Key Insights

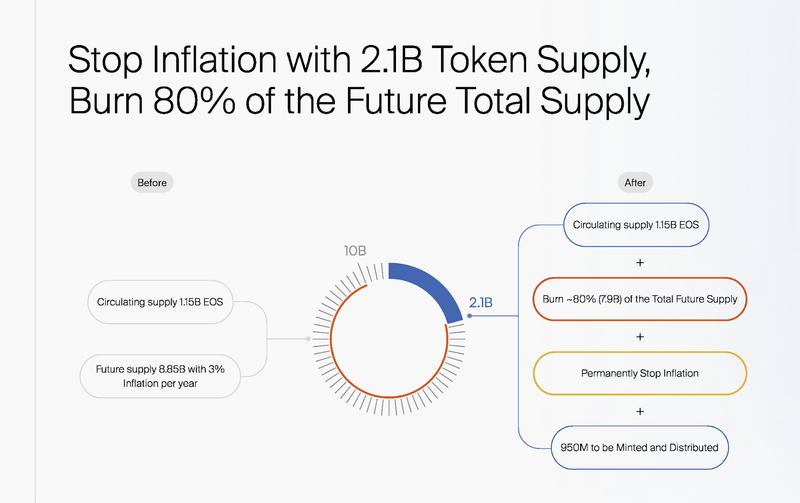

- The maximum EOS token supply was reduced from 10 billion to 2.1 billion with the release of EOS System Contracts v3.4.0, introducing a fixed supply for the network.

- The EOS network experienced growth QoQ, with daily transactions increasing by 33% and active addresses rising by 5.5%.

- EOS climbed in market cap rankings from 90th to 79th during the quarter, despite a 48.18% price drop from $1.10 to $0.57.

- Tether announced it would stop minting USDT on EOS, which could lead to new opportunities for other stablecoins or DeFi solutions within the ecosystem.

- Introduction of the exSat Network expanded EOS’s blockchain capabilities with the launch of a Bitcoin scaling solution built on EOS, enhancing its role in cross-chain interoperability and scalability.

Introduction

EOS (EOS) is a Layer-1 blockchain that operates on a Delegated Proof-of-Stake (DPoS) consensus mechanism, built with the open-source Antelope protocol formerly known as EOSIO.

The EOS Network Foundation is a non-profit organization formed from a community-driven initiative to take over the project, ensuring the protocol’s continuity and revitalizing the ecosystem. This grassroots effort has led to several key upgrades, including the introduction of inter-blockchain communication (IBC), an Ethereum Virtual Machine (EVM) solution, and the successfully completed Savannah hard fork bringing transaction speed down from 6 minutes to 1 second launched on the 25th of September. For an in-depth look at EOS, please refer to our Initiation of Coverage report (IOC).

Website / X (formerly Twitter) / Telegram

Key Metrics

Financial Analysis

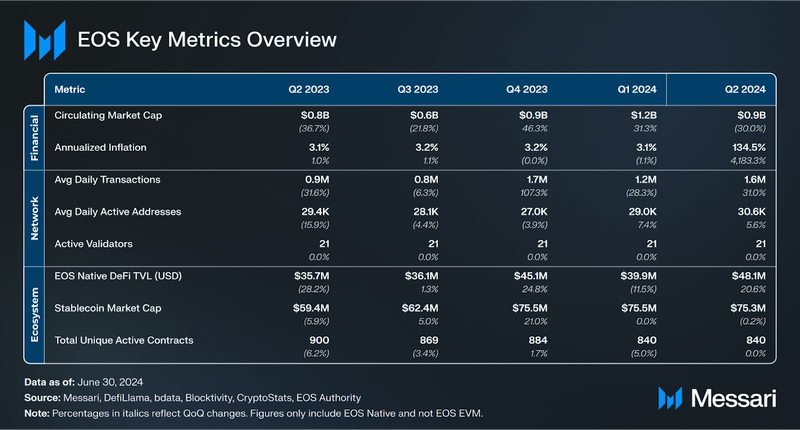

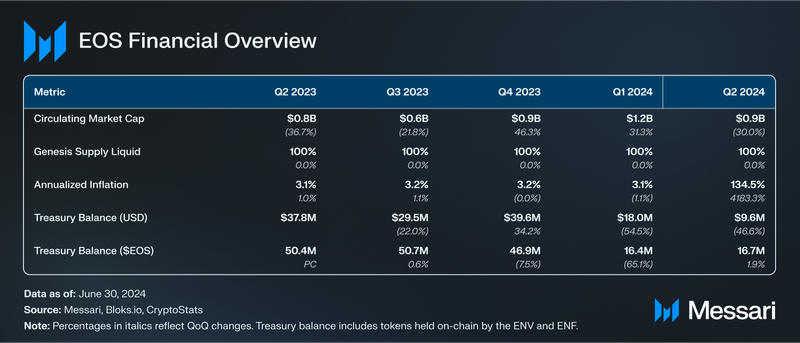

EOS’s price fell in line with the rest of the market, declining 48.18% from $1.10 to $0.57 QoQ. Despite a general price recovery across the broader crypto market in Q2’24, EOS experienced a downward trajectory. This is in contrast to majors like Bitcoin, which showed signs of recovery during the same period.

The overall crypto market did see a downward trend in market capitalization during this quarter, and this broader decline has been reflected in EOS’s market performance as well. EOS’s circulating market capitalization shrank by 25% QoQ, falling from $1.2 billion to $900 million. Despite the decrease in market cap, EOS improved its position in market cap rankings, climbing from 90th in Q1’24 to 79th in Q2’24. Nonetheless, the rise in ranking shows that while EOS struggled with its price and market cap, it fared better than many other similar assets in relative terms.

EOS Token Unlocks and Staking

Source: EOS Network

Updated EOS Tokenomics Model

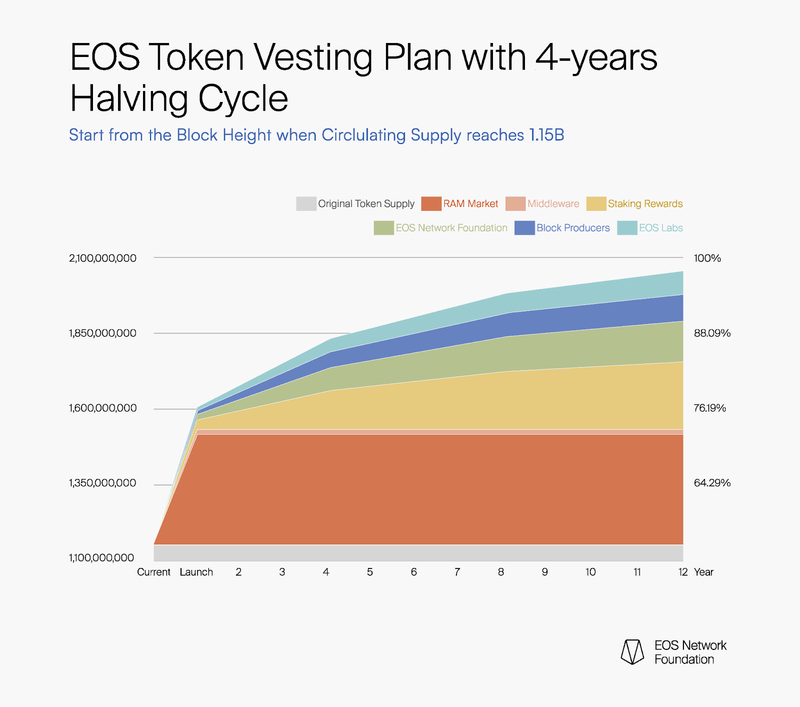

In Q2’24, EOS implemented a transformative shift in its tokenomics reducing the maximum total token supply from 10 billion to 2.1 billion and implementing a halving schedule to reduce the rate of inflation over time. The EOS Network Foundation (ENF) proposed the new model, which was designed to provide long-term stability and predictability for users and investors. The most prominent aspect of this change is the capping of the maximum total EOS supply at 2.1 billion tokens, significantly reducing the maximum token supply and also introducing a halving mechanism to reduce future inflation over time.

- Fixed Supply and Supply Cap: The key feature of the new tokenomics is the cap on the total supply of EOS at 2.1 billion tokens. Previously, EOS had a potential maximum supply of 10 billion tokens, but with the introduction of a fixed supply, and the burning of approximately 80% of future tokens, the Fully Diluted Value (FDV) of EOS has been reduced by 80%. This move provides a more predictable and stable economic environment for users and investors.

- Four-Year Halving Cycle: In addition to these allocations, the new model introduces a four-year halving cycle. This halving cycle is designed to gradually reduce the number of newly released tokens, mimicking the token issuance model used by Bitcoin. The goal is to moderate the token supply over time, reducing inflationary pressure. Between April 1 and June 30, 2024, the EOS token supply increased by 33.61%, primarily due to a one-time mint. As the new four-year halving cycle takes effect, the influx of new tokens into the market will gradually decrease, moderating the token supply over time and reducing inflationary pressure in future quarters.

- Allocation of Minted Tokens: The new tokenomics also involved the future minting of 950 million EOS tokens to support various ecosystem activities:

- 85 million EOS for ecosystem growth and partnerships through EOS Labs.

- 15 million EOS for public goods funding.

- 100 million EOS for block producer rewards.

- 150 million EOS allocated to the ENF for continued network development.

- 250 million EOS for staking rewards, as outlined in the staking mechanism.

- 350 million EOS dedicated to the RAM market, a critical component for ensuring data storage and transaction processing on the EOS blockchain.

Updated EOS Staking Mechanisms

The new EOS staking mechanism introduces several important updates aimed at improving both the user experience and the network’s long-term security. One of the key features is the introduction of high-yield staking rewards, where users can earn compounded returns over time by staking their EOS tokens. This is supported by a dedicated pool of 250 million EOS, which will release 31.25 million EOS annually as rewards, ensuring consistent engagement from the EOS community.

In addition to these rewards, the unstaking period has been extended from 4 to 21 days, providing greater network stability and discouraging short-term speculative behavior. This extended lock-up period helps ensure that stakers remain committed to the network for longer durations, enhancing its overall security.

EOS has also streamlined the staking process by removing the need for users to vote for 21 block producers or designate a proxy. This change simplifies the staking experience, making it more accessible to a wider range of participants. Along with these improvements, block producers now receive additional incentives in the form of network-generated fees, tied to the growing demand for the network. These incentives are layered on top of their traditional block rewards, further encouraging their active contribution to the network’s security and scalability.

Overall, the revamped staking mechanism not only offers increased returns for participants but also strengthens the network by promoting long-term participation, simplifying engagement, and ensuring adequate incentives for block producers to support the EOS ecosystem.

To date, over 150M EOS has been staked, representing 7.14% of the total locked supply. Since the new staking program was launched, over 100M has been staked in 4 months, with potential staking programs launching on centralized exchanges in the future.

Network Analysis

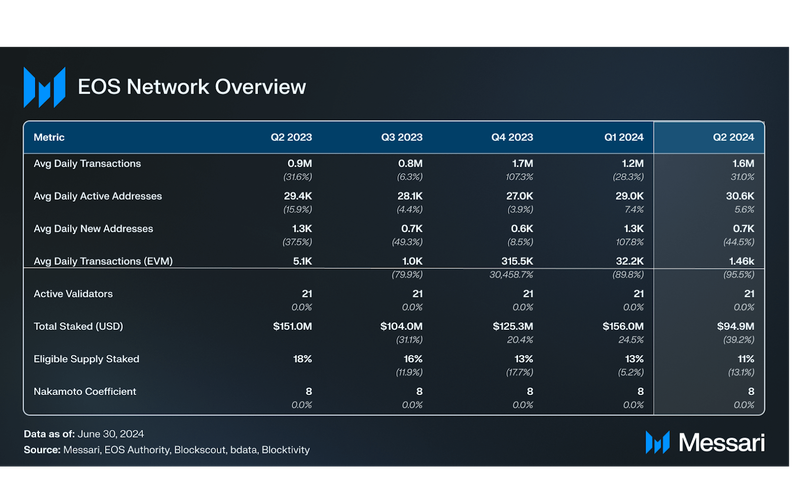

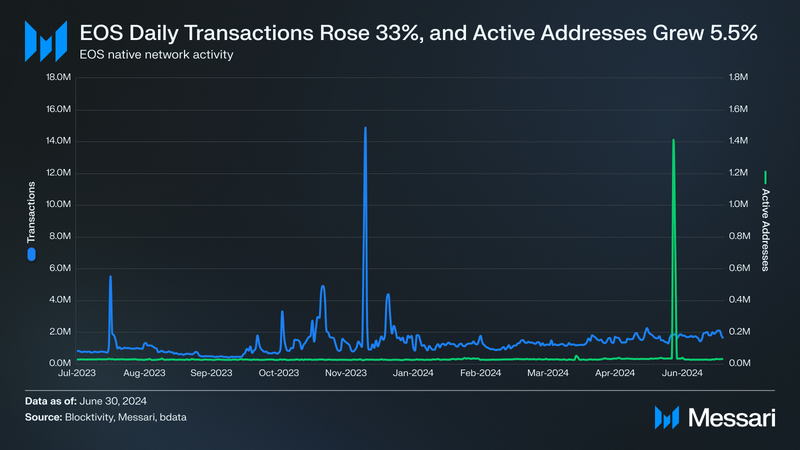

In Q2’24, both the daily active addresses (DAAs) and daily transactions on the EOS network saw increases QoQ. Daily transactions rose from 1.2 million to 1.6 million, representing a 33.33% increase. Similarly, the number of daily active addresses grew from 29.0K to 30.6K, reflecting a 5.52% increase.

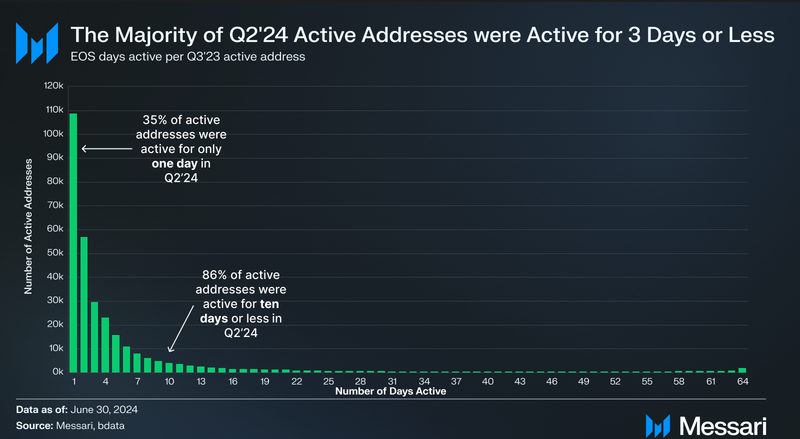

EOS saw growth in unique active addresses during Q2’24, reaching 309,421 addresses, representing a 10.01% increase QoQ. However, engagement levels, measured by the number of days each address was active, showed that the majority of addresses had low activity. Specifically, 35.10%, 18.34%, and 9.55% of addresses were active for 1, 2, and 3 days, respectively, accounting for 62.99% of total addresses. Notably, 35.10% of addresses were only active for one day, an increase of 25.36% QoQ. Additionally, 86.43% of wallets were active for 10 days or fewer during Q2’24.

On the other hand, the EOS EVM average daily transactions dropped from 32,000 to 1,046, a 96.73% decrease QoQ. Inscriptions primarily drove the spike in Q4’23 and Q1’24 transactions; however, EOS is now returning to pre-inscription levels, reverting closer to the 1,000 daily transaction average observed in Q3’23.

Upgrades and Technical Developments

On the technical front, EOS is gearing up for several major upgrades aimed at enhancing performance and scalability. A significant step was the launch of the Antelope Spring Beta 1.0 on the Jungle testnet on May 25, 2024, which lays the groundwork for the coming Savanna Consensus mechanism. Scheduled for implementation on July 31, 2024, the Savanna Consensus upgrade is expected to improve transaction finality and overall network efficiency, potentially increasing EOS’s performance by over 100 times. These advancements are critical for ensuring that EOS remains competitive in the evolving blockchain landscape, where high throughput and scalability are essential.

In addition to the consensus mechanism upgrade, the network has seen improvements in its RAM system with the launch of WRAM on April 17, 2024. WRAM adds transferability and increased utility through operating both on-chain and off-chain. Furthermore, 350 million EOS has been allocated for the development of the RAM market, aimed at optimizing network functionality and expanding use cases.

Ecosystem Analysis

Popular Contracts

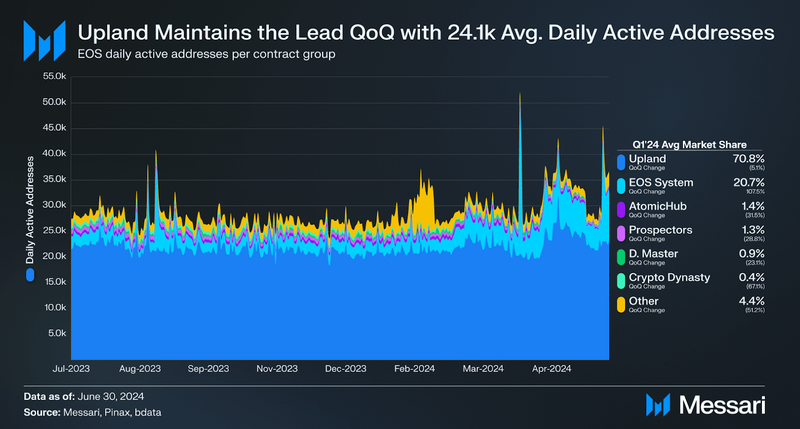

Virtual property game Upland maintained its lead QoQ, remaining the most popular EOS contract group by daily active addresses. In Q2’24, Upland averaged 24,110, up 9.59% from 22,000 QoQ.

Coming in second place is the EOS System Contract, which manages functions such as delegation and resource management. The daily active addresses averaged 6,870 in Q2’24, up 137.93% from a previous average of 2,900.

Ecosystem Updates

Further, the EOS network is expanding its capabilities with the introduction of new features and initiatives. Among the key developments is the exSat Network, a Bitcoin scaling solution built on EOS. This initiative highlights the network’s efforts to broaden its functionality within the blockchain ecosystem. The exSat Network is expected to utilize over 106 GB of EOS RAM, increasing the significance of RAM in the EOS ecosystem. exSat mainnet went live on October 23rd with 53% of BTC hash rate and 4,100 BTC staked to the network.

Additionally, the network’s infrastructure is being strengthened through the allocation of 5 million EOS to Greymass for middleware development. This investment aims to enhance the network’s technical infrastructure, supporting scalability and future growth.

DeFi

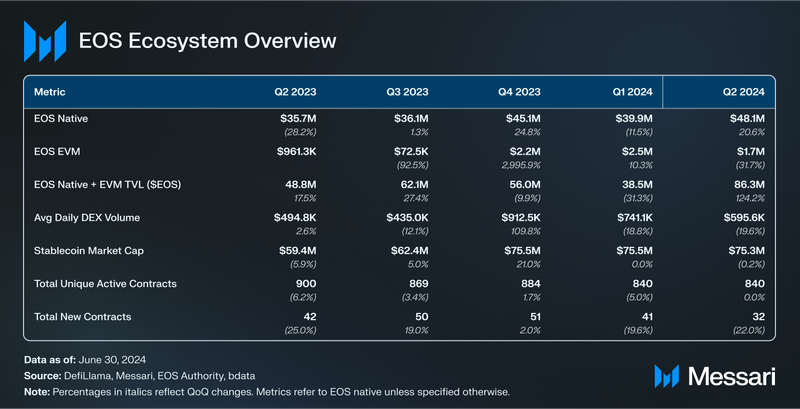

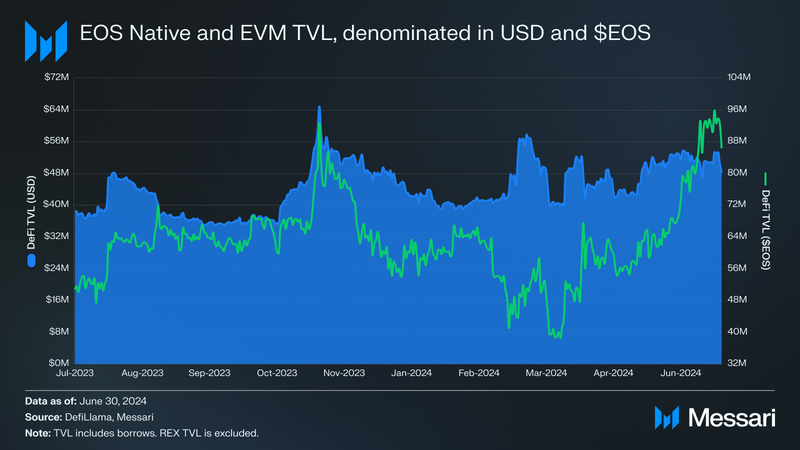

EOS’s Native DeFi Total Value Locked (TVL) increased by 20.55% QoQ, rising from $39.9M to $48.1M. This growth signals increased user activity and capital allocation within the EOS DeFi ecosystem. However, the EOS EVM TVL saw a decline during the same period, dropping 32.00% QoQ from $2.5M to $1.7M, reflecting reduced activity or liquidity in the EVM-compatible segment of the network.

Defibox continues to hold the largest share of EOS Native TVL QoQ, maintaining its lead with its swapping and lending services. Meanwhile, PayCash, a decentralized exchange and fiat onramp platform that facilitates transactions between cryptocurrencies and traditional currencies, has solidified its position in second place, holding a substantial portion of the EOS Native TVL.

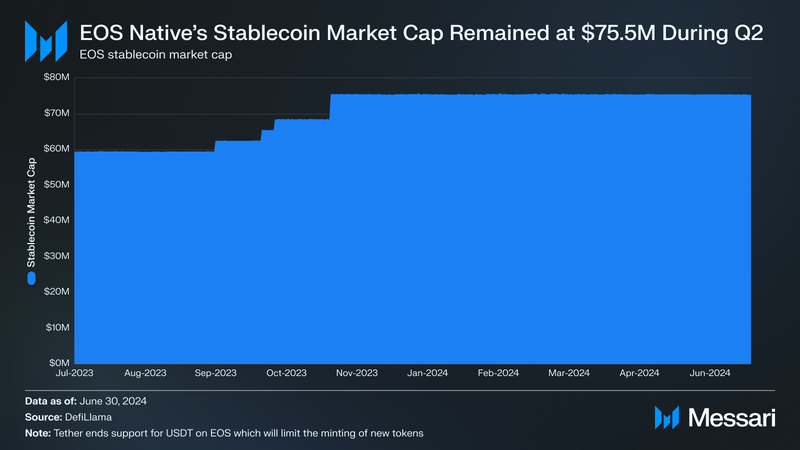

On June 24, 2024, Tether, the issuer of the world’s largest stablecoin USDT, announced it would no longer mint USDT on the EOS blockchain. This decision is significant, as USDT has been a cornerstone of the crypto market, offering stability and facilitating a wide range of decentralized finance (DeFi) activities across multiple blockchains. Stablecoins like USDT are crucial in liquidity pools, lending platforms, and decentralized exchanges, so the loss of direct USDT support could have a notable impact on EOS’s DeFi ecosystem.

Although EOS’s native stablecoin market cap remained steady at $75.5 million, continuing the trend quarter-over-quarter (QoQ), this figure is composed entirely of USDT. As Tether begins the process of redemptions, this number is set to change in the coming quarters, potentially leading to a realignment in the stablecoin landscape within the EOS network

Tether’s decision to discontinue minting USDT on EOS is part of a broader strategy to optimize its ecosystem and resource allocation. Although EOS represents a small portion of USDT’s total supply—only $17 million, which accounts for less than 0.1% of its $113 billion supply across 16 blockchains—the decision reflects Tether’s focus on larger networks such as Tron and Ethereum, which account for $59 billion and $52 billion of USDT supply, respectively.

This move follows a pattern, as Tether has previously ceased USDT support on other blockchains, such as Kusama, Bitcoin Cash’s Simple Ledger Protocol (SLP), and the Omni Layer Protocol. Nevertheless, Tether continues to expand onto new networks, such as The Open Network (TON). Its broader strategy includes offering additional stablecoins, such as CNHT (Chinese Yuan), EURT (Euro), and XAUT (gold-backed), to expand its range of financial products across global markets.

Tether’s decision to stop minting USDT on EOS introduces some challenges for the network, particularly in its DeFi ecosystem. However, Tether will continue to honor existing USDT on EOS and allow redemptions, ensuring current holders are not affected. USDT plays a key role in liquidity and user engagement, and the absence of native support could affect EOS’s ability to maintain its current DeFi activity. This shift reflects the evolving dynamics of blockchain ecosystems and highlights the competitive landscape smaller networks like EOS face when securing support from major players in the space.

Development

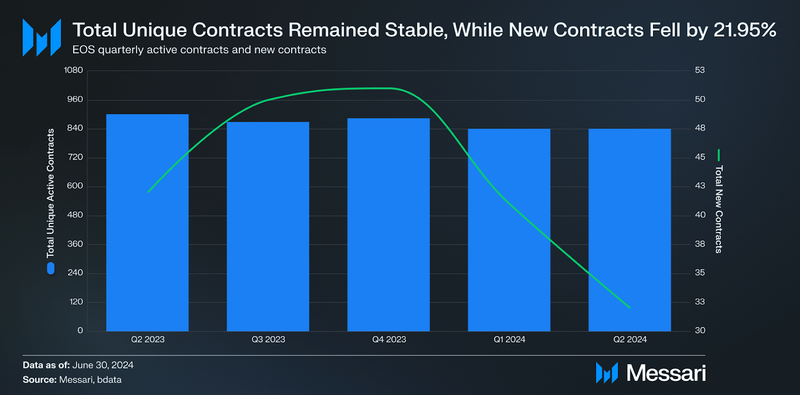

Ecosystem development, measured by the number of unique contracts called and new contracts, saw a slight decline in Q1. The number of unique contracts called throughout the quarter remained stable at 840 QoQ. However, the number of new contracts called decreased by 21.95% QoQ, falling from 41 to 32.

Closing Summary

In Q2 2024, EOS experienced several notable developments that have shaped its trajectory within the blockchain ecosystem. The most significant change was the transition to a fixed token supply model, capping the total supply at 2.1 billion EOS tokens. This move marks a shift away from the previous inflationary model and introduces long-term predictability for token holders. The introduction of new tokenomics features, including staking rewards and vesting schedules, aims to foster stability and sustainable growth within the network.

In the DeFi space, EOS saw a 20.55% increase in Native DeFi TVL, with platforms like Defibox and PayCash leading the way. However, challenges remain, particularly with Tether’s decision to stop minting USDT on EOS, which could impact liquidity and user activity in the DeFi ecosystem. Despite these challenges, EOS continues to expand its infrastructure, with initiatives such as the exSat Network and ongoing middleware development aiming to increase the network’s utility and adoption.

{kind=link}