Key Insights

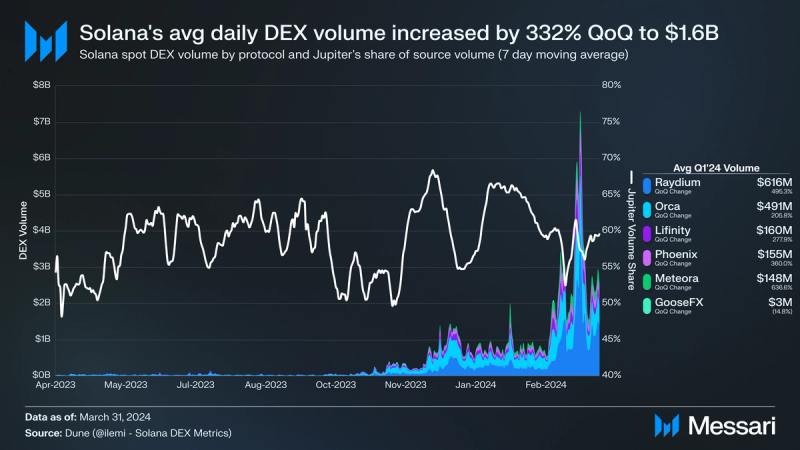

- Solana’s average daily spot DEX volume increased by 319% QoQ to $1.5 billion. Solana has become the primary home for retail users and memecoin traders.

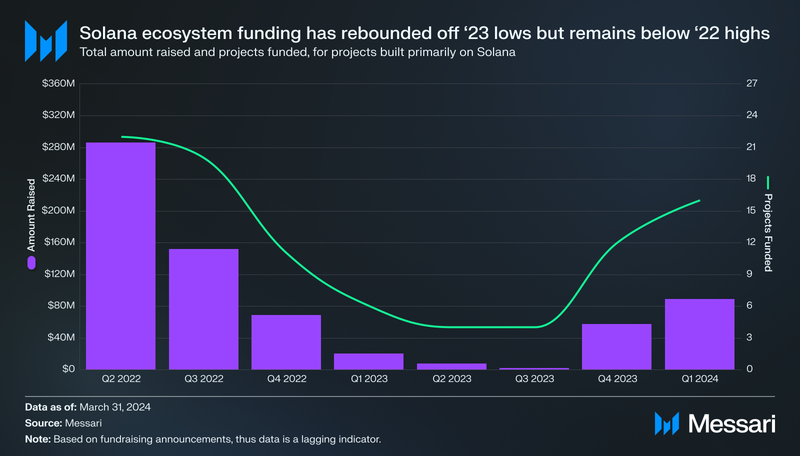

- Projects built primarily on Solana raised $89.2 million in Q1, $2.5 million more than the total amount raised throughout all of 2023.

- Token extensions launched, enabling a set of configurable features for token issuers. Token extensions have so far been adopted by stablecoin issuers, including Paxos and GMO Trust, as well as crypto-native projects like Photo Finish LIVE and Wen.

- The Solana ecosystem took notable strides toward further decentralization with the launches of developer shop Anza and growth organization Colosseum.

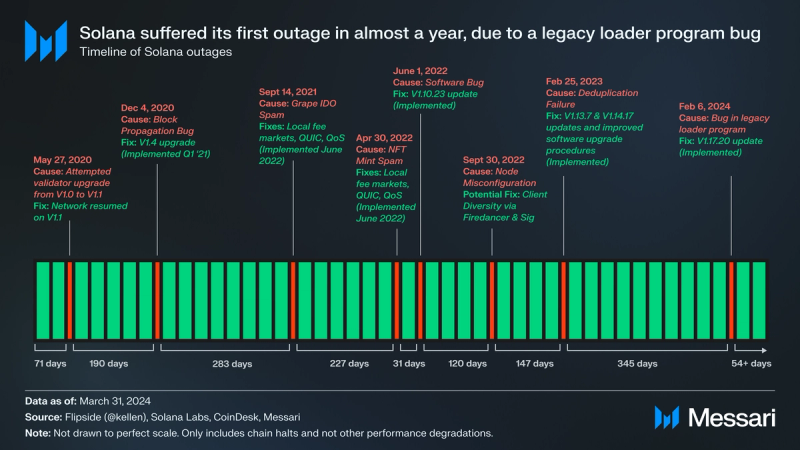

- The Solana network suffered its first outage in almost a year due to a bug in a legacy loader program. The network otherwise held up despite high usage, with upcoming scheduler and networking upgrades to reduce spam and improve the user experience.

Primer

Solana (SOL) is an integrated, open-source blockchain with the goal of synchronizing global information at the speed of light. Solana optimizes for latency and throughput, sacrificing some verifiability. It seeks to accomplish this through features such as its novel timestamp mechanism called Proof-of-History (PoH), block propagation protocol Turbine, and parallel transaction processing. Since mainnet launch in March 2020, several network upgrades have brought further network performance and resilience, including QUIC, stake-weighted Quality of Service (QoS), and local fee markets.

Network and ecosystem development and growth are supported by the non-profit Solana Foundation, Solana Labs, as well as many third-party organizations, including Anza, Colosseum, Helius, and Superteam. Solana Labs has raised over $335 million in private and public token sales. The Solana ecosystem features a growing set of projects across many sectors, including DeFi, consumer, DePIN, and payments.

Key Metrics

Financial Analysis

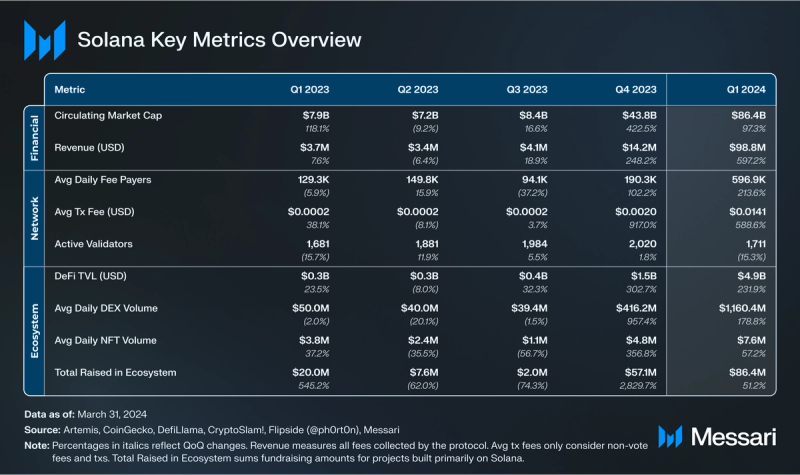

SOL continued to be a market leader after its breakout in Q4’23. It remained ranked 5th among all tokens in market cap, only behind BTC, ETH, USDT, and BNB. After peaking in the last cycle at $77 billion, SOL’s market cap continues to reach all-time highs. It ended Q1’24 with a market cap of $86.4 billion, increasing by 97% QoQ. However, SOL’s price at $194 remains 25% away from its all-time high of almost $260.

Revenue, which measures all fees collected by the protocol, increased by 200% QoQ in SOL terms. With SOL’s price appreciation, total quarterly revenue in USD increased by 597% QoQ to $98.8 million. Solana reached an all-time high of almost $4.9 million in daily revenue on March 18.

Half of these fees are burned, while the other half are distributed to the block producer. The burned tokens reduced Solana’s annualized quarterly inflation rate from 5.5% to 5.2% in Q1. This was the first quarter in Solana’s history where the burn had a non-negligible impact, decreasing inflation by 6%. The issuance rate of SOL is set to continue decreasing by 15% every epoch year until it settles at 1.5%.

As of writing, 62.9% of the SOL supply eligible to be staked is staked, with these holders opting out of dilution from issuance. Note that tokens held by Solana Labs or the Foundation are not all counted as circulating despite not being locked. With the uptick in fees, the annualized real yield rate for SOL stakers increased by 104% QoQ to 2.2%.

While all SOL from the initial distribution is liquid, inflationary pressure can arise due to secondary transactions that re-lock tokens, such as grants or token purchases. Of note, Alameda and FTX bought over 57 million SOL from the Solana Foundation and Solana Labs. However, these tokens are subject to various unlock schedules, with the average unlock date being in Q4’25. Upcoming unlocks can be viewed on Solana Compass and Gelato. In early March, it was reported that Pantera was raising a fund to buy up to $250 million of SOL tokens from the FTX Estate.

Network Analysis

Usage

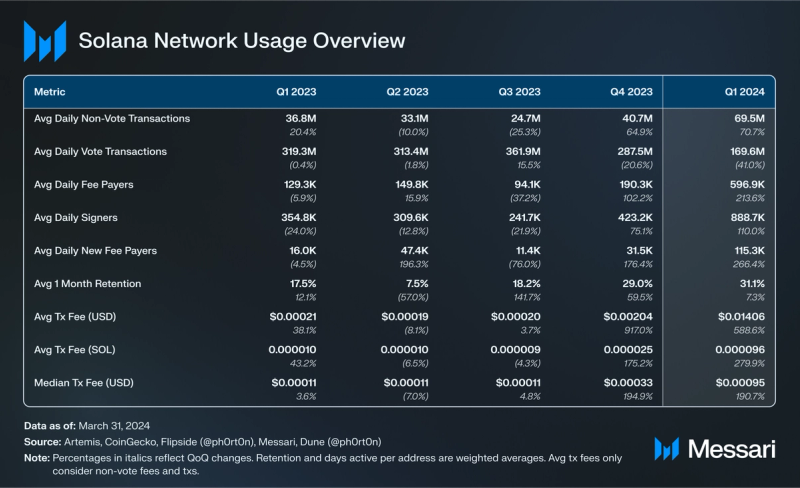

Network activity, measured by non-vote transactions and fee payers, continued to rise in Q1. Average daily fee payers increased by 214% QoQ to 597,000, reaching a peak of over 2 million on March 17. The growth in addresses was largely driven by memecoin trading. Average daily non-vote transactions increased by 71% QoQ to 70 million. However, 62% of non-vote transactions failed, up 10% QoQ. Failed transactions are still executed successfully – they pay fees and modify state – but they didn’t meet the smart contract’s success criteria. Failed transactions mostly come from arbitrage bots or user trades on DEXs where the price impact exceeds the set slippage maximum. That said, the high activity led to a suboptimal user experience, giving core and application developers more information about the necessary upgrades, further detailed in the Performance, Upgrades, and Roadmap section.

New fee payers followed a similar growth trend, reaching a high of almost 1.2 million on March 17. Average daily new fee payers increased by 266% QoQ to 115,000. New fee payers have also been retained at a higher rate. The December 2023, January 2024, and February 2024 new fee payer cohorts all had above 30% one-month retention rates, compared to an average 18% rate from January 2023 to November 2023.

The increase in network activity drove up transaction fees, with more transactions including a priority fee and priority fees being set higher. The priority fee rate reached 85% by the end of the quarter. The average transaction fee increased 280% QoQ to 0.000096 SOL ($0.014). The daily average transaction fee peaked on March 21 at 0.0003 SOL ($0.06).

However, the median fee remained steadier. On March 21, the median fee was 0.00002 SOL ($0.004), a 4x of the minimum transaction fee of 0.000005 SOL. While local fee markets have helped reduce global fee spikes, Solana’s fee markets are still not perfect. Discussions about improving them continued in Q1, as detailed in the Performance, Upgrades, and Roadmap section.

Security and Decentralization

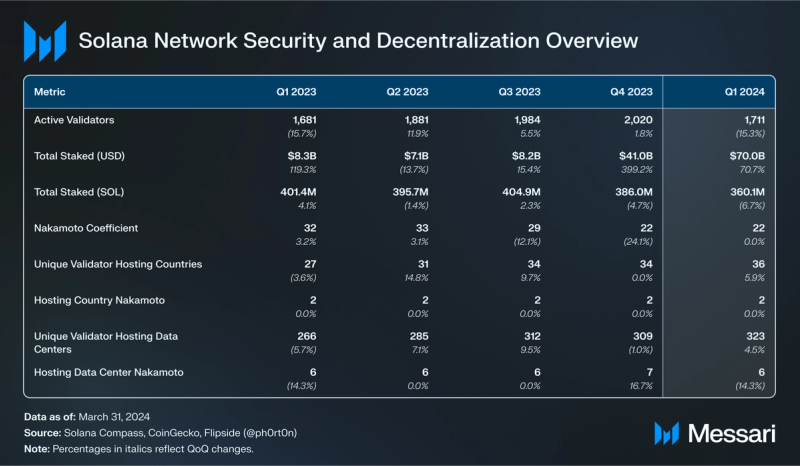

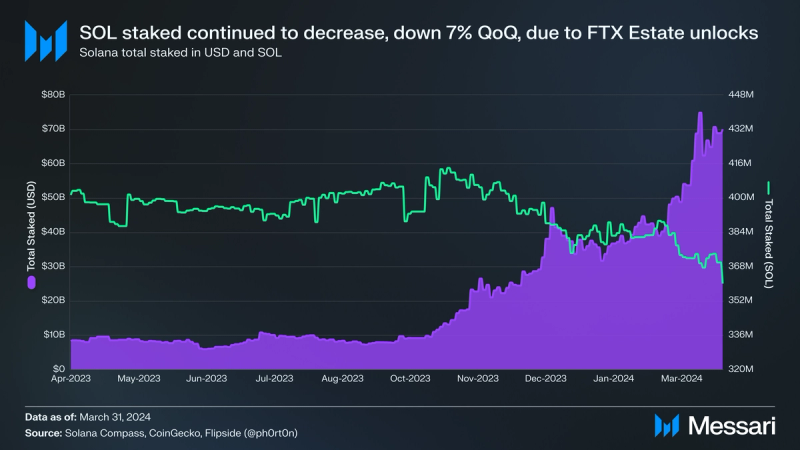

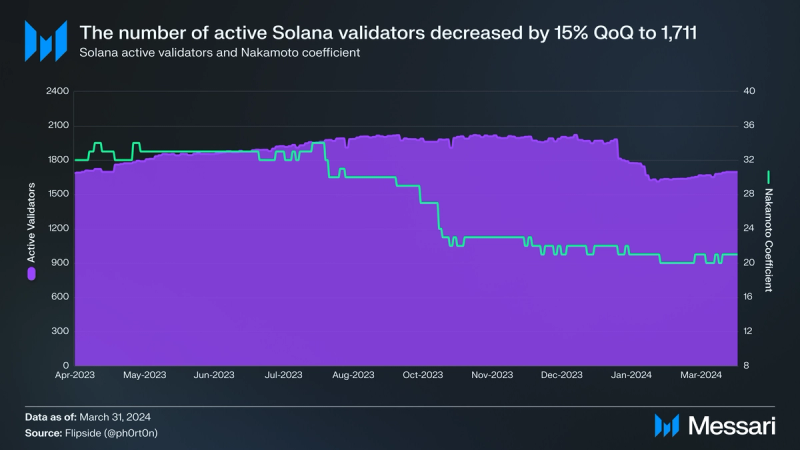

Staked SOL fell for the second straight quarter, down 7% QoQ. The decrease has largely been driven by FTX Estate unstaking its tokens as they unlock. However, with SOL’s price appreciation, total staked in USD terms grew by 71% QoQ to $70 billion, ranking Solana second among all networks behind Ethereum.

Solana’s Nakamoto coefficient stabilized this quarter after dropping in Q4’23, mostly due to FTX Estate’s unstaking, as Alameda/FTX staked to a wide spread of validators. While reaching yearly lows of 20, Solana’s quarter-end Nakamoto coefficient of 22 still remains above the median of other networks.

The Nakamoto coefficient is the minimum number of nodes needed to break liveness. The metric can also be measured across other dimensions important to the resilience of a validator network, including distribution of stake by location, hosting provider, and clients.

Solana network’s 1,711 active validators are hosted in 36 countries, up 33% YoY. The United States leads with 27% of all stake, down 10% QoQ. With Germany accounting for an 8% market share, Solana has a geographic Nakamoto coefficient of 2. Solana validators are hosted in 323 unique data centers, up 21% YoY. Solana has a data center Nakamoto coefficient of 6.

Q1 saw notable changes to both of Solana’s active validator clients, with the Agave fork of the Solana Labs client and the decision by Jito Labs to suspend the mempool in its Jito MEV client.

At the end of January, Anza launched. Anza is a Solana-focused developer shop founded by executives and engineers from Solana Labs. In early March, Anza forked the Solana Labs client. It will continue development on the forked client, Agave, and the Solana Labs client will be deprecated in the summer. Beyond maintaining the Agave client, Anza will work on tooling like token extensions and contribute to the development of ecosystem projects.

In early March, Jito Labs announced that it would suspend its mempool offering. The decision was made following an increase in sandwich attacks due to the rise in retail DEX trading. Jito Labs was largely praised by the community for putting Solana users ahead of its own revenue. Jito’s bundles and block engine continue operating, and MEV tips have not notably fallen. Due to the economic incentives, there will likely be teams that attempt to recreate Jito’s mempool offering. However, a similar offering would not be trivial to build, and even after being built, it would still require attracting validator stake, which may be difficult to do socially. Currently, 69% of stake is running the Jito client, up 43% QoQ.

As an MEV-optimized fork of the Agave client, the Jito client does not offer the same client diversity as a client written from scratch. Firedancer and Sig, two clients written from scratch, are being developed by Jump Crypto and Sig, respectively. Jump’s Frankendancer went live on testnet last quarter. It uses Firedancer’s code for networking functions but the original Labs client code for runtime and consensus mechanisms. Syndica shared an update on recent Sig engineering work in February.

Performance, Upgrades, and Roadmap

On February 6, 2024, the Solana network suffered its first outage in nearly a year. The outage, lasting around 5 hours, stemmed from a bug with the legacy loader program. The bug was previously identified on Solana’s devnet, but its fix had not yet been implemented.

The Solana network has otherwise held up despite the high demand. However, the increased network usage has led to congestion issues, worsening user experience. Identified issues and potential solutions include:

- Transaction Scheduler: Solana’s transaction scheduler is responsible for building blocks. The current implementation has limitations leading to non-deterministic transaction ordering and inclusion – it’s not guaranteed that a transaction with a higher priority fee will be ordered accordingly or have a higher probability of block inclusion. Instead, ordering and inclusion partially rely on variance and FIFO, which incentivizes spam. Anza’s Andrew Fitzgerald has driven development scheduler improvements in the v1.18 upgrade planned for April. To ensure the new scheduler is rolled out safely, it will be optional for validators to adopt it.

- Networking: The implementation of data transfer protocol QUIC in Q4’22 was one of the upgrades in response to previous spam-related network outages. While QUIC has helped eliminate spam-related outages, many have recently agreed it’s contributing to the network congestion issues. Core developers across the ecosystem are working on fixes. Notably, Jump’s Frankendancer testnet release last quarter addresses these issues. While Frankendancer/Firedancer might not hit mainnet soon, its learnings can be shared to help improve the Agave client.

- Fee Market: As discussed last quarter, Solana’s fee markets are inefficient. Of note, base fees are not determined by compute units (Solana’s equivalent of Ethereum gas units). While priority fees are priced by compute units, they’re determined by the number of compute units requested rather than used. This leads to a general lack of compute optimization incentives: transactions often request more CUs than needed, and developers don’t build programs with compute minimization top-of-mind. The v1.18 scheduler will include an upgrade to prioritize transactions with fewer CUs requested, which should reduce some of these issues. There have also been discussions to raise overall blockspace limits in order to increase capacity. Lastly, some believe economic upgrades are also necessary to reduce spam. SIMD-110 seeks to implement EIP-1559-style markets for write lock fees. However, there is much more debate around the need for economic upgrade than for scheduler and networking upgrades. As such, any potential implementation of SIMD-110 or similar proposals is further out.

The Solana Foundation also detailed immediate steps developers can take to improve performance. These include implementing priority fees, optimizing program CU usage, ensuring accurate CU requests, and using Stake-Weighted QoS.

The most notable network launch this quarter was token extensions. Token extensions are part of a new SPL token standard, enabling a set of configurable features for token issuers. They were designed largely based on feedback from discussions with enterprises and financial institutions, but they also have use cases in more crypto-native DeFi and consumer applications.

These extensions enable features that are largely possible on other networks but currently require either developers building the infrastructure themselves or permissioned environments. Implementing them directly into the token program layer thus has several advantages:

- Infrastructure Support: All major wallets, applications, and other infrastructure providers will support token extensions. It would be more difficult for a project building its own solution to reach this level of ecosystem infrastructure support.

- Composability: Tokens and applications that would otherwise have to be walled off in permissioned environments can co-exist on Solana mainnet with existing permissionless token experiences. Users don’t need to bridge, and applications and infrastructure providers don’t need to support another network.

There are over a dozen live extensions, including transfer fees, transfer hooks, and permanent delegate. The confidential transfers extension enables transfer token amounts to remain hidden from everyone except the transfer source, destination, and an optional third-party auditor that can be added by the issuer. The extension will go live once the ZK Token Proof Program, which was brought in the V1.17 upgrade, is activated. The V1.17 network upgrade reached a supermajority of validator stake in epoch 561 (January 17, 2024). It brought further ZK support with Poseidon and alt_bn128 syscalls and various validator and network efficiency improvements.

Ecosystem Analysis

DeFi

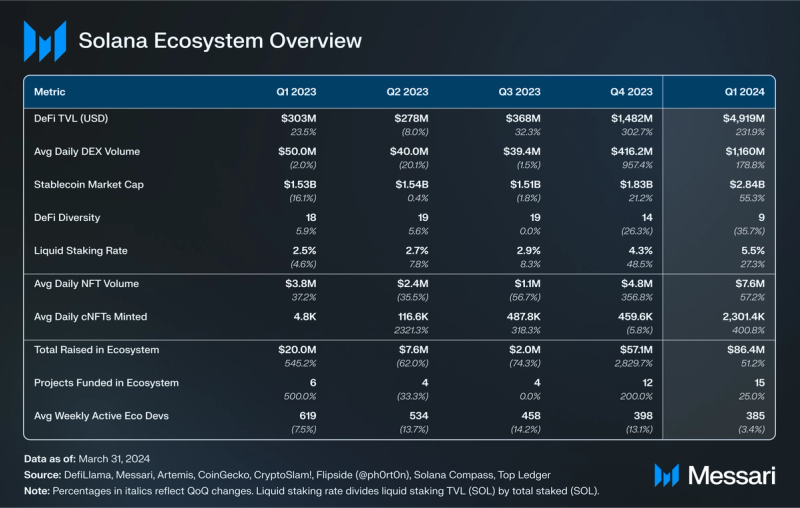

Solana DeFi TVL increased by 232% QoQ to $4.9 billion, ranking it fourth among networks. Lending and yield protocol Kamino jumped from Solana’s fourth largest to the top DeFi protocol by TVL. Its lending protocol ended the quarter with almost $1.3 billion in TVL, an 811% QoQ increase.

On March 7, Kamino announced that a points snapshot would be taken on March 31, ahead of the KMNO launch and airdrop in April. An initial 7% will be airdropped linearly based on points, and another 0.5% will be airdropped to “OGs” on a tiered basis. When Kamino announced the points snapshot, it had $440 million in TVL. Kamino’s yield protocol ended the quarter with an additional $153 million TVL, although it was not counted in Solana’s overall figures to avoid double counting.

While MarginFi lost market share, it still experienced positive QoQ growth, with its TVL increasing by 131% QoQ to $780 million. At the end of February, MarginFi released the whitepaper for YBX, an upcoming LST-backed stablecoin. The whitepaper hints at a MarginFi token, noting that a governance token could help manage bad debt, similar to MKR in MakerDAO. MarginFi’s points program has been running since July 3, 2023, with no announcement yet on a token launch. MarginFi also launched flash loans and the ability to repay loans with collateral.

Following Kamino and MarginFi in TVL was DEX Raydium at $679 million, Jupiter’s perps protocol at $384 million, lending protocol Solend at $351 million, and Drift’s perps protocol at $345 million. Solana’s DeFi TVL has become more concentrated in top protocols, with its DeFi Diversity decreasing from 14 to 9. DeFi Diversity measures the number of protocols that make up the top 90% of a network’s DeFi TVL.

DeFi volume also continued to grow, with average daily spot DEX volume increasing by 319% QoQ to $1.5 billion. Of the Q4 volumes, 38% used liquidity from Raydium, followed by Orca at a 32% market share.

The increase in DEX volumes was largely driven by memecoin trading. Following SOL-stable and stable-stable pairs, SLERF-SOL and WIF-SOL accounted for the fourth and fifth-highest token pair trading volume in Q1. SLERF and BOME, whose trading pair was the seventh-highest by volume, drove the memecoin “pre-sale meta”. Other memecoins in the top 15 by trading volume included BONK and WEN.

Telegram bots have become a popular trading venue for retail users, with Solana Telegram bot average daily active addresses increasing by 573% QoQ to 45,000. About 5% of total quarterly volume came from Telegram bots, an over 2x QoQ increase. BONKbot was the foremost Solana Telegram bot by volume, averaging $37 million daily volume. It collects a 1% fee on volume, used to buy BONK and distribute to various parties, including a burn (10% of the fee). In mid-March, BONKbot unveiled its Valhalla upgrade. Trojan on Solana launched at the end of January, originally under the Unibot branding, before spinning off following a dispute between the two teams. It averaged almost $14 million in daily volume and released its Bolt Pro feature in March. Other popular telegram trading bots include FluxBot, SolTradingBot, and Banana Gun.

Over 59% of spot DEX volume was routed via the Jupiter swap aggregator. After mockJUP and WEN stress tests, Jupiter released its native token JUP at the end of January. Of JUP’s total supply, 10% was airdropped at launch, with plans for three more airdrops of 10% of the supply on January 31 each year. Another 2.5% of JUP’s supply was offered in a launch pool, drawing criticism that it was similar to an IDO but not communicated as such. The launch pool used for WEN and JUP is part of Jupiter’s LFG Launchpad, which was opened to applications for other projects. Other Jupiter-related updates from Q1 include the integration of Mercury’s fiat onramp, a new value-average tool, and Catnip, a bribing tool for the launchpad made by a community developer.

Since its launch, Jupiter perps have averaged $328 million in daily trading volume. The other main Solana perps player is Drift, which has continued its strong growth. After Drift’s average daily perps volumes grew by about 10x in Q4, they grew by 6x in Q1 to $142 million. Near the end of January, Drift launched its points program, which will conclude in March, followed by a token launch. In mid-March, Drift launched its pre-launch markets product, offering perps for yet-to-launch tokens beginning with Wormhole’s W.

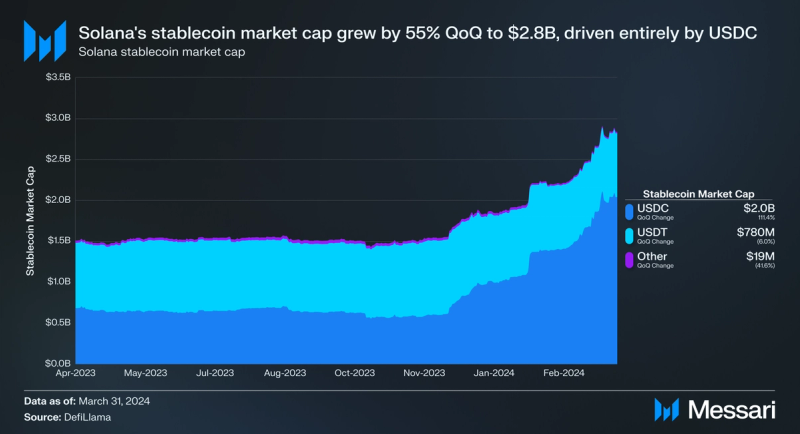

Following 21% growth last quarter, Solana’s stablecoin market cap increased by 55% QoQ to $2.8 billion, ranking it fifth among all networks. The growth was exclusively driven by USDC, whose Solana market cap grew by 111% QoQ to $2 billion. Solana now has the second most USDC of any network, following Ethereum.

At the end of March, Circle’s Cross-Chain Transfer Protocol (CCTP) launched on Solana. CCTP allows USDC to be seamlessly transferred across networks without needing wrapped USDC. Many Solana DeFi, interoperability, and payment protocols have already integrated CCTP.

Several stablecoin issuers have begun taking advantage of token extensions, including Paxos and GMO Trust. In mid-January, Paxos expanded its NYDFS-regulated USDP stablecoin program to Solana, making Solana the second network to support USDP after Ethereum. USDP ended the quarter with a supply of 250,000 tokens on Solana.

GMO Trust launched its NYDFS-regulated stablecoins GYEN (pegged to the Japanese yen) and ZUSD (pegged to the U.S. dollar) on Solana in mid-February. Circulating market caps at the end of the quarter were $180,000 for ZUSD and $97,000 for GYEN.

Other notable DeFi-related events include Dialect Operator, DFlow early access, Flash Trade’s full launch, Parcl’s token announcement, Zeta’s roadmap and token announcement, Meteora points, Juicer’s launch, PepperDEX’s closed beta launch, Zeus Network’s token announcement, Hubble 2.0, Dark Protocol’s re-opened beta, Picasso’s restaking vaults launch, Symmetry V2 and points, Exponent early access, Fluxbot snipe from pool, Bonk PooperScooper, Saros’ airdrop, Avici’s Solana integration, Raydium V3 UI, Convergent’s introduction, BullBot’s introduction, Pocket DeFi’s introduction, and Apollo’s introduction.

Liquid Staking

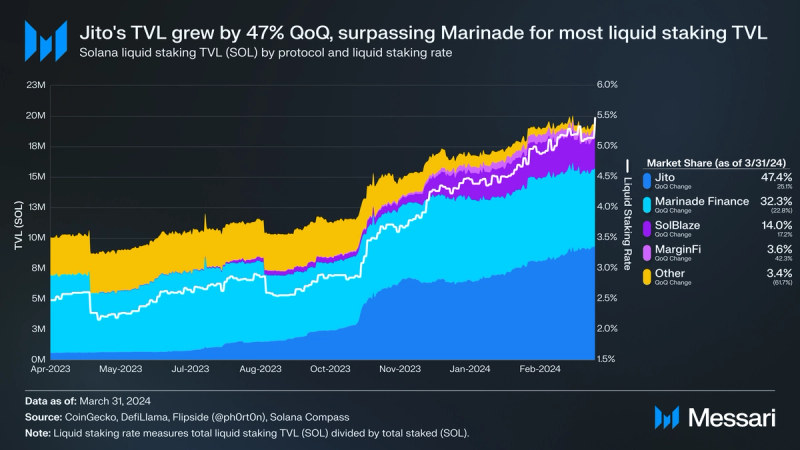

Solana’s liquid staking rate (the percent of staked SOL that is liquid-staked) increased by 27% QoQ to 5.5%. With 63% of eligible SOL supply staked, it will be critical for the liquid staking rate to continue growing to enable an ecosystem built on yield-bearing SOL.

The most notable liquid staking update this quarter was the launch of Sanctum Infinity. The Sanctum Infinity Pool is a multi-LST liquidity pool containing 22 LSTs. It prices LSTs by their “floor price” relative to SOL. This allows any LST in the pool to tap into any other’s liquidity. For example, if a user wants to sell xSOL for USDC, but no xSOL/USDC pool exists, xSOL could be swapped to ySOL and sold to USDC using the ySOL/USDC pool. By allowing any LST to tap into other LST’s liquidity, Sanctum may prevent the monopolistic/oligopolistic market structures that have arisen in other liquid staking ecosystems such as Ethereum. Sanctum’s INF LST has grown its market cap to $48 million. INF is given to users as a token receipt when they deposit into Infinity, and it accrues both staking rewards from the LSTs in the pool and trading fees from swaps.

Sanctum Infinity supports Solana’s top LSTs and a number of single-validator LSTs, many of which Sanctum has helped launch. Single-validator LSTs have offered unique rewards to attract stake, such as Bonk’s bonkSOL LST, which rewards stakers with BONK. Other single-validator LSTs, such as laineSOL and jucySOL, have been airdropping a portion of base and priority fees to stakers. Validators typically do not distribute these fees to stakers. In the past, this has not mattered much as fees made up around 1% of total rewards when combined with inflationary staking rewards. However, with the increase in Solana network activity, these fees have risen notably. During Epoch 590, from March 16-18, these fees made up over 13% of total rewards.

As for Solana’s top liquid staking protocols, Jito has been leading the pack in growth. Jito’s TVL grew by 47% QoQ to 9.4 million SOL, flipping Marinade for the top liquid staking protocol by TVL. Jito’s liquid staking market share ended the quarter nearing 50%. After Jito’s token launch in December 2023, the Jito Foundation selected 17 delegates to receive 12 million delegated JTO. The Jito Foundation posted the first Jito Improvement Proposal. It proposed to expand the Jito validator set to 200 and reduce the maximum commission for eligible validators from 10% to 5%.

Marinade Liquid’s TVL decreased by 9% QoQ to 6.4 million SOL. Marinade began the rollout of Protected Staking Rewards (PSR) and delegation strategy updates. PSR requires validators to put up a bond to be eligible for Marinade stake. The bond is then used to cover any losses in staking rewards due to validator performance issues, commission rugs, or other reasons. PSR will enable Marinade to expand its validator set without sacrificing APY. As such, the delegation strategy update will allow Marinade’s algorithmic delegation validator set to increase above 100, with growth tied to Marinade’s TVL, among other updates. Marinade’s native staking product, launched in Q3’23, ended Q1’24 with 3.8 million SOL TVL.

Blaze has continued its ongoing BLZE airdrop, which began in August. After growing by 344% in Q4, its TVL in SOL increased by 38% QoQ. Proposals also passed Blaze governance to increase stake gauges and update fee distribution.

TVL in MarginFi’s LST increased by 67% QoQ, cracking the top four Solana liquid staking protocols. As noted above, MarginFi released the whitepaper for YBX, a stablecoin backed by jitoSOL, mSOL, bSOL, and LST.

Consumer

NFTs

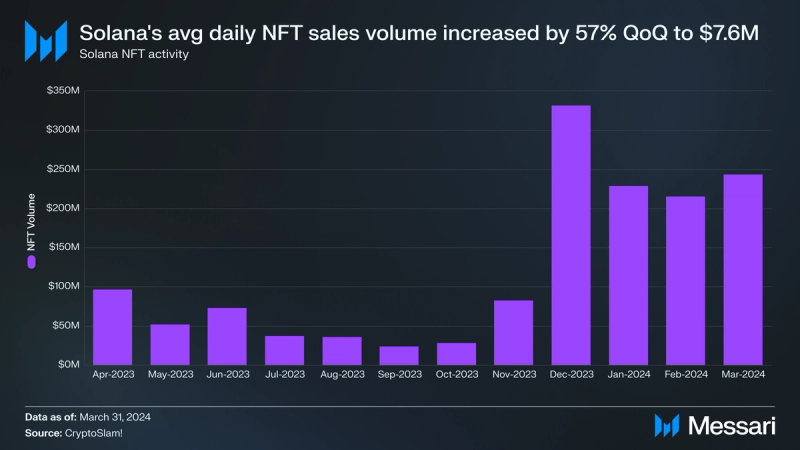

Average daily NFT volume increased by 57% QoQ to $7.6 million. Growth reversed in January and February following a breakout of over $331 million total volume in December 2023, but it increased again in March 2024.

NFT marketplace Tensor’s market share of organic volume increased by 9% QoQ to 71%. In mid-March, the Tensor Foundation introduced the TNSR token to govern the Tensor protocol. Other Tensor updates from Q1 include the launch of Price Lock, which effectively enables option trading on NFTs, and updates to the points program to reduce wash trading.

Magic Eden’s market share of organic volume has continued to decline, down 18% QoQ to 25%. Near the end of January, Magic Eden announced it would be open-sourcing and contributing its protocols to the newly formed Non-Fungible DAO. Non-Fungible DAO will be powered by its native $NFT token. Magic Eden launched a rewards program the following day. Magic Eden also released its own wallet at the end of January.

The top collections by total Q1 trading volume include Froganas (602,000 SOL), Mad Lads (518,000 SOL), and Tensorians (375,000 SOL).

The majority of Solana NFTs are minted via Metaplex NFT standards. At the end of March, Metaplex announced a new NFT standard, Core. Core uses a single account design for cost and performance optimizations and a flexible plugin system for further customization. Core is currently live on devnet. Metaplex also announced that 50% of all historic and future protocol fees will be used to purchase MPLX and sent to the Metaplex DAO. Metaplex fees have totaled 87,000 SOL since March 2023 ($16.9 million using SOL’s price at the end of Q1’24).

There’s also been an increasing amount of NFT token standard experimentation from other entities. The Jupiter and Ovols teams collaborated on the WEN New Standard (WNS), a lightweight NFT standard built on top of token extensions. The first WNS token was WEN, a 1/1 NFT fractionalized using Ovols. WEN was deployed partially as a stress test for the JUP airdrop. It finished the quarter with a $297 million market cap. Other tokens using WNS include ones by Degen Poet and AssetDash.

In general, there was much more experimentation with token standards this quarter, including other lightweight standards on top of token extensions and “hybrid” DeFi/NFT standards. These include epNFTs, TinySPL, SPL22, Nifty, the Solana Hybrid Standard, and SPL-404.

Other NFT-related events include SharkyFi’s selection for Jupiter’s LFG launchpad, LibrePlex fair launch updates, Metaplex Inscriptions, Backpack’s Tensor integration, Ovols V2, Kamino NFT vaults, Rain.fi SPL loans for NFTs, Coca-Cola HBC credentials, and Sniper’s launchpad.

Social and Creator Platforms

Compressed NFTs (cNFTs) are the first successful use case of state compression, which was introduced at the beginning of Q2’23. State compression provides a cost-efficient method for storing data onchain by hashing data into Merkle trees and posting its root hash onchain. Depending on the composability level, the cost to mint and store 1 million cNFTs ranges from 5.3 to 63.7 SOL compared to 24,000 SOL without compression.

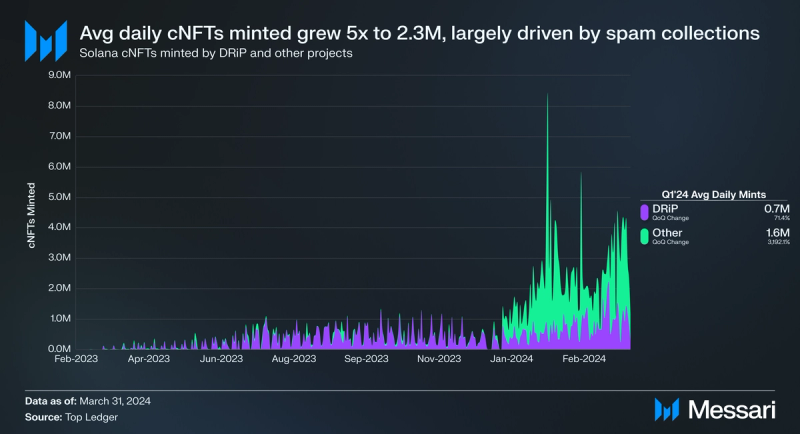

cNFTs enable new use cases across several sectors, namely consumer and DePIN. DRiP is the foremost example of a consumer application only possible with cNFTs. DRiP partners with artists for free NFT art mints, with collection sizes much larger than the normal 10,000. DRiP minted over 64 million cNFTs in Q1, a 71% QoQ increase.

In Q1, DRiP announced partnerships with Worldcoin, Bryan Johnson, DMC, Pyth, Parcl, and SharkyFi, among others. During the memecoin-driven periods of high activity, DRiP mints took longer to reach users. In response, DRiP released an update allowing users to see their collectibles that had yet to be distributed onchain. DRiP is planning several further updates to address the issue.

Overall, average daily cNFTs minted increased by 401% QoQ to 2.3 million. The overall increase in cNFTs minted was largely driven by spam collections. Several projects were quickly released to address the poor UX caused by the spam, including filtoor and Sol-Incinerator.

Other consumer-related events include:

- Farcaster’s Solana Integration: Farcaster was one of the hottest consumer-related narratives across all of crypto following the launch of its Frames product at the end of January. Near the end of February, Farcaster added support for Solana addresses, spurring developers to launch Frames such as a free cNFT minter.

- Solarplex Updates: Solana-native social media platform Solarplex launched its own frames product at the end of February. Solarplex became permissionless to join earlier in the month. It also launched a social NFT buying and selling feature.

- Other: Primitives Protocol whitepaper, Only1’s Flow update and roadmap release, Single’s partnership with Eric Church, Etched’s introduction, Sollinked updates, dReader’s “Enter the Tensorverse”, Publique’s launch, Furrend’s Solana integration, 0xPPL’s Solana integration, CryptoConvo’s introduction, Moonwalk’s introduction, and the launch of SolChat audio and video calls.

Gaming

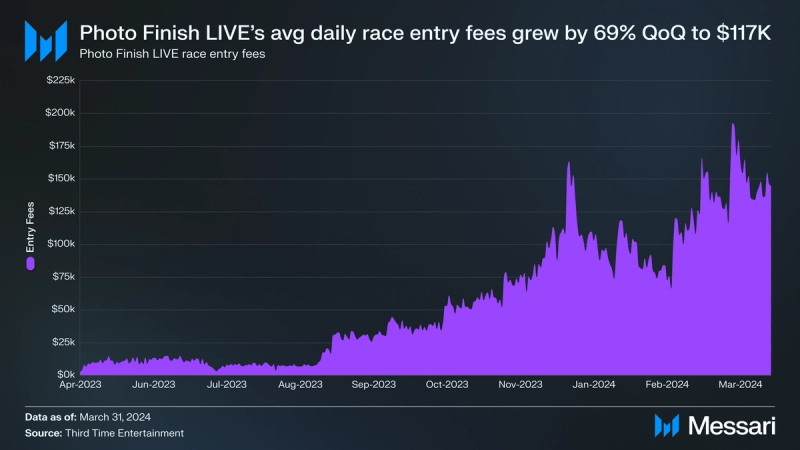

Photo Finish LIVE is a play-to-earn virtual horse racing game that’s officially partnered with the Kentucky Derby. In Q1, its average daily race entry fees increased by 69% QoQ to $117,000. Photo Finish announced a partnership with BONK to rebrand an existing racetrack to “BONK Raceway” for a limited time, which will be followed by a BONK Derby in Q2. On May 4, Photo Finish will host the officially licensed Virtual Kentucky Derby, on the same day as the actual event.

In mid-March, Parallel released the whitepaper for upcoming AI-based game Colony, revealing that its onchain aspects will use Solana. Colony is expected to launch public alpha in Q4’24 or Q1’25. Parallel simultaneously spun out a generalized version of their agent execution network called Wayfinder. Wayfinder is a graph network of tools that AI agents can use to execute onchain actions across various blockchain ecosystems. The Wayfinder whitepaper proposes to anchor this network on Solana. At the end of March, Parallel Studios announced a $35 million funding round.

In early February, Solana Labs announced that its Web3 gaming development API GameShift has exited beta. New GameShift additions this quarter include Dynamic NFTs, Asset Lending, In-game Marketplaces powered by Tensor, Asset Airdrops, Fiat Payouts, and Custom Transactions.

Other gaming-related developments from Q1 include MagicBlock’s acceptance into a16z Crypto’s Crypto Startup Accelerator, Star Atlas’ roadmap release, Nyan Heroes pre-alpha demo, Solana Civ’s v0.2.0 update, GolfN’s genesis mint, GG’s beta launch, BR1: INFINITE’s Loot Box mint and Preseason Games launch, BlockGames’ Solana integration, and Legends of the Sun introduction and crowdfunding.

DePIN

Solana is becoming a hub for DePIN applications, hosting Helium, Hivemapper, Render, Teleport, and GenesysGo, among others.

Notable Q1 events include:

- Helium Wi-Fi and Telefonica Partnership: In January, Nova Labs announced a partnership with telco Telefonica to launch Helium Mobile Hotspots in Mexico and integrate them into Telefonica’s network. A month later, Helium Mobile Wi-Fi launched, allowing Helium Mobile Hotspot owners to offer secure, free public Wi-Fi while still providing Helium Network coverage. Helium Mobile also released International Roaming capabilities.

- Io.net Raise and Ignition Program: In early March, decentralized GPU aggregator io.net announced a $30 million Series A at a $1 billion valuation. The project also launched points program Ignition, rewarding network suppliers and community participants via Galxe, ahead of an expected token launch at the end of April.

- Teleport First Riders: Decentralized rideshare protocol Teleport officially kicked off with its first rides in its genesis city of College Station, Texas.

- Hivemapper Bee Unveiled: Hivemapper aims to create a decentralized global map. In February, it introduced a new dashcam, Bee, and opened it for pre-orders. Compared to the existing Dashcam and Dashcam S models, the Bee is designed to be easier to use and more performant. Over 10 million unique road kilometers (17% of the global road network) have been mapped by Hivemapper contributors.

- Decentralized internet connectivity protocol Dabba released tokenomics info, sold out the first round of its hardware release, and opened a waitlist for the next round of sales.

- Other developments: launch of distributed GPU cluster for LLM inference Kuzco, launch of decentralized storage protocol Sdrive, launch of map-to-earn protocol Proto on the Apple and Google Play app stores, launch of Genesys Go’s shdwDrive Testnet2, the successful proposal to integrate Nosana into the Render Network, and launch of decentralized cloud smartphone APhone.

Payments

With low transaction costs, sub-second finality, and a network of several thousand nodes, Solana promises to help power mainstream payment flows — so says Visa, which expanded its USDC settlement pilot to Solana in Q3’23.

Notable events from Solana-native payments infrastructure companies and applications this quarter include:

- Sphere Seed Round: Payments protocol Sphere announced a $2.8 million seed round led by TCG Crypto and Jump Crypto. Sphere launched its early access last quarter after placing first in the 2022 Solana Summer Camp Hackathon payments track. In late March, Sphere added a feature to send payments via a link.

- Code Seed Round: Payments platform Code, focused on micropayments, announced a $6.5 million seed round led by M13 and Union Square Ventures.

- Meso U.S. Launch and Seed Round: Fiat on/offramp Meso launched for U.S. citizens in January and later announced a $9.5 million seed round. Meso currently supports Ethereum and Solana.

- Espresso Launch and Solana Labs Incubator: Espresso Cash launched its global money transfer app for users in the USA, Europe, and Nigeria in January. Solana Labs announced in March that Espresso Cash was one of the six selected projects for its incubator.

- Ottr Acquisition: At the end of February, Solana payments wallet Ottr announced that it was acquired by Tools for Humanity, one of the contributors to Worldcoin. The team will sunset Ottr Wallet as they shift to developing the World App.

- Other developments: Grab Singapore’s Solana integration, Breezepay’s Solana integration, Travel Care’s Solana integration, Giveth’s Solana integration, Beam’s onramp waitlist, and Open’s Solana integration.

Infrastructure

Notable infrastructure-related events from Q4 include:

- Solana Mobile Chapter 2: Solana Labs announced and opened pre-orders for Chapter 2. The announcement capitalized on the momentum from the original Saga phone, which quickly sold out after a surge of sales in December driven by community airdrops. Chapter 2 offers a lower price point at $450 and will ship in H1’25. The phone surpassed 100,000 pre-orders within a month. Two snapshots of the referral leaderboard were taken, distributing a soulbound NFT and rewards from participating ecosystem projects.

- Backpack Series A: Wallet and centralized exchange Backpack announced a $17 million Series A led by Placeholder at the end of February. Backpack Exchange became available to residents of 11 U.S. states and the U.K. Other Backpack Exchange upgrades include fiat support, new rewards distribution system The Dro, and preparation for a mobile release. Q1 Backpack Wallet updates include the Side Panel, native SOL staking, and Wormhole integration.

- Cube Series A: Hybrid exchange Cube announced a $12 million Series A at a $100 million valuation led by 6th Man Ventures, following a $9 million round in October 2023. Cube combines offchain order matching with onchain settlement, using multi-party computation to store user funds.

- Helius Series A: Developer tooling company Helius announced a $9.5 million Series A led by Foundation Capital. Helius releases from Q1 include the node deployment tool Automatic Private Nodes, a new Solana Fee API, and portfolio viewer Galleria.

- MetaDAO Token Sales and Releases: MetaDAO is a DAO governed by markets – the first implementation of futarchy. After launching in Q4, MetaDAO gained attention in Q1 due to mtnDAO discussions and token sale proposals by Pantera Capital and Ben Hawkins. While both these proposals failed, a later proposal by Colosseum to acquire $250,000 in META succeeded, adding to the $75,000 raised in a public token sale. MetaDAO shipped bribes market Vota and is developing a Futarchy-as-a-Service platform.

- Other developments:

- Wallets: Dynamic’s embedded wallet launch, Phantom Wallet Watcher, Brave Rewards’ Solana integration, Squads’ Fuse waitlist opened, and Hey Wallet!’s Solana integration.

- Interoperability, VM Infra, and Modularity: SVM L2 Eclipse’s $50 million Series A, atomiq’s grant from the Solana Foundation, Wormhole EVM to Solana cross-chain swaps powered by Hashflow, support for Neon EVM on deBridge, Wormhole’s tokenomics release, Injective and Bonfida’s omnichain domain launch, and Rome’s introduction of Rhea and Remus.

- Developer tooling: Crossmint’s acquisition of Winter, Armada staking program open-sourced, Neodyme Riverguard, Luzid’s release, LightDAS’ release, Eject’s release, Lighthouse Protocol’s introduction, and RustRover IDE debugger.

- Explorers, Data, and User Tools: Etherscan’s acquisition of Solscan, Google Cloud BigQuery Public Data integration, Vybe Network’s API release, SolanaFM verifiable builds, Webacy’s Solana integration, and Space Operator’s mint.

- AI: DAIN’s private beta launch, TARS Protocol’s AI grant from Solana Foundation, Wayfinder’s whitepaper, and Trustless Engineering Corp’s AI grant from Superteam.

- Other: Dialect Alerts Stack, Elusiv’s V1 sunset and MXEs introduction, Pyth’s dapp airdrop, Switchboard Randomness Service and On-Demand, and DePlan’s introduction.

Growth

After an enduring bear market, Solana ecosystem funding is picking back up. 16 projects that are building primarily on Solana announced funding rounds in Q1, totaling $89.2 million raised. Combined with Q4’23, 25 projects raised $146.3 million, compared to $9.6 million raised across 7 projects in the two quarters before.

Solana Foundation hackathons have historically been very successful in generating projects that later raise VC funding. These hackathons were led by former Solana Foundation head of growth Matty Taylor, who in Q1 announced the formation of Colosseum, along with co-founders Nate Levine and Clay Robbins. Colosseum is similar to Y-Combinator – it runs an accelerator with a venture capital arm. It differs in that eligibility to participate comes from winning its hackathons instead of through a college-style application. Colosseum also features a platform where builders can discuss ideas and meet co-founders. Colosseum’s first Solana hackathon, Renaissance, began on March 4 and will run until April 8. Winners will be eligible for acceptance into Colosseum’s accelerator and receive $250,000 in pre-seed capital. Several organizations are also running side-track events with additional prizes.

Along with developer shop Anza, the founding of Colosseum marks a shift toward the decentralization of Solana’s social layer. Hackathons and other growth initiatives are increasingly being organized by the community rather than the Solana Foundation or Solana Labs.

The flagship community-led Solana event has been mtnDAO. The month-long hacker house ran its fifth iteration in Salt Lake City in February. mtnDAO is organized by the founders of DeFi protocols Cypher and MarginFi.

A similar month-long hacker house was officially unveiled in March. Instead of being on a mountain, IslandDAO will run from mid-May to mid-June in Crete, Greece. Applications are live.

Lamport DAO organized Solana’s first hackathon for written content, Solana Scribes, which took place during the month of February. The hackathon distributed over $140,000 in prizes and garnered 2,795 submissions from 1,057 participants.

Cubik is a platform facilitating quadratic funding of public goods, similar to Gitcoin. In the second half of March, it ran its first round of public good grant funding with $55,000 in its matching pool. Total community donations exceeded $100,000.

Of course, the Solana Foundation and Solana Labs are still leading growth in their own right. The Solana Hacker House tour hosted by the Solana Foundation is back for its third year, with Circle as the presenting sponsor for the four 2024 hacker houses. The first one of the year took place at the end of March in New York City, focusing on DeFi, security, and regulations. The next one will take place in mid-April in Dubai, focusing on RWA, stablecoins, and regulation. The Solana Foundation also released new RFPs for grant applications centered on audit and security tools. In addition, it partnered with AD Global Market and joined the Tokenized Asset Coalition and Crypto Council for Innovation. Lastly, tickets went on sale for Solana Foundation’s annual Breakpoint conference, taking place in Singapore in late September.

After announcing its Solana Incubator in Q4, Solana Labs selected the first six teams set to join in March. The cohort features tokenomics tooling platform Armada, payments app Espresso Cash, yield-optimizer Juicer, liquid staking liquidity layer Sanctum, DePIN network for gaming computers Shaga, and onchain gaming platform Zeebit.

Other initiatives from Q1 include:

- The formation of developer shop Turbin3.

- FluxBeam’s Token Extensions Hackathon, with over $25,000 in prizes, began in February and will run until April 20.

- RareSkills launched 60 Days of Solana: A Solana Course for Ethereum Developers.

- Launches of Solfate’s DevList and the 76 Devs’ Devnet Directory.

- Speakers were announced for the Solana Crossroads conference in May, which is run by Step Finance’s ambassador program Solana Allstars.

- New Superteam divisions in Brazil, the Philippines, Malaysia, and the Balkans.

- Superteam UAE’s partnership with Hub71.

- Metaplex distributed 1 million MPLX in its cNFT-focused hackathon, Metaplex cHack, and introduced its Startup Program.

- Winners were announced for the second Solana Speedrun, a gaming hackathon hosted by MagicBlock along with Lamport DAO and the Solana Foundation.

- LD Capital announced a Solana Ecosystem Fund.

- Christex Foundation hosted the first-ever blockchain hackathon in Sierra Leone and a two-week bootcamp to prepare developers for Colosseum.

- Heavy Duty Builders ran an online developer camp in Spanish.

- The first Summer Sol Sessions hackathon in Argentina took place.

- Solana University conducted its Solana Developer Bootcamp.

- The Solana Foundation conducted its MCM Founder’s Bootcamp.

- Solana Developers ran crash courses.

- Encode Club hosted a Solana hackathon and Spring bootcamp.

- DecentraGrants distributed its first grants, with Space Operator and Gib.work the recipients.

- Web3 Builders Alliance held its Q1 Solana Master Builder Cohort.

- Helius released a front-end development course.

- Ackee Blockchain’s School of Solana Season 5 was announced.

- Bonkathon was announced, a hackathon hosted by RadiantsDAO, Phase Labs, and Bonk with $300,000 in prizes.

Closing Summary

Solana’s growth continued in 2024 after a strong close to 2023. Solana became the primary home for retail users and memecoin traders. Its average daily spot DEX volume increased by 319% QoQ to $1.5 billion. Solana also took strides in its ability to support institutions with the launch of token extensions, which enable a set of configurable features for token issuers.

However, the increased network activity led to congestion issues, which are being addressed in upcoming networking, scheduler, and fee market upgrades. Although unrelated to the high activity, the Solana network suffered its first outage in almost a year.

VC funding for Solana-based projects is heating up after an enduring bear market. Projects built primarily on Solana raised $89.2 million in Q1, $2.5 million more than the total amount raised throughout all of 2023. The Solana ecosystem is also becoming more decentralized. Former Solana Labs engineers and executives announced the formation of developer shop Anza, and the former Solana Foundation head of growth launched the growth organization Colosseum.