Yesterday, a report by Kerrisdale Capital was made public stating that currently MicroStrategy’s stocks are being traded on the stock exchange at a premium deemed unjustified compared to Bitcoin.

MicroStrategy is a company listed on the Nasdaq with the ticker MSTR, but now the bulk of its assets are made up of Bitcoin.

Since August 2020, the company has purchased a total of 214,000 BTC, investing nearly 7 billion dollars.

At this moment, the Bitcoins owned by MicroStrategy have a market value close to 15 billion dollars, but its market capitalization on the stock exchange is close to 29 billion.

Kerrisdale Capital’s report: MicroStrategy’s premium compared to Bitcoin

Kerrisdale Capital is an investor who is short selling MSTR shares.

It is very likely that this decision stems precisely from their consideration that the value of MicroStrategy’s stocks on the stock exchange actually includes a premium compared to the price of Bitcoin, in other words, that they are overvalued.

In its report, Kerrisdale states that it is long on BTC, but short on the MSTR stock, which is now defined as “a proxy for Bitcoin”. It also adds that it believes that this stock is currently trading on the stock exchange at an unjustifiable premium compared to the digital asset that determines its value.

So according to analysts at Kerrisdale Capital, all the value of MicroStrategy would come from the BTC it has in its treasury.

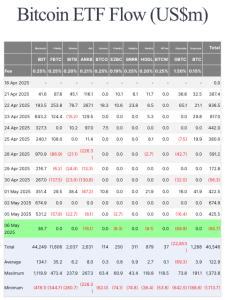

The problem is that on Bitcoin it is now possible to invest directly even on the stock exchange, for example thanks to ETFs, and moreover with low fees.

At this point, the common reasons to justify the attractiveness of the MSTR stock are lacking, while before January it made more sense to invest in this stock in the absence of BTC spot ETFs on US exchanges.

The MicroStrategy title on the stock exchange

MicroStrategy started accumulating Bitcoin in August 2020.

At the time, the price of its stocks on the stock exchange was less than $120.

During 2021, in the midst of a speculative bubble in the crypto markets, the price of MSTR shares skyrocketed to over $1,000, only to then drop back to around $140 by the end of 2022.

However, in 2023 it started to rise again, first going back above $300, and then by the end of the year rising to $685 just a few days before the launch of the new Bitcoin spot ETFs in the USA.

At that point, one could have expected the end of the bull run, but instead, starting from the end of February, a spectacular rally was triggered that brought the stock up to $1,900 just two days ago.

A +280% in less than two months for a stock listed on the Nasdaq seems truly excessive, even though being a proxy of Bitcoin it could somehow be justified.

However, the problem is that during the same period the price of BTC has risen “only” by 75%, which makes the premium highlighted by Kerrisdale Capital quite evident.

At the end of February, the market capitalization was less than 8.5 billion dollars, a figure in line with the market value of the BTC held by the company.

Starting from the beginning of March, however, the price of MSTR started to rise much more than that of BTC, proportionally, creating the above-mentioned premium.

The problem

Kerrisdale Capital assigns a total value of only 1.25 billion dollars to MicroStrategy’s original software business, much less than the 15 billion dollars worth of BTC they hold.

By making all the calculations, they estimate a premium of over 50% of MSTR compared to Bitcoin, with a MicroStrategy stock price of about two and a half times that of BTC, in proportion to the number of Bitcoins held and the number of shares in circulation.

In light of these considerations, it is obvious to imagine that the reason they are shorting the stock is precisely this.

Furthermore, they are not the only ones doing it, because other investors, like S3 Partners, are also short on MSTR, or on Coinbase.

It is also possible that the recent drop in MicroStrategy’s stock price is due to the dissemination of this data.

Yesterday MSTR had opened at $1,944, and then its price had risen up to $1,989. However, it later dropped below $1,850, and then even below $1,700. It then closed at $1,704.

It should be noted, however, that $1,700 is a level reached only on March 13, less than two weeks ago, so for now the losses have been limited to the big gains of the last few weeks.

It should not be forgotten that at the end of February, before the March rally, the price was still below $700.

However, in the last few weeks, a speculative mini-bubble may have inflated around the price of MSTR that could also be ready to burst. However, even a return to $700, with a loss of almost 60%, may not affect the long-term trend.

{kind=link}