Discover how the Kelly criterion betting strategy can enhance your crypto trading performance by optimizing risk management and maximizing potential profits.

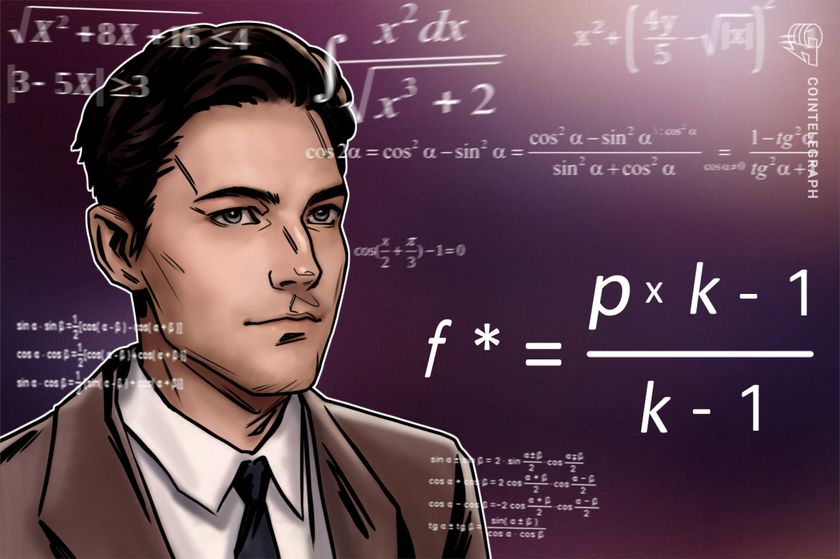

The Kelly criterion, a mathematical strategy that revolutionized gambling and investing, was applied to optimize bet sizes for maximizing long-term wealth. The formula calculates optimal bet sizes based on winning probabilities, but its practical application requires adjustments for transaction costs and psychological factors in volatile markets like cryptocurrencies.

This article will explain what Kelly criterion is, how it works, how it can be used in crypto trading, juxtaposition with the Black-Scholes model, and the associated benefits and pitfalls.

The Kelly criterion is a mathematical technique used in gambling and investing to calculate the ideal size of a sequence of bets. Its fundamental idea is to minimize the chance of financial risks while increasing the rate at which capital grows over time. The algorithm takes into account the likelihood of winning or losing a bet in addition to the potential profit-to-loss ratio.

{kind=link}