Key Insights

- Contango’s total open interest (OI) was 168,200 ETH in Q1, up 8% QoQ. Leverage on stablecoin pairs increased relative to ETH-related asset pairs.

- Total trading volume in Q1 was $1.2 billion, down 45% QoQ. Ethereum remained the leading chain by volume and grew to 69% volume share compared to 41% in Q4.

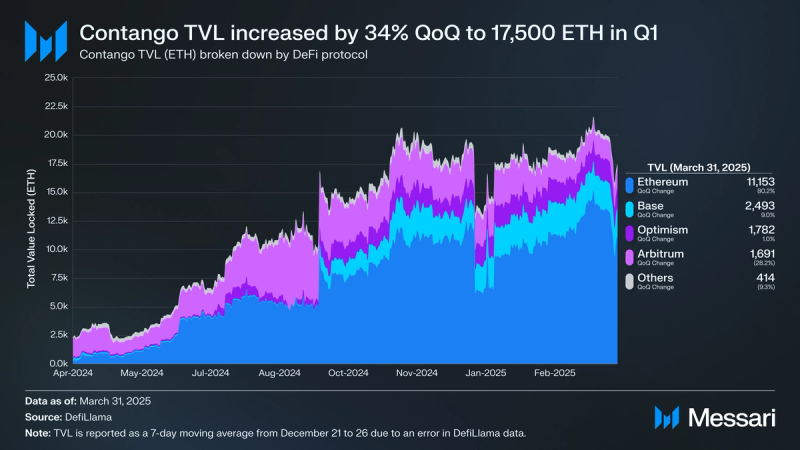

- Contango TVL increased by 34% QoQ to 17,500 ETH, though in USD, it decreased 54% QoQ to $31.7 million, amid a broader slowdown in crypto trading activity.

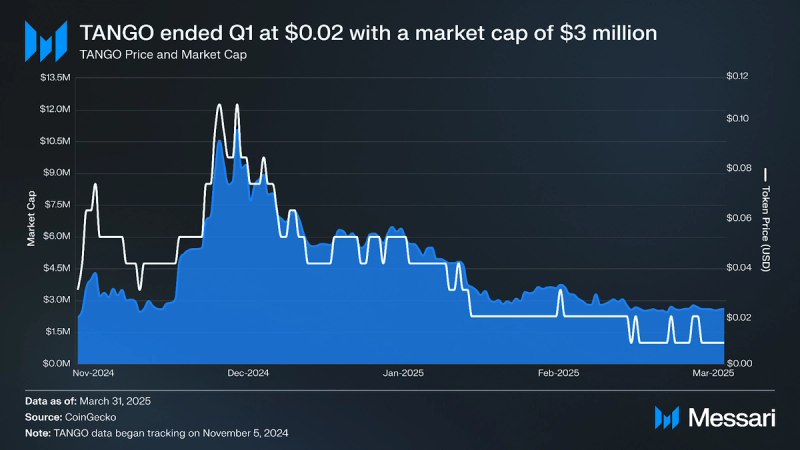

- TANGO traded at $0.02 at the end of Q1, with a $2.6 million market cap. 12% of oTANGO (22.3 million tokens) have been claimed, generating $1.7m in USDC proceeds for the Contango treasury.

Primer

Contango (TANGO) is a DeFi protocol that allows users to loop (recursively lend and borrow via money markets) various assets onchain, creating leveraged positions similar to perpetual contracts but with lower funding costs. It enables trading by building positions on top of spot and money markets, thus aggregating liquidity from both markets and facilitating large trades with minimal impact on rates and prices. Contango supports trading on multiple chains and markets, including ten chains, 12 money markets, and more than 250 trading pairs. Contango launched its native token, TANGO, in November 2024. TANGO stakers earn 100% of Contango’s protocol fees.

Contango accommodates various types of users, providing distinct interfaces for different needs. Loopers can automate their recursive lending and borrowing strategies, while advanced traders can use the professional trade interface to take directional bets. Users can also farm yields and rewards from LSTs, LRTs, and stablecoin pairs, or arbitrage rate differentials. With its comprehensive looping capabilities and UX, Contango positions itself as a leading looping layer in DeFi.

Key Metrics

Analysis

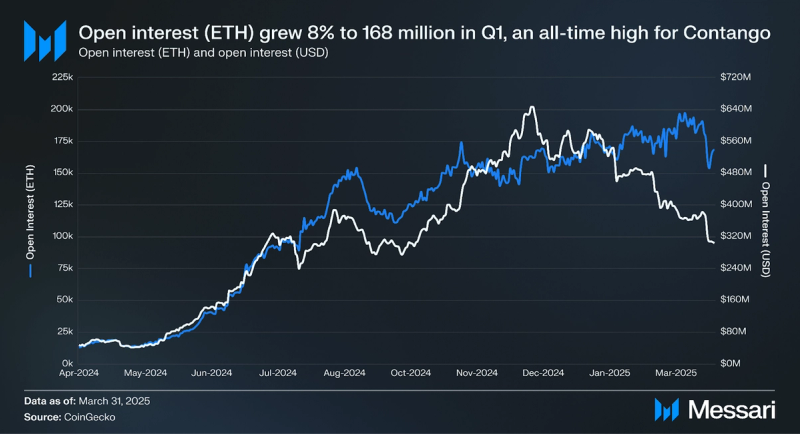

Open interest (OI) denominated in ETH grew 8% Q1 to 168.2 million, an all-time high for Contango. Conversely, OI denominated in USD declined 24% QoQ to $303.6 million due to ETH 45% price decline in Q1. Though dollar value fluctuates with ETH price, ETH-denominated open interest has steadily risen since the protocol launched.

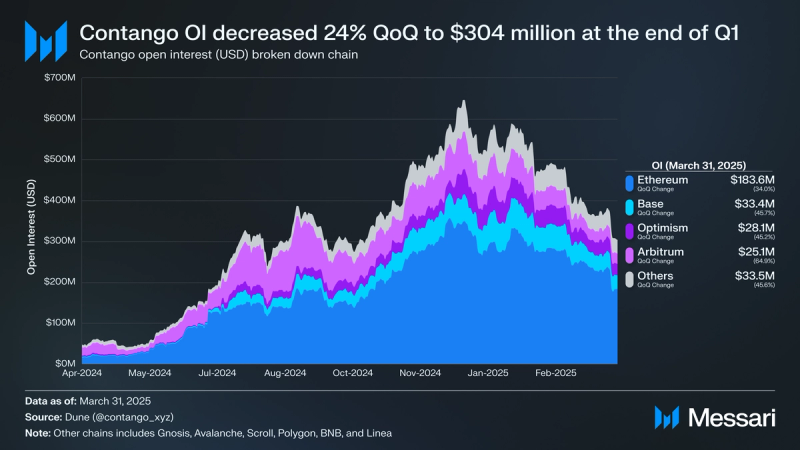

Ethereum remained the leading chain by OI with $183.6 million, a 34% increase QoQ. Ethereum comprised 61% of Contango’s total OI and has remained the dominant chain for open interest since June 2024. weETH pairs from ether.fi and wstETH pairs from Lido have historically had the highest open interest on Ethereum. Stablecoin leverage increased in Q1, possibly due to major’s (BTC, ETH, SOL) price depreciation and new listings of srUSD, stUSR, and other yield-bearing stablecoins.

OI on Base grew 663% QoQ to $33.4 million due to the increased popularity of wstETH/ETH, weETH/ETH, and Pendle PT pairs on MorphoBlue. Optimism experienced the highest OI growth, up 710% QoQ to $28.1 million, due to wstETH/ETH on Aave and rETH on Aave and Compound (Compound III is commonly referred to as Comet). Grants from Optimism to Contango and Compound boosted open interest. OI on Arbitrum decreased 51% QoQ to $25.1 million—8% of total OI. The leading pairs on Arbitrum were weETH/ETH on Aave V3 and wsETH/ETH on Aave V3 and Fluid.

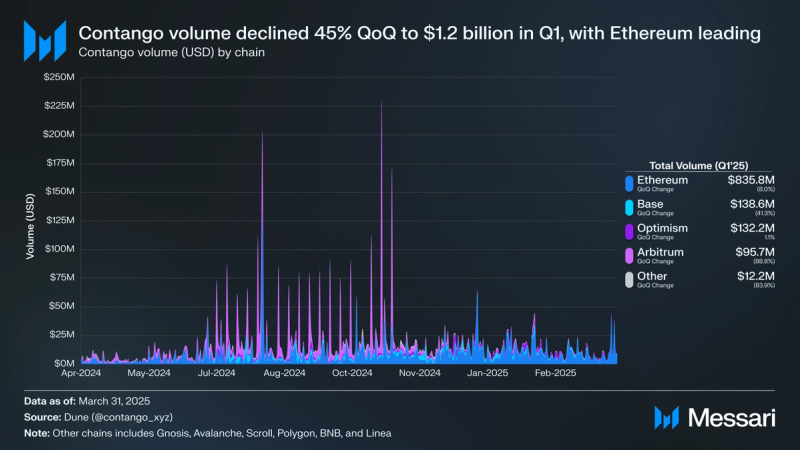

Total trading volume routed through Contango declined 45% QoQ to $1.2 billion amid a broader slowdown in crypto trading activity. Despite volume on Ethereum decreasing 8% QoQ to $835.8 million, Ethereum’s market share of volume rose to 69% from 41% in Q1. The top traded pair was weETH/ETH, with $199.3 million volume, down 14% QoQ. The rising popularity of stablecoin pairs like srUSD/rUSD ($89.0 million volume, up 2,182% QoQ) and sUSDe/USDC ($68.1 million volume, up 15% QoQ) also drove activity on Ethereum in Q1.

Volume on Base, the second most popular chain by volume, fell 41% in Q1 to $138.6 million (-84% QoQ). The top traded pairs on Base were wstETH/ETH ($41.2 million volume, up 2% QoQ) and PT-LBTC-27MAR2025/LBTC, a new pair with $30.0 million volume. Optimism was the third most popular chain by volume, with $132.2 million (+1% QoQ). The top traded pairs were wstETH/ETH with $65.0 million volume (-71% QoQ) and rETH/ETH with $38.0 million volume (+126% QoQ).

Arbitrum’s volume fell 89% in Q1 to $95.6 million, accounting for 8% of Contango’s total volume in Q1. The remaining chains combined for a total quarterly trading volume of $12.3 million, an 84% decrease QoQ.

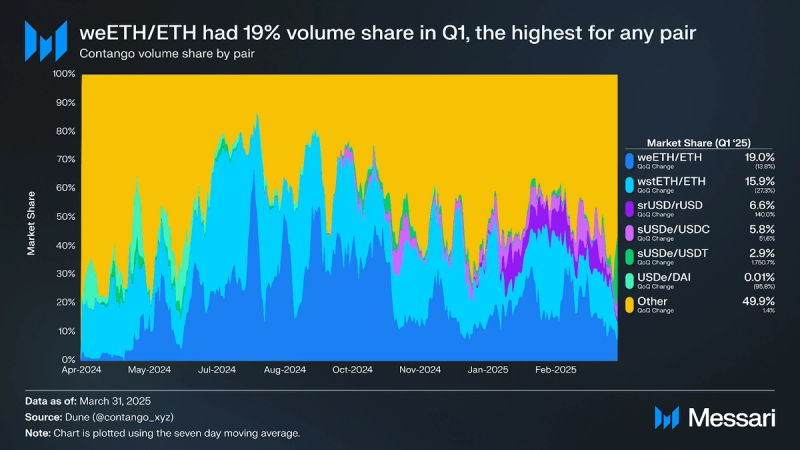

weETH/ETH was the most popular pair on Contango, with $272.9 million in total volume during Q1, a 71% decline QoQ. wstETH/ETH was the second most popular pair with $182.4 million in total volume, a 51% QoQ increase. weETH/ETH held a 19% volume share, whereas wstETH/ETH held a 16% average volume share. Stablecoin volume (i.e., USDC, USDT, DAI, sUSDe, EURC) decreased 11% QoQ to $449.6 million, displaying relative strength against ETH-denominated pairs.

Copilot Insights: How does Pendle PT work?

Additionally, Contango has established itself as a popular venue for trading Pendle PT tokens on leverage, with $279.5 million in total volume in Q1, a 9% increase QoQ. PT trading is most popular on Morpho on Ethereum, with $206.8 million volume in Q1 (+143% QoQ).

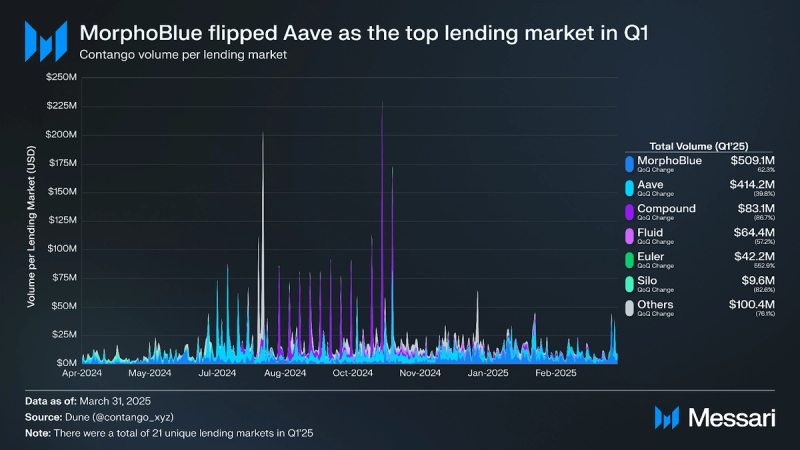

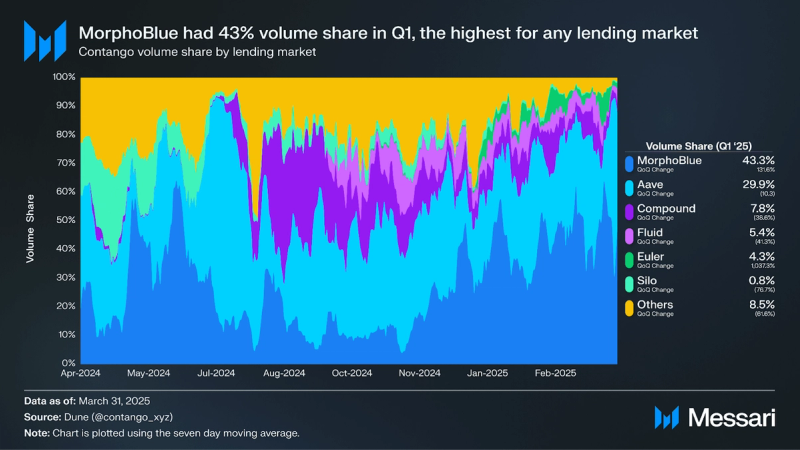

In Q1 2025, Contango supported 12 lending markets across ten EVM chains. MorphoBlue flipped Aave in volume routed through Contango for the first time and grew 62% to $509.1 million. This was mainly due to increased wstETH/ETH and weETH/ETH volume on Morpho. Contango was the leading front-end for Morpho on Base in Q1.

Aave usage decreased 40% QoQ to $414.2 million, primarily due to the decline in wstETH/ETH trading. Compound, the third most popular money market by lending/borrowing volume, saw an 87% decrease QoQ to $83.1 million. Euler grew 553% to $42.2 million, primarily due to the popularity of Usual’s new USD0++/USDC pair ($12.4 million volume) and wstETH/ETH trading ($7.2 million volume, up 2,104% QoQ).

MorphoBlue’s volume share increased 132% QoQ to 43%, the highest of any lending market in Q1. Aave, the largest lending market by volume share in previous quarters, declined 10% QoQ to 30% volume share. Euler, the largest gainer in Q1, held a 4% volume share, a 1,037% increase QoQ.

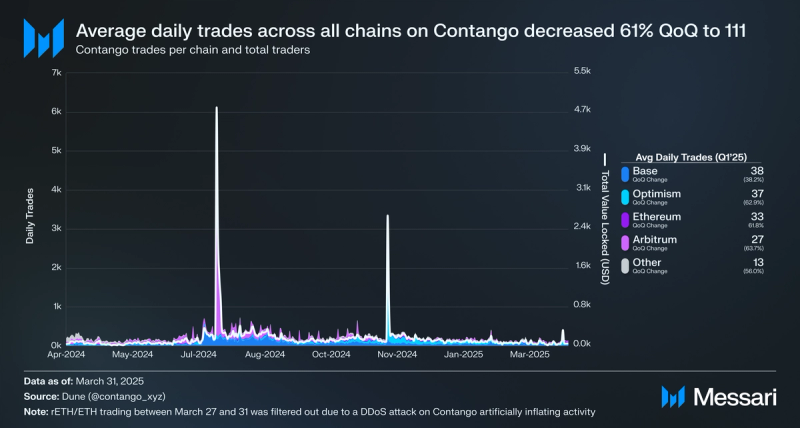

Average daily total trades decreased by 22% QoQ to 223, and average daily traders decreased by 16% QoQ to 154. Activity spiked on March 27 across all chains. A couple of events may have been responsible for this spike. The Hyperliquid $JELLY exploit on March 26 may have driven Hyperliquid users to other perp DEXs. Alternatively, Gamestop announced on March 27 that they would raise $1.3 billion to purchase BTC.

Optimism remained the most popular network by average daily trades, likely due to a 12-week incentive program to give away 100,000 OP tokens in Q1 2025. Base was the second most active network, with 39 average daily trades, a 38% decrease QoQ, followed by Ethereum, which grew 59% QoQ to 34 average daily trades.

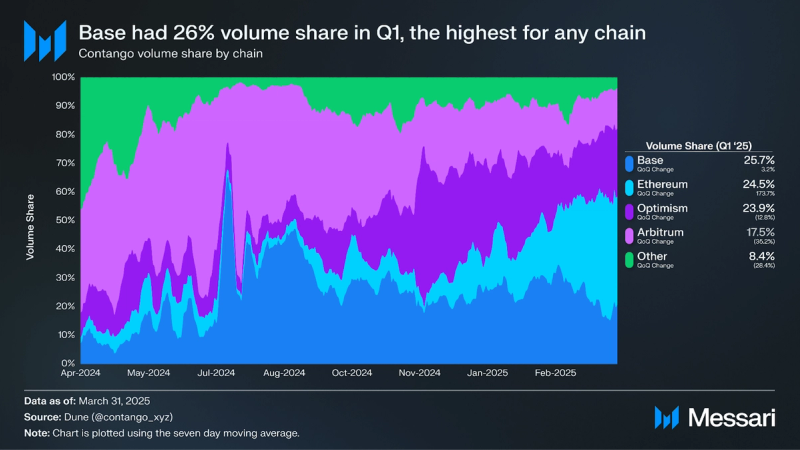

Base held the highest volume share for trading activity in Q1 at 26%, a 3% increase QoQ. Ethereum’s volume share increased by 174% QoQ to 25%. There is no notable reason, although a reduction in gas fees could have made trading more accessible. Activity on Optimism spiked in November following Contango’s announcement that they would give away 100,000 OP tokens worth $176,000 at the end of Q4. Arbitrum declined 35% QoQ to an 18% market share.

Contango’s TVL increased by 34% QoQ to 17,500 ETH, mainly due to ETH’s price depreciation (-45% QoQ). TVL in USD-denominated terms decreased 54% QoQ to $31.7 million. Ethereum remained the TVL leader with 11,200 ETH, an 80% decrease QoQ. Base and Optimism flipped Arbitrum as the second and third highest chain by TVL, with 2,500 and 1,800 ETH, respectively. Arbitrum’s TVL decreased by 25% QoQ to 1,700 ETH.

TANGO Token

Contango launched its native token, TANGO, through a curated fixed-price presale on Fjord between October 21 and October 28, 2024. The presale raised $3 million at a $45 million FDV ($0.045 per TANGO token) and sold out in under 4 hours.

TANGO’s circulating market cap decreased 54% QoQ to $2.6 billion. Likewise, TANGO’s price fell 54% QoQ.

Copilot Insights: How does the oTANGO mechanism work?

Copilot Insights: How does the oTANGO mechanism work?

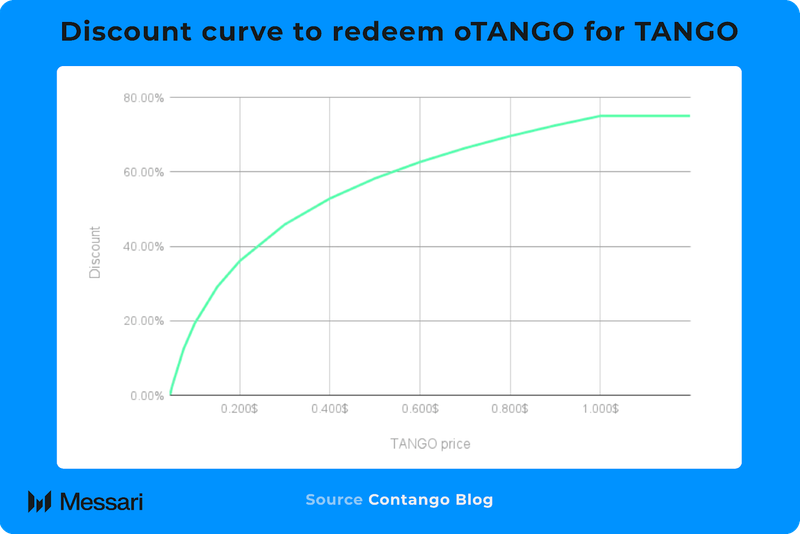

An airdrop was conducted for early users alongside the presale on Fjord. The airdrop leveraged the oTANGO mechanism, which offered TANGO options at a discount. To protect Contango’s seed valuation and buyers at the Fjord pre-sale, the oTANGO mechanism sets a 0% discount when TANGO is $0.045 (FDV $45.0M). Below $0.045, the redemption price stays fixed; above, a discount of up to 75% applies at $1 or higher, incentivizing holding for price appreciation. TANGO became claimable on November 4 and oTANGO became redeemable on November 25. By the end of Q1, only 12% of the oTANGO supply—22.5 million tokens—had been exercised at discounts ranging from 2% to 23%, generating $1.7m in USDC proceeds for the treasury. Many oTANGO tokenholders may be waiting to redeem their tokens, expecting a discount driven by potential price appreciation.

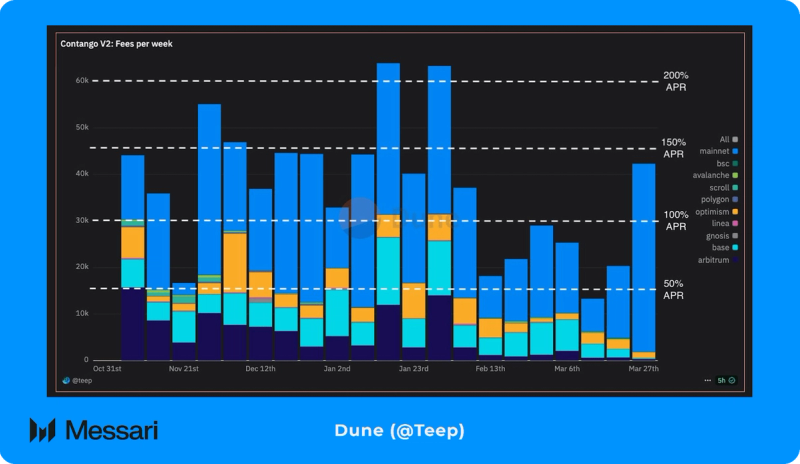

Contango enabled fees in Q4, leading to higher APRs for TANGO stakers since 100% of token fees go directly to stakers. Contango’s smart contracts are free to use, but trading via the app carries a 0.05% fee for correlated pairs (e.g., weETH/ETH) and a 0.25% fee for non-correlated pairs (e.g., weETH/USDC). Staking APR is paid out to stakers in a basket of blue-chip assets that includes ETH, WBTC, USDC.

Closing Summary

In Q1, Contango showed varied performance across its metrics. Total open interest declined 3% to $303.6 million, while trading volume declined $1.2 billion, with Ethereum holding a 69% volume share. TVL rose 34% to 17,500 ETH, though TVL declined 54% to $31.7 million in USD terms due to ETH’s 45% QoQ decline. Stablecoin open interest rose, and stablecoin pairs traded more frequently relative to ETH pairs. Optimism also saw increased activity due to a 100,000 OP token incentive program. While overall metrics in USD terms declined in sync with the market, the same cannot be said for ETH terms.

Launched in November 2024, the TANGO token closed Q1 at $0.02, with a $2.6 million market cap, while the oTANGO mechanism facilitated airdrops with a discount structure tied to token price. These efforts to enhance the protocol’s functionality bode well for its future utility regardless of market conditions.

{kind=link}