(Any views expressed here are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.)

Want More? Follow the Author on Instagram and X

Like Pavlovian dogs, we all believe the correct response to rate cuts is to BTFD. This behavioural response is rooted in the recent memories of Pax Americana’s subdued inflation. Whenever there was a threat of deflation, which is terrible for financial asset holders, aka rich cunts, the US Federal Reserve (Fed) responded forcefully by pressing the Brrr button on its money printer. The dollar is the global reserve currency, creating easy monetary conditions for the world.

The effects of global fiscal policies to fight the COVID hoax or pandemic, depending on your view, ended an era of deflation and ushered in an era of inflation. Central banks belatedly acknowledged the inflationary effects of COVID-19, justified monetary and fiscal policies, and hiked rates. Global bond markets, and most importantly, the US bond market, believed our monetary masters’ seriousness about vanquishing inflation and did not send yields 2 da moon. However, the assumption is that the witches and warlocks at the helm of various central banks will continue raising the price of money and reducing its supply to appease the bond market. This is a very dubious assumption, given the current political climate.

I will focus on the US Treasury market as it is the most critical debt market globally due to the dollar’s role as the global reserve currency. Every other debt instrument, regardless of the issued currency, reacts in some way to Treasury bond yields. A bond’s yield combines the market’s forward expectations for growth and inflation. The Goldilocks economic scenario is growth with little to no inflation. The big bad wolf economic scenario is growth with lots of inflation.

The Fed convinced the Treasury market it was serious about fighting inflation by raising its policy rate at the fastest pace since the early 1980s. From March 2022 until July 2023, the Fed raised rates by at least 0.25% at each meeting. The 10-year US Treasury yield never surpassed 4% during that period, even while the manipulated government inflation index hit 40-year highs. The market was satisfied that the Fed would keep raising rates to eradicate inflation so long-term yields wouldn’t go asymptotic.

US Consumer Price Index (white), 10-year US Treasury Bond Yield (gold), Fed Funds Upper Bound (green)

All that changed at the August 2023 Jackson Hole central wanker circle jerk. Powell indicated that the Fed was on pause at its upcoming September meeting. But the spectre of inflation still haunted the markets. This was chiefly because inflation was driven primarily by increased government spending that showed no signs of abating.

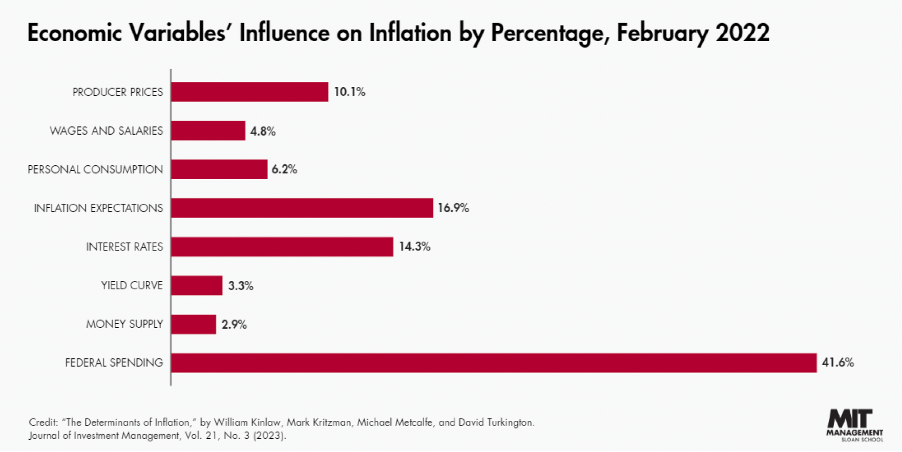

MIT economists discovered government spending was the most significant culprit for stoking inflation.

On one paw, politicians know that high inflation reduces their re-election chances. But on the other paw, providing free shit to voters paid for via currency debasement improves their re-election chances. If you only hand out goodies to your clique, but they are paid for by the larger denominator of the hard-earned savings of your opponents plus supporters, then the political calculus favours increasing government spending. As a result, you are never voted out of office. That’s precisely the policy US President Biden’s administration pursued.

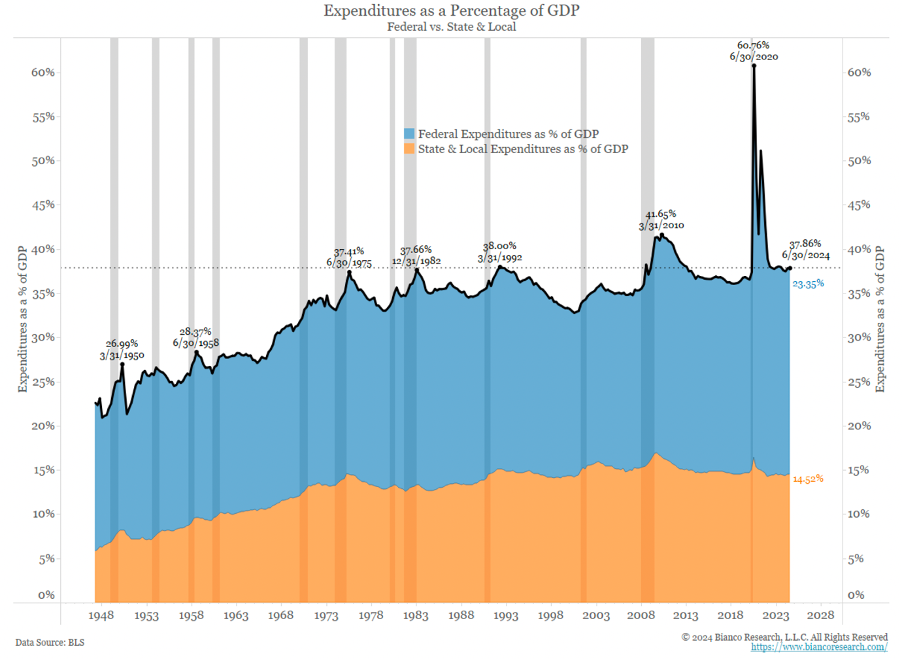

Total government spending is the highest it’s ever been in peacetime. I use the word “peace” in a relativistic way, of course, only focusing on how citizens of the empire feel; for those poor souls who died and continue dying as the result of US-made weapons put in the hands of those advancing democracy, these last few years have hardly been peaceful.

If taxes were raised to pay for the largesse, then spending wouldn’t be an issue. However, raising taxes is a very unpopular thing for an incumbent politician. Therefore, it didn’t happen.

Against this fiscal backdrop, on 23 August 2023 at the Jackson Hole conference, Fed chair Powell signalled they would pause hiking rates at its upcoming September meeting. The more the Fed hikes rates, the more expensive it is for the government to finance deficits. The Fed can put a stop to this wanton spending by making financing the deficit more expensive. Spending was the primary driver of inflation that the Fed sought to quell, but it refused to continue raising rates to achieve success. Therefore, the market would do the Fed’s job for it.

The 10-year US Treasury yield began a quick ascent from ~4.4% to 5% after the speech. This is quite shocking considering that even at 9% YoY inflation in 2022, the 10-year yield only hovered around 2%; 18 months later, after inflation fell to ~3%, 10-year yields were marching towards 5%. The higher rates caused a 10% correction in the stock market and, more importantly, reignited fears of another bout of US regional bank failures due to losses on their Treasury bond portfolios. Faced with a higher cost to fund government deficits, a falling stock market leading to reduced capital gains tax receipts, and a potential banking crisis, Bad Gurl Yellen stepped in to provide dollar liquidity and end the rout.

As I wrote in my essay “Bad Gurl,” Yellen gave forward guidance that the US Treasury would issue more Treasury bills (T-bills). The net effect of this was to pull money out of the Fed’s Reverse Repo Program (RRP) and into T-bills, which can be re-leveraged throughout the financial system. That announcement came on 1 November 2023 and kicked off the bull market in stocks, bonds, and, most importantly, crypto.

Bitcoin chopped around from late August to late October 2023. However, after Yellen’s liquidity injection, it took off, eventually hitting a new all-time high in March of this year.

Reverse Reverse

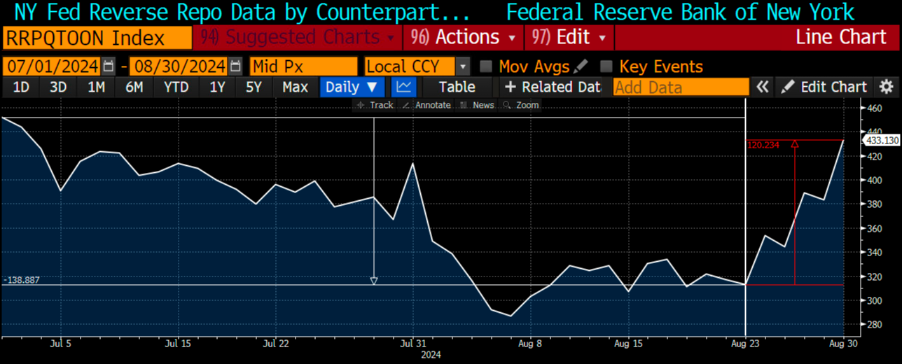

History never repeats itself, but it does rhyme. I failed to appreciate this fact in my last essay, “Sugar High,” where I talked about the effects of the Powell Payroll Pivot. I was a bit uneasy that I held a consensus opinion on the positive impact of an upcoming rate cut on risk markets. On my way to Seoul, I happened to glance at my Bloomberg watchlist, where I track the daily changes of the RRP. I noticed it moved higher from the last time I checked, which was puzzling because I expected it to continue falling due to net Treasury bill (T-bill) issuance by the US Treasury. I dug in a bit deeper and saw the surge higher began August 23rd, the day Powell pivoted. I next considered whether the RRP surge could be explained by window dressing. Financial institutions generally lie about the state of their balance sheet at quarter ends. Regarding the RRP, financial institutions generally park money at quarter end in this facility and remove it the week after. The third quarter ends September 30th, so window dressing doesn’t explain the surge.

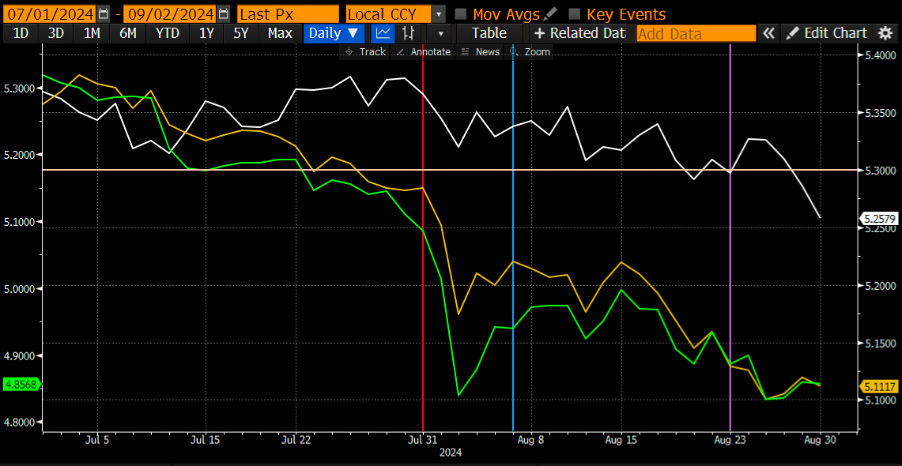

Then I thought, would money market funds (MMF) in search of the highest and safest short-term USD yield sell T-bills and deposit cash in the RRP because T-bill yields declined? I pulled up a chart below of 1m (white), 3m (yellow), and 6m (green) T-bills. The vertical lines mark the following dates: red line – when the BOJ hiked rates, blue line – when the BOJ caved and announced future rate hikes will not be considered if they believe the markets will react poorly, purple line – the day of the Jackson Hole speech.

MMF fund managers must decide how to earn the most yield on new deposits and maturing T-bills. The RRP yields 5.3%, and funds will be invested in T-bills if their yield is slightly greater. Starting mid-July, the 3m and 6m T-bill yield dropped below the RRP’s. However, that was primarily driven by market expectations of aggressive Fed easing due to the strong yen-inspired carry trade unwind. The 1m’s yield still traded slightly above the RRP’s yield, which makes sense because the Fed had not given forward guidance that a September rate cut would occur. To confirm my suspicion, I charted the RRP balances.

RRP balances generally fell until the August 23rd Powell Jackson Hole speech, where he announced the September rate cut (denoted on the chart above by the vertical white line). The Fed will meet on September 18th, and the Fed Funds Rate will be cut at a minimum of 5.00% to 5.25%. This confirmed the anticipated move of the 3m and 6m T-bill, and the 1m T-bill yield began closing the gap. The yield on the RRP will only decline the day after the rate cut. Therefore, the facility offers the highest yield from now until September 18th out of the universe of suitable yield-bearing instruments. Predictably, RRP balances started rising immediately after Powell’s speech as MMF managers maximised current and future interest income.

While Bitcoin initially popped to $64,000 the day of the Powell Payroll Pivot, it gave back 10% of its fiat dollar price over the last week. I believe Bitcoin is the most sensitive instrument that tracks dollar fiat liquidity conditions. As soon as the RRP started rising to the tune of ~$120bn, Bitcoin swooned. A rising RRP sterilises money as it sits inert on the Fed’s balance sheet, unable to be re-leveraged within the global financial system.

Bitcoin is extremely volatile, so I accept the criticism that I may be reading too deeply into one week’s price action. But my explanation of the events combined with the observed price action lines up too perfectly to be explained by just random noise. It will be easy to validate my theory. Assuming the Fed doesn’t cut rates before the September meeting, I expect T-bill yields to stay firmly below those of the RRP. As such, RRP balances should continue to rise, and Bitcoin, at best, will chop around these levels and, at worst, slowly leak lower towards $50,000. Let’s see how the cookie crumbles.

My shift in opinion keeps my hand hovering over the Buy button. I am not selling crypto because I am short-term bearish. As I will explain, my bearishness is temporary.

Runaway Deficits

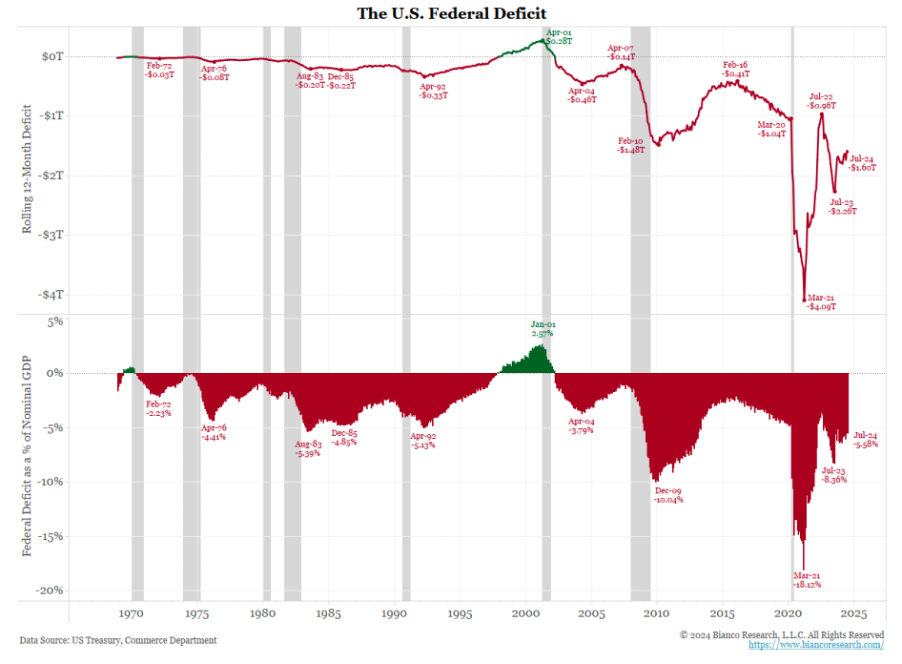

The Fed has done nothing to reign in the most significant contributor to inflation: government spending. The government will only spend less or tax more when it becomes too expensive to finance the deficit. The Fed’s so-called restrictive policy is all talk, and its independence is a cute story taught to gullible economist acolytes.

If the Fed won’t tighten conditions, the bond market will instead. Like the unexpected rise in 10-year yields after the Fed’s 2023 pause, the Fed’s 2024 rate cut will spur a move in yields toward the dangerous 5%.

Why is a 5% yielding 10-year Treasury bond so dangerous to the health of the Pax Americana fugazi financial system? To answer the question, it is because that is the level where Bad Gurl Yellen believed it necessary to step in and inject liquidity last year. She knows more than I about how fucked the banking system is as bond yields bear steepen; I can only guess at the magnitude of the problem given her actions.

Like a dog, she has conditioned me to expect a response given certain stimuli. 5% 10-year Treasury bond yields will stop the stonk bull market in its tracks. It will also reignite worries over the health of non-Too Big To Fail bank balance sheets. Mortgage rates will rise and decrease housing affordability, a big issue for US voters this election cycle. All this could materialise before the Fed cuts rates. Given these circumstances and Yellen’s dogged loyalty to the Democratic party’s Manchurian candidate Kamala Harris, those red bottoms ‘bout to stomp all over the “free” market.

Obviously, Bad Gurl Yellen will only stop once she has done everything possible to ensure Kamala Harris is elected as the US President. First, she will start running down the Treasury General Account (TGA). Yellen might even provide forward guidance on her desire to deplete the TGA so the market quickly reacts how she wishes … pump up the jam! She will then instruct Powell to cease quantitative tightening (QT) and possibly restart quantitative easing (QE). All these monetary machinations are positive for risk assets, especially Bitcoin. The magnitude of the money supply injections must be large enough to counteract the rising RRP balance, assuming the Fed continues cutting rates.

Yellen must act quickly, or the situation could metastasise into a full-blown voter crisis of confidence in the US economy. That would spell death for Harris at the ballot box … unless some trove of mail-in ballots is miraculously discovered. As Stalin may have said, “It’s not the people who vote that count; it’s the people who count the votes.” I kid … I kid ;).

If this scenario occurs, I expect intervention to begin in late September. Between now and then, Bitcoin will, at best, continue to chop, and altcoins could dive deeper into the gutter.

I went on record saying that the bull market begins anew in September. I have changed my mind, but it doesn’t affect my positioning at all. I’m still long as fuck in an unlevered fashion. The only additions to my portfolio will be increasing position sizes in solid shitcoin projects at deeper and deeper discounts to my perception of fair value. Tokens of projects with users that pay real money to use a product will surge once the fiat liquidity taps are predictably ratcheted higher.

For those of you who are professional traders with monthly PNL targets or weekend warriors who use leverage, soz, my short-term market predictions are no better than flipping a coin. I have a long-term bias that the flunkies who run the system will resort to printing money to fix all problems. I write these essays to contextualise current financial and political events and observe whether my long-term hypothesis remains valid. But I promise one day my short-term predictions will be more accurate … maybe … I hope ;).

Want More? Follow the Author on Instagram and X

The post Boom Times … Delayed appeared first on BitMEX Blog.

{kind=link}