking system troubles, resulting in crypto continuing to march higher even if the RRP runs dry and the BTFP is not renewed. The trading setup then becomes a lot less appealing in terms of risk vs. reward, and I might choose not to buy any puts but switch to buying more crypto risk.

Japan

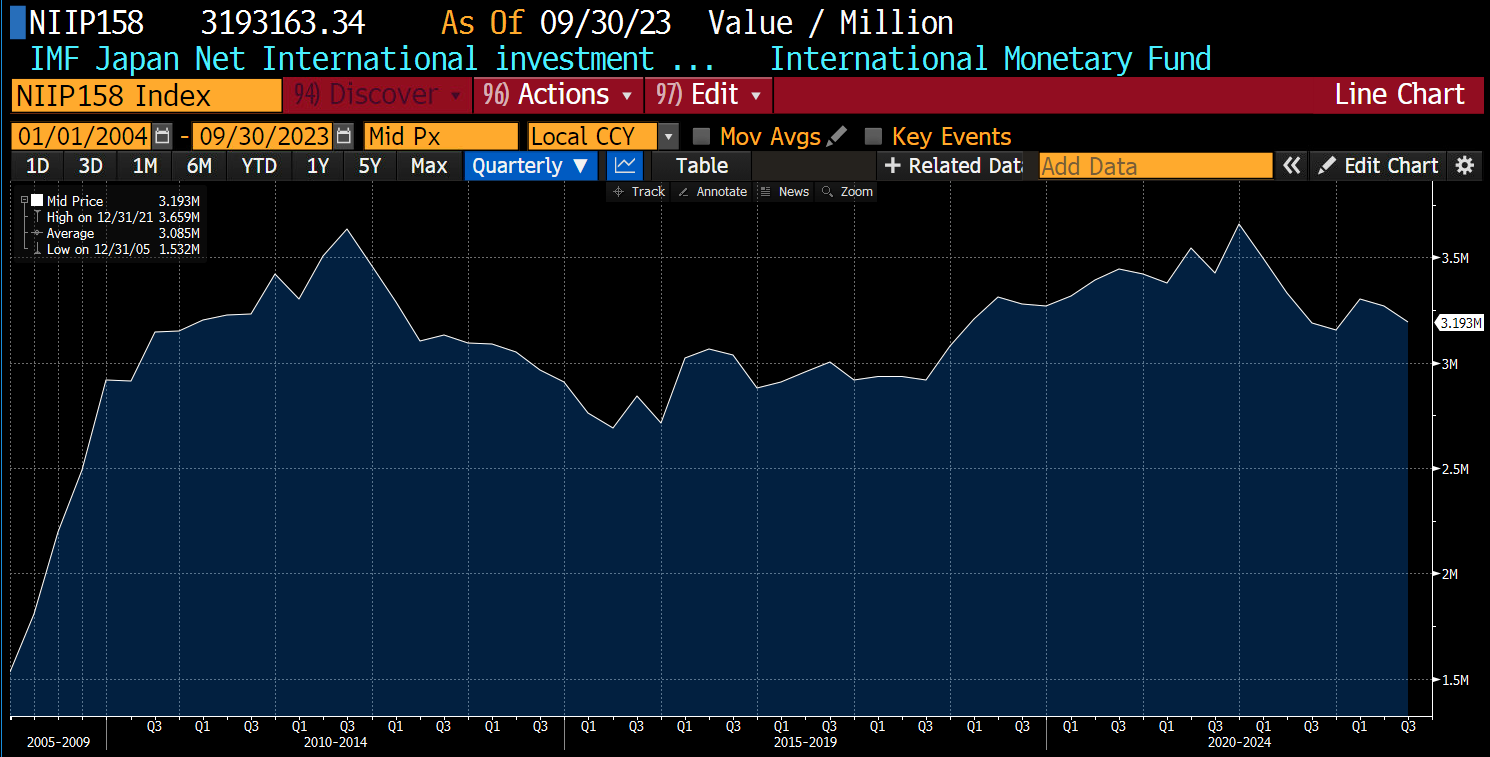

The Bank of Japan (BOJ) is in the process of slowly allowing Japanese Government Bond (JGB) yields to rise. If JGB yields continue rising, it financially incentivises Japanese corporates, pension and insurance funds, and households to repatriate capital. They will sell US Treasuries and buy JGB’s because the yields onshore are better. If this trend picks up steam, I will definitely bless you readers with an essay describing the phenomenon in more detail. Given that Japan is the largest holder of US Treasury bonds and the largest international creditor as viewed by its net international investment position, actions of the Japanese private sector could place enormous upward pressure on 10-year plus maturity US Treasury bond yields.

This is data from the IMF which estimates Japan’s net international investment position is a positive $3.3 trillion.

This pressure could mount well before early March and necessitate more money-printing measures from Bad Gurl Yellen. If that is the case, I might not even get the chance to put this trade on because well before mid-March Yellen has already renewed the BTFP and rolled out some newfangled way to print money without calling it printing money. One candidate is the nascent plan by the US Treasury to buy off-the-run long-dated US Treasuries by issuing more short-dated bills. This is a soft version of yield curve control, which she called the buyback program. There was an explanatory paper written about this last year, I have linked it here if you wish to peruse it.

Downside Risks

With a new year, printed money gushing in various forms from every central bank, and the expected US-listed and Hong Kong-listed spot Bitcoin ETFs, the risks are on the downside. It is not hard to be bullish right now. I like to buy things that do well when situations the market believes never can happen are then viewed as possibly happening. The risk-reward from a trading perspective, using these signposts representing binary outcomes to take a non-consensus view, is better. I may ultimately be wrong. But if I’m right on an expected value basis, my profit is much greater than going with the herd.

The post Signposts appeared first on BitMEX Blog.

{kind=link}