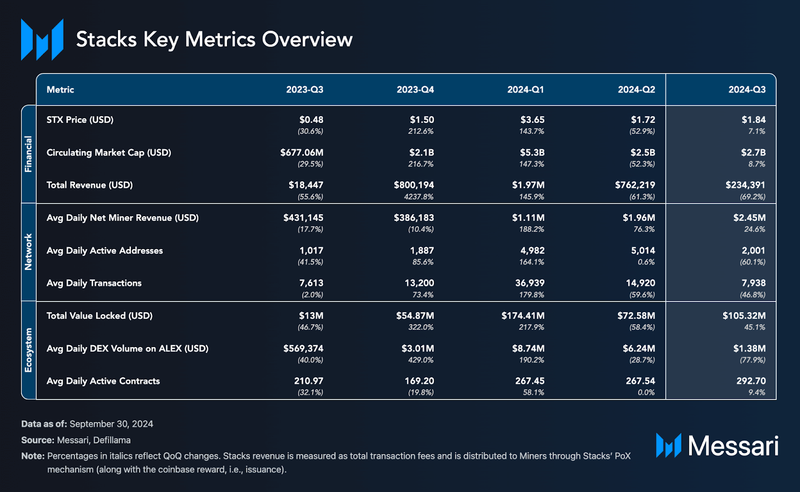

Key Insights

- From Q1 to Q3 2024, TVL in USD decreased by ~39.61%, while TVL in native STX tokens increased by ~19.74%, indicating maintained native token engagement despite the overall fluctuating value of assets in USD.

- The SEC ruled in favor of Stacks on July 12, 2024, concluding a three-year investigation into its 2017 token sale with no recommendation for enforcement action.

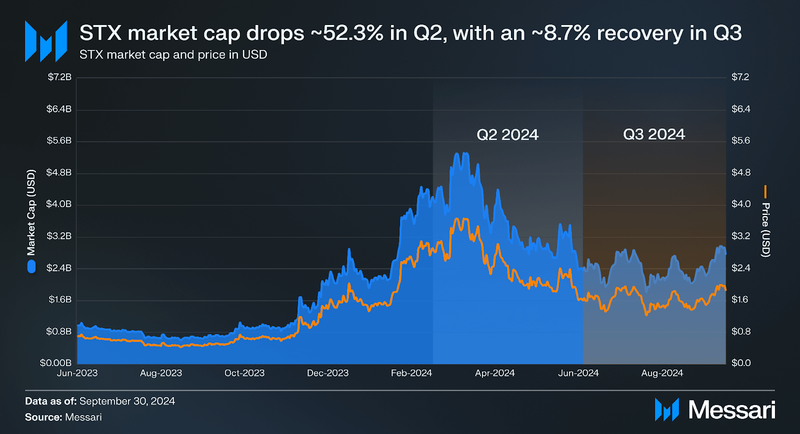

- Despite a ~52.33% decline in market cap in Q2, STX saw an ~8.70% rebound in Q3, bringing its market cap to ~$2.75 billion, increasing its position from 43rd to 39th overall in market cap rank.

- The Nakamoto upgrade made significant progress, reaching its hard fork milestone – introducing improvements in block production speed, security, and Bitcoin finality.

- Net burn increased ~135.40% from Q1 to Q3, while net rewards grew ~110.00%, reflecting strong reward distribution despite declining stacker and miner participation in Q3.

Primer

Stacks (STX) is a Bitcoin Layer-2 (L2) that allows smart contracts and decentralized applications to use Bitcoin as a secure base layer. Transactions are executed on Stacks and settled on Bitcoin, leveraging Bitcoin’s security and capital while offering arbitrary programmability that is not possible on its scriptable settlement layer.

Stacks has knowledge of the full Bitcoin state, thanks to its Proof-of-Transfer (PoX) consensus mechanism and Clarity programming language, allowing it to read from Bitcoin at any time. With PoX, miners commit BTC to eligible Stacks addresses that participate in consensus. This process of STX token-holders participating in consensus and earning BTC from miners is known as Stacking. PoX runs parallel to Bitcoin’s Proof-of-Work (PoW) consensus, hashing and settling Stacks transactions on Bitcoin. Metadata from newly mined Stacks blocks are anchored to every Bitcoin block, allowing users to verify the canonical Stacks blockchain via Bitcoin blocks.

The new Nakamoto upgrade strengthens Stacks’ integration with Bitcoin by (i) introducing sBTC for non-custodial BTC transfers, (ii) enabling faster block production, (iii) improving Bitcoin finality, and (iv) reducing the chances of Maximal Extractable Value (MEV) exploitation.

Website / X (Twitter) / Discord

Key Metrics

Financial Analysis

Market Cap and Price

Relative to Bitcoin and Ethereum benchmarks, which saw their respective circulating market caps decrease by ~12.00% and ~6.00% in Q2 2024, Stacks experienced a stronger decline. Its circulating market cap dropped ~52.33% to ~$2.50 billion, lowering its market cap ranking from 28th to 43rd overall.

However, in Q3 2024, Stacks saw a modest recovery, with its circulating market cap increasing ~8.69% to ~$2.75 billion, bumping its market cap rank to 39th overall. The price of STX (USD) mirrored this trend, declining ~52.92% in Q2 but rebounding ~7.09% in Q3.

Despite this volatility, when comparing Q3 to the beginning of Q1 (January 1, 2024), Stacks saw positive growth. The circulating market cap rose ~20.94% from ~$2.27 billion at the start of the year, and STX’s price increased ~15.99% from ~$1.59 during the same period.

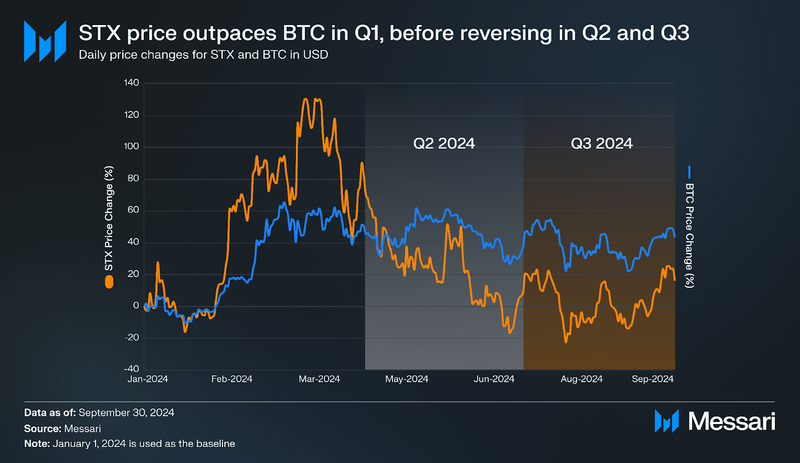

As a Bitcoin L2, Stacks is closely integrated with Bitcoin not only through its technical architecture but also in terms of its price activity. In early 2024, STX deviated from BTC’s price trajectory, growing by ~130.06%, outpacing BTC’s ~61.45% growth in the same period.

This trend reversed in Q2, where the price of STX declined by ~52.92%, while BTC only declined by ~9.85%. By the end of Q3, BTC had gained ~43.00% since January 1, 2024, while STX only increased ~16.00% over the same period.

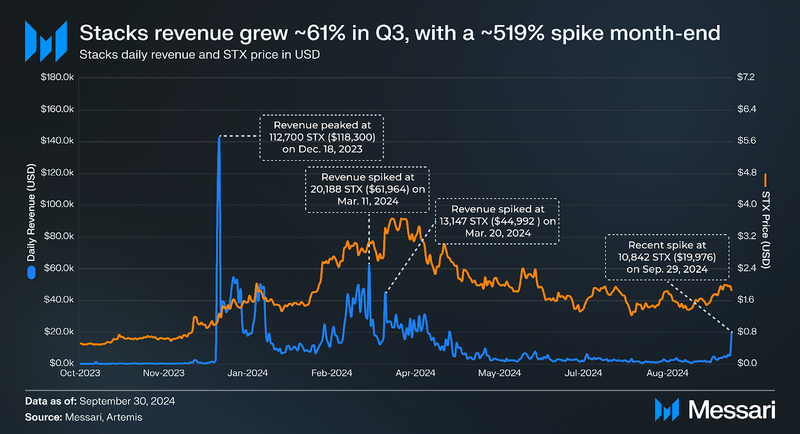

Revenue

Stacks revenue is measured as total transaction fees and is distributed to Miners through Stacks’ PoX mechanism (along with the coinbase reward, i.e., issuance). Throughout 2024, revenue and price have seen notable volatility.

In the grander scheme of things, from Q1 to Q3 (excluding the September 2024 spike), revenue in USD terms decreased ~66.77%, falling from ~$15,572 to ~$5,174. In STX terms, the decline was less pronounced at ~38.23%, with revenue dropping from ~4,261 STX to ~2,632 STX. This indicates an overall reduction in transaction volume and user activity on the network.

The most significant change occurred in Q2, where revenue dropped ~79.30% to ~$3,223. In Q3, Stacks saw a partial recovery, with revenue increasing ~60.52% to ~$5,174 by the end of September. In STX terms, revenue rose ~40.51% during the same period.

Despite this recovery, revenue and price remained below the highs recorded in Q1, largely driven by key events earlier in the year. In December 2023, revenue peaked at 112,700 STX ($118,300) following the release of STX20 inscriptions. Further spikes occurred in March 2024, with a rise to 20,188 STX ($61,964) after the Argon pre-launch testnet was announced and again when revenue reached 13,147 STX ($44,992) following the approval of SIP-021: Nakamoto Release.

While excluding the September 2024 spike – driven by the successful activation of the Nakamoto Testnet on September 27, 2024 – offers a more conservative view of the Q3 recovery, the event’s impact cannot be overlooked. Including the spike, revenue increased ~519.78% QoQ to ~$19,976, in contrast to the ~60.52% QoQ increase excluding such. In STX terms, revenue grew ~478.71%, including the spike, and ~40.51% without. Lastly, the spike significantly shifted the overall revenue trend, changing what would have been a ~66.77% decrease (in USD terms) from Q1 to Q3 into a ~28.28% increase, with Q3 revenue surpassing Q1 levels.

Network Analysis

Usage

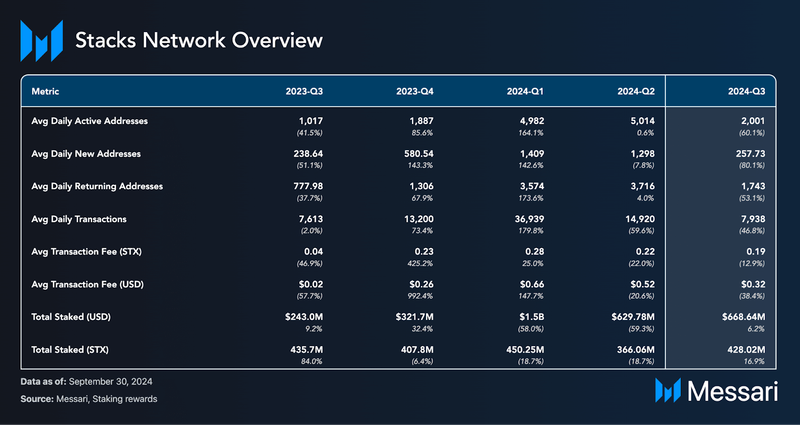

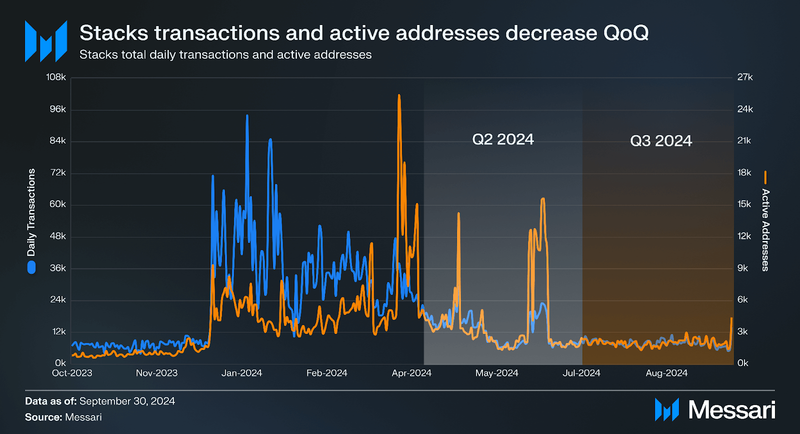

To paint a bigger picture, average daily active addresses dropped by ~92.35%, from 20,912 in Q1 to ~1,600 by the end of Q3, without the September spike. Including the spike, the drop reaches ~78.97%. The overall decline followed strong user engagement in early 2024, driven by events like STX20 inscriptions, the Neon testnet release, and various ecosystem developments (i.e., ALEX, Velar, BitFlow, and StackingDAO).

Zooming into Q1 to Q2, average daily active addresses fell ~92.50% from 20,912 to 1,568. However, between Q2 and Q3, excluding the September spike, average daily active addresses increased ~0.06% from 1,568 to 1,600. Factoring in the spike, they increased ~180.42%.

Similarly, total daily transactions from Q1 to Q3 dropped ~58.71% from 32,696 to 13,826. During Q1 to Q2, total daily transactions dropped ~80.63% from 32,696 to 6,332. Between Q2 and Q3, excluding the September spike, total daily transactions continued to decline ~16.47% from 6,332 to 5,289. However, factoring in the spike, total daily transactions increased ~118.35% from 6,332 to 13,826.

The spike in active addresses that occurred in April (25,393), May (14,235), and June (15,525) can be attributed to various ecosystem developments, which inherently drove new users to the L2.

With the decline in user engagement, transaction fees (both in STX and USD terms) naturally decreased from Q2 to Q3, with average fees in STX terms dropping ~12.90% to 0.19 STX and in USD terms dropping ~38.40% to ~$0.32. Despite the decline in network activity, the total amount of staked STX increased ~16.90% QoQ and dropped ~4.94% when comparing Q3 to Q1.

Stacks Improvement Proposals (SIP)

From January to September 2024, several SIPs were introduced to improve the efficiency, security, and user experience of Stacks.

SIP-021: Nakamoto Release

Proposed on Feb. 14, 2024, the Nakamoto upgrade was formally introduced via SIP-021, representing a significant change in Stacks’ architecture. Key differences involved Bitcoin finality, reducing MEV opportunities, and enabling faster block production by decoupling Stacks’ blocks from Bitcoin’s blocks. It also laid the groundwork for sBTC, an asset pegged to the value of BTC, allowing for 1:1 redemptions and trustless transfers between Bitcoin and the Stacks ecosystem. Full details can be found in the latest whitepaper. Voting for the proposal concluded on March 9, 2024, with unanimous approval from Stackers and the endorsement of all three Consideration Advisory Boards (CABs).

SIP-025: Simplifying the Signature Generation Schema for Nakamoto Activation

Proposed on July 23, 2024, SIP-025 served as a “rider” SIP to SIP-021, designed to temporarily simplify the signature generation process during the Nakamoto Activation phase. SIP-021 proposed using Weighted Schnorr Threshold Signatures (WSTS) for block validation. However, WSTS is complex and not required until future releases tied to sBTC are rolled out. SIP-025 introduces a temporary, simplified method for generating signatures using concatenation, similar to Bitcoin’s P2SH multi-sig. Once Stacks 3.0 is activated, the full WSTS system will be implemented in Stacks 3.1, aligning with future sBTC releases. This SIP was also approved.

SIP-027: Non-Sequential Multi-Sig Transactions

Proposed on July 23, 2024, SIP-027 suggested a new format for multi-sig transactions. It eliminated the need for a fixed signer order, improving the user experience for signing multi-sig transactions without sacrificing security or increasing transaction size. It was designed to coexist with the current format established in SIP-005, allowing flexibility and backward compatibility. Voting for the proposal ended on August 16, 2024, with 100.00% of solo and pool Stackers voting in favor.

Nakamoto Developments

The Nakamoto upgrade reached several major milestones in Q2 and Q3 in accordance with Stacks’ proposed rollout plan.

- Apr. 4, 2024: Stacks developers selected Bitcoin block 839,444 to be the instantiation block/beginning of the Nakamoto upgrade (expected to be on Apr. 16, 2024).

- Apr. 22, 2024: The Nakamoto instantiation block (Bitcoin block 840,360) arrived, officially starting the Nakamoto rollout, albeit slightly later than the original expectation.

- Jul. 11, 2024: Stacks developers announced that Nakamoto “is now code complete” ahead of the target date of Jul. 15, 2024. Testing followed until the activation occurred on Aug. 28, 2024.

- Aug. 28, 2024: Official start of the Nakamoto Activation Window. Network operators were given one stacking cycle to upgrade, with final activation after the handoff between Cycle 92 and Cycle 93.

- Sept. 20, 2024: After the successful Signer handoff, Stacks developers selected Bitcoin block 864,864 for the hard fork, scheduled for Oct. 9, 2024.

- Sept. 27, 2024: Following a successful Nakamoto hard fork on testnet, Stacks developers announced that a “slight adjustment to the mainnet hard fork block” would be required after bugs were detected. With the upgrade, Stackers will now be responsible for validating transactions on the Stacks network, which will require them to run an operational signer. Additionally, Stackers may need to re-stack or re-delegate after the upgrade is completed.

sBTC Developments

sBTC is the first decentralized, non-custodial Bitcoin peg that allows smart contracts to write back to the Bitcoin blockchain. Unlike other synthetic BTC variants, like wBTC (wrapped BTC) and RBTC (Rootstock BTC), sBTC does not rely on federations or centralized custodians. Instead, sBTC uses an open network in which anyone can help maintain the peg. The exact details can be read in the original whitepaper.

The sBTC rollout plan outlined by Bitcoin Writes on April 30, 2024, covers two main phases:

- Bootstrapping Phase: This initial phase involved launching sBTC with a limited group of Signers, who will be selected through community voting. These Signers will maintain the sBTC peg wallet, ensuring a 1:1 backing of BTC by sBTC.

- Signer Rotation Phase: Planned for Q1 2025, this phase will see the full decentralization of the Signer set, transitioning from the bootstrapping group to an open and dynamically rotating Signer set.

In the bootstrapping phase, the Nakamoto Activation sequence kicked off on Aug. 28, 2024, with the sBTC mainnet release anticipated approximately four weeks later in October. Several notable sBTC developments have since occurred, including:

- Apr. 9, 2024: Portal Finance announced their support for Stacks and sBTC via their Portal DEX Network.

- Jun. 21, 2024: Critical bounties were announced, one of which was to build a centralized website for a Bitcoin L1 to Stacks L2 Bridge (sBTC).

- Jul. 19, 2024: BitGo announced its integration with Stacks, which includes support for sBTC, joining the Stacks Signer network, supporting SIP-10 tokens, and enabling STX stacking directly from their wallet.

- Sept. 12, 2024: Trust Machines launched Granite, a new Bitcoin lending protocol on Stacks using sBTC as the bridge

- Sept. 17, 2024: Aptos Network announced its integration with sBTC.

- Sept. 20, 2024: Solana announced its integration with sBTC.

Signers

While Stacking has been live since launch, the Nakamoto upgrade introduced a new role of “Signer.” Signers validate and sign blocks produced by miners, who enable programmable Bitcoin via sBTC by processing deposits and withdrawals of BTC into the system. More details can be read here.

As of Aug. 2, 2024, Stacks had 39 Signers (e.g., Blockdaemon and Figment), which can be monitored live through this dashboard. In Q2 and Q3, eight new signers joined the network, including:

- Aptos Network: A Layer-1 blockchain focused on scalability, safety, and reliability.

- Luxor: A Bitcoin mining pool and blockchain technology company that offers mining software solutions and services.

- BitGo: An institutional digital asset custody, trading, and financial services provider.

- InfStones: An infrastructure provider that offers cloud-based staking, API, and node management services.

- Edgevana: An infrastructure provider that offers white-label validating.

- Kiln: An infrastructure provider that offers “Staking as a Service” solutions.

- Restake: An automated restaking service with institutional standards.

- SenseiNode: An infrastructure provider that offers secure node management and staking services for developers and institutions across multiple networks.

Stacking

As mentioned in the Q4 2023 Stacks report – Stacking, similar to mining on Bitcoin, is largely dominated by pools. Because of this, one should keep in mind that the number of participants across decentralized and custodial stacking pools is considerably lower when counted as unique Stackers. It is impossible to know how many participants are in the custodial pools as the data is not directly onchain.

Regardless, the system operates as a feedback loop driven by the interaction between miners and Stackers through the Proof-of-Transfer (PoX) mechanism. Miners burn BTC to produce blocks, while Stackers lock STX to support consensus and receive BTC rewards. This creates a cycle where increased miner participation boosts rewards for Stackers, making Stacking more attractive – more Stackers improve network security, drawing more miners to burn BTC in competition for block rewards.

Miners and Stackers

The number of daily miners increased ~25.90% from Q1 to Q2 2024. However, this was followed by a ~44.50% decline in Q3, bringing the total number of daily miners down ~30.10% compared to Q1.

Similarly, the average number of daily Stackers fell, decreasing ~47.50% from Q1 to Q2 and dropping another ~52.60% in Q3. The overall loss of Stackers between Q1 and Q3 was ~75.10%. This sharp reduction in Stackers led to less STX being locked in the network, which directly impacted miner engagement and incentives.

Net Burn and Net Stack

The average daily net burn experienced a significant rise from Q1 to Q2, increasing ~280.40% as a result of the growing number of daily miners. However, in alignment with the daily miner decline, net burn dropped ~38.10% in Q3. Despite this drop, net burn was still up ~135.40% compared to Q1.

The net stack metric followed a similar trend, up ~18.10% from Q1 to Q2 but down ~30.80% in Q3. The initial rise in net burn and net stack values in Q2 implies strong competition among miners during that period, likely driven by the rising BTC rewards caused by the increase in Stackers. However, as Stackers and miners withdrew in Q3, the reduction in locked STX and burned BTC led to a drop in these metrics.

Net Rewards and Expense Fees

Despite the reduction in miners and Stackers, net rewards in USD and BTC terms continued to increase in Q3. Net rewards rose ~17.60% (USD) and ~29.50% (BTC) from Q2, largely driven by fewer participants competing for the same rewards – allowing those remaining to capture larger shares. Between Q1 and Q3, net rewards increased by ~110.00% (USD) and ~76.80% (BTC).

Expense fees surged ~112.30% in Q2, driven by the increase in daily miners competing to include transactions in blocks. However, in Q3, expense fees dropped ~65.90%, reflecting the decline in both miners and Stackers. The decrease in fees reflects reduced competition and activity, aligning with the significant drop in miner participation.

Miner Revenue

Miner revenue increased ~76.30% from Q1 to Q2 as miners competed for block rewards. This trend continued into Q3, with miner revenue rising ~24.60% despite fewer miners being active. The decrease in competition allowed the remaining miners to capture larger shares of the available rewards, resulting in a ~120.60% increase in miner revenue between Q1 and Q3. In BTC terms, miner revenue grew ~85.50% over the same period.

Overall, the decline in miners and Stackers from Q2 to Q3 created a feedback loop that reduced network activity, as reflected in the drops in net burn, net stack, and expense fees. However, the remaining miners and Stackers benefited from larger rewards. As fewer participants competed, those that remained saw higher individual profitability, maintaining a balance in the network despite reduced overall engagement.

Ecosystem Overview

Stacks’ ecosystem saw growth from both established and newer protocols, including:

- ALEX: A protocol that includes an AMM, BRC-20 DEX, launchpad, bridge, and more.

- Arkadiko: A stablecoin issuer and DEX.

- Gamma: An NFT marketplace.

- StackingDAO: A liquid staking protocol.

- STX20: An inscription protocol.

- Leather and Xverse: Browser wallets.

- Bitflow: A DEX.

- Zest: A lending protocol.

- Hermetica: A platform for Bitcoin yield products.

- Velar: A perps DEX.

And many more, which can be explored here.

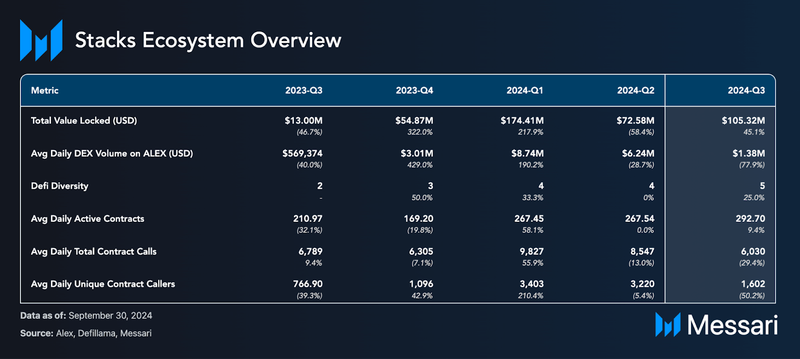

The overview table highlights various metrics, one of which is the DeFi Diversity score, reflecting the number of protocols that comprise the top 90.00% of DeFi TVL. A more diverse spread of TVL helps mitigate systemic protocol risks from adverse events. Stacks ended Q3 2024 with a DeFi Diversity score of 5. For reference, Ethereum and Solana’s DeFi Diversity scores were 32 and 12, respectively.

In addition to DeFi Diversity, the network also showed growth in developer activity. From Q1 to Q3, the number of active contracts increased ~9.40%, rising from ~268 to ~293, suggesting sustained interest in building on the network. However, this uptick in active contracts did not translate into increased user interaction. The number of total contract calls dropped ~29.40%, declining from ~9,827 in Q1 to ~6,030 in Q3. Looking more closely at unique contract callers, the metric dropped ~52.90% from ~3,403 in Q1 to ~1,602 in Q3.

Zooming in QoQ further illustrates these shifts. From Q1 to Q2, active contracts remained stable; however, both total contract calls and unique contract callers declined by ~13.00% and ~5.40%, respectively. This downward trend persisted from Q2 to Q3, where total contract calls fell ~29.40% and unique contract callers dropped ~50.20%. While the number of active contracts on Stacks grew modestly, the drop in contract calls and unique callers reflects a broader contraction in user participation throughout 2024.

DeFi

Total Value Locked (TVL)

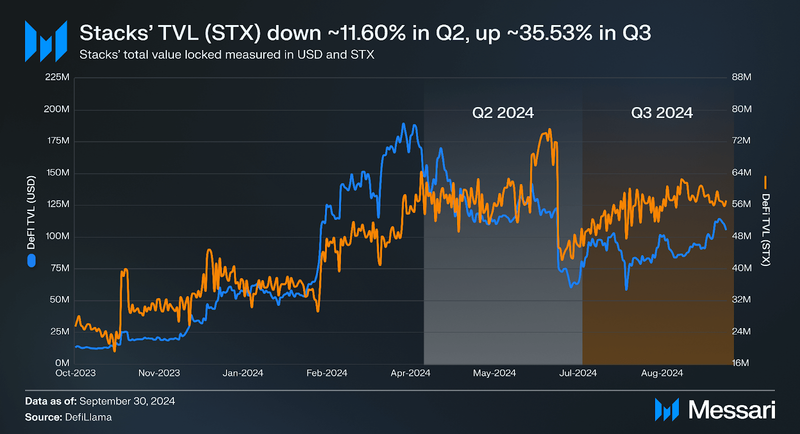

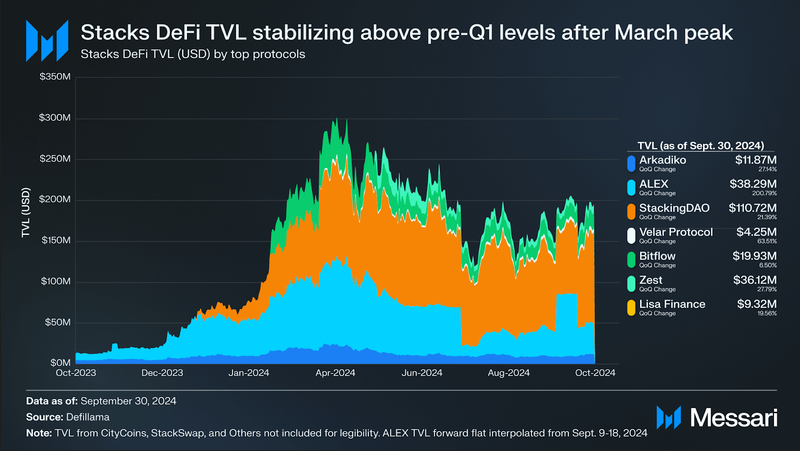

From Q1 to Q3, Stacks’ TVL showed contrasting trends in USD and STX terms. TVL (USD) reached an all-time high of ~$75.17 million on June 23, 2024, before declining ~39.61% as the dollar value of assets within the ecosystem decreased. However, TVL (STX) increased ~19.74%.

Zooming in on the quarterly changes, Q2’s TVL in USD and STX terms declined ~58.38% and ~11.61%, respectively. In Q3, the ecosystem recovered, with TVL in USD and STX terms increasing ~45.10% and ~35.49%, respectively. Despite the overall decline in TVL in USD terms from Q1 to Q3, the positive rebound in STX terms indicates a resilient ecosystem with increasing native token participation.

The total TVL across Stacks’ DeFi protocols showed significant growth in Q3, stabilizing above pre-Q1 levels after the March peak. ALEX, which had dominated TVL back in Q4 2023, and Velar Protocol led the way with triple-digit percentage increases in Q3. However, StackingDAO, now commanding ~48.02% of the market share with a TVL of ~$110.72 million, has overtaken ALEX, which accounts for ~16.60% of the total TVL at ~$38.29 million. Meanwhile, Zest and Bitflow maintain notable positions with ~15.67% and ~8.65% market shares, respectively, while Arkadiko and Lisa Finance capture ~5.15% and ~4.04%. Velar Protocol, despite its triple-digit growth, holds ~1.84% of the TVL.

Arkadiko

Arkadiko, a DeFi protocol enabling collateralized borrowing, saw its TVL drop ~61.39% in Q2 and increase ~27.14% in Q3. Based on a commercially reasonable search, no protocol-specific developments occurred during this time.

ALEX

ALEX increased its TVL by ~200.79% in Q3, recovering from an ~87.58% drop in Q2 following security hacks, after which they released various statements outlining a recovery plan. In Q2, they released the AMM SDK, which was used by XBot to introduce automated trading on Stacks via Telegram. The platform also announced cross-chain bridges for xBTC, xUSD, and Runes. In Q3, ALEX continued to expand its product offerings with the launch of ALEX V2, which integrates AMM and orderbook functionalities into a central liquidity hub. Most recently, they collaborated with STX City to introduce a bonding curve mechanism and partnered with Zeroshadow to strengthen security.

StackingDAO

StackingDAO’s TVL dropped ~23.87% in Q2 and grew ~21.39% QoQ in Q3. In Q2, the platform experienced a rebrand, followed by a partnership with Wintermute to unlock stSTX liquidity and a collaboration with OrangeCryptoHQ.

Bitflow

Bitflow saw its TVL drop ~59.62% in Q2, followed by an ~6.50% increase in Q3. In Q2, the protocol experienced a rebrand. Following this, they introduced new trading routes (i.e., STX to WELSH, ODIN, LEO, and PEPE) and launched an upgraded AMM pool for the USDA<>USDC pair. In Q3, to guarantee swap rates, they released a complete DEX aggregator and developed a Runes AMM. Most recently, they integrated its SDK with Stacks City, enabling native token swaps, and launched a new explorer tab for all assets.

Velar Protocol

Velar Protocol experienced a ~37.99% TVL drop in Q2, followed by a ~63.51% increase in Q3. In Q2, Velar introduced Multi-Hop Swaps for its DEX and later partnered with BOB to bridge the Bitcoin and Ethereum ecosystems. In Q3, Viking Swap integrated the Velar SDK, while Velar integrated with the Orange Wallet. Velar later became the exclusive swap provider for the Xverse wallet via Velar Dharma and launched Velar Artha, the world’s first perpetual DEX on Bitcoin. They have since partnered with Hermetica to support USDh liquidity and collaborated with Bitlayer to strengthen Bitcoin L2 innovations.

Zest Protocol

Zest Protocol increased its TVL ~27.79% in Q3. Earlier this year, Zest raised $3.50 million, backed by Draper Associates, Binance Labs, and Trust Machines. Additionally, they launched the first money market on Stacks. Following this, they encountered a smart contract attack; however, they recovered and released a statement regarding security improvements. They recently (i) launched a BTC yield product, BTCz, in collaboration with Babylon, (ii) introduced the Clarity Alliance to improve Stacks’ security, and (iii) enabled stSTX borrowing.

Lisa Finance

Lisa Finance, a liquid staking project launched by ALEX in Q1 2024, grew its TVL by ~19.56% in Q3. Based on a commercially reasonable search, no protocol-specific developments occurred during this time.

DEX Volume

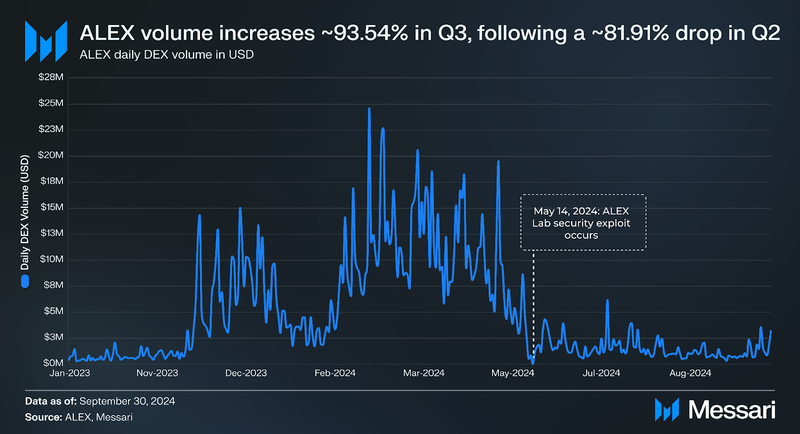

ALEX, a key DeFi protocol in the Stacks ecosystem — as displayed by its TVL dominance – offers decentralized trading and lending services. Despite its strong TVL metrics, the DEX showed significant volatility in its volume performance.

Specifically, the platform experienced an ~81.90% decline in total volume from Q1 to Q2, likely driven by the $4.30 million hack that occurred on May 14, 2024. Notably, the average daily DEX volume in Q2 was ~$6.24 million, with a peak high of ~$9.51 million on May 1, 2024.

In Q3 2024, ALEX displayed a recovery with a ~93.48% QoQ increase in total volume compared to Q2. The average daily DEX volume in Q3 was ~$1.38 million, a drop from the Q2 average, indicating that while there was a recovery, trading activity was still lower compared to the previous quarter.

Despite the sharp decline in Q2, the recovery in Q3 shows ALEX’s resilience. However, the platform is still far from reaching the heights seen earlier in the year, with overall DEX volume down ~64.98% from Q1 to Q3.

General Development and Growth

The development ecosystem experienced moderate growth from Q1 to Q2, with core developers increasing ~8.43% and ecosystem developers ~6.98%. However, this upward trend reversed in Q3, where core developers dropped ~23.33% and ecosystem developers declined ~28.26%. From Q1 to Q3, the number of core developers decreased ~16.87%, while ecosystem developers saw a larger overall drop of ~23.26%.

Despite this, various developments occurred, including:

- April:

- Ready Layer-2 Competition (RL2), where 30+ projects were submitted.

- The Stacks Foundation hosted the “Building on Bitcoin: Halving Edition” virtual event.

- Galxe integrated Stacks, boosting the builder network.

- The Stacks Foundation and LearnWeb3 partnered to help developers via the Stacks Developer Degree program.

- Yala collaborated with Stacks to boost liquidity within the DeFi ecosystem.

- May:

- Grayscale announced the Stacks Trust.

- The UpHold wallet integrated STX.

- The Bitcoin Layers pitch competition was hosted in Lisbon.

- The EasyA x Stacks Harvard hackathon was completed, with another scheduled for October.

- Axelar Network integrated Stacks.

- Stacks announced the critical bounties program.

- A 2nd round of the $50,000 Decentralized Grants (DeGrants) program was announced.

- June:

- Haruko integrated with Stacks to streamline the management of Stacks exposure for institutional investors.

- The EasyA x Stacks Consensus hackathon occurred.

- The Code for STX program was announced. Every month, a pool of 10,000 STX is available to all developers actively working on ecosystem projects.

- July:

- The Stacks Foundation introduced “Stacks Streets,” a gamified quest experience where individuals can try different Stacks applications.

- HypernativeLabs, an institutional-grade Web3 security platform, integrated Stacks, which now benefits from real-time threat detection and response platforms.

- Stacks announced an Asia Conference Tour.

- Hermitica Finance launched USDh, the first Bitcoin-backed, yield-bearing synthetic dollar protocol on Runes and Stacks.

- Xverse announced Sats Connect, a developer tool that integrates Bitcoin wallets, allowing users to directly mint and etch Runes.

- Trust Machines launched .locker, a digital identity and domain solution.

- August:

- “21 Days of Nakamoto” was announced to encourage community building.

- Degen Labs created stacking.tools for the three main ecosystem stakeholders.

- Binance added the STX-USDC trading pair.

- September:

- Grayscale Research announced their Q4 2024 Top 20, which included STX.

- Stacks announced a BTC Bash event for October.

- The Stacks Asia Foundation was launched to expand initiatives.

- Tokensoft partnered with Stacks to help ecosystem startups with legal efforts.

- The “Best and Brightest” campaign was launched to educate the community about leaders in space.

- Asigna lets users create a Stacks multi-sig directly via Ledger.

- Crypto.com began offering STX stacking to its customers.

- Anchorage began supporting custody for Stacks.

For more information, Stacksnacks releases monthly recaps of ecosystem developments.

Regulatory Developments

In 2017, Stacks (formerly Blockstack) faced regulatory scrutiny from the US Securities and Exchange Commission (SEC) regarding classifying STX as a security. The investigation began after Blockstack raised $70.00 million through a token sale, where a portion of it was conducted under the SEC’s Regulation A+, which allows issuers to sell limited amounts of securities to the public without requiring full registration. Other portions of the sale were conducted under exemptions for accredited investors (Reg D) and international investors (Reg S). The SEC deemed STX a security due to its sales under this framework. However, on July 12, 2024, the SEC concluded its three-year investigation into Hiro Systems and Stacks, not recommending any enforcement action against either entity.

Closing Summary

The broader crypto market experienced a decline in Q2 2024, and Stacks was not immune to this trend. In Q2, the circulating market cap of STX fell ~52.33% QoQ to ~$2.50 billion. However, by Q3, the network showed signs of recovery with an ~8.70% increase, bringing the circulating market cap to ~$2.75 billion – ranking it 29th overall. Despite these fluctuations, the network demonstrated resilience in key metrics, like stacking, which saw the total amount of stacked STX increase by ~16.90% in Q3. Metrics like revenue and total daily transactions also saw significant growth in anticipation of the Nakamoto upgrade, spiking ~519.78% and ~118.35%, respectively, by the end of Q3. Additionally, the TVL (STX) increased ~35.49% in Q3, indicating a steady recovery in native engagement and support within the ecosystem.

Notably, the Nakamoto upgrade and sBTC are steadily rolling out, improving transaction speed and security by reducing block times from minutes to seconds while also expanding Stacks’ cross-chain capabilities. Key initiatives, such as the integration with Aptos and Solana for sBTC and new DeFi features introduced by platforms like ALEX and Velar Protocol, further strengthened the ecosystem. Institutional interest in Stacks is also clearly shown with the launch of the Grayscale Stacks Trust.

{kind=link}