Key Insights

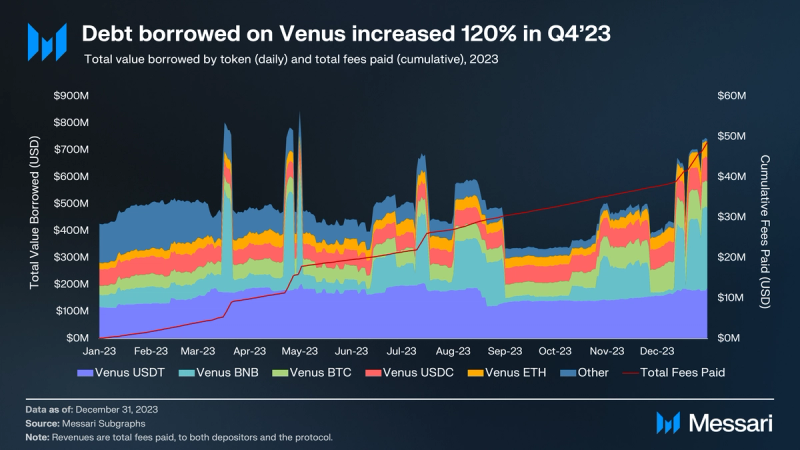

- Borrowing demand on Venus increased to the highest levels of the year, ending with $740 million in active borrows, up 120% QoQ and 74% YoY.

- TVL increased significantly less than the total amount borrowed, leading to higher rates and a 4.5% average APY for depositors in Q4.

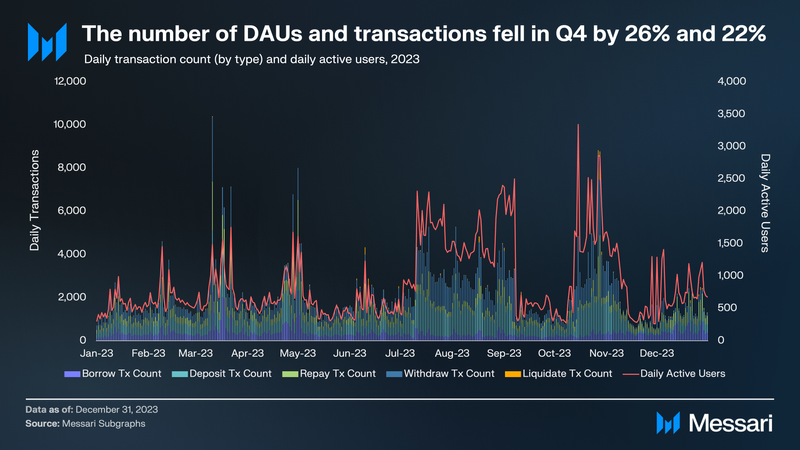

- Transactions fell 22% QoQ, partially because of a high comp but also because depositors were less active.

- The treasury saw a large outflow related to the repayment of the BUSD shortfall after winding down BUSD deposits on the protocol.

Primer

Venus (XVS) is a decentralized finance (DeFi) platform that operates on the BNB Chain, offering a robust money market protocol for the crypto community. At its core, Venus enables users to deposit a variety of cryptoassets, which can then be borrowed. Unlike traditional financial systems where interest rates are often set by central entities, Venus employs a unique algorithmic approach. The interest rates for borrowing and lending on Venus are dynamically adjusted based on an interest rate model. This model takes into account the utilization ratio, which is the proportion of deposited assets that have been borrowed.

The utilization ratio is a critical component of Venus Protocol. When there’s a high demand for borrowing a particular asset, the utilization ratio increases, leading to a rise in interest rates. Conversely, when the demand for borrowing is low, the utilization ratio decreases, causing interest rates to drop. This dynamic adjustment ensures that the system remains balanced, incentivizing lenders when demand is high and borrowers when it’s low.

The protocol is overseen by the Venus DAO community. This is facilitated through the XVS token, which acts as the governance token for Venus Protocol. Holders of the XVS token can actively participate in the governance process, proposing changes or voting on proposals. Additionally, XVS holders can stake their tokens in a specialized vault that comes with financial incentives. Per the Venus tokenomics model, stakers are entitled to a share of the protocol’s revenue in the form of a buyback and redistribution, ensuring that those who actively participate in the platform’s governance are rewarded for their contributions. For a full primer on Venus, refer to our Initiation of Coverage report.

Website / X (Twitter) / Discord

Key Metrics

Financial Metrics

Performance Analysis

Protocol Usage

TVL increased QoQ across the board on Venus, with BTC TVL increasing by 100% and BNB by 33%. ETH, USDC, and other assets by 24%, 14%, and 15%, respectively. However, the increases were largely from token price changes rather than increased deposits. In native token terms, BTC deposits only increased by 53% and ETH deposits by 10%, while BNB deposits actually fell by 8%.

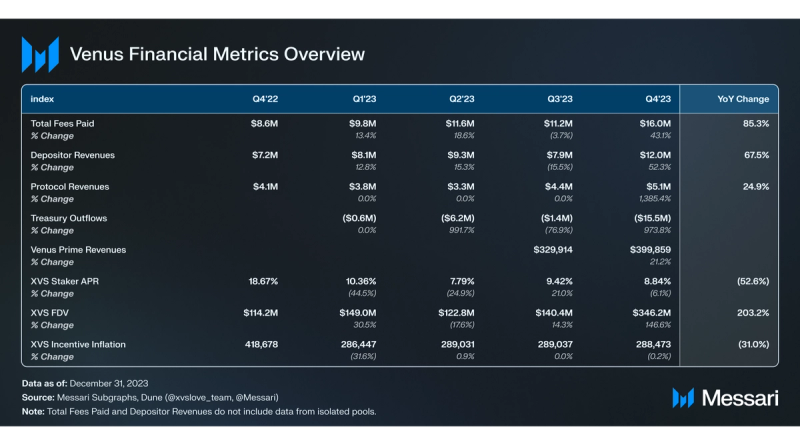

Depositors earned $12 million in interest revenues in Q4 2023, a 52% increase QoQ. The increase was driven by the borrowing of stablecoin and BNB. While BUSD was wound down by Binance and thus on Venus, revenues from BUSD borrowing fell $520,000, but revenues from USDT and USDC borrowing rose by $1.9 million and $622,000, respectively. Those totals were 103% and 63% greater than the Q3 borrowing fees for those stablecoins. BNB continued to be the most borrowed asset on Venus, driving $8.7 million in fees for lenders, a 48% increase QoQ.

While TVL increased 27% QoQ, demand for leverage returned to Venus in a big way, up 120% in Q4. Notably, 70% of the increase in demand came from BNB borrowing, increasing $283 million from $16 million at the end of Q3 to nearly $300 million at the end of Q4. BNB now makes up 40% of the total amount borrowed on Venus. BTC and ETH also saw USD increases in borrowing demand of 87% and 61%, respectively. Stablecoin borrowing in the form of USDT and USDC increased by 37% to $276 million. Borrowers paid $16 million in interest fees in Q4, up 43% from the previous quarter.

Throughout 2023, Venus continued to see consistent activity, even during the bear market. Q4 saw a slight drop in activity after the busy Q3. October brought a large spike in activity as Binance wound down BUSD and Venus worked to help users remove their remaining loans. Average DAUs of 973 was down 26% QoQ, but the metric increased significantly from the quieter first two quarters of 2023. Transaction counts also fell QoQ by 22%, led by depositor activity as users primarily managed their borrows in the bullish price action. Deposits and withdrawals were both down by 40% QoQ, while borrows and repayments increased by 35% each. The BUSD activity also drove liquidations to increase 175% in the quarter, though liquidations make up just 1% of the activity on Venus.

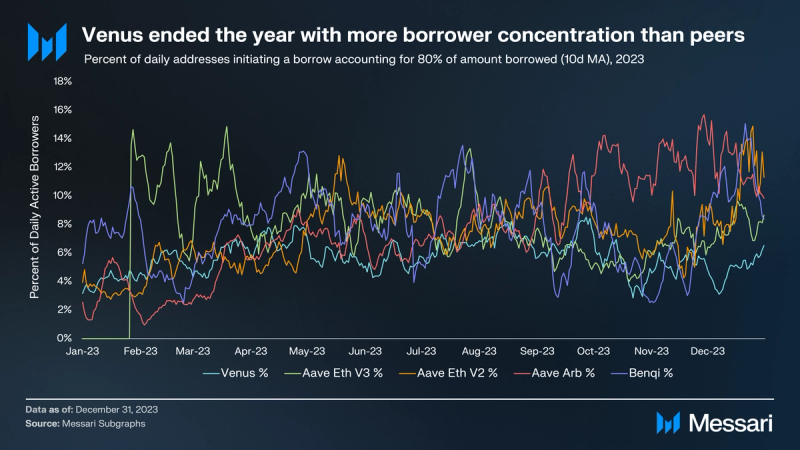

While Ethereum is typically thought of as the whale chain, Venus has lagged behind even its Ethereum-based peers in diversifying borrowers. Measuring the percent of unique borrowers each day that account for 80% of the amount borrowed can give insight into a protocol’s borrower diversity. In Q4, the metric showed that borrowing demand on Venus was consistently more concentrated than other lending protocols. There are pros and cons to a diversified user base. Early products rely on power users to build around, but later-stage businesses tend to value diversification.

Token Accrual

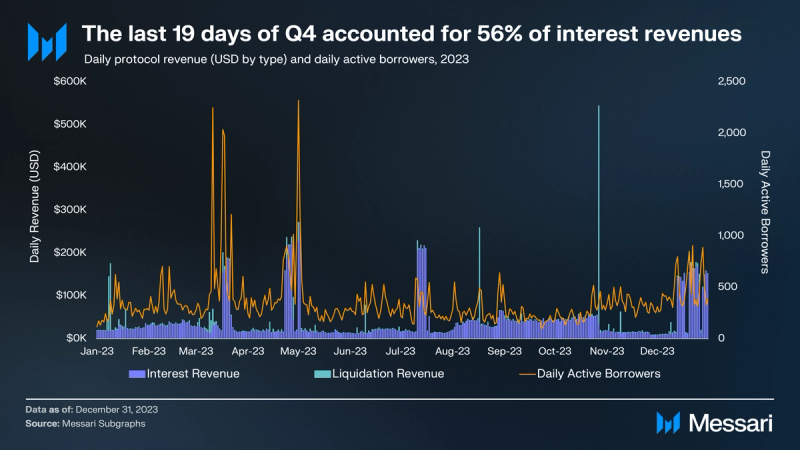

Protocol revenue surpassed $5 million in Q4, ending 2023 on a very lucrative three week stretch. Protocol revenues are split between the risk fund (40% allocation), the treasury (40% allocation), XVS vault stakers (10% allocation), and XVS prime stakers (10% allocation). The forced BUSD liquidations also drove a revenue spike in November. This spiked followed the highest revenue day of the year on October 27, which brought in over $500,000.

Product usage, measured by the number of daily active borrowers, was fairly consistent throughout the year despite the quiet market conditions. The end-of-year revenue spike was accompanied by more borrowers, namely, borrowers who were willing to pay more for their leverage.

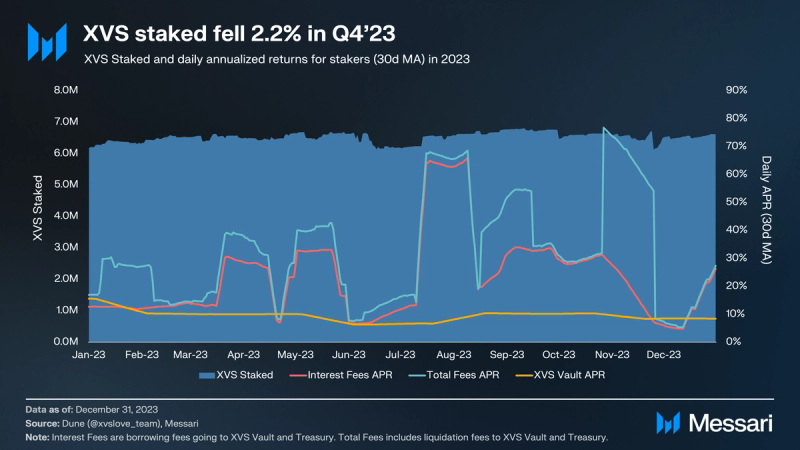

XVS stakers earn from protocol revenue in two ways:

- They receive buyback distributions (10% of protocol revenues are used to buy back XVS, which is then paid out to XVS stakers).

- They manage the treasury and thus indirectly earn protocol revenues allocated to the treasury.

The risk fund is also managed by XVS stakers and voters. However, it is not included in the APR as it is meant to serve as an insurance fund should any bad debt accrue on the protocol. Stakers also earn emission incentives, but given that these are a cost to the protocol, they are not included as revenue. Measuring the rewards and revenue in USD on the day they were earned, XVS stakers averaged a 9% APR from XVS rewards and a nearly 45% APR from total fees plus XVS rewards. After removing the liquidation earnings from October 27, that number falls to 30%.

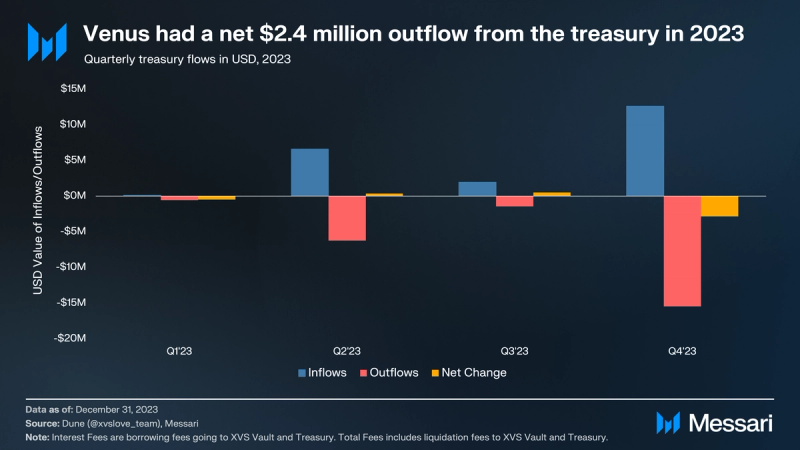

Treasury numbers for both inflows and outflows in Q4 are exaggerated because of the transactions around the BUSD shortfall responsible for $13 million of outflows and $6.4 million of inflows. The shortfall repayment ended up costing $6.6 million BUSD from the risk fund, which is currently hosted in the same account as the treasury assets. The shortfall netted to a $2.9 million reduction. Excluding the repayments, however, treasury flows in Q4 were positive by $3.7 million. Ultimately, the treasury ended the year with nearly $7 million in assets.

Qualitative Analysis

Venus Prime

Venus Prime is an incentive program for stakers within Venus Protocol aimed at enhancing user engagement and protocol growth. By encouraging staking of the protocol’s native token, XVS, Venus Prime addresses the need for a sustainable and self-fueling reward system. Its design promotes long-term staking and active participation in liquidity markets, intended to solve the problem of transient and unstable liquidity that DeFi protocols often face. It also gives a new, sustainable reward mechanism to power users and owners of the token.

Venus Prime allows users to stake XVS tokens to earn Prime tokens, which then qualify the wallet for increased revenue sharing over other stakers. This system uses a Cobb-Douglas reward function. It ensures that rewards are distributed in proportion to both the amount of XVS staked and the user’s active participation in the protocol through supplying and borrowing actions. The system has been implemented in stages through Venus Improvement Proposals (VIPs) to enable various functionalities like claiming Prime tokens, configuring liquidity provider contracts, and setting distribution speeds for rewards.

Venus Prime’s incentive program brings a number of advantages and challenges to the table. On the positive side, it’s designed to foster long-term engagement by requiring XVS tokens to be staked for a specified duration. This relationship should result in a more stable liquidity environment for the protocol. It also rewards active participation, not just passive staking, by offering incentives for users who supply and borrow on the platform. Doing so aligns user behavior with the protocol’s growth objectives. In general, supporting power users is a good strategy for product and network building.

However, there are some potential downsides to consider. The complexity of the program, with its complicated reward conditions, might be intimidating or confusing for some users. To combat a potentially lower rate of adoption the core team created a calculator to help users quantify their rewards. Lastly, Venus Prime requires a significant commitment of 1,000 tokens for 90 days, which may alienate smaller investors or create a two-tiered investor class.

In the long-term, Venus Prime’s design as a self-sustaining program could contribute to the protocol’s longevity by creating a stable economic model. If it leads to increased demand for XVS, the tokenomics of the protocol could see a positive impact, potentially enhancing the token’s value. A successful incentive program could also strengthen the community, fostering greater involvement in governance and decision-making processes. Furthermore, Venus Prime’s success would set a precedent for other DeFi protocols. It could even end up influencing the incentive design landscape across the broader decentralized finance ecosystem and encouraging the creation of similar programs.

Clearing BUSD

BUSD is a stablecoin that used to be supported by Binance. On December 15, 2023, Binance announced it would officially stop supporting BUSD. This decision necessitated immediate action from platforms like Venus that still supported BUSD, as the cessation of support posed significant risks to user deposits. Venus had to ensure a smooth transition away from BUSD to prevent potential liquidity issues and mitigate risks associated with the depreciation of BUSD.

Venus addressed this situation through a series of Venus Improvement Proposals (VIPs):

- VIP-191: Enabled forced liquidations on the BUSD market using a new contract (BUSDLiquidator), and stopped accruing interests in the BUSD market.

- VIP-199: Initiated steps to repay a portion of the shortfall in the BUSD market using treasury funds.

- VIP-204: Used accumulated reserves to repay BUSD debt on behalf of a specific wallet address.

- VIP-215: Authorized a contract (MoveDebtDelegate) to facilitate the repayment of BUSD borrows and borrow equivalent amounts of USDT or USDC as compensation.

- VIP-216: Converted BUSD in the Community Treasury to USDT to mitigate risks associated with BUSD depreciation.

- VIP-221: Adjusted risk parameters for BUSD, notably reducing its collateral factor, and addressed parameters for XVS.

Thanks to these efforts, Venus mitigated the potential negative impacts of BUSD’s deprecation on the protocol and its users. The reduction of the collateral factor for BUSD in VIP-221 was a significant step in de-emphasizing BUSD’s role in the protocol, aligning with the new reality post-Binance support. Venus showcased a proactive and responsive approach to managing changes in the cryptocurrency landscape, demonstrating its commitment to maintaining protocol stability and user trust.

In summary, DeFi platforms like Venus face many such challenges in the rapidly evolving DeFi market. Venus’ handling of the BUSD transition underscores the importance of agile and comprehensive risk management strategies in DeFi.

Expanding to Ethereum

On November 17, the Venus Community passed an offchain vote signaling its desire and intention to launch the protocol on Ethereum Mainnet. This move aims to create mutual benefits by leveraging Ethereum’s liquidity and Curve’s position in the DeFi ecosystem.

The proposal for deploying Venus Protocol on Ethereum Mainnet is primarily driven by Ethereum’s prominent market position, known for its substantial liquidity and volume of large onchain transactions. This move is also aimed at enhancing the brand visibility of Venus by becoming a part of Ethereum Mainnet. Furthermore, the integration aligns strategically with Curve’s ambition to expand its footprint across various lending protocols and to promote its stablecoin, crvUSD. Ultimately, this collaboration seeks to foster mutual ecosystem growth, allowing Curve to support Venus assets on Ethereum, like VAI, thereby benefiting both platforms.

The proposal also included the establishment of a Core Pool on Venus. If passed, Curve’s crvUSD and CRV tokens would be listed with specific supply and borrow caps, along with the application of collateral factors for risk management. Additionally, the proposal includes setting up Isolated Pools that would introduce crvUSD/CRV and crvUSD paired with other stablecoins.

The proposal also features the Liquidity Mining Incentive. It involves the allocation of 500,000 CRV tokens, complemented by matching incentives from Venus, to stimulate liquidity provision. The plan also extends to the creation of pools on Curve. It would establish various pools on the Ethereum Mainnet and provide support for future BSC deployments. Moreover, the proposal suggests that gauges be used for the emission of CRV tokens to incentivize liquidity providers.

As observed in forum discussions, the community’s response has been predominantly enthusiastic, viewing it as a significant opportunity for growth. There is a strong consensus on the mutual benefits it could bring to the Venus, Curve, and Ethereum ecosystems.

The proposal to deploy Venus Protocol on Ethereum and integrate Curve’s tokens is seen as a strategic move to enhance liquidity, brand visibility, and ecosystem synergy. While it presents numerous opportunities, there are also notable challenges related to integration complexity, market volatility, and transaction costs. Aave and Compound dominate the lending markets on Ethereum, so it will be no small task for Venus to take market share. That said, the upside opportunity and partnership with Curve provide plenty of potential heading into 2024.

Closing Summary

All in all, 2023 was a resilient year for Venus: the protocol dealt with legal issues with the largest asset on the protocol (BNB), an attempt to add a stablecoin, BSC Token Hub exploit, and the winding down of BUSD. Through it all, the protocol generated over $37 million in fees for depositors. Q4 was the most lucrative quarter for depositors and XVS stakers to date. The amount borrowed more than doubled, while the amount staked fell in the quarter. While the number of users did not increase significantly, existing users showed they are borrowing more and willing to pay more to do so.