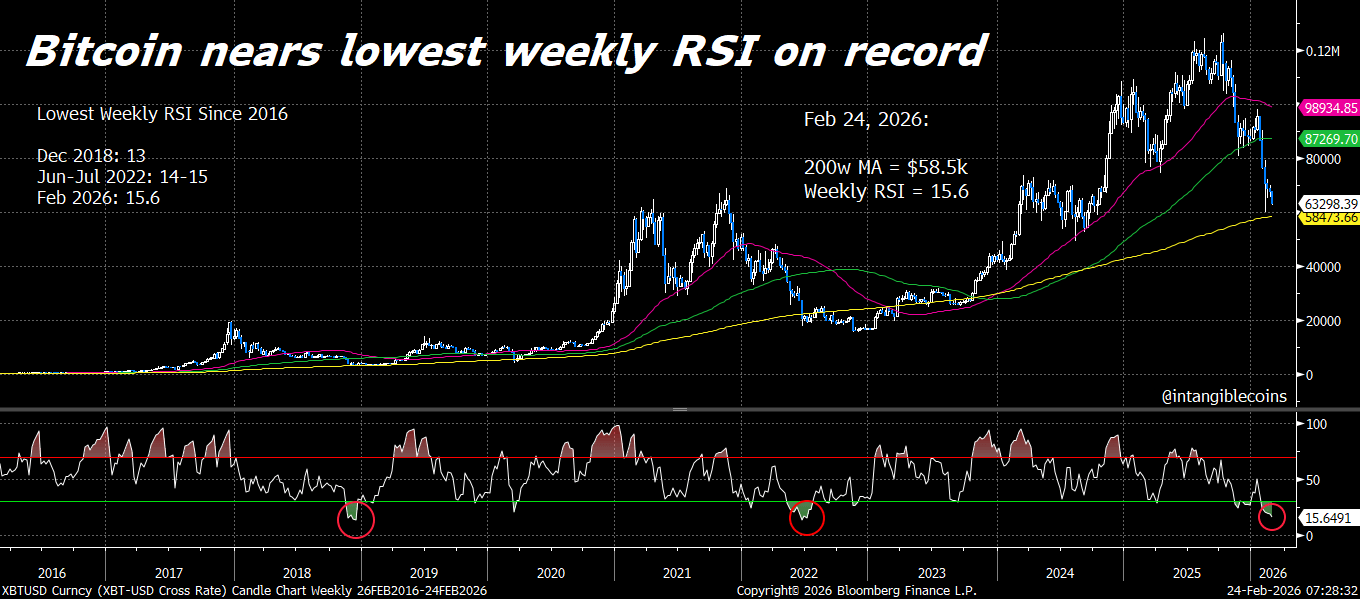

Bitcoin is flashing its most oversold signal on record amid its continued price struggles in this current macroeconomic environment and persistent exchange-traded fund (ETF) outflows.

According to CryptoSlate data, BTC’s price dipped to around $62,700 over the last 24 hours, while its weekly relative strength index (RSI) printed roughly 25.7. BTC has risen to above $66,000 as of press time.

Alex Thorn, Galaxy Digital’s head of research, pointed out that this weekly RSI is “lower than any time except the darkest of bears.”

Thorn also noted that the only lower readings since 2016 were in November and December 2018, when BTC price dropped from $6,000 to $3,000, and in June and July 2022, when crypto lending firms Genesis and Three Arrows Capital collapsed.

As a result, market observers have described the current setup as “full capitulation,” arguing that similar RSI extremes have historically been followed by long, messy recoveries rather than instant reversals.

Capitulation signals are flashing, but Bitcoin may still be in the base-building phase

Momentum has reached an extreme, but Bitcoin’s price discovery still appears to be driven by forced selling, fund de-risking, and the transfer of inventory from weaker holders to larger buyers.

That distinction matters because oversold conditions do not automatically mark a bottom. They often emerge when selling becomes mechanical rather than emotional.

In that setup, liquidations, risk reductions, and thinner liquidity can keep a market pinned in a weak momentum regime even after the initial panic phase begins to fade.

Glassnode data supports that reading. The firm’s 90-day realized profit-and-loss ratio for Bitcoin has fallen below 1, a threshold it describes as an “excess loss-realization” regime.

In practical terms, realized losses are dominating the tape, which suggests sellers remain the marginal price-setters.

CryptoQuant is describing the same period as the deepest pain phase of the current drawdown.

The firm says on-chain investors are posting their largest realized losses on record, while active traders are absorbing the biggest losses of this cycle. In its view, that stress has already changed who is participating in the market.

Its interpretation is that retail holders have largely capitulated, while whales continue to accumulate at a greater intensity.

That pattern, weaker hands exiting while larger holders absorb supply, is often seen in later-stage corrections when a market starts building a base.

CryptoQuant also frames the move as a correction rather than a full bear market, comparing the scale of realized losses to November 2019, when Bitcoin later moved higher.

That comparison is best treated as an analog rather than a forecast, but it reinforces the idea that deep realized losses can coincide with longer-term opportunity.

This is where many RSI-based headlines miss the nuance. A record-low RSI can signal that capitulation is underway, and capitulation is often a precondition for a bottom.

However, it does not, on its own, confirm that the market has finished searching for a durable bid.

That helps explain why extreme RSI readings are often followed by choppy, range-bound trading instead of a V-shaped rebound. If the market is still processing heavy realized losses, buyers tend to demand discounts, while trapped holders may sell into rallies to reduce exposure.

In that framing, RSI extremes are often better understood as a phase shift, from capitulation toward base-building, rather than a precise turning point.

Alphractal’s Sharpe Ratio analysis points in a similar direction, but through a different lens.

While CryptoQuant focuses on on-chain loss realization and holder behavior, Alphractal looks at risk-adjusted returns across the broader cycle. Its data suggest Bitcoin is in an advanced stage of a repair process, with the risk-versus-return profile more compressed than it was a year ago.

The firm argues that allocating to BTC at current levels implies lower expected returns over the coming months, but also lower relative risk than earlier in the decline.

Historically, even lower Sharpe Ratio readings have aligned with major bottoming phases, when the market’s risk-return profile becomes most compressed and long-term asymmetry begins to improve.

Alphractal’s point is that Bitcoin may be getting close to that zone, but may not be there yet.

Taken together, the signals describe a market under severe momentum stress, with realized losses still being absorbed and risk-adjusted returns increasingly compressed.

That is consistent with a late-stage repair phase. It is a constructive setup for base formation, but not definitive proof that the repair is complete.

The missing institutional bid, ETFs leak billions, and liquidity is thin

What distinguishes this pullback from earlier ones is that one of Bitcoin’s most visible demand channels has started to fade.

Data from SoSo Value shows US spot Bitcoin ETFs have recorded more than $4.5 billion in net outflows across the 12 funds since the start of the year, extending a five-week redemption streak.

In prior drawdowns, the ETF complex often functioned as a steady marginal buyer. However, that flow has flipped this year, with capital leaving the wrapper as prices weaken.

The impact has been more pronounced because market depth is thinner than it was during earlier selloffs.

Coin Metrics said the average spot Bitcoin order book depth, measured within plus or minus 2% of the mid-price, fell from roughly $40 million to $50 million between August and October 2025, then thinned further to $15 million to $25 million, and then thinned further in February.

In a shallower order book, sell pressure tends to move price more aggressively, creating air pockets and sharper downside gaps even in the absence of a fresh catalyst.

Coin Metrics also pointed to slower stablecoin growth. Aggregate supply for USDT and USDC has been hovering around $260 billion, indicating the market is not seeing a strong wave of new liquidity at a time when Bitcoin is trying to establish a floor.

That pattern suggests stagnation in fresh inflows rather than a broad-based exit from crypto, but the distinction offers limited near-term support when other demand sources are already weakening.

CryptoQuant’s derivatives data adds to the defensive picture.

The firm said bears remain in control of Bitcoin futures, with funding rates in negative territory around the current bottom zone of roughly $62,000 to $68,000. That is a notable shift from the earlier bottom near $80,000, when funding stayed positive for most of the period.

CryptoQuant also said selling has been the dominant force since July 2025, with buy limit orders largely acting as passive absorbers rather than active drivers of price. It added that the current selling pressure is the strongest in three months.

None of that rules out a rebound. Negative funding can create conditions for a short squeeze if bearish positioning becomes crowded and spot selling starts to fade.

But for now, the structure still points to a market trading defensively rather than one showing clear signs of renewed risk appetite.

Options markets have reflected the same caution.

CryptoSlate previously reported that demand for downside protection stayed elevated even after Bitcoin rebounded above $70,000 on Feb. 6, with traders concentrated in $60,000 to $50,000 put strikes ahead of the Feb. 27 expiry.

When put demand remains firm after a bounce, it usually signals that traders still assign meaningful odds to further downside, even if dip buyers are active in spot.

The post Bitcoin reveals a rare bullish cycle bottom signal before bouncing as futures bears tighten their grip appeared first on CryptoSlate.

{kind=link}