Image credit to X user @CryptoTubeYT, I added the text.

(Any views expressed in the below are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.)

The last moments of life are the most expensive from a healthcare perspective. We are willing to spend infinite money on any treatment advertised to forestall the inevitable. Similarly, the elites in charge of Pax Americana and her vassals are willing to do whatever it takes to preserve the current world order because they have benefited the most from its existence. But ever since 2008, when dodgy mortgage loans made to broke-ass Americans caused a global economic crisis so severe it harkened back to the 1930’s Great Depression, Pax Americana has been on her deathbed. What was the medicine the mediaeval neo-Keynesian barbers – blindly led by Ben Bernanke – prescribed? The same rudimentary cure that is always prescribed to a dying empire … money printer go brrr.

The empire and her European, Chinese, and Japanese vassals, strategic competitors, and allies printed money to solve different symptoms of the same rot. The rot being a global economic and political architecture that is grossly unbalanced. America, led by the Federal Reserve (Fed), printed money and bought US government bonds and mortgages. Europe, led by the European Central Bank (ECB), printed money and bought Euro member government bonds to keep the flawed monetary – but not fiscal – union alive. China, led by the People’s Bank of China (PBOC), demanded the banking system hand out loans to industrial firms that overbuilt apartments, steel mills, and other large infrastructure projects. China built so much useless capacity that it created the Belt and Road Initiative to export this production to the developing world, which desperately needed capital investment. Japan, led by the Bank of Japan (BOJ), continued printing money in its quest to create the illusive inflation that departed after the 1989 property crash.

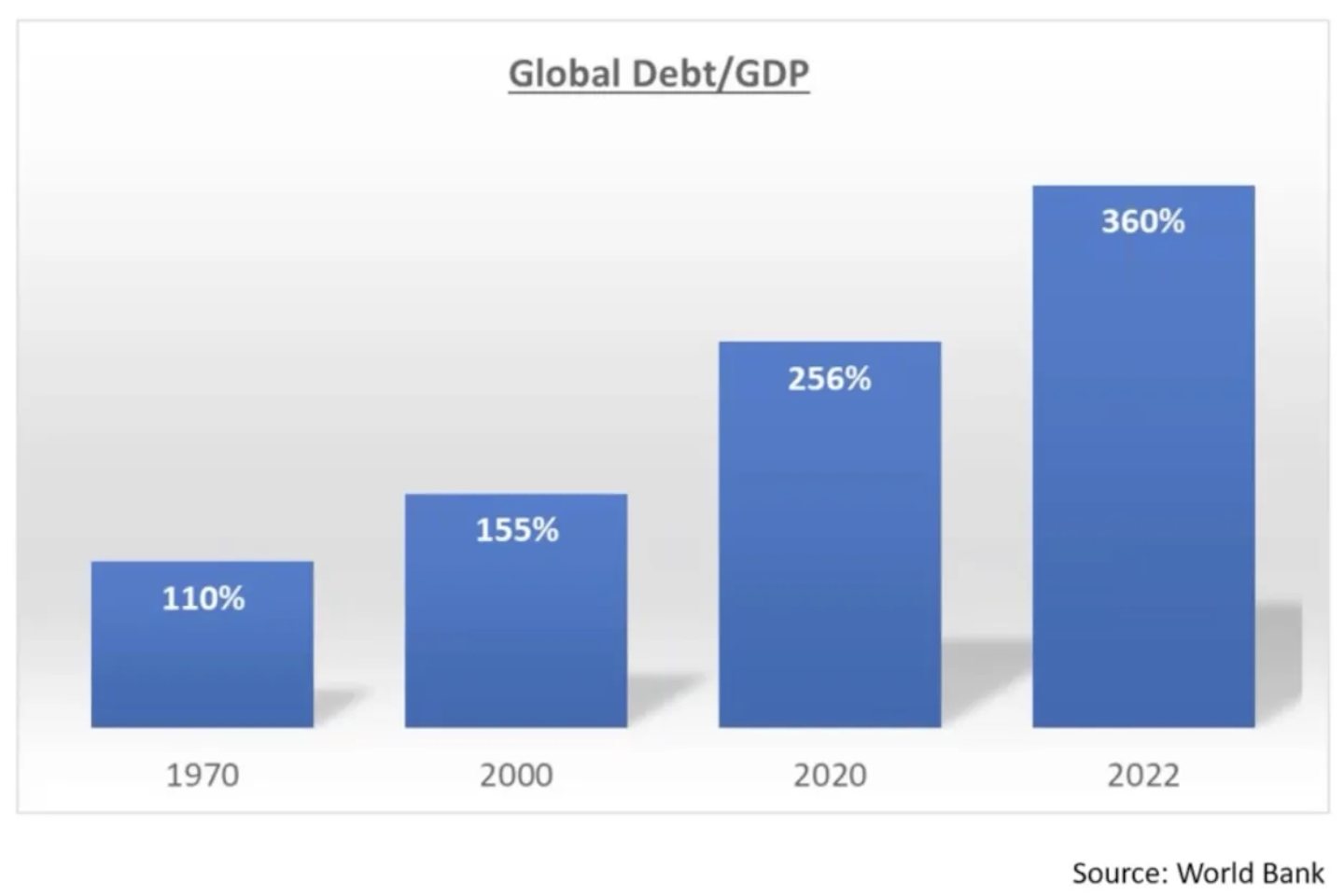

The result of this wanton money printing was an acceleration of global debt-to-GDP. Interest rates globally hit their lowest levels in 5,000 years. Almost $20 trillion of corporate and government bonds featured a negative yield at its height. As interest is compensation for the time value of money, if interest is negative, are we saying time is no longer valuable?

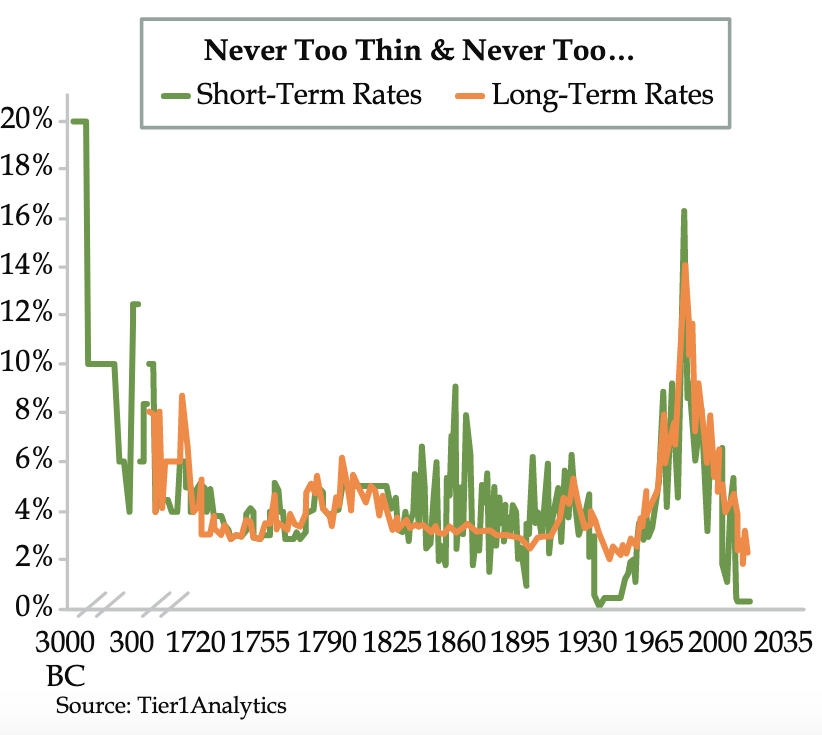

Thank you Danielle DiMartino Booth at Quill Intelligence for this chart. As you can see in response to the 2008 Global Financial Crisis (GFC) rates were pushed to their 5,000 year nadir.

This is a Bloomberg index of the total amount of globally negatively yielding debt. From nothing pre-2008 GFC, it reached a high of $17.76 trillion in 2020. This was made possible by central banks globally cutting rates to 0% and below.

Most of the world’s population doesn’t own enough financial assets to benefit from this global fiat monetary debasement. Inflation in various goods in various places sprung up around the world. Remember the Arab Spring of 2011? Remember when an avocado toast cost less than $20 in every major global financial centre? Remember when a family with a median income could afford a house at the median price level without resorting to handouts from the bank of mom and dad?

The only kind-of way out was to own a bit of gold. But gold is impracticable to own physically. It is heavy and hard to hide from rapacious governments in large amounts. As a result, the people just ate their humble pie so that the elites could continue partying in Davos like it’s 2007.

But like a lotus that blooms in a pond of dung, Lord Satoshi published the Bitcoin Whitepaper while wallowing in a morally, politically, and economically bankrupt empire. The whitepaper laid out a system whereby the people could use internet-connected machines and cryptographic proofs to separate money from the state in a globally scalable fashion for the first time in human history. I say “globally scalable” because Bitcoin is weightless. Whether you hodl 1 Satoshi or 1 million Bitcoin, the weight is the same amount of nothing. Furthermore, you can secure your Bitcoin using just your mind by remembering a mnemonic phrase that unlocks your Bitcoin wallet. Bitcoin offers everyone a fully complete financial system with an internet-connected device not attached to the ancient regime.

The people finally had a way to escape the global fiat debasement jamboree. However, Bitcoin was too immature to offer a credible escape valve for the faithful in the aftermath of the 2008 Great Financial Crisis. Bitcoin, and the crypto markets in general, had to grow in the number of users and prove that they could weather a severe crisis.

We, the faithful, received our crucible in 2022. The Fed, followed by most central banks globally, embarked on a journey to tighten financial conditions at the fastest pace since the 1980s. Pax Americana’s banking system and debt markets could not withstand the Fed’s onslaught. In March 2023, three US banks (Silvergate, Silicon Valley Bank, and Signature Bank) failed within a fortnight of each other. The US banking system was and still is insolvent if their US Treasury debt and mortgage-backed securities holdings were/are marked to market. As a result, US Treasury Secretary Bad Gurl Yellen created the Bank Term Funding Program (BTFP) as a stealthy way to bail out the entire US banking system.

Crypto was not immune from disturbances caused by high and rising interest rates. Centralised lenders such as BlockFi, Celsius, and Genesis all went bankrupt as loans to over-leveraged trading firms like Three Arrows Capital went bye-bye, birdie. Terra Luna, a USD-pegged stablecoin, also went bust due to the fall in the price of Luna, its governance token, which backed issued UST stablecoins. This event wiped out over $40 billion in fugazi value within two days. Then centralised exchanges started going under, of which FTX was the largest. FTX, run by the “right” kind of Pax Americana white boy Sam Bankman-Fried, stole over $10 billion worth of customer money, and his caper was revealed as crypto asset prices plummeted.

What happened to Bitcoin, Ethereum, and DeFi projects such as Uniswap, Compound, Aave, GMX, dYdX, etc.? Did they falter? Did they phone home and get a bailout from the central bank of crypto? Absolutely not. Over-leveraged positions were liquidated. Prices fell. People lost a lot of money. Centralised companies ceased to exist. But Bitcoin blocks were still produced every 10 minutes on average. DeFi platforms did not go bankrupt themselves. In short, there was no bailout because crypto cannot be bailed out. And we took our knocks but kept on truckin’.

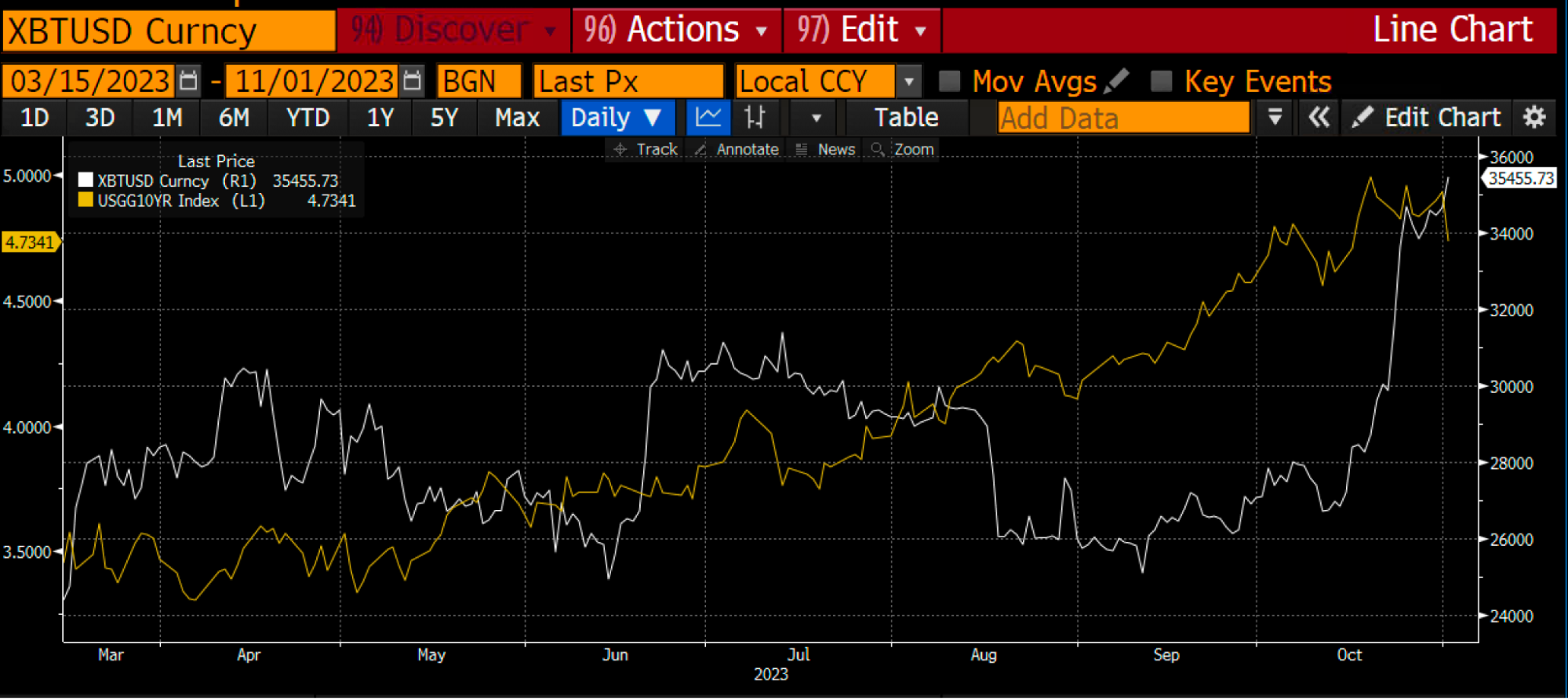

Out of the ashes in 2023, it became clear that Pax Americana and her vassals could not continue tightening monetary policy. To do so would bankrupt the entire system, as the leverage and debt pile is too high. A curious thing occurred as long-end US Treasury yields began stair-stepping higher. Bitcoin and crypto rallied whilst bond prices fell.

Bitcoin (white) vs. US 10-yr Treasury Yield (yellow)

As you can see in the above chart, Bitcoin acted like all other long duration assets when interest rates rise … it fell.

After the BTFP, the relationship flipped. Bitcoin rose alongside yields. Rising yields, particularly rising yields in a bear-steepening fashion, indicate that investors do not believe in the “system”. In response, they are dumping the safest government bonds in the empire, US Treasury bonds. This capital mainly fled to the Magnificent 7 AI tech stocks (Apple, Alphabet, Microsoft, Amazon, Meta, Tesla, Nvidia) and to a small degree, crypto. After almost 15 years, Bitcoin finally displayed its true colours as the “money of the people” and not just another risky asset derivative of the empire. This has created a very problematic issue for TradFi.

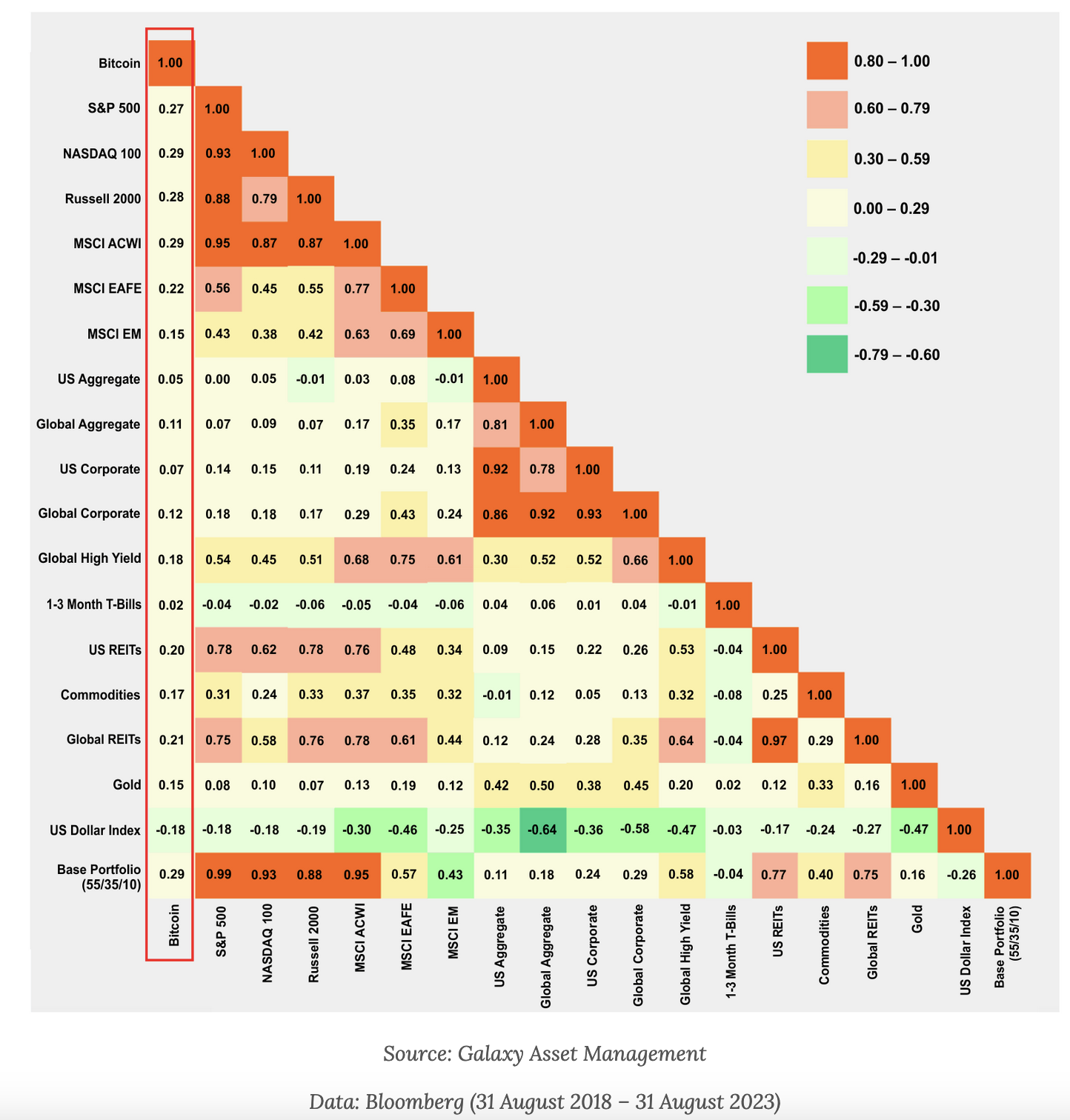

Capital must stay within the system to inflate away the vast pile of unproductive debt. Bitcoin is outside the system and now exhibits zero to a slightly negative correlation with bonds (remember, bond prices fall when yields rise). The global financial system collapses if bond vigilantes express their dismay with government bonds by selling them and purchasing Bitcoin and other cryptos. It collapses because the inherent losses being nursed within the system are finally recognised, and large financial firms and governments will have to reduce in size radically.

To avoid this reckoning, the elite must financialise Bitcoin by creating a highly liquid Exchange Traded Fund (ETF). This is the same trick they played on the gold market when the US Securities and Exchange Commission (SEC) approved ETFs such as SPDR GLD in 2004 that supposedly hold gold bars in vaults worldwide. If all capital wishing to flee a blowup in the global government bond markets purchases a Bitcoin ETF managed by large TradFi firms such as Blackrock, then the capital is still safely within the system.

As it became apparent that to safeguard the global bond markets, the Fed and all other major central banks must switch to money printing once more, Blackrock formally applied for a Bitcoin ETF in June of 2023. Blackrock followed a long line of firms who wished to gain approval for a Spot Bitcoin ETF in the US. However, in 2023, the US SEC finally seemed receptive to such an application. I present the following to highlight the strangeness of the current events surrounding the ETF approval process. The Winklevoss twins applied for a Spot Bitcoin ETF in 2013, and the SEC denied their application for over a decade. Blackrock applies and, within six months, gains approval. Things that make you go, “hmmmm.”

As I wrote in my last essay, “Expression”, a spot Bitcoin ETF is a trading product. You purchase it with fiat to earn more fiat. It is not Bitcoin. It is not a path to financial freedom. It is not outside of the TradFi system. If you want to escape, you must buy Bitcoin, withdraw it from the exchange, and self-custody it.

I wrote this lengthy preamble to explain “why now?” Why is the spot Bitcoin ETF finally getting approval at this critical juncture for the empire and its financial system? I hope you can appreciate the magnitude of this development. The global bond market is estimated at $133 trillion; imagine the inflows into the Bitcoin ETF if bond prices continue falling even as the Fed possibly starts cutting rates in March. Bond prices could continue falling if inflation bottoms and resumes its march higher. Just remember, war is inflationary, and the periphery of the empire is definitely at war.

Also, don’t forget that China will launch an exact copy of the US-listed ETF in the Hong Kong financial markets to capture flows within China and the Asia Pacific. Pax Americana leads, and her frenemies shall follow.

The rest of this essay will discuss the market impact of the Spot Bitcoin ETF. I will only focus on the Blackrock ETF because Blackrock is the largest asset manager in the world. They have the best ETF distribution platform globally. They can sell products to family offices, retail financial advisory firms, retirement and pension plans, sovereign wealth funds, and even central banks. All the other firms will try their best, but the Blackrock ETF will be the hands-down winner regarding assets under management (AUM). Whether this prediction is correct or not, the following strategies will work if ETF volumes of any issuer are large.

This essay will address the following and how the inner workings of the ETF will create amazing trading opportunities for those who can trade in the TradFi and crypto markets:

- The creation and redemption process

- Spot exchange arbitrage and time series analysis of trading

- ETF derivatives such as listed options

- The effect of ETF financing trades

With all of that out of the way, let’s make some fucking money!

Cash Rules Everything Around Me

It’s been settled. Money into (creation) and out of (redemption) can only happen using cash. The most feared aspect of this ETF would be allowing plebes to purchase the ETF with fiat and elect to redeem the ETF in kind for Bitcoin. The point of this product is to warehouse fiat, not to provide an easy way to buy physical Bitcoin with your retirement account.

Creation

To create shares of the ETF, authorised participants (AP) must send the USD value of the creation basket, which is a certain amount of shares of the ETF, to the fund by a certain time each day.

APs are large TradFi trading firms. A who’s-who of TradFi vampire cephalopods have signed up to be APs for various ETF issues. Firms whose CEOs called on the government to ban crypto like Jamie Dimon, CEO of JP Morgan, will be participating. Colour me surprised

Example:

Each share of the ETF is worth 0.001 BTC. The creation basket is 10,000 shares; at 4 pm EST, those Bitcoin are worth $1,000,000. The AP must wire that amount of money to the fund. The fund will then instruct its trading counterparties to purchase 10 Bitcoin. Once the Bitcoin has been purchased, the fund will credit the AP with ETF shares.

1 Basket = 0.001 BTC * 10,000 Shares = 10 BTC

10 BTC * $100,000 BTC/USD = $1,000,000

Redemption

To redeem units of the ETF, an AP must send shares of the ETF to the fund by 4 pm EST. The fund will then instruct its trading counterparties to sell 10 Bitcoin. Once the Bitcoin has been sold, the fund will credit the AP with $1,000,000.

1 Basket = 0.001 BTC * 10,000 Shares = 10 BTC

10 BTC * $100,000 BTC/USD = $1,000,000

For us traders, what we want to know is where Bitcoin must be traded. Of course, the counterparties that help the fund buy and sell Bitcoin can trade on any venue they like, but to reduce slippage, they must match the fund’s net asset value (NAV).

The NAV of the fund is based on the CF Benchmark’s 4 pm EST price of BTC/USD. The CF Benchmark receives prices between 3 – 4 pm EDT from Bitstamp, Coinbase, itBit, Kraken, Gemini, and LMAX. Any trader wishing to perfectly match NAV by taking minimal execution risk will just trade directly on all these exchanges.

Bitcoin is a global market, and price discovery happens primarily on Binance (I guess based in Abu Dhabi). Another large Asian exchange excluded from the CF Benchmark is OKX. For the first time in a long time, the Bitcoin markets will have a predictable and long-lasting arbitrage opportunity. Hopefully, billions of dollars of flow will be concentrated in an hour-long period on exchanges that are less-liquid and price followers of their larger Eastern competitors. I expect there to be juicy spot arbitrage opportunities available.

Obviously, if the ETF is wildly successful, price discovery could move from East to West. But don’t forget about Hong Kong and its copycat ETF products. Hong Kong will only allow its listed ETFs to trade on regulated exchanges in Hong Kong. Binance and OKX might service this market. But new exchanges will be spun up to service this China southbound flow.

Whatever happens in New York and Hong Kong, neither city will allow fund managers to trade Bitcoin at the best price, but they may only trade on “select” exchanges. This unnatural state of play only serves to create more market inefficiencies from which we, as arbitrageurs, can profit.

Here is an easy arbitrage example:

Days of Average Daily Volume (ADV) = (Exchange’s CF Benchmark Weight * Daily Market on Close (MOC) USD Notional) / CF Benchmark Exchange’s USD ADV

Pick the least liquid exchange of the CF Benchmark – that is, the one with the highest Days of ADV. If the pressure is on the buy side, the CF Benchmark exchange’s Bitcoin price will be higher than Binance. If the pressure is on the sell side, the CF Benchmark exchange’s Bitcoin price will be lower than Binance. Then you sell Bitcoin on the expensive exchange and buy it on the cheap exchange. You can estimate the direction of create/redeem flow by the premium or discount the ETF trades to its intraday net asset value (INAV). If the ETF is at a premium, there will be creation flow. The AP sells short the ETF expensive and creates it at NAV cheaper. If the ETF is at a discount, there will be redemption flow. The AP buys the ETF for cheap in the secondary market and redeems it at NAV, which is at a higher price.

To make this trade in a price-neutral fashion, you need to place dollars and Bitcoin on both the CF Benchmark exchanges and Binance. However, as a risk-neutral arb trader, your Bitcoin needs to be hedged. To do that, buy Bitcoin with USD and short a BitMEX Bitcoin/USD Bitcoin Margined Inverse Perpetual Swap Contract. Place some Bitcoin margin on BitMEX, and the remaining Bitcoin can be spread out on the relevant exchanges.

ETF Options

To really get the ETF casino going, we need leveraged derivatives. The zero-day options (0DTE) market in the US has exploded. Options with a one-day expiration are akin to lottery tickets, especially if you purchase them out of the money (OTM). 0DTE options are now the most traded options instrument in the US. Duh, Mofos love to gamble.

After the ETF has been listed for some time, listed options will start appearing on US exchanges. Now, the real fun begins.

It’s difficult to get 100x leverage in TradFi. They don’t have places like BitMEX that scratch the itch. But OTM options with short expiries have very low premiums which creates high gearing or leverage. To understand why, please brush up on your theoretical options pricing knowledge by studying Black-Scholes, for example.

Degen traders with brokerage accounts that can trade on US options exchanges will now have a liquid way to place highly leveraged bets on the price of Bitcoin. The underlying of these options will be the ETF.

Here is a simple example.

ETF = 0.001 BTC per Share

BTC/USD = $100,000

ETF share price = $100

You believe that by the end of the week, the price of Bitcoin will go up 25%, so you purchase a $125 strike call option. The option is OTM because the current ETF price is 25% below the current strike price. The volatility is high but not extremely high, so the premium is relatively low, $1. The most you can lose is $1, and if the option goes in the money very quickly (above $125), you could make much more in terms of the change in the options premium than the 25% you would have made if you just bought and sold the ETF shares themselves. This is a very rough way to explain gearing.

The degens in the US capital markets are a serious bunch. With these new highly leveraged ETF options products, they are going to fuck some shit up with regards to the implied volatility and forward-term structure of Bitcoin.

Forward Arbitrage

Call – Put = Long Forward

As ETF options prices get bid up due to lottery ticket buyers, the at-the-money (ATM) forward will rise in price. The opportunity this presents is open to arbitrage between Bitcoin/USD perps on exchanges like BitMEX and the ATM forward derived from ETF options prices.

Futures Basis = Futures Price – Spot Price

I expect the ETF ATM forward basis to trade more expensively than BitMEX futures’ basis. Here is how you trade it.

Go short the ETF ATM forward by selling an ATM call and buying an ATM put.

Go long the BitMEX Bitcoin/USD fixed expiry futures contract of a similar expiry date.

Wait for the prices to converge near expiry. This won’t be a perfect arbitrage as BitMEX and the ETF use different exchange prices to construct the spot index price of Bitcoin.

Volatility (Vol) Arbitrage

To a large extent, when you trade options, you are trading vol. The types of ETF options traders and their preference for maturities and strikes are different from those who currently trade Bitcoin options on crypto native non-US exchanges. I predict the volume of ETF options trading to dominate global flows of Bitcoin options. Because the two pools of traders, US-based and non-USD based, cannot interact on the same exchanges, arbitrage opportunities will emerge.

Direct arbitrage opportunities will exist where options with the same maturity and strike trade at different prices. There will also be more general vol arbitrage opportunities where parts of the ETF options vol surface differ significantly from the Bitcoin vol surface outside of the US. It takes a bit more trading sophistication to spot and capitalise on these opportunities, but I know there will be a lot of French degens licking their lips to arb the fuck out of these markets.

MOC Flows

Because the ETF will cause US-listed ETF derivatives volumes to surge, the 4pm print of the CF Benchmark index will become very important. A derivative derives its value from the underlying. With soon-to-be billions of notional of options and futures expiring daily vs. the ETF’s closing traded price, matching the NAV is essential.

This will create statistically significant trading behaviour on and around 4 pm EST vs. the rest of the trading day. Those of you who are good with datasets and have good trading bots will earn yuge monies arbitraging these market inefficiencies.

ETF Financing

Centralised lending platforms like Blockfi, Celsius, and Genesis were very popular with Bitcoin HODLers who wanted to borrow fiat collateralised with their Bitcoin. Alas, the dream of an end-to-end Bitcoin economy has not yet been realised. The faithful still need fiat to pay for life’s essentials using filthy fiat.

All of the centralised lenders I just mentioned blew up alongside many others. It is harder and more expensive to borrow fiat with Bitcoin collateral. TradFi is very used to lending against liquid ETFs. Getting competitively priced fiat loans in large size will now be possible as long as you pledge Bitcoin ETF shares. The problem for those who believe in financial freedom is maintaining control of one’s Bitcoin and taking advantage of this cheaper capital.

The solution to this problem is a Bitcoin for ETF swap. Here is how it will work.

APs who can borrow in the interbank market will create ETF shares and hedge out the Bitcoin/USD price risk. This is the create-to-lend business. In delta-one speak, it’s the repo value of the ETF shares.

Here is the flow:

- Borrow USD in the interbank market and cash created shares of the ETF.

- Sell an ATM call and buy an ATM put on the ETF to create a short synthetic forward.

- The act of creating ETF units creates positive carry as the Forward Basis > Interbank USD Rate.

- Lend out ETF shares in exchange for Bitcoin collateral.

Let’s bring in Chad and talk about what he needs to do with his Bitcoin.

Chad is a HODLer with 10 BTC who needs to pay his AMEX bill in USD. Those bottles of bubbly are fucking criminally expensive at the club. Chad hits up his boy Jerome, a slippery Frenchman at SocGen who used to be a prime finance middle office muppet, did some time for aggressive futures trading, but got his job back (you can’t fire anybody in France), and is now running the crypto trading desk. Chad asks Jerome for a BTC vs. ETF swap for 30 days. Jerome quotes him -0.1%. That means Chad will swap 10 BTC for 10,000 shares of the ETF, assuming each share is worth 0.001 BTC, and after 30 days Chad will receive back 9.99 BTC.

During the 30 days where Chad owns 10,000 shares of the ETF rather than 10 BTC, he pledges his ETF shares to borrow dollars from his TradFi stock broker at a very cheap rate. Everyone is happy. Chad can continue being a baller at the club without selling his Bitcoin. And Jerome makes a financing spread.

The ETF financing business will grow to become extremely important and influence Bitcoin interest rates. I will highlight attractive ETF, physical Bitcoin, and Bitcoin derivatives financing trades as this market develops.

Your Size is My Size

For these trading opportunities to last a long time and allow arbitrageurs to execute them in sufficient size, the Bitcoin Spot ETF complex must trade billions of dollars-worth of shares each day. On Friday January 12th, the daily total volume reached $3.1 billion. This is very encouraging and as the various fund managers start activating their vast global distribution network, trading volumes will only increase. With a liquid way within the TradFi system to trade the financial version of Bitcoin, money managers will be able to escape the terrible returns that bonds now deliver in this global inflationary environment.

We are in the early stages of this shift into a period of persistent global inflation. There is a lot of noise, but as time goes on, it will become apparent to managers who run the stock-bond correlations that things have changed. Bonds stop doing their job within a portfolio at the zero bound of interest rates, and even more so when there is persistent inflation. The market will slowly realise this, and the rush out of the >$100 trillion bond market will destroy nations. These managers must then find another asset class that is not meaningfully correlated to stocks or any TradFi asset classes. Bitcoin accomplishes this.

With an ETF, a money manager can import the volatility-reducing but return-enhancing properties of Bitcoin without having to deal with custody. The manager also doesn’t need to update their mandate as they are already cleared to invest in US-listed or Hong Kong-listed ETFs. The only hurdle to adding Bitcoin risk to a fund, it’s a simple and quick phone-call to a brokerage house.

From a secular long-term trend perspective, the crypto ETF complex will only gather assets as inflation persists. Inflation will persist because we are in the process of unwinding the post-WW2 global economic and military arrangement. War is sadly inevitable. The top dog never goes quietly into the night as they are nipped from below. Lastly, war is always inflationary, as we humans engage in the dumb exercise of spending energy to destroy the world to then rebuild it by burning even more energy.

I hope that allays any concerns of those who worry there will not be enough ETF trading volumes to generate juicy long-lasting arbitrage scenarios.

Other faithful followers of Lord Satohsi might wonder if the ETF listing date marked the top of this bull cycle. Be not dismayed by the lacklustre price performance of Bitcoin since the ETFs began trading last week. All around the world central bankers and governments are creating the reasons why the money printer must go brrr. Once the narrative is in place, and a sufficient crisis allows the politicians and bureaucrats to use the fear of a financial systemic collapse to frighten the public into accepting more destructive fiat debasement, money will gush out of central banks and we will enter another leg up in the crypto bull market.

While I didn’t expect this sort of price action, it wasn’t an outcome I ignored. It only reinforces my choice not to add any crypto risk to my portfolio until the middle of March once the BTFP renewal and Fed rate decisions are behind us.

Just remember that the financialization of an asset by TradFi usually results, at least initially, in a price rise of the underlying asset in fiat terms. Bitcoin’s financial properties being added to the Pax Americana and, subsequently Chinese financial markets will be no different over the medium term. The bull market is just beginning. 2024 will be a choppy year with regards to price action, but I still expect by year-end, we will be at or above an all-time high in the market cap of Bitcoin and the entire crypto complex.

In the name of Lord Satoshi, Yahtzee!!!

The post ETF Wif Hat appeared first on BitMEX Blog.

{kind=link}